3D_generator/iStock via Getty Images

Crown Crafts, Inc. (NASDAQ:CRWS) has an inventory problem. The company’s inventory on hand is up ~45% compared to last year and its largest customers have already reported holding too much product. Crown Craft is also experiencing slowing sales which will exacerbate the problem. While the company’s balance sheet and long-term vitality are not in jeopardy, the coming quarters present a challenge for management and will likely weigh on the stock price. Therefore, CRWS maintains a Hold rating until sales stabilize and the company works through its inventory surplus.

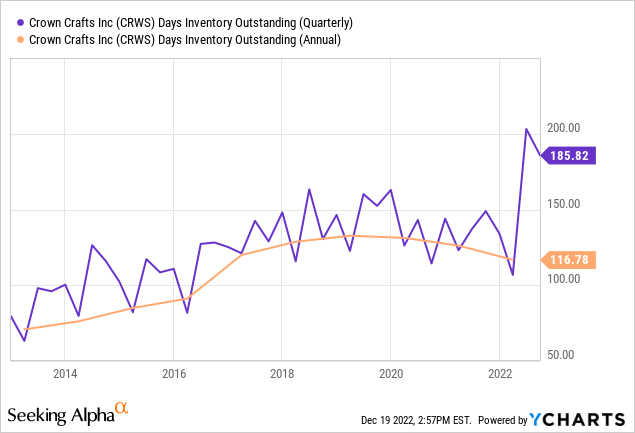

Inventory Glut

At the end of Q2’FY23, Crown Craft had ~186 days of inventory on hand, up significantly from previous quarters:

Here is what management said regarding the glut:

After experiencing empty shelves during the 2021 holiday season due to port congestion, retailers responded by building up their inventory levels during the first calendar quarter of 2022, resulting in an over-inventory situation by late spring. This situation has been exacerbated by a change in consumer buying patterns whereby many consumers are now trading down to lower-priced items, buying fewer items or foregoing some items altogether due to the inflationary concerns.

This is probably the worst time for Crown Crafts to have an oversupply of inventory. It has been reported that the company’s major customers (i.e., Walmart, Amazon, and Target) are eager to clear inventory glut, but, despite heavy discounting, inventory levels could continue to plague retailers in 1H’23. The company’s sales have slowed materially in 1H (down 11.5%), and will likely remain depressed through the balance of the year. These factors combined present a significant headwind for Crown Craft in Q3 and Q4.

The company’s excess inventory will impact the company’s earnings in 2H. This is because Crown Craft will likely have to rely on discounting to move product. Management has stated, “in order to move some inventory to make room for some new programs, [the company] may need to provide higher-than-normal discounts to retailers.” The goal is to have inventory closer to a normal level by end of the fiscal year. If management cannot clear the surplus, a write down might be in order. Therefore, the next several quarters are not promising for Crown Craft’s P/L.

Reduced earnings will have a material impact on Crown Craft’s market valuation. The company has historically traded at an average ~11.5x TTM earnings. Currently, it trades at ~6.5x, suggesting the company is undervalued. However, inventory overhang and slowing sales have yet to be fully realized into the company’s valuation. With earnings expected to come down in 2H, it is best to hold or avoid Crown Crafts until the dust settles.

With that said, Crown Crafts remains a solidly profitable company with a strong position in a niche product category. Management noted thus far during this downturn it has maintained overall shelf space at retailers and partnerships remain strong. Additionally, the company’s balance sheet is attractive with zero debt and ample access to capital if needed. The dividend policy, currently at 32¢/per annum, has been stable for years, and the company generates adequate cash to maintain its policy through an economic recession. Therefore, Crown Crafts will stay on the radar until a more attractive valuation avails itself.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment