imaginima/E+ via Getty Images

Crescent Point Energy (CPG) is a NYSE and Toronto Exchange listed company that does business on both sides of the border. Like many oil and gas companies, this one has benefited from the strong commodity price environment. Unlike many companies, management made a pretty good-sized acquisition just before the rally really got underway. So, there could be more upside for this stock if the acquisition performs as expected in the future.

Crescent Point Energy Common Stock Price History And Key Valuation Metrics (Seeking Alpha Website March 1, 2022)

The stock price has more than doubled from recent low prices. That is a decent performance for a company that is the size of this company. But the market relies on a lot of company history. This company has a debt happy history that the current management has been trying to move away from. Debt levels were low enough to allow management to consider an acquisition that used some stock to keep debt ratios low.

Management will be announcing year-end results very soon. It is likely that the company is going to report a lot of operational improvements as well as benefits from strong commodity prices. That could encourage the market in the future. It also helps the relatively new management establish a very different track record from the debt happy days.

Any large acquisition takes time to optimize. It is not unusual for an acquisition of the size completed by this company to take about a year to fully integrate into the company operations. The nice part about using both debt and common stock is the ability to increase the operating leverage as the price of oil and natural gas rises. That could imply that investors could reap some unexpectedly good returns in the current fiscal year as long as the acquisition meets management goals.

(Canadian Dollars Unless Otherwise Specified)

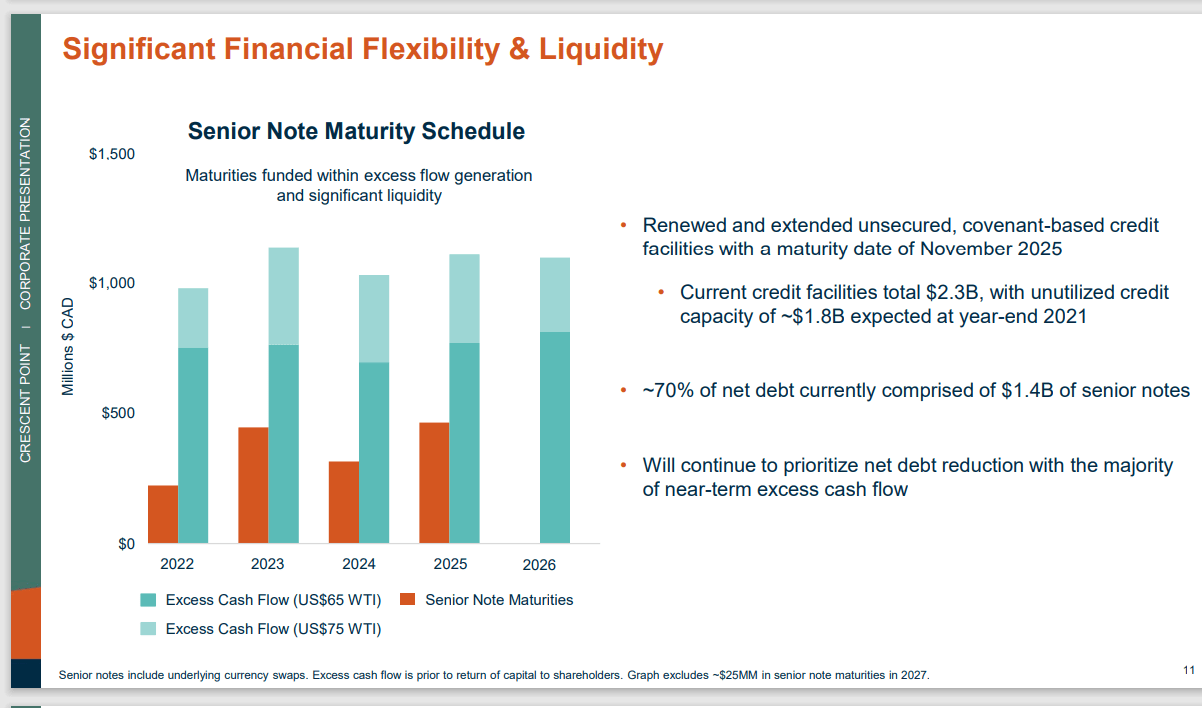

Crescent Point Energy Balance Sheet Improvement And Financial Options (Crescent Point Energy December 2021, Corporate Presentation)

The company usually keeps a fairly large unused credit line. This allows for considerable flexibility should the right acquisition opportunity present itself. It could well be that the proposed debt repayments combined with the credit line will position the company for future opportunities. That would allow the company to grow both through acquisition and organic growth. As long as the deals keep the debt ratio low, the financial risk to shareholders should be minimal.

Similarly, the management will adopt a fairly conservative dividend strategy by Canadian standards. Usually, Canadian companies that list on the NYSE do so because they gain access not only to more shareholders but also because the listing company may gain access to the American debt market (which is larger and more liquid).

But that means that the company generally adopts an American dividend strategy and shareholder returns policy. The dividend percentage of cash flow at less than 10% is therefore not unexpected. That low amount allows the company to maintain the dividend at a time of weak commodity prices. This also fits with the current strategy of repaying debt as it comes due so that the company has maximum financial flexibility to determine the best priorities for shareholders during an industry downturn. Extra cash flow will be diverted to share repurchases that can be discontinued should sales prices weaken considerably.

Canadian companies tend to return more money to shareholders during the boom times of the business cycle while cutting the dividend when the tougher times prevail. That strategy is unlikely to happen with this Canadian-based company for the foreseeable future.

Management has announced a new dividend for the current fiscal year of C$.045 per quarter. That is about a 50% increase from the previous rate. In conjunction with the distribution increase, the company has also planned a share repurchase program. One thing that needs to be emphasized is most share repurchase programs are done on an opportunistic basis. If the share price rises too much, then management may not execute the purchase of any shares. A share repurchase program, therefore, gives shareholders an idea as to whether or not management thinks the stock is properly valued or even overvalued.

Additionally, management raised the production guidance for the year. This management is conservative enough in their guidance that I would likely expect more upside guidance revisions to production as the year continues.

One of the things Mr. Market regularly ignores is the maintenance by management of the capital budget despite the accomplishment of decreasing well costs. This strategy has the effect of growing production through a few incremental wells without management admitting to any more production growth in the name of holding the capital budget constant.

Production growth is kind of “out of style” in the eyes of Mr. Market. It is more about maintaining production while returning excess cash to the shareholders one way or another. Yet production growth on an industrywide basis is clearly happening as it tends to in any recovery. It is being presented to the market as a surprise outperformance much of the time instead of a budgeted item. I find that rather fascinating.

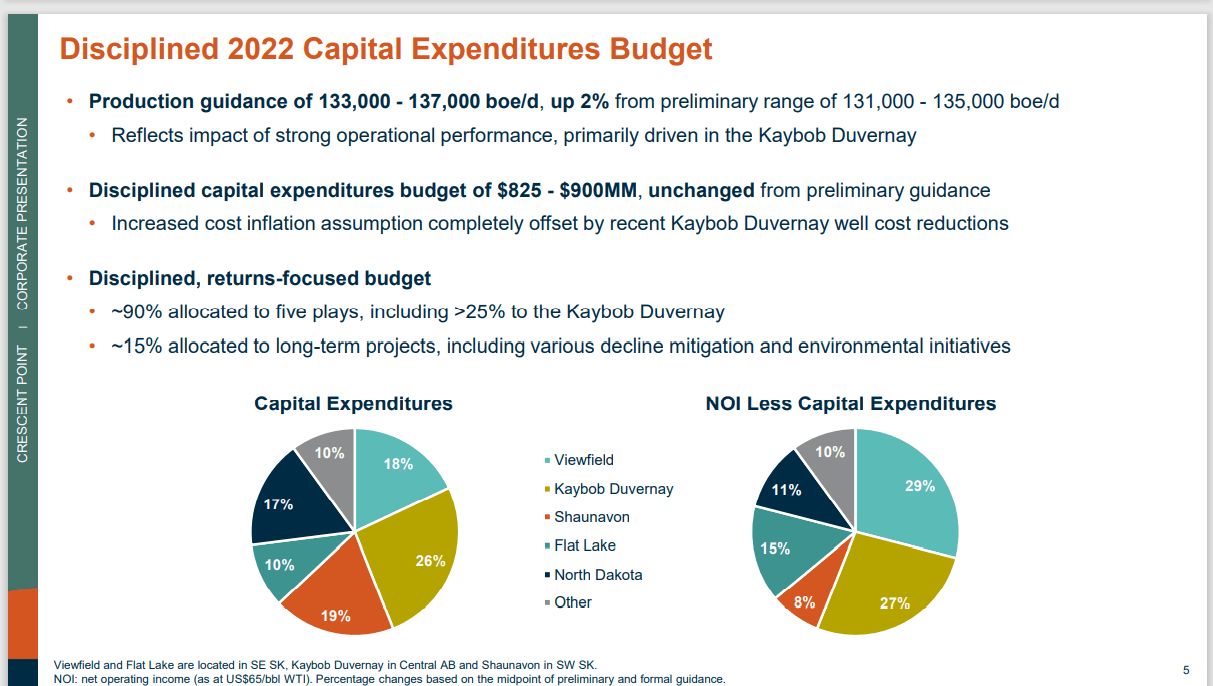

(Canadian Dollars Unless Otherwise Specified)

Crescent Point Energy Proposed Fiscal Year 2022 Capital Expenditures (Crescent Point Energy December 2021, Corporate Presentation)

This company has some low-cost secondary recovery projects. The low-cost part is highly unusual in the secondary recovery business. It is clearly the case here. That means that the company has a lower production decline rate because secondary recovery projects tend to have very low decline rates.

That gives the company a budget advantage should the management desire to raise production at a faster rate than shown above. Of course, management does boast about a lower decline rate than many companies in the unconventional business. But that is because management has a mixture of unconventional and secondary recovery businesses. It is not because they found a miracle way to reduce the unconventional decline rate in the first year of a well’s production.

Investment Safety

The relatively new management is pursuing several conservative strategies that considerably lower the investment risk when compared to many upstream companies in the industry.

The primary lower risk strategy relates to keeping the debt ratios far lower than they were a few years back. Mr. Market may want some more history before deciding to revalue the shares based upon the more conservative debt strategy. Such a future would not require management to do anything extraordinary. All they need to do is just keep doing what they are currently doing.

The second thing lowering the risk is the inclusion of some low-cost secondary recovery projects that lower the average corporate decline rate. A profitable low-cost secondary recovery business allows management to increase production while spending far less than the unconventional business requires. That potentially could turn out to be a long-term competitive advantage that shows itself as more free cash flow than the market would normally expect.

Even though the upstream part of the industry can be very volatile, this management has materially lowered the risk of total loss of principal. Therefore, this company may be a suitable buy and hold for those that want to hold the stock through the cyclical business cycles. Future growth is likely to be from both acquisitions and organic growth. Therefore, growth may occur when the market least expects it.

Others may want to sell the stock before the next downturn. For that reason, this stock may appeal to a wide variety of investors.

Be the first to comment