imaginima

Investors usually look for the biggest midstream firms to invest in which explains the popularity of companies such as Enterprise Products Partners (EPD) or Energy Transfer (ET). However, smaller midstream firms that are not on everyone’s radar may also be attractive yield investments for investors. One midstream especially, Crestwood Equity Partners LP (NYSE:CEQP), is a growing master limited partnership (MLP) with great distribution coverage and an attractive 9.5% dividend yield. The company’s units are also attractively valued based off of distributable cash flow and EBITDA!

Growing MLP with high percentage of fee-based revenues

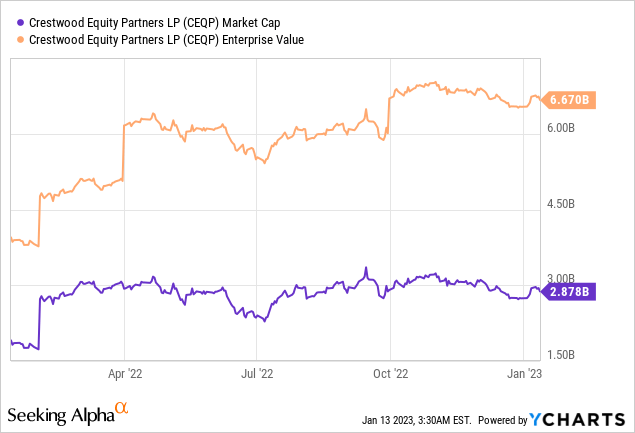

Crestwood Equity Partners owns a diversified portfolio of midstream assets that are connected chiefly to three operating areas: the Williston, Delaware and Powder River Basins in the U.S. The company’s core operations include the gathering, processing, transportation and storage of energy products such as natural gas, NGL and crude oil. Crestwood Equity Partners is a typical master limited partnership, but a small one with a market cap of only $2.9B and an enterprise value (market cap plus debt) of $6.7B.

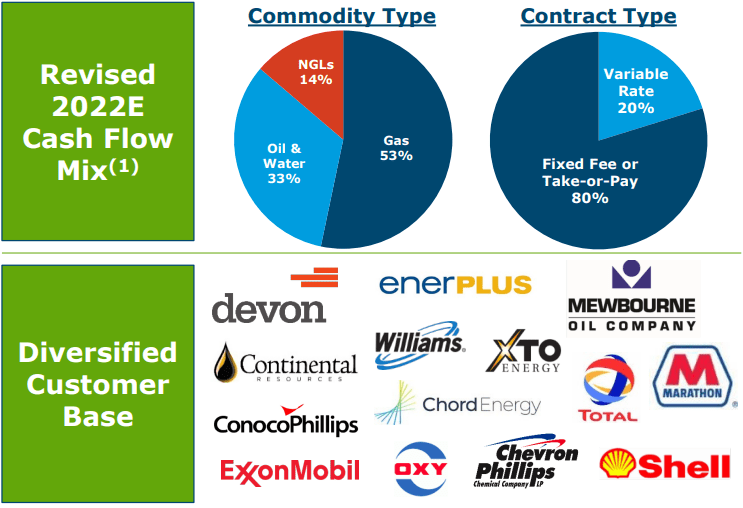

As a midstream firm, Crestwood Equity Partners contracts its gathering, transportation and storage services chiefly on a fee basis which helps the company generate highly predictable cash flow that is used to pay unitholders a generous distribution rate. More than half of the firm’s cash flow comes from the operation of assets related to natural gas while 33% of cash flow is derived from crude oil and produced water. Only about 14% of cash flow comes from Crestwood Equity Partners’ NGL business.

About 80% of the MLP’s earnings structure is subjected to fees or take-or-pay contracts, both of which limit risks for midstream firms and keep price risk for energy commodities with the producers. Among the customers of Crestwood Equity Partners are top-rated energy firms like Shell, ConocoPhillips, ExxonMobil, Marathon and XTO Energy.

Source: CEQP

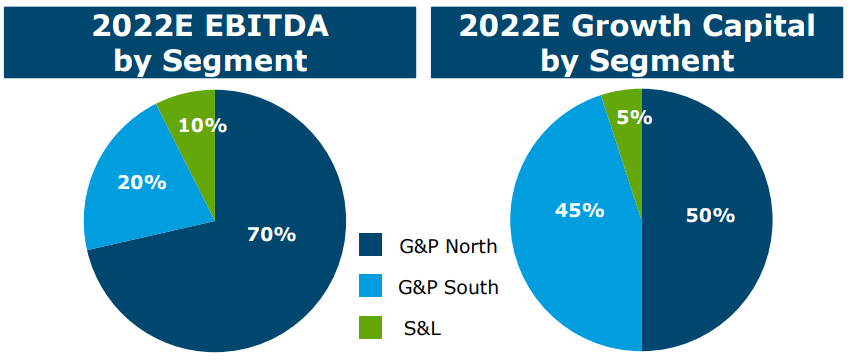

Crestwood Equity Partners groups its business into three segments: Gathering & Processing North (comprising of Williston and Power River Basin assets), Gathering & Processing South (Delaware Basin assets) and Storage & Logistics. Crestwood Equity Partners’ Gathering & Processing North business is expected to generate 70% of the firm’s EBITDA in FY 2022 and it receives about 50% of growth investments.

Source: CEQP

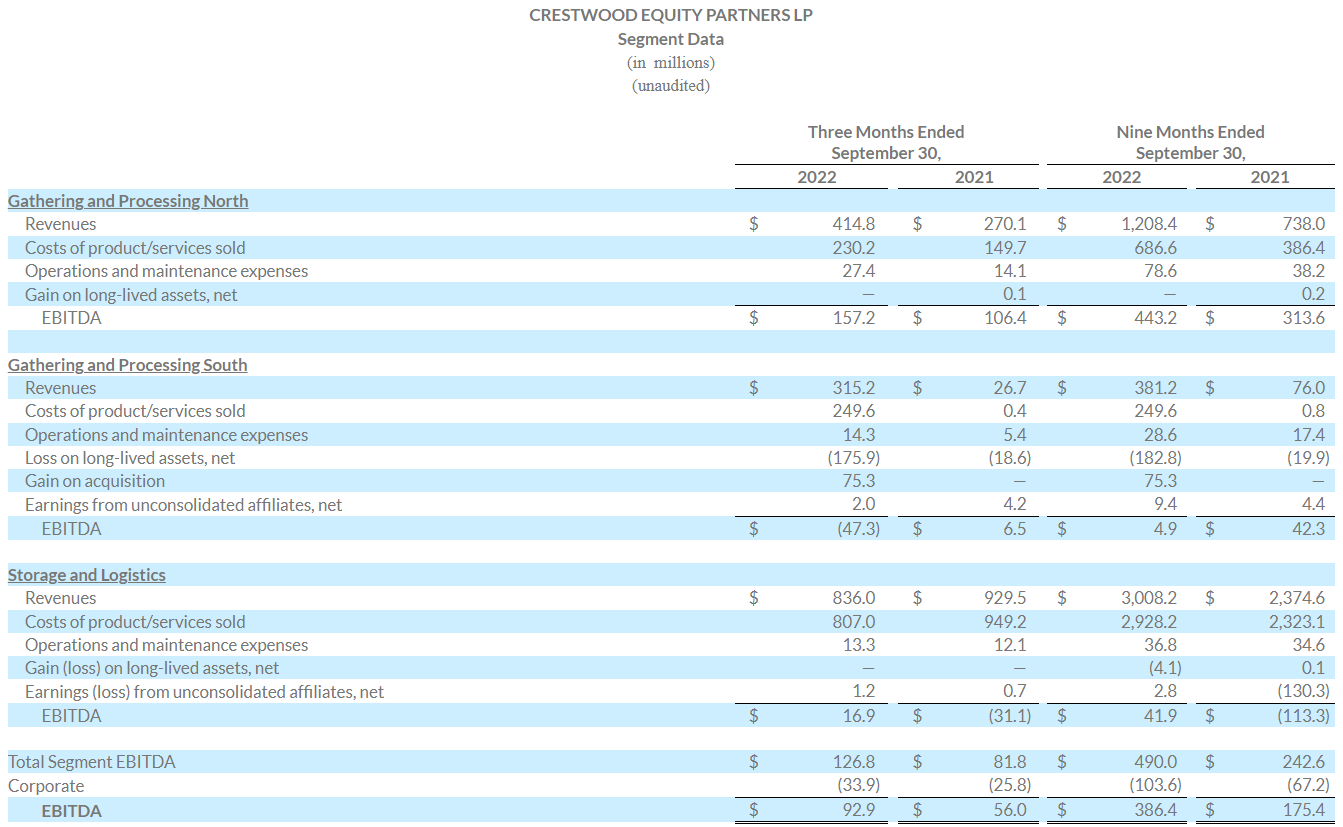

The firm’s EBITDA increased 55% year-over-year to $126.8M in the third quarter due to expanded operations and growth in natural gas gathering and processing volumes. In the first nine months of FY 2022, the firm generated a total EBITDA of $490.0M, showing 102% year-over-year growth, the majority of which came from the Gathering and Processing North segment.

Source: CEQP

Crestwood Equity Partners: Outlook and valuation

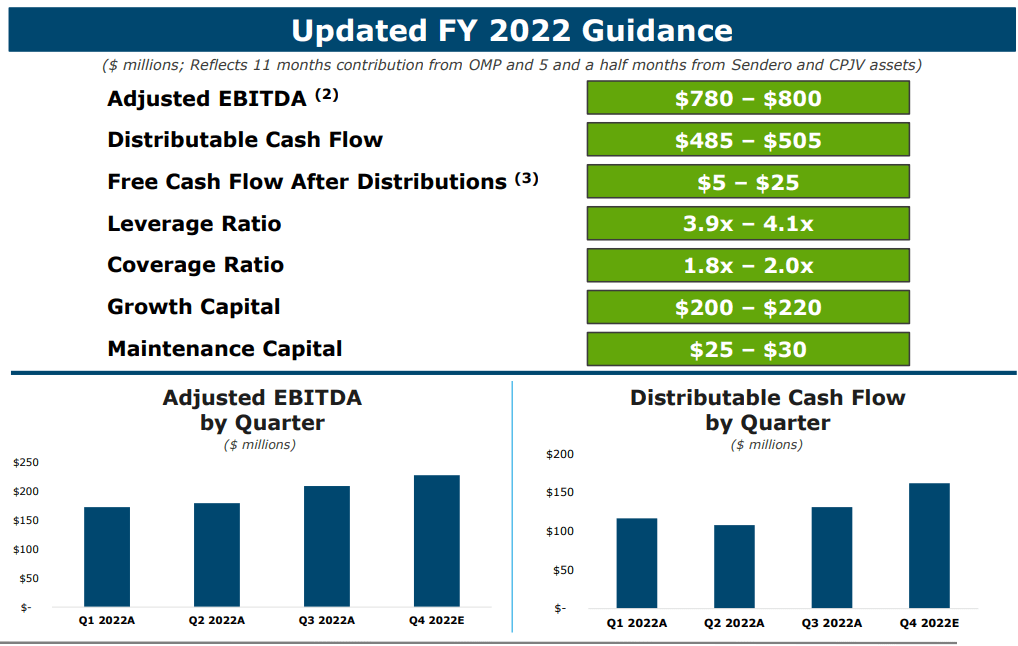

The midstream firm’s distributable cash flow is, like its EBITDA, on an up-swing due to past growth investments in gathering and processing capacity that are now paying off. Crestwood Equity Partners earned $355.8M in distributable cash flow in the first nine months of FY 2022, showing an increase of 27% year-over-year. The outlook for the full-year implies that Crestwood Equity Partners is set to add at least $129M to this balance in the fourth quarter. Crestwood Equity Partners has guided for $780-800M in adjusted EBITDA and $485-505M in distributable cash flow in FY 2022.

Source: CEQP

In the first nine months of FY 2022, Crestwood Equity Partners paid $196.9M in distributions to common unitholders and had distributable cash flow of $355.8 which translates to a discounted cash flow (“DCF”) coverage ratio of 1.8 X. The DCF coverage ratio in Q3’22 was even higher, 1.9 X. The full-year outlook calls for 1.8-2.0 X coverage, based off of distributable cash flow, which equals the strong distribution coverage ratio of 1.8 X of the much larger, more diversified Enterprise Products Partners.

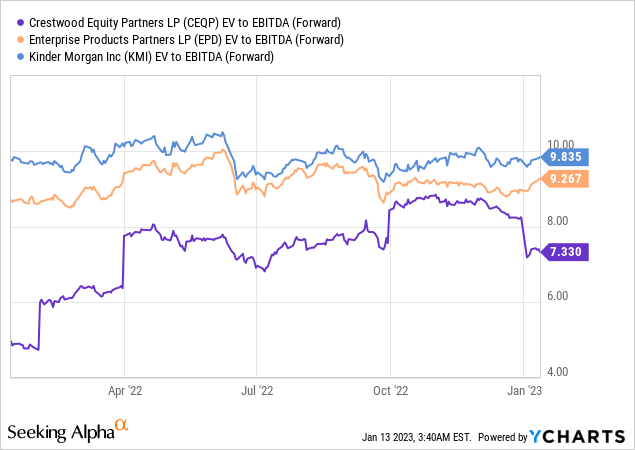

Crestwood Equity Partners also has a very attractive DCF-based valuation factor. With about half a billion in FY 2022E distributable cash flow, the midstream firm’s energy assets are valued at just 5.8 X DCF. Based off of EBITDA, Crestwood Equity Partners is also cheap: investors must pay 7.3 X forward EBITDA for the midstream firm while Enterprise Products Partners, a company 20 times larger than CEQP, is trading at an EV/EBITDA ratio of 9.3 X. Kinder Morgan (KMI) is also significantly more expensive on an EBITDA basis with a multiplier factor of 9.8 X.

Unit distribution yield

Crestwood Equity Partners raised its distribution to unitholders by 5% in Q1’22, compared to the year-earlier period, and the midstream firm’s units currently yield 9.5%. Considering that Crestwood Equity Partners projects to have a DCF-based coverage ratio of at least 1.8 X in FY 2022, I believe the distribution is very safe.

Risks with Crestwood Equity Partners

Crestwood Equity Partners is a smaller midstream firm and offers less diversification than other, larger midstream firms. With a less diversified asset base and 20% of its cash flow exposed to variable service rates, the midstream firm has therefore higher risks than midstream companies like Enterprise Products Partners or Kinder Morgan. Another risk I see with Crestwood Equity Partners is that the US government is not friendly to the fossil fuel sector which could hamper the growth potential of the entire industry and, by extension, hurt the firm’s prospects for distributable cash flow and distribution growth.

Final thoughts

Crestwood Equity Partners LP is a well-run midstream firm that is flying under the radar due to its relatively small size and less diversified asset base relative to its larger cousins in the industry. But that doesn’t mean the company is executing badly: Crestwood Equity Partners has strong distribution coverage which makes the distribution and the 9.5% yield very safe. The valuation, based off of DCF and EBITDA, is also attractive and it suggests that investors are currently getting a really good deal with Crestwood Equity Partners LP!

Be the first to comment