ricochet64/iStock Editorial via Getty Images

In our last analysis, we explicitly said that Crédit Agricole’s (OTCPK:CRARF) stock price was still lagging behind its closest peers, whereas our EU banking coverage with multiple buy ratings provided tangible results – i.e. UniCredit, UBS, and ISP were clear examples. Following the quarterly results of SocGen and BNP Paribas, today it is Crédit Agricole time.

Since our last publication (Dec-22), the bank was up by more than 22%, confirming our investment case which was supported by: 1) no exposure from Russia compared to SocGen, 2) M&A optionality with a particular emphasis on the Italian market where we believe there is a strong discount in our EU banking universe coverage, 3) strong acceleration in net interest margin development given the ECB interest rate hikes, and 4) the new strategic plan called ‘Ambitions 2025‘ which confirm our thesis on the “integrated bank-insurance-asset management business model“.

Mare Evidence Lab’s previous publication

Q4 and Italian performance

In Q4, the bank reported a clean net profit of €1.55 billion, beating consensus estimates by more than 50%. This was due to revenue acceleration and lower provisions. However, all the divisions outperformed, in particular, we should report insurance and large customer division performances. In detail, the former segment beat Wall Street estimates by €134 million thanks to stronger revenues, while the latter was up by €191 million thanks to margin development. It is key to report that Crédit Agricole delivered a strong commercial activity and gross customer capture was up by almost 2 million clients in retail banking.

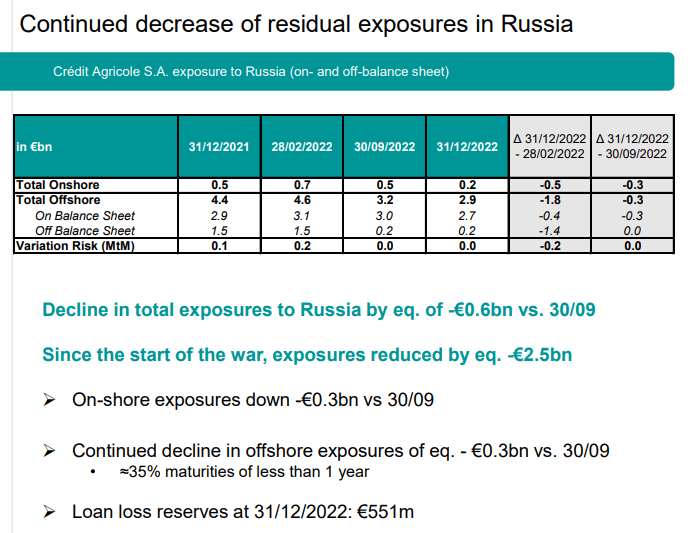

Looking at risk management, the bank’s cost of risk stood at €443 million compared to an average consensus of €580 million, while the CET1 ratio was up by 0.3% on a quarterly basis and reached 11% fully loaded. Even if the bank had lower exposure to Russian activities, they are continuing to decrease the bank’s country-specific liabilities. Speaking of numbers, Russia’s exposures declined to €2.9 billion with a provision of €551 million.

Crédit Agricole’s Russian exposure

Here at the Lab, in 2022, we published two detailed analyses on Crédit Agricole’s Italian optionality.

- Crédit Agricole And Its Italian Optionality: Part 1

- Crédit Agricole And Its Italian Optionality: Part 2

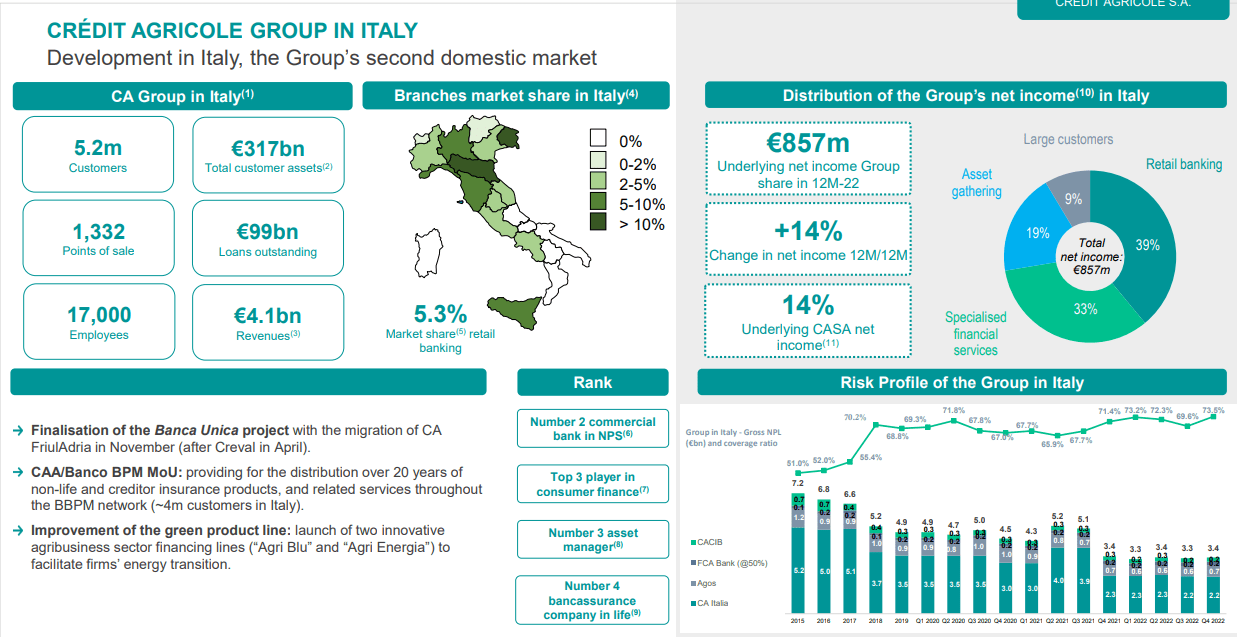

We are not surprised to see Crédit Agricole Italy’s performance (very much in line with our buy thesis). The Italian division recorded an aggregate net profit of €1.09 billion up by +11% year-on-year. Operating costs were slightly down compared to 2021 and the credit cost also decreased by 15.7%. More important was the net non-performing loans ratio evolution which fell to 1.8% and gross non-performing loans which stood at 3.3%. This was so supportive that Moody’s agency confirmed Crédit Agricole Italia with Baa1 negative outlook, a higher rating than the Italian banking system.

Crédit Agricole’s Italian development

Conclusion and Valuation

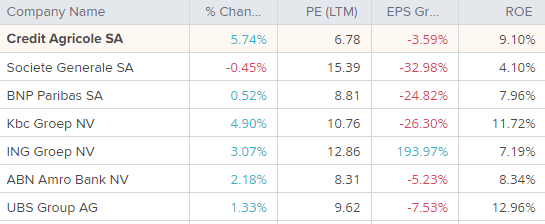

Crédit Agricole has better fundamentals and announced a dividend per share of €1.05 with a 50% payout ratio, plus a €0.20 per share still related to the 2019 dividend accruals. At the moment, it is yielding 9.42%. The bank also confirmed its 2025 financial targets and is still trading at a discount versus its historical average on the TBV (0.5x versus 0.6x). In addition, the company is still behind its peers on P/E and is trading in the first quartile based on ROE. We are not surprised to see a positive stock reaction (+5%), and we reiterate our buy rating at €13 per share.

Mare Evidence Lab’s internal estimates

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment