Crew rowing Alistair Berg/DigitalVision via Getty Images

Introduction

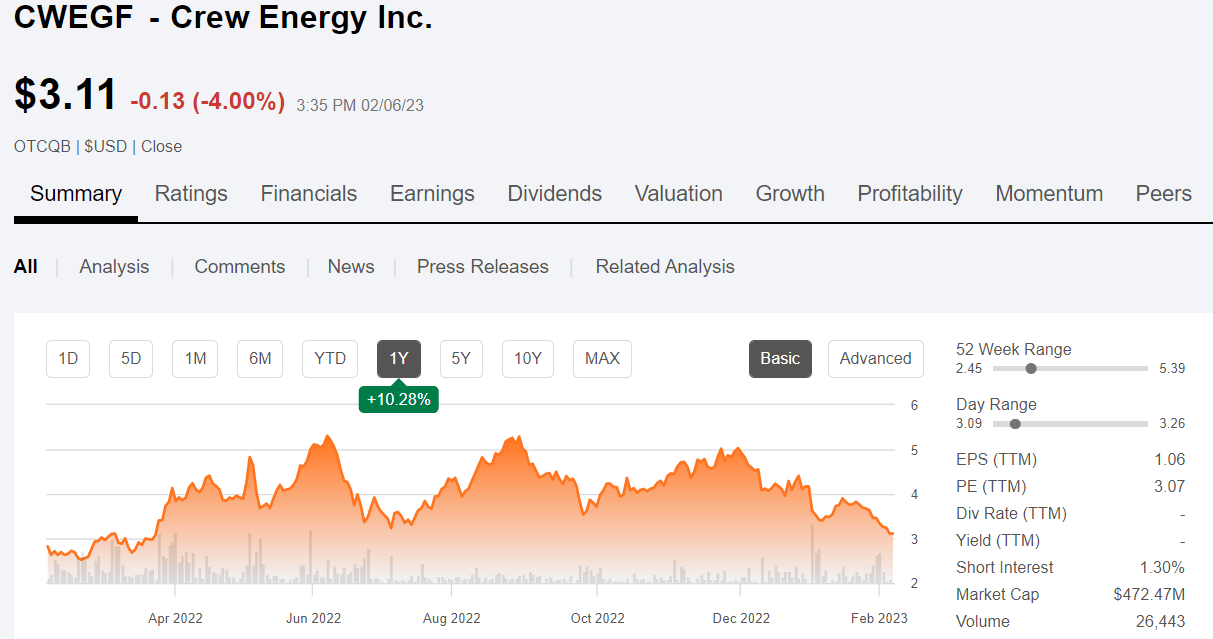

Last May, Crew Energy Inc., (OTCQB:CWEGF) seemed like a solid bet for growth, and in fairness, in the bullish environment that persisted in the crude and natural gas space until June, it was. I gave them a favorable write-up, and you should refer to that article for deep background on the company. Crew hit the low $5’s in the June swoon, then rebounded to the low $5’s twice more during the year before sagging back to the low $3’s as gas swooned in December. In the travel business, that’s called a return ticket. A good thing generally if you’re going someplace, but not so much in investing.

Crew Energy price chart (Seeking Alpha)

Let’s catch up with Crew Energy Inc. and see if any of this is their fault, or are they just a victim of the malaise in the crude, and particularly, in the gas market, as are so many others.

The analyst community is high on the company presently, with an overweight rating, and price targets ranging from $7.00 CAD on the low side $11.00 CAD at the upper end of the range. That range corresponds to a USD price of $5.22 to $8.21 at current prices, giving us a reason to take a closer look.

The thesis for Crew in 2023

I will admit that I’ve been sharpening my knife for several months, to carve up some of the gas players at 50, 60, and 70% discounts to early Q-4 prices. The tea leaves were portending a rebound in gas prices from the mid-$6’s, as winter arrived. Crew Energy Inc. is just the sort of Canadian energy player I’ve been keeping an eye upon, now selling near a 40% discount from recent prices thanks to a very tardy and sketchy winter thus far.

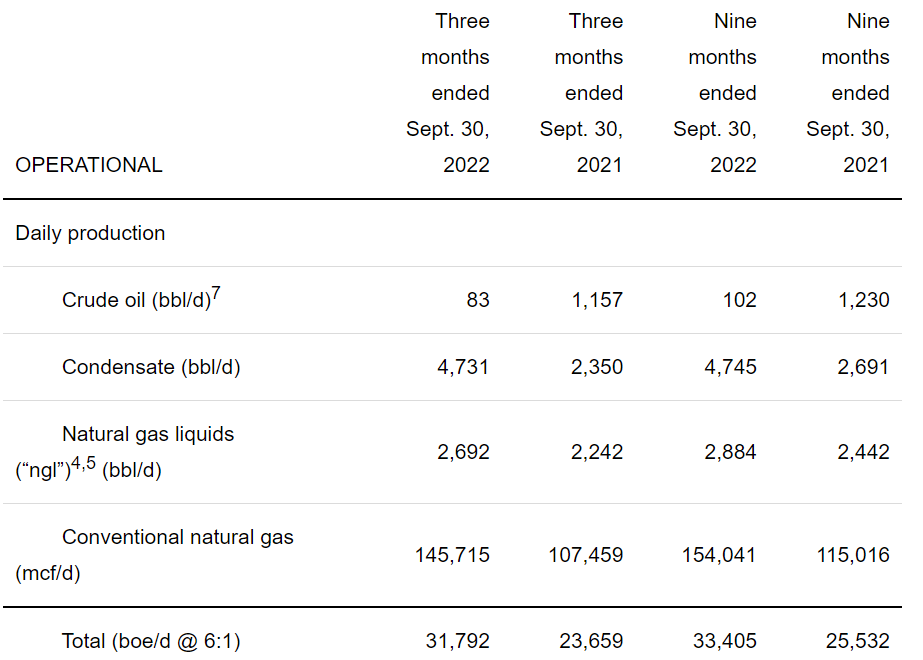

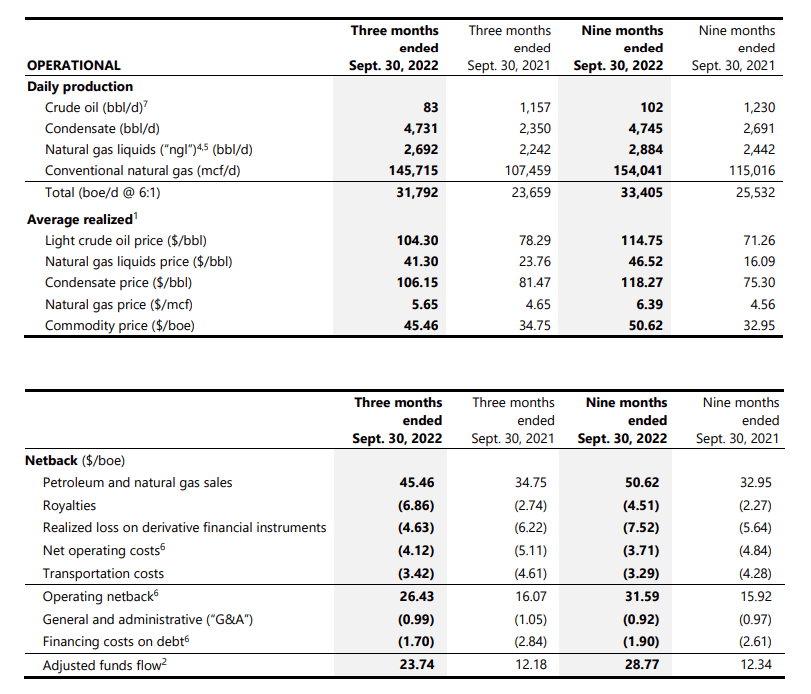

Crew Q-3 results (Crew Energy)

Winter, it turned out, was late, not putting in an appearance until Thanksgiving, and then retreating until Christmas. Our friends over in the EU had a similar experience with winter and have not severely drawn down the reserves built up last summer.

With every shale basin producing record amounts of gas, there was only one thing to do. Inject it. Storage declined at a fairly slow rate for the entire season so far, and pretty much knocked on the head of any idea of a rally. Today we are about 750 BCF above year ago levels. And, down gas went, dropping from $7.00 to a 2-year low of $2.41 MCF.

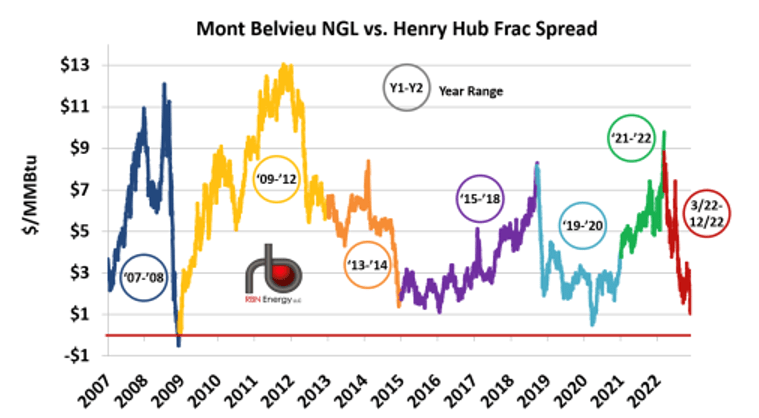

As if that weren’t enough, the NGL’s market is brimming as well with the price for the composite NGL index plummeting, as supply outstrips demand. What’s going on? The frac spread can give a clue. This graph from RBN Energy gives a multiyear lookback at this metric and reveals it is nearing the lows of 2020.

