Chun han/E+ via Getty Images

Since I wrote about the Irish construction company CRH (NYSE:CRH) in November last year, it is up by almost 14%. This was to be expected. At the time, I had penciled in a 10% short-term upside to it going by its fundamentals, prospects and market multiples. The increase is slightly bigger than expected, not just because of the fundamentals, but also for two more reasons.

Why has CRH’s price risen?

The first is its own share buyback programme. With fewer shares available to trade, it is to be expected that the price will increase. This also attracts new investors to it, potentially pushing the price up further. The company initiated the buyback on December 19, 2022, and it will end at the end of March this year.

There are broader macro factors at play too. I believe this year, it has been further supported by the rotation towards cyclical stocks. Last year saw investors shirking from buying them as a recession looked all but guaranteed. But come 2023, and suddenly they are back in favour. This is evident to some extent in the materials sector. It is still down by 3.6% year-on-year (YoY) but has made gains, of 5.7% this year (see chart below).

S&P 500 Materials Index (Source: S&P Global)

What market multiples say

Here I take a closer look at if there’s more upside to CRH. First things first, compared to the same time last year, it is still down by almost 10%, which alone could indicate more upside. But let’s look at its valuations to confirm this. When I checked last, the company’s price-to-earnings (P/E) ratio was at 11.2x, lower than the then 12.15x for the materials sector. Now, it is at 12.8x, which is basically in line with that for the materials sector at 12.7x. This indicates that at least by this measure, CRH is fairly priced now.

But this is just a part of the story. The materials sector is a broad classification that covers other industries, like mining for instance, as well. So while it is instructive, a closer look at the peers offers even more insight into how well, or not, a stock or its ADRs are priced.

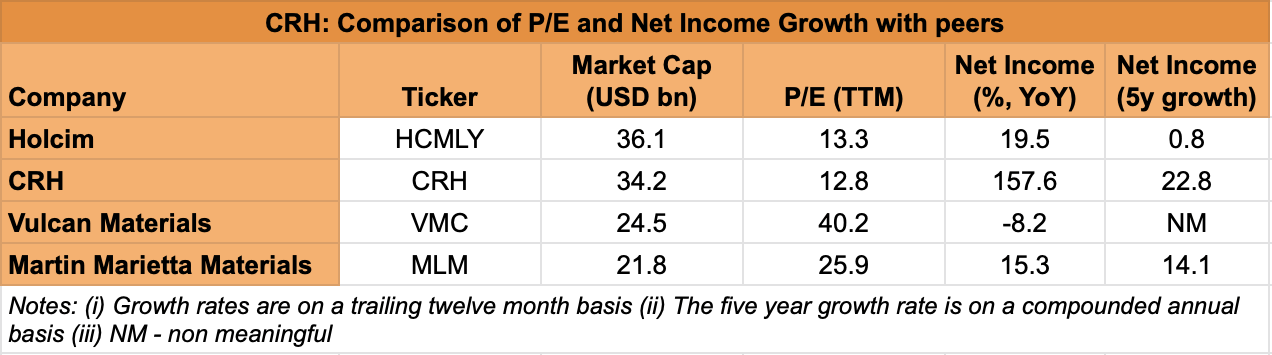

Comparing CRH to other construction companies like Holcim (OTCPK:HCMLY), Vulcan Materials (VMC) and Martin Marietta Materials (MLM), its closest counterparts in terms of market capitalisation, reveals that it is in fact likely to be undervalued. VMC for instance has a P/E of 40.2x and MLM is at an earnings ratio of 26.7x. HCMLY is closer to CRH, but even that has a higher P/E at 13.3x. Further, the company’s trading at a relatively low P/E even by its own historical standards. Its median P/E for the last decade is at 21.5x.

What the fundamentals indicate

However, only if the company’s fundamentals are sound is it likely to see a sustainable price rise that brings it closer to its historical average P/E or that of its peers. Since last November, when it released its trading update, there have been no more stock-moving announcements from the company besides the buyback. This means, that there’s nothing to fundamentally change the CRH story. In fact, it is only strengthened, considering its superior performance to peers as highlighted the last time (see table below) in conjunction with its P/E.

Source: Seeking Alpha

Signs of a construction recovery

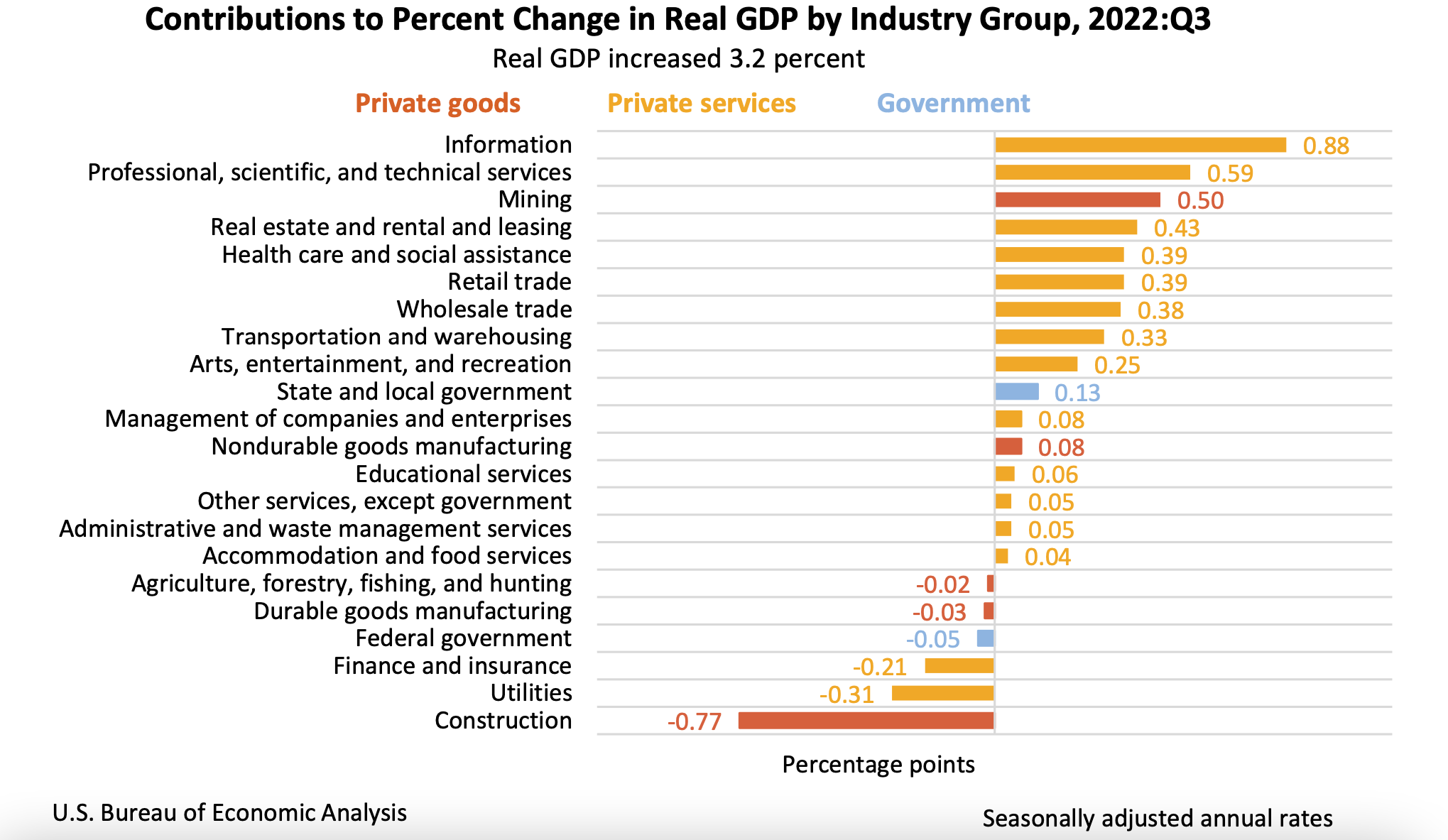

However, the fact remains that the construction industry is still in a weak spot. For the third quarter of 2022 (Q3 2022), it was the biggest drag on the US GDP (see chart below), which is important for CRH since more than half of its revenues are generated from the market. However, there are sure signs of recovery:

- The construction industry’s GDP seasonally adjusted decrease is still glaring at 17.8% quarter-on-quarter (QoQ), and the biggest among all industries, but it’s still less than the 19.2% decline seen in Q2 2022.

- Construction starts are up by 27% month-on-month [MoM] on a seasonally adjusted basis from December 2022. This is driven by an increase of 51% in nonresidential construction and 30% in non-building construction, which is significant, considering that 65% of CRH’s exposure is in non-residential and infrastructure segments. This can more than make up for the zero growth in residential construction.

- More hearteningly, this is not just a single-month’s trend. Construction starts rose by 15% year-on-year (YoY) in 2022 as well, despite a 3% drag from residential construction.

Source: BEA

Note of caution

However, a recovery in construction can hardly be taken for granted. The Dodge Momentum Index, which is a leading indicator for nonresidential construction, dropped by 8.4% in January 2023. In its release, Dodge Data and Analytics quotes Sarah Martin, associate director of forecasting for Dodge Construction Network as saying “…we expect the Index to work its way back towards historical norms this year, in tandem with weaker economic growth.” In other words, a muted economic scenario is still likely to play on the industry for a while longer. Also, in the UK which accounts for some 25% of CRH’s revenues, the outlook for the construction industry is recessionary, in line with expectations for the economy as such.

It is hardly all gloom and doom though, at least for the US. As Martin adds, though, “Overall, levels of planning activity remained comparatively strong over the month — which bodes well for the construction sector.” To me, this indicates the likelihood of cautious recovery in the sector in any case. The Inflation Reduction Act [IRA] in the US would also boost the segment further. In any case, some of the latest figures on construction in the US as noted above are positive.

What next?

The important bit to remember about CRH is that it showed impressive growth over the last 12 months, despite the construction industry not being in the best place. Can it continue to grow at such a fast clip? Its EBITDA growth at 21% as per the last update for the first half of 2022, was higher than its full-year forecast of 10%. So we should expect a correction here.

At the same time, the full-year EBITDA is still expected to grow. It is also still trading at attractive valuations. Further, over the past decade, its price has risen by more than 120%. It also pays a dividend. Its yield is not the highest at 2.6%, but it has paid them consistently for the past 12 years, which counts for something. It is one to consider, just for that reason, from a passive income perspective, besides its price performance. In the short term, I reckon CRH can fluctuate, going by uncertainty around construction or if investor sentiment turns against cyclicals again, but it remains an attractive buy from a medium to long-term perspective.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment