ClaudineVM

Dear readers/Followers,

I’m going to update my Covestro AG (OTCPK:COVTY) thesis, with the latest piece published around July. That means it’s been almost half a year since my last update on Covestro and my mid-sized position in the company.

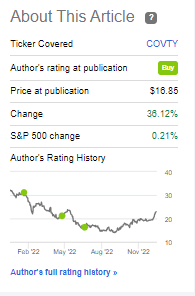

Covestro has outperformed the market.

Covestro Article (Seeking Alpha)

While it’s near-impossible to know how far down a market can push a stock, the fact that a stock is undervalued is something I believe myself to be quite apt at seeing. As the stock dropped, I slowly expanded my position in the company, building up a very decent ~1% position that is now up around 20% in total, including dividends and other considerations.

Covestro – An update

Covestro, if you recall what I’ve written before is the former material science division from Bayer (BAYRY). It’s not any sort of new company nor a group without experience – it has roots going back over 60-80 years, depending on what you look at, and while it has issues related to some of its legacy, it’s a very attractive business.

The company is a chemical/basic materials company with operations in polyurethane and polycarbonate-based materials, with end products such as isocyanates and polyols for what’s known as cellular foams, TPU polycarbonate pellets, and additives. End markets are found in the entire industrial sector. This is a basic materials company, which is a sector I’m going to be somewhat careful with this year because I believe headwinds will be significant. However, even after climbing 30%+, Covestro isn’t unattractive to me.

Covestro IR (Covestro IR)

The company’s end markets are across the board, and include Automotive, Construction, Cosmetics, Electronics/Appliances, Energy and Healthcare, as well as Furniture, Railroad, and Sports/Leisure. It’s easier to ask and say what the company doesn’t do than what it actually does, because virtually every industry on earth uses some form of the company’s end products.

I’m a pretty big investor in Basic chemicals and materials. My holdings include sizeable chunks of BASF (OTCQX:BASFY), Solvay (OTCQX:SOLVY), Wacker Chemie (OTC:WKCMF), Dow, LyondellBasell (LYB) and others active in similar fields.

A “good” basic materials company, to me, is relatively easy to spot – at least if we’re looking at fundamentals. What you want is:

- Vertical integration

- Scale

- Global Customer Base

- # of Patents and technologies

- Feedstock hedges/sourcing stability

- Balance sheet quality

If these qualities are fulfilled, it’s my experience that a company will have a good dividend and the right sort of circumstances for long-term outperformance.

The company has been listed since 2015, and Bayer sold its remaining stake in Covestro around 2018, with the company’s pension fund having a 6.8% stake that’s managed separately.

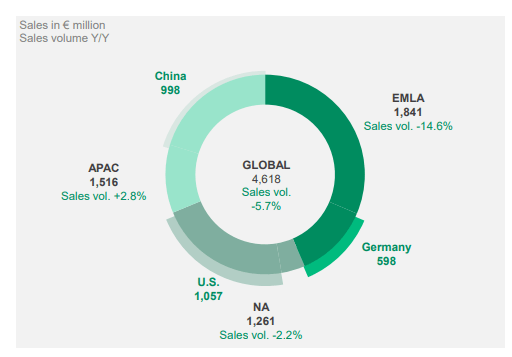

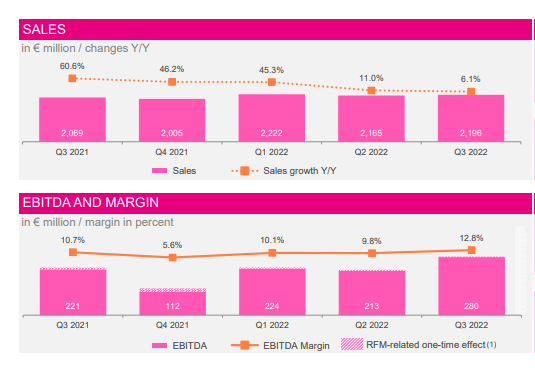

The latest results for the company are somewhat of a mixed bag, despite the recent outperformance. The company generated €4.6B in sales for the quarter of 3Q22, out of which €302M was EBITDA, narrowing its 2022 guidance range.

However, there were continued volume declines on a global basis, even if APAC saw some recovery.

Covestro IR (Covestro IR)

This was mostly due to the overall environment in Europe, which the company is already characterizing as recessionary, with declines mostly across the board – except automotive and transport, which is seeing an upswing.

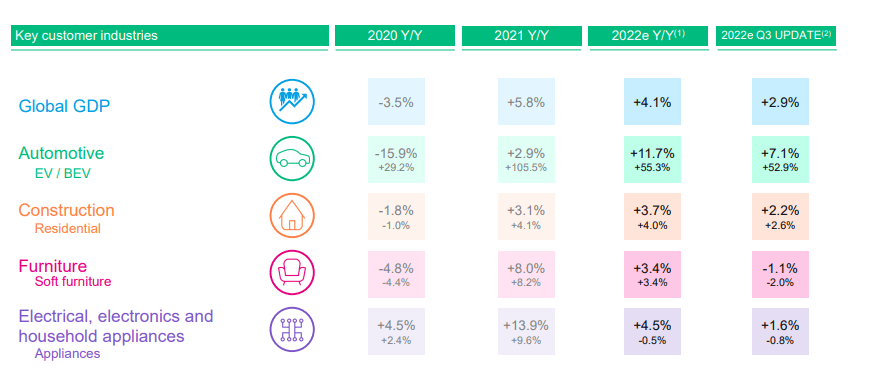

However, globally and going forward, the company is expecting slowing demand for its products, in line with the global GDP forecast. Covestro remains a cyclical business, so GDP growth or lack of it is a serious impact here.

Covestro IR (Covestro IR)

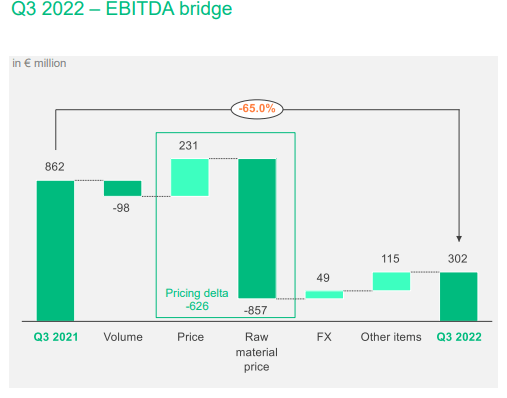

The company sales growth is a function of bumping prices and FX – in terms of volume, things are actually down almost 6%. The only positive that can be garnered here is that the company’s sales prices are being accepted by the customers, which led to those impressive sales – but also contributed to lower overall earnings, meaning more than a halving of the company’s EBITDA.

Covestro IR (Covestro IR)

You can see the impact of input materials, which despite price increases on the sale side really couldn’t weigh up the profit/loss side of things, resulting in a negative pricing delta which I view as unlikely to go away soon. Remember though, this negative delta is something I have been forecasting in my articles and forecasting models for this company. It’s neither unexpected nor “odd” as such.

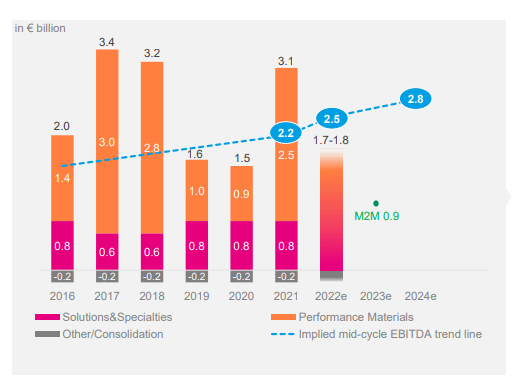

Performance Materials saw the hardest impact, with EBITDA going down significantly, almost negative and margins down to 3.2%. Solutions & Specialties was the star of the show during the quarter, showcasing instead very positive overall trends across the board, even increasing its margin levels YoY, even if sales were down slightly. It goes to show you, it’s about the quality of the sale, not the sale itself.

Covestro IR (Covestro IR)

The company has kept paying dividends though, despite these issues. This has weighed down net debt in a time of pressured FOCF, and resulted in a higher net debt up to €3.15B. Covestro remains committed to IG, and still has IG under its belt – so no near-term worries there.

The company also narrowed guidance.