Mont Belvieu vs HH Frac spread (RBN Energy)

In a December blog post, RBN discussed some of the factors driving NGL’s into the poor house.

Global demand (and especially Asian demand) for ethylene and propylene are off sharply, an estimated 15% to 20% of U.S. steam cracker capacity is offline, and the prices of ethylene and propylene are off by 29% and 39%, respectively, in the past six months. As for normal butane, isobutane and natural gasoline, they are used primarily as motor gasoline blendstocks and for other uses in the motor fuel markets, and consequently follow crude oil prices closely — hence, they’ve been tumbling the past few months. And propane? Its prices are affected to some degree by oil prices and by the strength (or, lately, the weakness) of the petchem industry, both in the U.S. and internationally. The downturn in petchem demand, combined with an uptick in NGL production, has resulted in a build-up in U.S. propane inventory, which has had its own dampening effect on propane prices.

RBN.

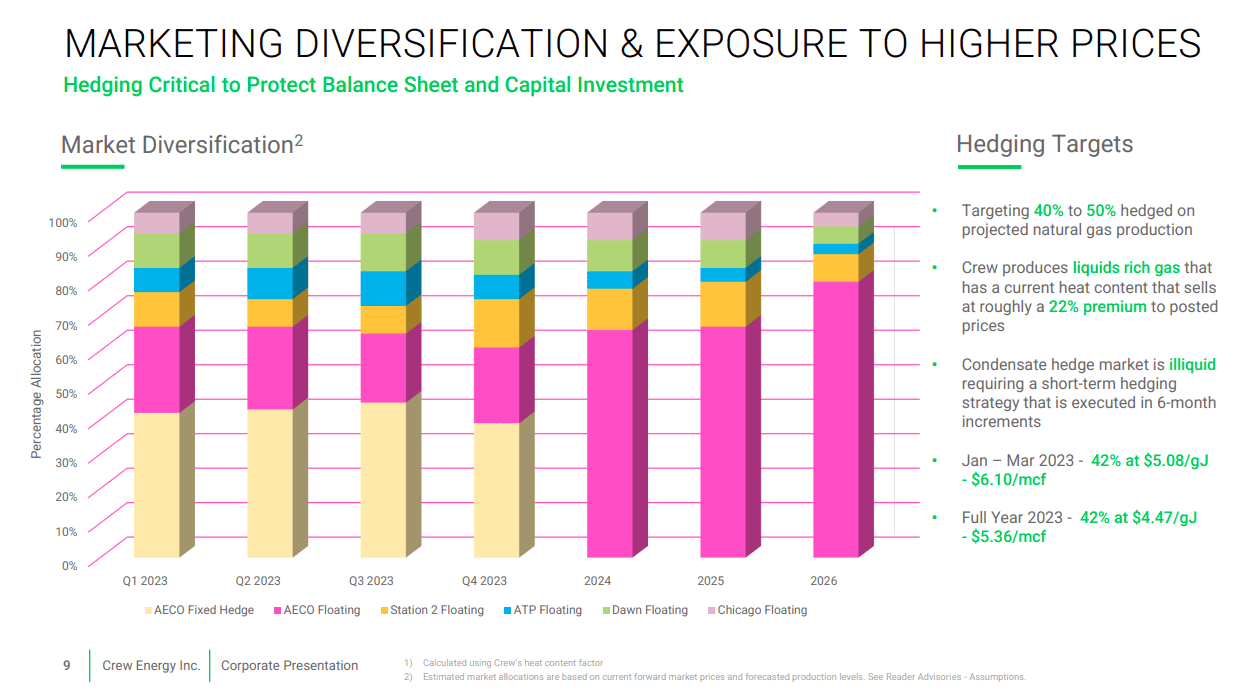

With the market in the tank for much of its production, weighted about 80% to gas and NGL’s, there is only one thing that can save the year for Crew: hedging and the ability to select the markets where gas is sold.

Hedging and Marketing for 2023

Q4 2022 should come in pretty good for Crew, with gas prices averaging in the low $6’s for most of the quarter. Analyst estimates are for $0.20 CAD per share which is where they were for Q3, when Crew surprised with $0.65 CAD per share. Clearly the ability to ship gas to other markets than AECO enabled this tripling of analyst estimates for Q-3, and should have a favorable impact for Q4.

Crew Energy hedging strategy (Crew Energy)

As the table below reveals, realized prices were quite a bit higher in Q3, than they are likely to be for Q4, 2022, except for gas. And, it’s gas that really matters to Crew. That probably means a surprise triple of analyst estimates, is off the table, but with Crew’s nimble marketing they will do better than $0.20 CAD.

Crew Energy results for Q-3 (Crew Energy)

Risks

I think Crew is largely de-risked at current prices. The forward strip suggests the bottom is in for Natty, but the near-term upside isn’t particularly compelling. That being the case, the principal risk I see is dead money until we get a strong buy signal from the gas market. That might not happen until summer.

Weak gas prices could curtail capex allocation and hit planned growth.

The outlier is China. If they begin absorbing every global commodity again, the risk could be to the upside.

Your takeaway

I think Crew Energy Inc. will beat estimates for the quarter. Through smart hedging and nimble marketing, they have a history of doing this. Using a conservative estimate of $28 WCS differential to WTI probably gets you in the neighborhood of $42 CAD for a realized price. If they hit production targets of 32k BOEPD in Q-4, they should generate revenues of $115 mm CAD, or about $86 mm USD. OPEX costs of around $20 per barrel result in a netback in $22/bbl range, or about $0.39 per share (22*32K*90/162 mm). That seems doable to me.

The question is, will a nice beat like this move Crew Energy Inc. stock? I doubt it over the near term with the dour macro environment we are facing for gas.

Right now, Crew Energy Inc. is selling at 2.5X EV/EBITDA and $16.7K per flowing barrel. Using those metrics, Crew is a strong buy at current prices for patient investors. I underline patient as until a catalyst – China, restart of Freeport LNG, summer cooling in the U.S. – we could be range bound in the $3’s for this stock. Long term, if you’ve wished to take a position in this company for eventual growth, you’ve got your wish.

Crew Energy details (Crew Energy)

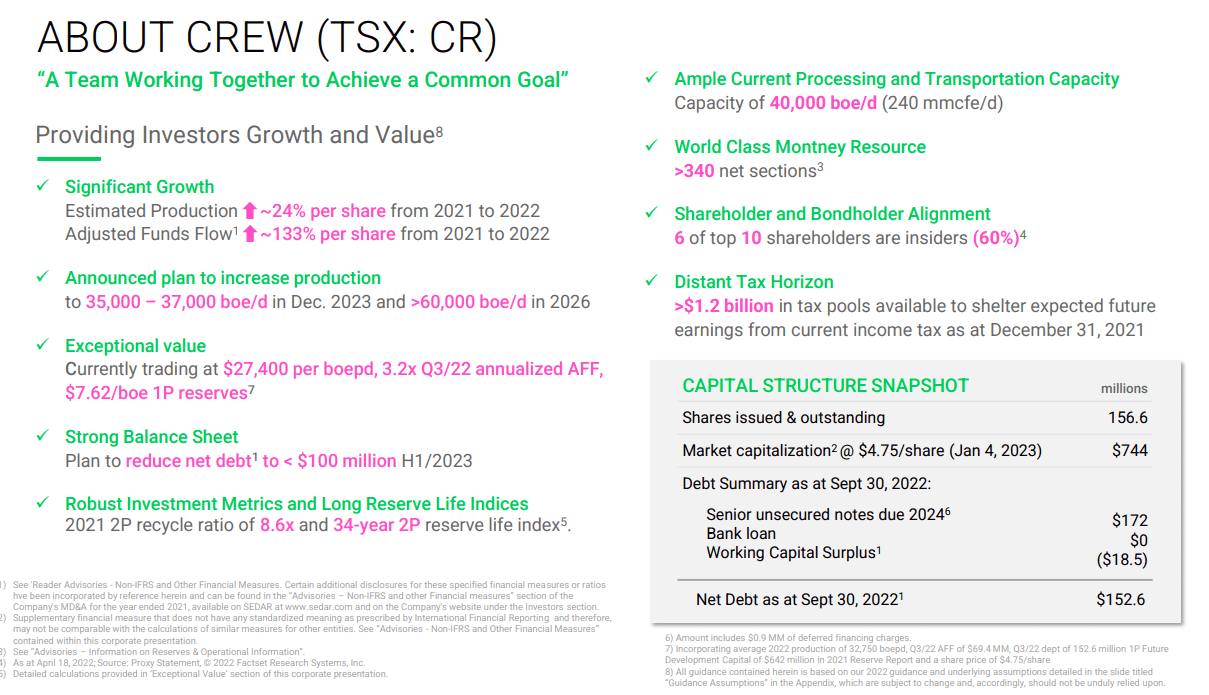

Bottom line: Crew Energy Inc. is doing everything right. They have grown and are continuing to grow production. It has plans for 2023 to exit with 37K of BOEPD production as shown below. They are paying down debt with cash flow and covering their capex of $30 mm per quarter. Their hedging should enable realizations to move higher through the year, further buttressing efforts with their balance sheet.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment