grandriver

Introduction and CRT Business Overview

I recently came across Cross Timbers Royalty Trust (NYSE:CRT), a business with a simple business model which offers investors dividends from oil and gas properties, and has since it was first created in 1991. The Trust receives 90% net profit interests from oil and gas-producing properties in Texas, Oklahoma, and New Mexico, and 75% net profit interests from other properties in Texas and Oklahoma.

The 90% net profit properties are “overriding,” meaning CRT simply skims its share from ending profits, and the 75% net profit properties are “working” interests which means profits are accounted after exploration and production costs.

The Trust’s income is skewed roughly 2:1 oil to gas, though this fluctuates with the market prices for both.

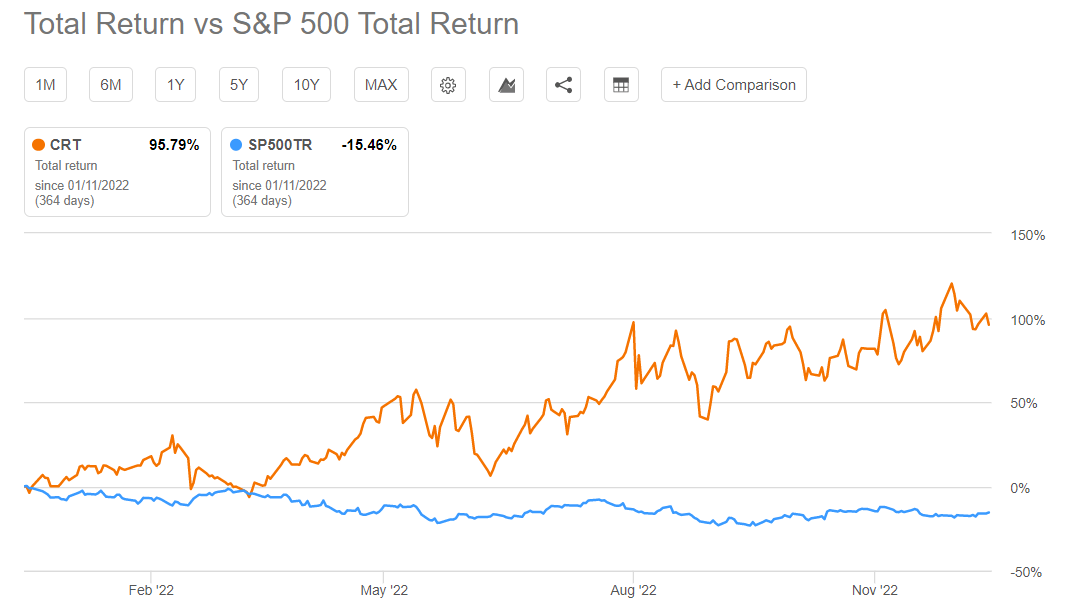

Quick Total Return Overview

In addition to rising 75% over the last 12 months, the Trust has also paid out nearly $2 in dividends, amounting to another 20% return on cost, for a total return over the last 12 months of ~95%. This is in comparison with the S&P’s performance over the last 12 months of -15%.

Seeking Alpha

While I don’t expect CRT to duplicate its 2022 performance in 2023 due to lower forward energy prices, I believe the Trust will continue its market outperformance and is worth holding for investors looking for income and some price appreciation from the energy markets.

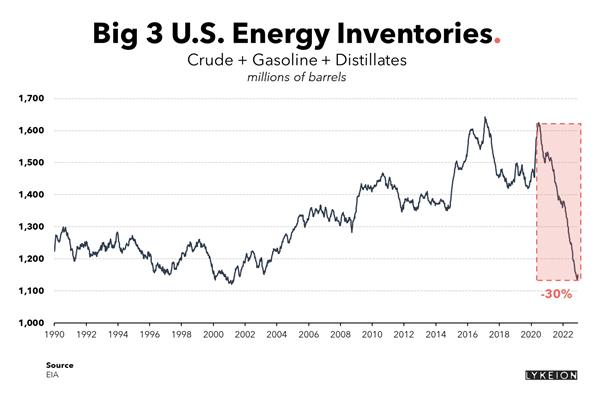

Energy Prices Likely Near Their Lows

I won’t dive too deeply into the broad macro picture for oil and gas here, but I do believe both oil and gas prices are near some respective bottoming points and have upside into 2023 and beyond.

Due to China reopening, SPR and Russian flows declining, simple underinvestment from the last half decade+ and increased production costs, I think WTI crude is headed toward $90+ by the end of the year. I don’t believe we’ll see the $140 purported by other hedge fund managers, but IMO the supply/demand situation is too tight for oil to remain in the low-$70s.

I’m including one fundamental chart below showing the drawdown we’ve taken in crude + product inventory which doesn’t leave much room for further drawdowns.

EIA

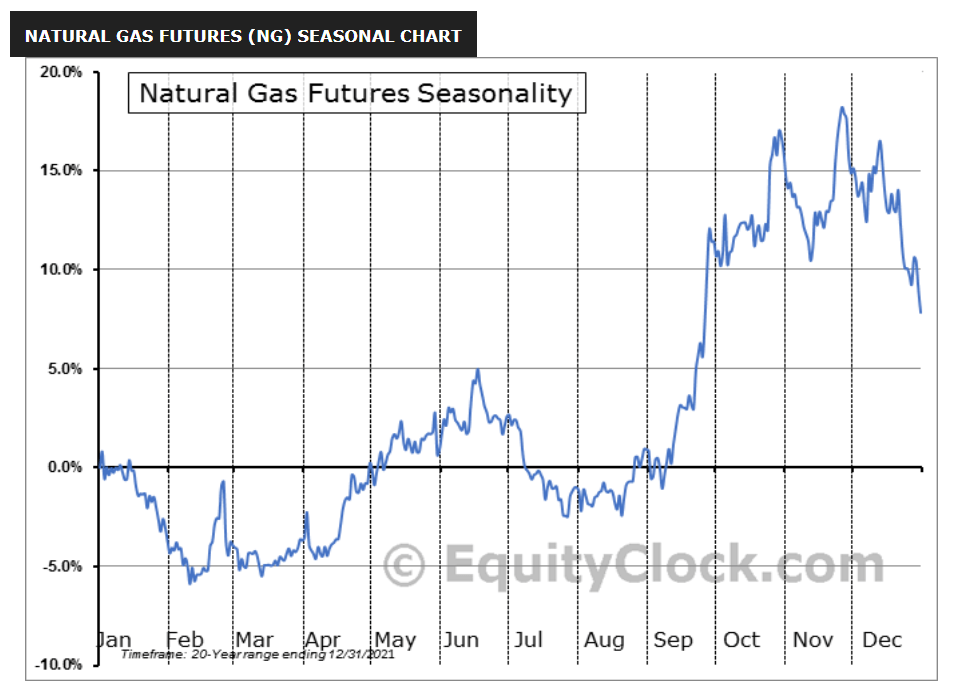

Nat gas, while volatile and weather-dependent, is nearing its production cost in the U.S., U.S. export capacity including Freeport is coming back online soon, European and Asian prices are still multiples higher and dependent on foreign production, and industrial shutdowns have contributed to demand loss but cannot remain in place forever. In addition, seasonality says prices may dip slightly further but will soon turn positive. NG prices seem very likely to bounce from current levels around $4-$7+ for the year ahead.

EquityClock

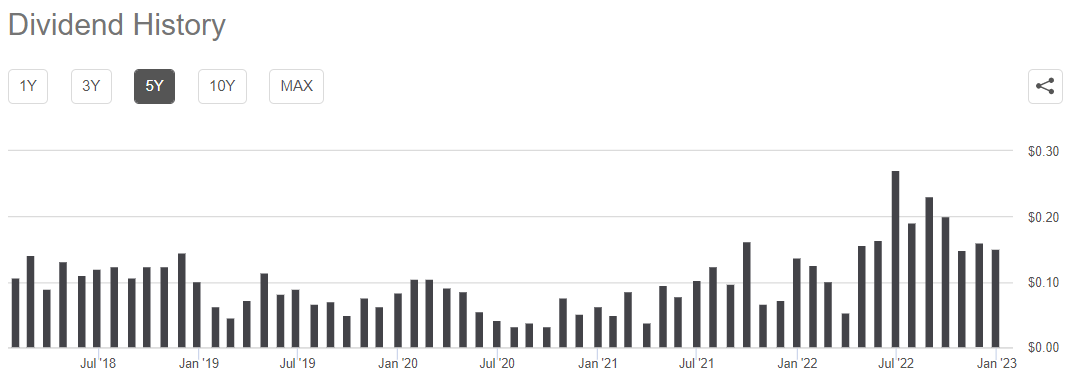

While the next couple months of dividends will be lower due to lower oil and gas prices, I believe investors can hold CRT with confidence of future payouts remaining valuable.

CRT Dividends and Reserves Stable

One bear thesis point for CRT, though it has basis in truth, is that the Trust is a “depleting” asset as it turns production into shareholder returns every year. In fact, the company estimates natural declines in its properties of 6-8% per annum. From the company’s SEC filings:

CRT SEC Filings

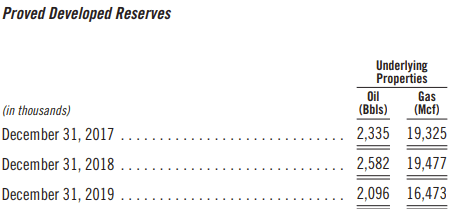

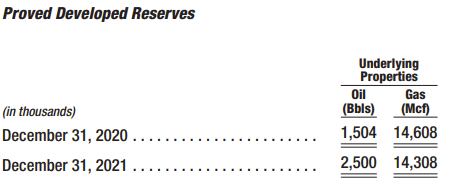

However, the Trust has been operating for over 30 years and has always been able to keep producing and replenish its reserves from increased drilling techniques and recovery methods, as well as a gradual increase in prices over time. Below is the 5-year dividend chart for CRT, showing relative stability (though dipping from payments during COVID, which occur with a slight lag) as well as growth over the last couple years as energy prices have gone higher.

Seeking Alpha

In addition, the charts below show relatively stable reserve numbers over the last 6 years, though again 2020 caused a dip as COVID crushed energy prices with oil going negative and nat gas falling to ~$1.50/mmBTU.

CRT SEC Filings CRT SEC Filings

I do not believe the Trust has significant depletion concerns in the immediate term.

If oil and gas prices can remain steady from here, CRT should continue paying its 8% yield without too much difficulty. Upside to energy prices could add an additional 10-20% return for the remainder of 2023.

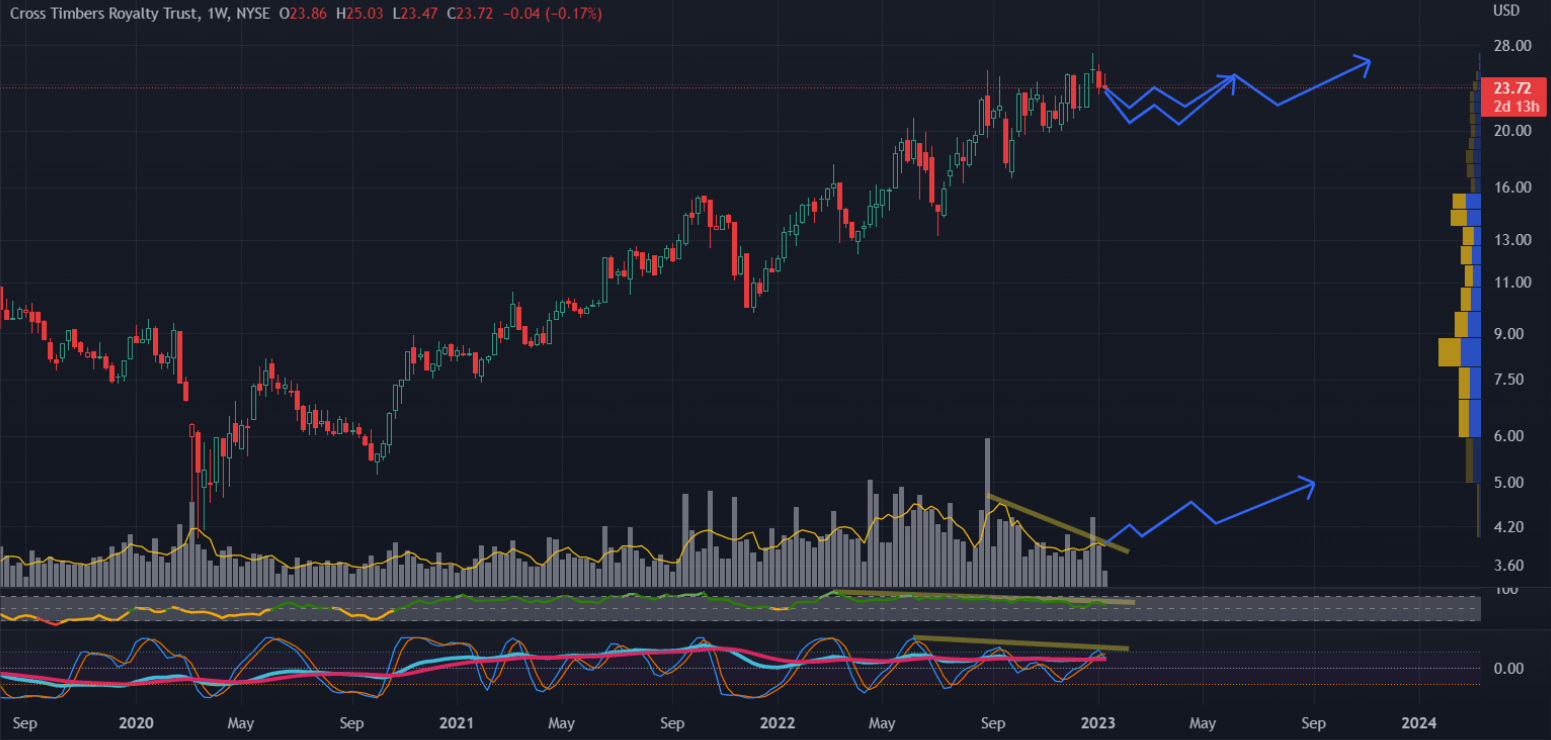

Technical Analysis

Below is my estimate of where we can see CRT moving into the remainder of 2023.

Author’s Analysis

Solely based on technicals, it actually looks to me like CRT could face some short-term downside. This may line up with lower dividend payments over the next few months from lower energy prices, which may be an excellent accumulation opportunity for investors who want exposure to the name. I’ve marked 3 indicators telling me of the potential dip, namely:

- Declining volume since September on a run-up in price

- Decreases in money flow (first indicator below the chart) since June

- Declining Stochastic RSI and Total Strength Index since June (second indicator panel)

In my experience, these indicators usually need to put in a higher low before they are able to fully “reset” for another leg higher.

Also recall that dividends paid from the Trust will be removed from the stock price on the ex-dividend date, so “downward” or sideways movement can still occur during periods of total shareholder return.

Risks/Other

As readers of my other articles will know, one of the main risks I see to energy-related names (and certainly CRT) is a resolution to the Ukraine-Russia conflict. Geopolitics are difficult to predict, and while a resolution to the conflict would not necessarily lead to immediate resumption of Russia’s energy production, I do believe the market would quickly and forcefully sell energy names in such an event. Investors should be prepared for what could be a ~20% drop overnight.

As discussed above, I have a bullish view on energy for the mid- and long-term, so do not believe this would be a death blow to CRT or other energy names, but prospective investors should be aware of this risk and be comfortable holding through such a volatility event.

Trustee Change

One other brief note is that CRT just underwent a change of its Trustee on 12/30/2022. The old Trustee, Simmons Bank, announced their resignation back in November of 2021 (perhaps wishing to divest from fossil fuels), and the new Trustee is Argent Trust Company, a well-established Trustee in operation for 30+ years. I do not believe there is anything materially concerning here, but this is something investors should be aware of.

Closing

In closing, I believe CRT is a fairly-priced vehicle at current energy prices with upside exposure for the next year and beyond. In my opinion, investors wanting exposure to the energy markets while also wanting dividend income can use CRT as a healthy building block in their portfolio.

As you can see from my technical analysis, CRT could face some downside ahead, but investors should expect income / shareholder returns to continue and can use dips to accumulate a position.

I own another Oil and Gas Trust (PBT) which has been investing more heavily in growth leading to more volatility, but may be adding CRT or other Royalty/Trust names to my portfolios this year and will likely hold them until the global energy situation drastically improves. I may do an article on PBT soon and will update investors on any significant moves or changes in the thesis.

Be the first to comment