sutthirat sutthisumdang

Introduction

I’ve been long CrowdStrike (NASDAQ:CRWD) for roughly a year, layering into the stock as it kept falling back throughout 2022, having added as high as $209.54 á share, and as low as $114.16 á share. Those reading my prior articles concerning CrowdStrike, will have seen me dissect the company, each time coming to the conclusion, that operationally and strategically, this company delivers strong results quarter after quarter, while coming with a lofty valuation that required dollar cost averaging and acceptance, that this is a play requiring the long-term perspective.

In this article, I’ll review the headline arguments for and against, to refresh my perspective on where this company is in its timeline with respect to the overall market. This is also necessary, as the bear case has developed strongly throughout 2022 due to the strong response by the FED, altering how we price assets.

The Bear Case Perspective

Some powerful themes are at play on the bear side of this case. Structural changes as to how the market is willing to value companies such as CrowdStrike can weigh heavy on the company, and ensure that investors who bought at the peak may have to wait a very long to ever see that peak again.

Similarly, investors who bought Cisco (CSCO) at the dot.com mania when the stock reached as high as $80 per share in the beginning of this millennium, are nowhere near to having seen that money returned. At least not if you exclude dividends. There is, in my opinion, a fair chance that investors with some of these growth names will suffer a similar fate looking back at the Covid-19 induced valuation levels in a decade or two.

Bear Case Argument # 1 – The Reintroduction Of Positive Interest Rate Levels:

Having found ourselves in a decade of zero percent interest rates, it has become possible for market participants to price companies at unbelievable levels as the reliance on future income is less of a pickle when there are no interest rates to hollow the future earnings.

What we know today is that many developed economies can’t tolerate high interest rate levels, as their current fiscal debt burdens would make that unsavvy in the mid- to long-term as it would crush their national finances. Just as zombie like companies are allowed to live during zero interest rate like conditions, nations aren’t incentivised to seek the path of economic reform in a time where debt isn’t a concern. One way out of this pickle is to inflate our way out of the debt, and ultimately, we don’t know where interest rates will land. However, we do know, that interest rates at zero, was never a healthy diet for our economies, as it causes less clever allocation of capital as a side effect, allowing companies to live longer than they should, nations to ignore the fiscal bear trap straight ahead as well as markets to price assets at prices ignoring gravity. It’s doubtful if we’ll ever get to experience such a prolonged period again, and in fact, we shouldn’t strive for it, as it ultimately isn’t healthy for the market economy.

If that turns out to be the case, it will reduce the markets willingness to provide companies with lofty valuations, particularly those where earnings aren’t fully established and where the company isn’t GAAP profitable. This argument finally arrived at a point of relevance for CrowdStrike, as the company still isn’t GAAP profitable.

Bear Case Argument #2 – CrowdStrike’s Massive Growth Days Are Over:

As has been the custom in recent years, CrowdStrike delivered a performance ahead of guidance in Q3-2023. Unfortunately, that doesn’t matter much, as the market constantly occupies itself with what happens six months down the line, and not what happened yesterday. Therefore, what matters here is that management delivered a weak guidance, which caused the stock to crash intraday.

In the words of CEO, George Kurtz

“However, I would first like to address the increased macroeconomic headwinds we saw in the quarter, which caused Q3 net new ARR to come in below our expectations. As we discussed on our last earnings call, organizations were starting to respond to macroeconomic conditions by adding extra layers of required approvals and extending the time it took to close some deals.

As Q3 progressed and fears of a recession grew, this dynamic became more pronounced. In our smaller, more transactional non-enterprise accounts, we saw customers increasingly delay purchasing decisions with average days to close lengthening by approximately 11% and net new ARR contribution decreasing $15 million from Q2. This also impacted our net new logo additions in the quarter, even though our quarter-over-quarter POV win rates increased meaningfully over more complex vendors that require more headcount to manage. While sales cycles lengthen, we believe the vast majority of these deals are not lost, just delayed.

In the enterprise, sales cycles or average days to close remain consistent with last quarter’s modestly higher level. In Q3, these larger customers continue to prioritize their CrowdStrike investments, but some also had to manage timing issues related to OpEx budgets and cash flow amidst the rapidly evolving macro.

To achieve this, some customers signed contracts that have multi-phase subscription start dates, which pushes their expense and CrowdStrike’s ARR recognition into future quarters. While every quarter, we have some deals with multiphase subscription start dates, in comparison to last quarter, in Q3, we saw approximately $10 million more ARR deferred into future quarters. We expect these macro headwinds to persist through Q4.”

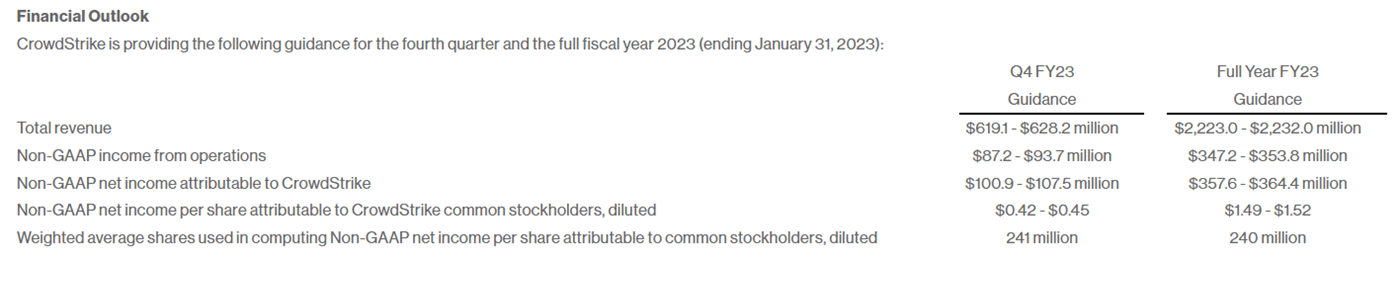

Full Year 2023 CrowdStrike Outlook (CrowdStrike Investors Page)

I’ve said it before in my previous articles – this is a market where no leniency is shown if you don’t live up to the growth expectations upheld by Wall Street. There is no room for error as a weak guidance will cause the investor community to conclude that it also carries over into the longer-term outlook for an individual company.

Perhaps the best example here is in the wording of the CEO who says that deals aren’t lost, they are simply expected to be postponed. A bear might argue that the CEO is slowly putting himself into a position, where he can ultimately disappoint the market by saying the management team overstated the growth potential within the industry of cybersecurity, and that deals in fact are lost and not simply postponed. We don’t know, but that uncertainty is what makes its way into the longer team outlook.

With a forward revenue guidance for Q4-2023 in the range of $619.1 to $628.2 million, it wasn’t far off Wall Street’s estimate of $634.2 million, but that’s not the essence as I just laid out in the section prior.

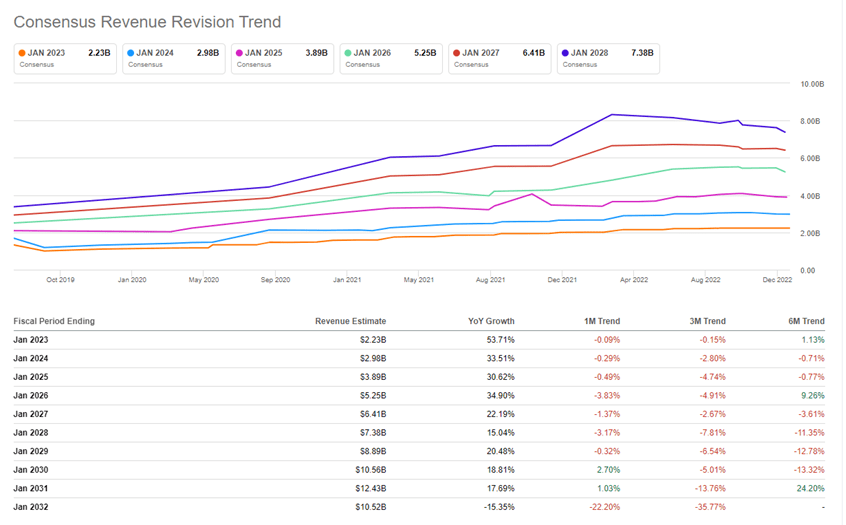

CrowdStrike Revenue Revisions (Seeking Alpha)

The uncertainty related to management’s own forward-looking expectations also spill over into the consensus estimates, where CrowdStrike has suffered twice as many downward revisions of revenue as opposed to upwards revisions in the last quarter.

Remember, today, the market isn’t even expectating a harsh recession, so imagine what happens to these forward estimates in that scenario.

Bear Case Argument #3– The Valuation:

If interest rates aren’t returning to zero, and the growth outlook is slowing, also impacting CrowdStrike’s path to becoming GAAP positive, then where does that leave the valuation?

Answer: Between a rock and a hard place

But the price is more than 65% off its most recent high and has only been so once since its IPO, doesn’t that constitute an automatic buy? No it doesn’t.

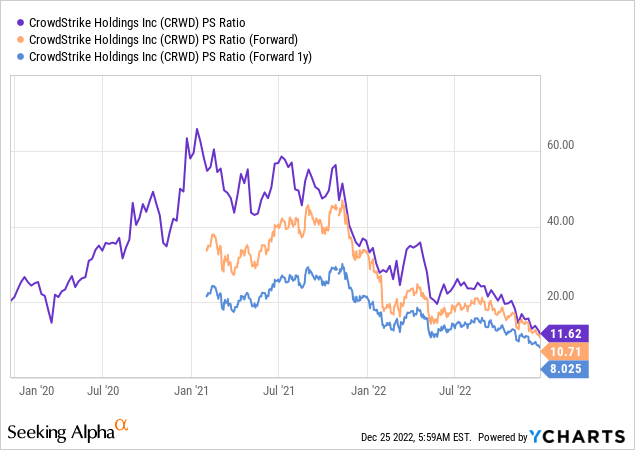

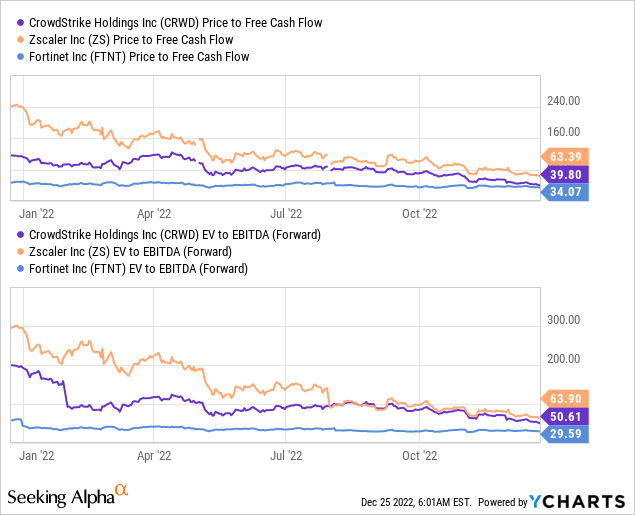

CrowdStrike was never a cheap company, bulls would argue that was the situation on the premise of strong performance. However, it quickly becomes difficult to argue exactly what valuation a strong performance can justify. That’s relative and doesn’t carry a definitive answer. All we say is that relatively few companies are allowed to be priced with a P/S ratio in excess of 10 for longer periods, especially for companies who are still working towards their target operating model.

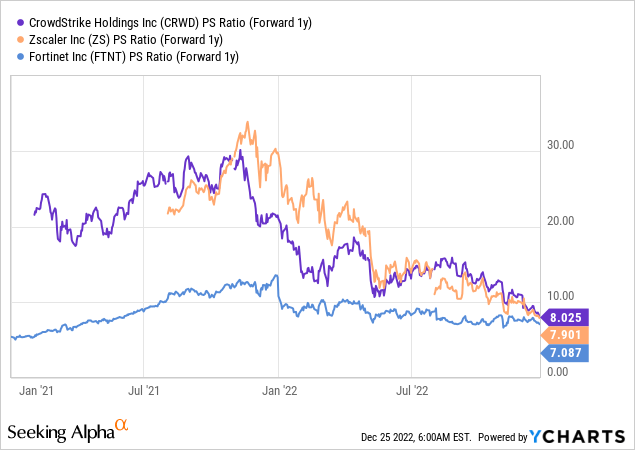

In fact, comparing CrowdStrike to two of its competitors, Zscaler (ZS) and Fortinet (FTNT), it gets gloomier, at least in terms of Fortinet who is already profitable, even on a GAAP basis, and has been so for a very long time. In addition, Fortinet is a substantially larger company with TTM revenue of $4.1 billion compared to CrowdStrike’s TTM revenue of $2.0 billion. Naturally, Fortinet is growing at a slower pace, but also coming off a much larger revenue base, meaning that by 2028, Fortinet’s revenue is still expected to be well ahead of CrowdStrike. Are these two companies identical? No they aren’t, but it’s one of the closer proxies available to gauge CrowdStrike’s valuation relative to something relevant.

Comparing the three companies across several valuation metrics, and we obtain a somewhat similar picture with Zscaler and CrowdStrike being provided with a higher multiple. Is this sustainable, a bear might ask.

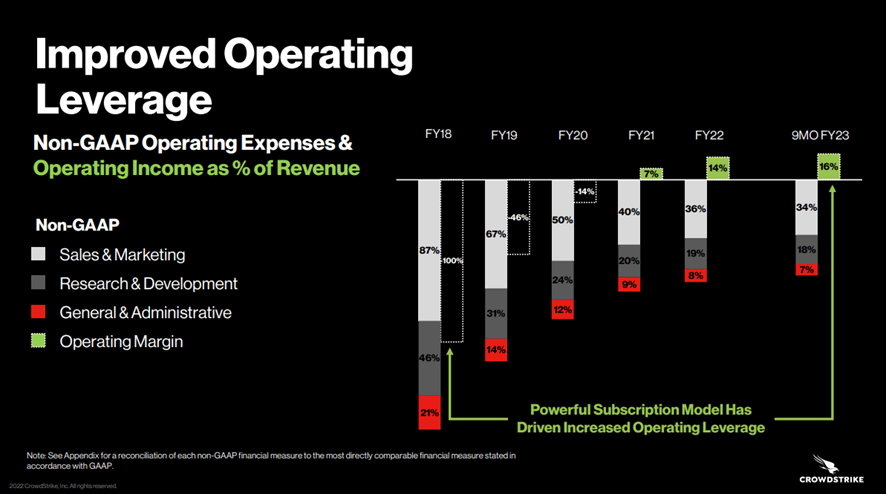

CrowdStrike Operating Leverage (CrowdStrike Investors Page)

One aspect that will impact the valuation, is CrowdStrike’s path towards becoming GAAP positive, and an aspect where a bear might argue management has more to lose than to gain at this point in time, because being on path is fine, but having to communicate that shareholders have to await GAAP profitability, could come with severe punishment from a valuation standpoint.

The Bull Case Perspective

Similarly, to the bear case perspective, strong forces are at play from the bull case side of the argument. However, those arguments revolve mainly around the industry, as well as expectations tied to the company itself.

Bull Case Argument #1– Industry Growth Is In Its Early Innings:

We all understand the concept of insurance, and it’s basically the same idea surrounding CrowdStrike’s offerings. In a world where the number of PC and internet endpoints are ever growing, how can any respectable company conduct its operations without proper state-of-the-art cybersecurity? That would be a natural question asked by a cybersecurity bull. This is an industry undergoing immense growth over the coming decades. Here, Fortune Business Insights argue that cybersecurity as a marketplace, will experience 13.4% CAGR until 2029, a growth level well in excess of general GDP, suggesting we have an industry undergoing supernormal growth. Looking beyond 2030 is a very complex task, but it’s perhaps a fair assumption that cybersecurity won’t become less relevant as time passes.

This is on the basis that whatever large cap companies have to pay for cybersecurity, dwarfs in comparison to the potential costs associated to a large security breach rendering one’s operations out of function for hours, days or longer. Global shipping company A. P. Møller – Mærsk A/S (OTCPK:AMKBY), a $40 billion market cap company suffered a major breach in 2017, that ended up costing the company in excess of $200-$300 million from lost operational uptime, while perhaps also causing customers to look elsewhere to ensure their goods wouldn’t face a potential delay. Moreso, these incidents also potentially cause brand damage e.g., in instances where customers and clients private data is leaked as a result, so there is plenty of reason for the board of directors for any given company to consider carefully, before scrapping the idea of applying cybersecurity infrastructure to one’s company.

Going back to summer of 2022, and CrowdStrike’s CEO argued in their earnings call, that they weren’t experiencing receding demand for their services, as cybersecurity remained a top priority amongst board of directors. This would be a logical conclusion, also seen from my standpoint given the potential downside associated to a breach, but as we saw in the most recent earnings call, we can’t be entirely certain that cybersecurity will be the last cost to get cut in an uncertain economic environment.

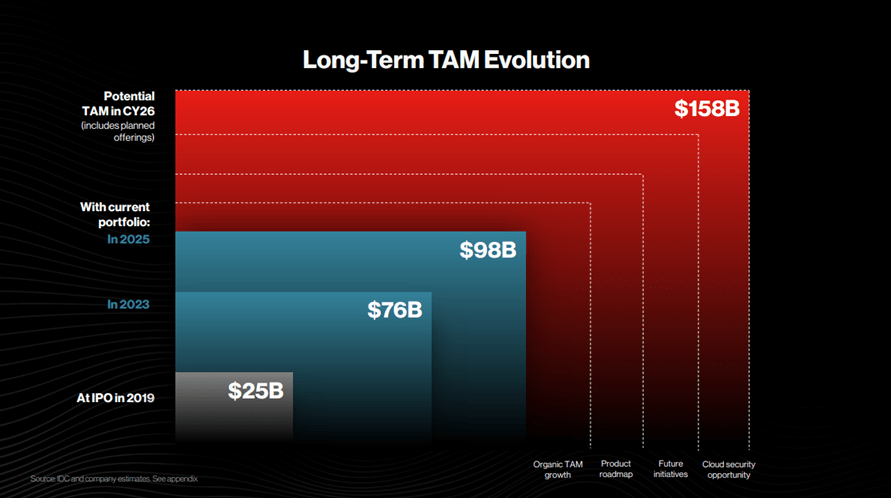

CrowdStrike Total Addressable Market (CrowdStrike Investors Page)

For the management team, this industry outlook translates into a massive total addressable market. This has to be read with caution, and it’s provided by the company who has an interest in getting to a point where revenue grows beyond belief, but it’s also a strong bull argument, suggesting that there is a lot of top line growth ahead for this company.

Bull Case Argument #2– The Company Performance:

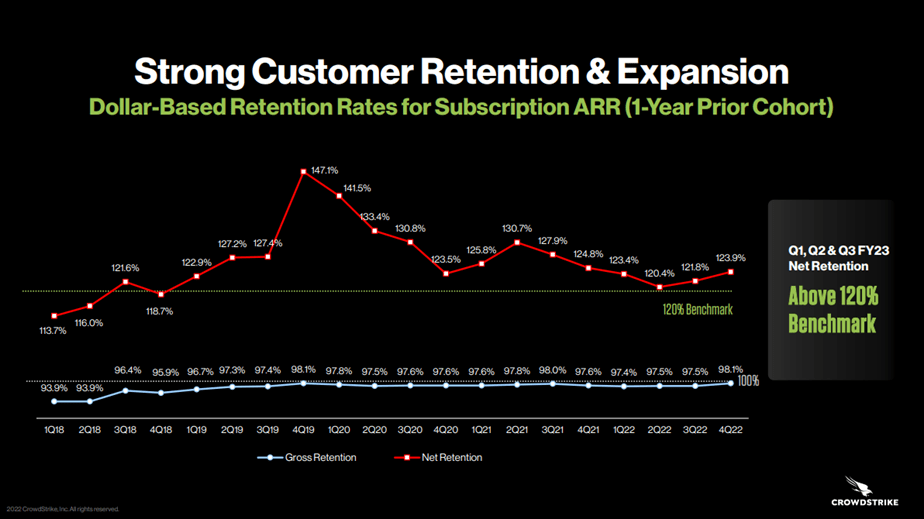

Below is probably one of the first slide’s bull’s jump to whenever CrowdStrike releases its most recent financial performance, as it encapsules the strong performance of the company.

CrowdStrike Customer Retention (CrowdStrike Investor Page)

The illustration above provides two of the strongest selling points on behalf of CrowdStrike.

- Dollar-Based Retention Rate: showing how much revenue the company makes from its existing customer base over time. For the past 16 quarters, the company has exceeded a dollar-based retention rate of 120% suggesting that customers are pleased with the service they are procuring, to the point where they spend more money with CrowdStrike over time. A strong sign of customer satisfaction.

- Gross retention: Showing the number of customers the company manages to keep on its books as time passes, with the best possible outcome being 100%, which of course is an unrealistic achievement given some customers come and go, others go out of business and so on. Gross retention is at 98% and has been in that ballpark for 18 quarters in a row – extremely impressive.

If you then consider why exactly CrowdStrike is able to upsell so consistently to existing customers, and why they are able to retain more or less all of them throughout time, then we get to some of the arguments that fascinate bulls.

I’ve snipped the argument below from one of my previous articles covering the company, speaking about what’s fascinating about this company in particular.

- CrowdStrike offers cybersecurity solutions anchored in the cloud, based on a SaaS (software as a service) model. These solutions are built around an AI, which improves its intelligence every time it encounters a threat or breach.

- As the AI becomes smarter, it strengthens its resilience towards cyber related threats, but also makes it increasingly difficult for new competitors to match the services provided by CrowdStrike.

- This creates a strong network effect benefitting CrowdStrike, as every new or existing customer benefits from the combined AI knowledge growing over time.

- CrowdStrike is recognised by Gartner as an EPP (End Point Protection) leader, based upon strength of vision and ability to execute.

- CrowdStrike took its point of departure in what the legacy cybersecurity industry did wrong – it was inflexible, complex and failed to provide the security, which customers relied upon. CrowdStrike remains founder led and carries high ambitions, considering itself a category leader.

