JERO SenneGs/iStock via Getty Images

Overview

CPI Card Group (NASDAQ:PMTS) is a payments and payments technology company. Its offerings include debit, credit, and prepaid cards. The company provides both the physical cards as well as the digital infrastructure required to have them work on payment networks. Customers for these products are entities such as banks, credit unions, and card processors.

Notably, CPI CARD Group has a leading market position in which it works with some of the largest card issuers in the United States. These marquee customers include JPMorgan (JPM), Bank of America (BAC), and American Express (AXP), all of which were listed in its prospectus for going public in Q4 2015.

sec.gov PMTS 1.6.22

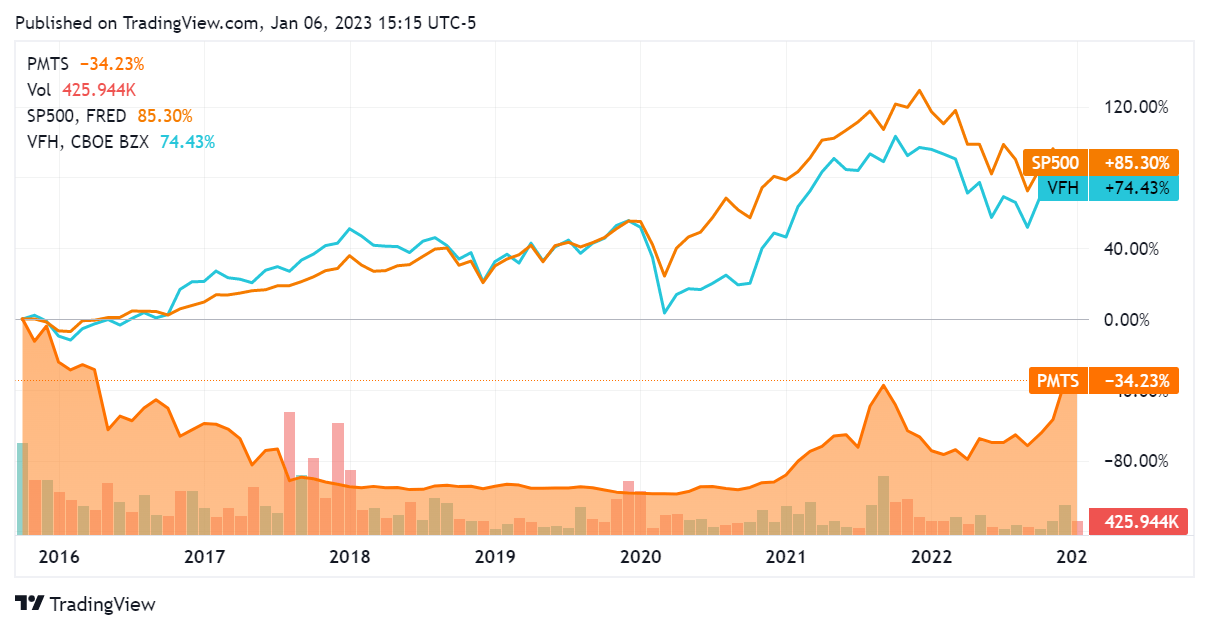

Since first going public in Q4 2015, CPI Card Group has underperformed both the SP500 and the financial sector as a whole (indexed by the Vanguard Financials ETF (VFH)).

SeekingAlpha.com PMTS 1.6.22

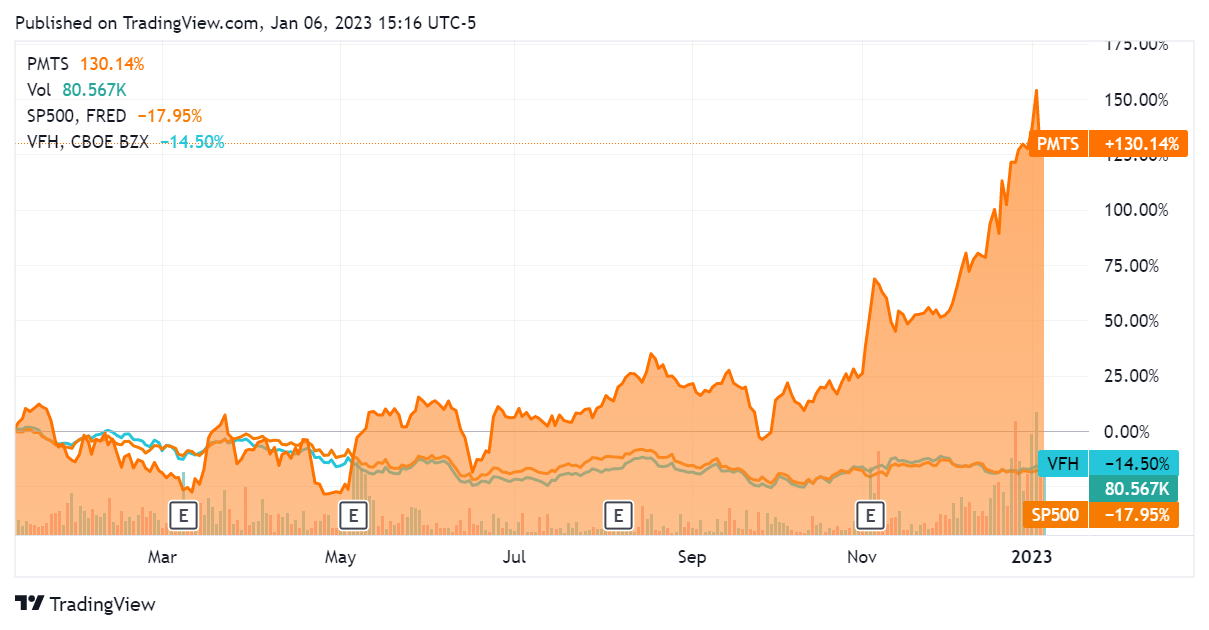

On a more recent timetable, CPI Card Group significantly outperformed both of these indices in 2022, posting returns of 130% over the past year while both the SP500 & financial sector showed double-digit losses. This strong countercyclical momentum indicates that there may be ongoing strength in the stock, which we will review through the lens of its financials.

SeekingAlpha.com PMTS 1.6.22

Financials

CPI Card Group has showed mostly consistent revenue growth throughout the last decade, albeit in a relatively volatile fashion.

SeekingAlpha.com PMTS 1.6.22

Fiscal years 2016 and 2017 showed significant YoY decreases in revenues, but the last 4 fiscal years as well as the TTM figure show continued positive growth. It is worth noting that the TTM figure shows a slowdown in growth; this is likely linked to the late stage of the credit cycle in which we are now in.

SeekingAlpha.com PMTS 1.6.22

These revenue figures occur against a backdrop of a company that is mostly profitable. The company saw negative net income in the years following a slowdown in its business but has posted 2 fiscal years of profitability since. Interestingly, the trailing twelve months net income figure is the highest that we have seen yet – even as revenue growth has slowed down.

SeekingAlpha.com PMTS 1.6.22

This may imply that the company is at the part of its growth cycle wherein it can generate consistent profits. This can usually be inferred by the retained earnings of a company moving in a consistently positive direction. Unfortunately the picture here is somewhat murky; the firm had a period of positive retained earnings in fiscal year 2016 but appears to have continued to aggressively funnel capital back into its business since then. As of its Q3 2022 filing, it is back in the black on this metric.

SeekingAlpha.com PMTS 1.6.22

The question now becomes whether this company can continue to grow its retained earnings and thus increase its fundamental per-share valuation; this is of course a question about its cash flow.

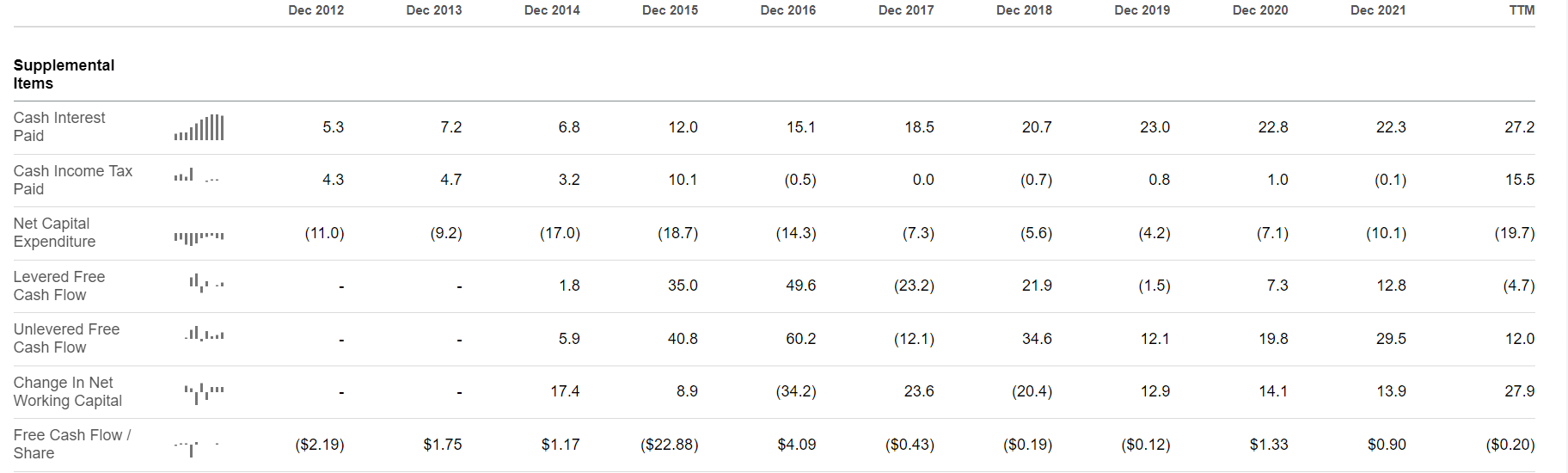

Here the picture is also somewhat murky. In line with revenue metrics, the company had very low cash from operations during its down years. While recovering somewhat since then, it is still posting a weaker trendline than it had during the first half of the decade.

SeekingAlpha.com PMTS 1.6.22

Looking further, we see the likely culprit: steadily increasing levels of cash interest payments. In line with the rising cost of capital, the latest figure has been the highest one yet. Indeed, the $27.2M that the company had to pay in Q3 2022 for interest appears to have been enough to make it cash flow negative – note that levered cash flow was -$4.7M for the last filing while unlevered cash flow was $12M. Essentially, the company’s level of debt service made it cash flow negative in its latest filing – certainly a point of concern.

SeekingAlpha.com PMTS 1.6.22

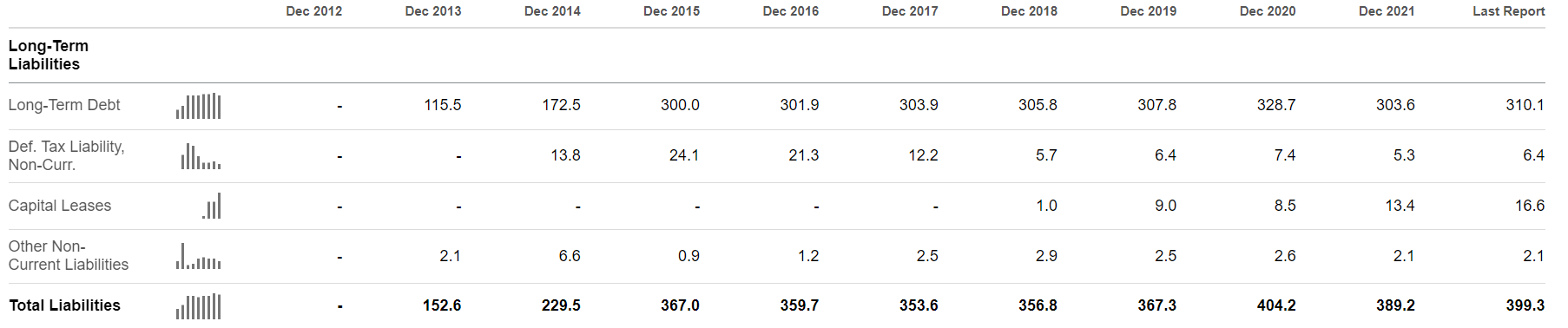

Worth noting is that this occurred even as the firms current and total liabilities has stayed relatively constant. The company is evidently paying more for capital borrowed, with a material impact on its bottom line. This is something worth looking at closely at the company’s next quarterly filing.

SeekingAlpha.com PMTS 1.6.22 SeekingAlpha.com PMTS 1.6.22

Overall, it would appear that CPI Card Group finds itself at an inflection point. It needs to generate more cash from operations in order to be cash flow positive, and it failed to do that last quarter.

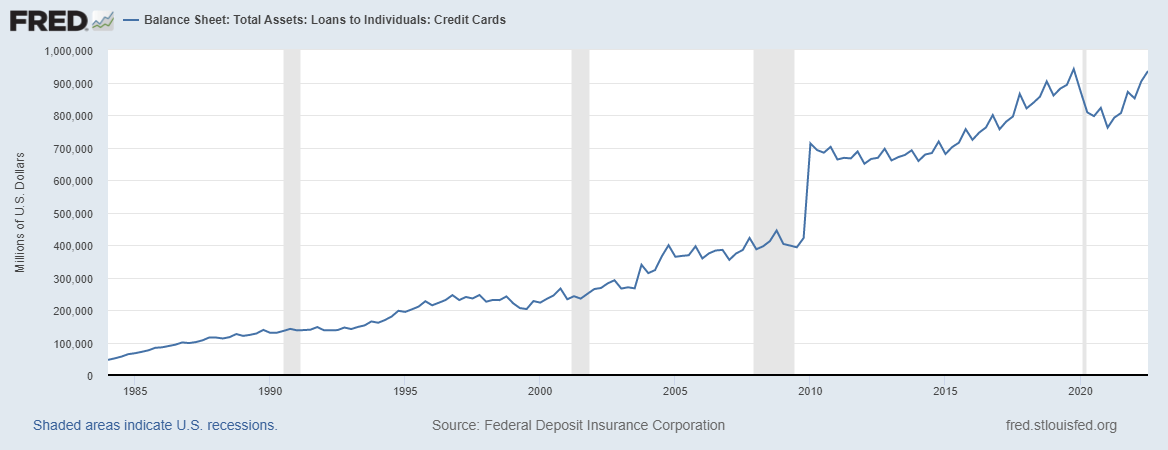

There are also significant secular trends affecting this stock. The first and most obvious one is rising rates, which are both affecting the company’s bottom line and may very well affect consumer demand for its products. More expensive consumer debt should imply a slower rate of card issuance – something we are already seeing in the latest quarter. Looking at the data for this, we see that consumer credit in the form of credit cards is at an all-time high (roughly equivalent to Q4 2019 at present). When it is already this high, of course there is less room to grow – all the more so as the economy is slowing down.

St Louis Federal Reserve 1.6.22

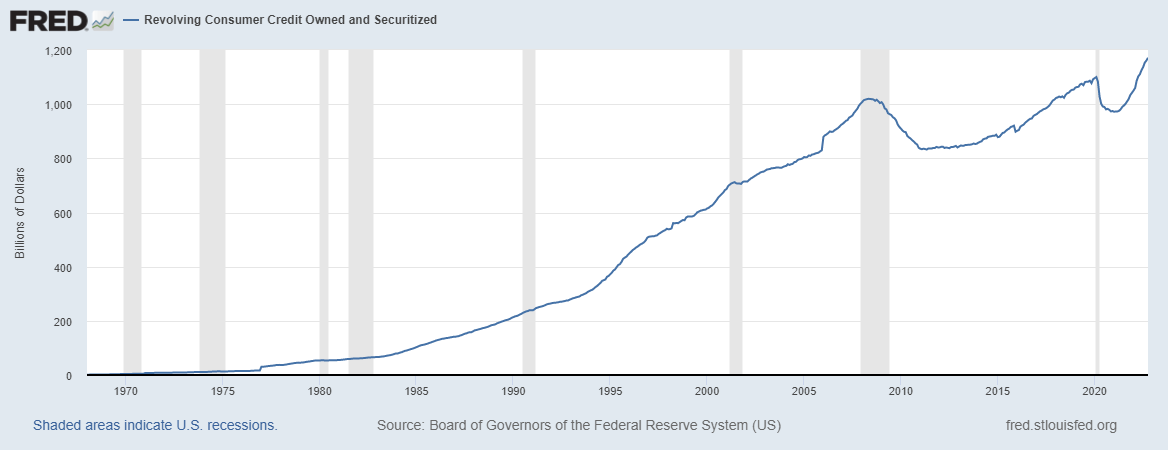

This becomes even more stark when we look at the total revolving consumer credit owned at present, which is very clearly at an all-time high.

St Louis Federal Reserve 1.6.22

Since the credit cycle sees maximum credit issuance when money is cheapest, with a drop-off thereafter, these charts present a point of concern from my perspective. Simply put there is that much less room to run when we are structurally at this point. This is a significant headwind that may offer a leading indicator for CPI Card Group’s business. It is fair to assume that credit card issuance and utilization will further drop off as debt gets more expensive and consumers have less wiggle room.

Valuation

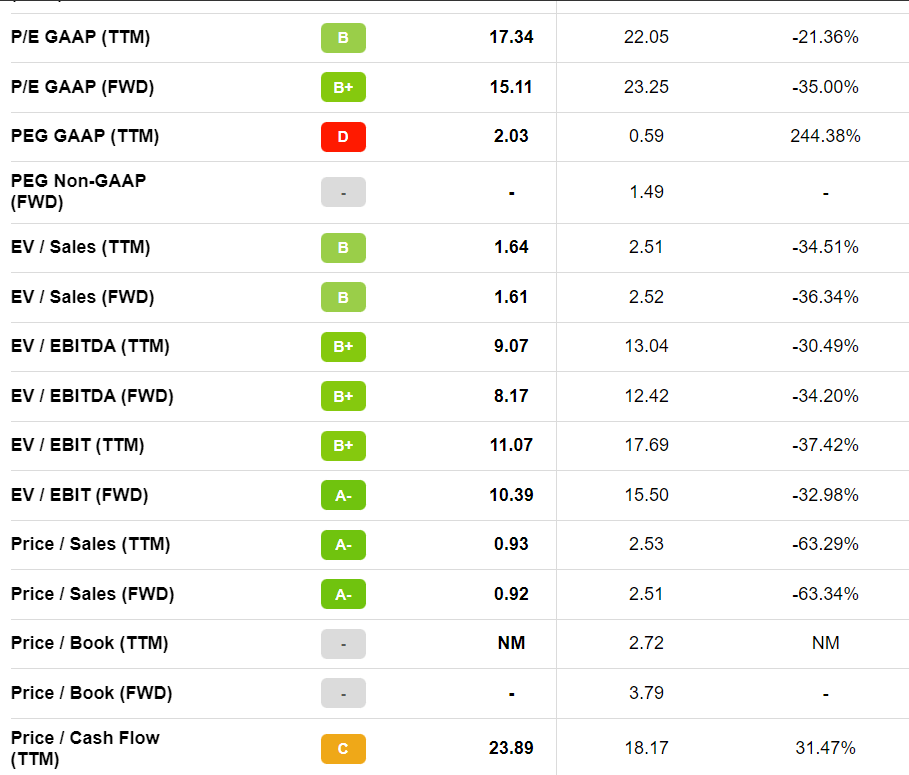

Even through its recent triple-digit appreciation throughout 2022, CPI Card Group is in the middle of the road as to valuation. At current prices it is below sector median as to its P/E multiple, but significantly above sector median when looking at cash flow. This company is technically part of the Information Technology sector, where P/E ratios tend to be high. Nonetheless the cash valuation is quite expensive – especially considering that this is far from being a ‘pure’ technology company. While they offer technology, their main business is simply printing cards. This doesn’t occur to me as a good price at which to enter this stock.

SeekingAlpha.com PMTS 1.6.22

Conclusion

While there are several good aspects to this business, notably its niche as well as its marquee client base, it doesn’t appear to be the best investment at this time. This is squarely due to its volatile and recently negative cash flows as well as slowing revenue growth. When we consider this in the context of the current economy, this slowdown makes sense.

I don’t expect CPI Card Group to outperform expectations in the following year (as it has this past year), and I think the stock is relatively expensive for the numbers that it is putting up. While the economic/consumer context may not totally destroy this business, it will act as a headwind for the foreseeable future. Yet, I am hesitant to outright call it a sell. The company is well-positioned in its niche and its customers will need to continue providing and printing credit cards. As I believe the next quarter will be indicative of how the company is performing in this new environment, I will call this a hold at present.

Be the first to comment