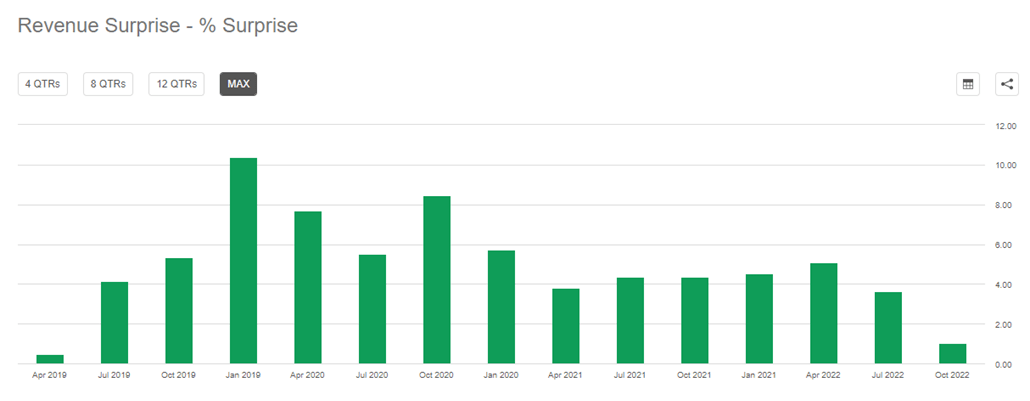

These factors also make their way into the profit & loss statement of the company, where CrowdStrike has a history of surprising to the upside. Consistently doing so can compound meaningfully over time, meaning that consensus estimates consistently have to be reviewed upwards to factor in the revenue surprises, driving faster growth than previously anticipated.

CrowdStrike Revenue Surprise (Seeking Alpha)

Bull Case Argument #3– The Valuation:

Interestingly, there is also a bull side of the valuation perspective.

Here, the bull will argue that the company can grow into its valuation. That, the valuation was certainly lofty, and while it perhaps still is, it is now at a point where the company can grow into it.

One year ago, the forward consensus estimates came in as follows

- FY2023 revenue of $2 billion (YoY growth of 40%)

- FY2024 revenue of $2.65 billion (YoY growth of 32%)

Today, those consensus estimates look the following

- FY2023 revenue of $2.23 billion (up from $2.2 billion in June 2022)

- FY2024 revenue of $2.98 billion (up from $2.9 billion in June 2022)

As you saw in the earlier valuation graph, the P/S ratio stood at above 35 just a year ago, having come down substantially at this point. Should management achieve the FY2024 consensus estimates, the P/S ratio would stand at 8.0 with today’s market cap. The current consensus estimates for the years to come provide the following P/S ratios.

- FY2025 revenue of $3.89 billion corresponding to a P/S ratio of 6.1

- FY2026 revenue of $5.25 billion corresponding to a P/S ratio of 4.5

Should management continue its tendency to overdeliver in comparison to the consensus estimates, then the path to growing into the valuation suddenly appears much more feasible. As such, the bull would argue that today’s valuation isn’t completely off the market if management can deliver on the consensus estimates, where they typically have managed to overdeliver.

Takeaway

Going back one year, and many of the bear side arguments didn’t require much attention, but they’ve grown stronger throughout 2022 as the FED have raised interest rates at a record 0.75 basis points. In addition, the FED has hiked faster than ever before in newer history, causing the bear case arguments to command more respect. On top, management reached a point where they had to communicate disappointing news impacting the outlook. A potent mix with the already uncertain and volatile markets, which forced a very strong downwards stock price reaction.

At the same time, it’s difficult to argue that CrowdStrike isn’t delivering on its roadmap, while finding itself in an industry that’s problematic to avoid for board of directors, as they can’t take the risk of not protecting their companies towards breaches. In addition, with the company being down 48.6% YTD, the valuation has perhaps finally gotten to a point where it’s not considered lofty, but just high, as the P/S ratio on a forward basis continues to stay above 10.

I’m already long the stock with respect to the bull side arguments, but I also recognise that I was early given how the bear side of the argument developed in a very hasty manner throughout 2022. I’ve layered into the stock since, with room for one last buy before I’ve reached a full position. Given where the valuation is at this point, I hold firm the opinion, that CrowdStrike can grow into its valuation.

However, management has opened pandora box, indicating that forward guidance might have to be slashed in one of the upcoming quarters, should deals turn out to be cancelled and not just postponed, referencing the CEO’s own earnings call discussion. Trading with a P/S ratio above 10, the market will once more act without leniency if that turns out to be the case. Therefore, despite the valuation not being as lofty as it used to just six- to twelve months ago, this is still a case that requires patience and, in my opinion, a dollar cost averaging approach to smoothen out additional potential downside.

Which side of the arguments resonate more with you, the bull or bear perspective?

Be the first to comment