Covestro IR (Covestro IR)

The main impacts for Covestro remain the very high energy costs, with the current recessionary and complex environment impacting things heavily. The company uses mid-cycle implied trends (the blue line above) to clarify that it sees EBITDA standing at about that level for the foreseeable future – and this is a level I more or less agree with, and also expect – it’s a level I’ve been more or less working with for the past year or so, and FY22 EBITDA is expected to be higher than FY21 – by quite a bit, as it happens.

Global energy costs have tripled within 2 years. That’s not something any company can be expected to handle with ease, or even with difficulty. It’s a massive impact that has changed the cost structure for a lot of companies, not just Covestro.

Despite all those difficulties though, I believe it fair to say that Covestro has actually hit most of its goals. Continually higher sales, EBITDA within the guidance range, positive FOCF despite challenges (an absolutely massive advantage), narrowing EBITDA guidance, and, as the company has wanted to do, focusing more on ESG and circularity.

Let’s look at the updated valuation.

Covestro – The valuation

Covestro’s valuation still reflects the overall basic forecasts in the sector, but also the current pressure the industry is under. I believe that based on current supply chain tightness and pricing environments, Covestro is still quite likely to outperform YoY in 2022 and 2023, and deliver its mid-cycle targets.

My own long-term growth rate in my forecast models still comes to around 2% on the high end in my DCF model to reflect GDP growth as well as the cyclicality of the business. I’ve also discounted the company’s peer-average multiples by 8-10% to reflect this cyclicality further – so take all of the numbers that are about to be written, and consider them highly discounted.

Regardless of how you twist around and discount Covestro though, you can really escape the conclusion that the company remains undervalued here.

The native 1COV ticker trades at around €42.8 at this time, which is still a 25% negative decline over a 1 year period. We’ve seen the lows at around €30/share, and while analysts have had a target of €70/share less than a year ago, 19 analysts are still coming to an average around €42/share, meaning the company is fairly valued here. Still, 10 out of 19 analysts are either at a “BUY” or an “Outperform” rating for this stock, and when we look at multiples, the company is still being traded on the low end of its historical spectrum.

With 0.5x sales and revenue multiples of 0.6x, as well as a P/E of around 8x, it’s trading at a discount to its peers. Companies in the same field include the ones I mentioned, and even BASF trades closer to an 8-10x EBITDA multiple on a normalized basis, with companies considered “high quality”, like Sherwin-Williams (SHW), L’Air Liquide (OTCPK:AIQUY), Corteva (CTVA) trading at significantly higher multiples. Even LYB is around 8-9x here, with Covestro still below 8x. Revenue multiples should not even be compared. Despite how cheap Dow is, Covestro’s revenues are being incredibly discounted here – less than a sixth of SHW’s at this time.

So my basic thesis for Covestro remains – it’s undervalued.

The ADR for Covestro is COVTY, which is a 0.5X ADR, meaning every ADR is half of a native share. This ADR is somewhat thinly traded, so the best option is investing in the native stock, if at all possible.

I expect a full valuation of no less than €70/share, and I target a significant RoR including dividends here. Once the company delivers this, I will reassess this investment and look at the market situation we’re in at that point.

But that may take time.

Here is my continued thesis for Covestro.

Thesis for Covestro’s Common Share

- Covestro is a cyclical but qualitative chemicals company in key industries – and it’s being incredibly undervalued at today’s prices. Despite recovering over 30% since the relative lows we’ve seen, Covestro remains incredibly undervalued to peers, and as I see it, to its forecasts.

- Because of this, I give the company a PT of €70/share at this time – unchanged since my first article on Covestro – and go for a “BUY” here.

- While this investment requires significant degrees of patience and tolerance, I believe the potential eventual outperformance could be nothing short of amazing.

- However, there is an alternative play for Covestro here – the options one, and that one may be attractive as well.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria, making it relatively clear why I still view it as a “BUY” here.

Thesis for the Options

There are options available for Covestro. I would go so far as to say that Covestro lends itself well for options play, because of its volatility. The only issue is that it very recently saw a massive rise, which could also mean that we’re in for a dip, which might defeat the near-term purpose of the following cash-secured put, because it might be a very high probability of being assigned.

Keep in mind that Covestro has a well-established history of “doing the dip” as well as the climb quite clearly.

Covestro, Interactive Brokers (IB)

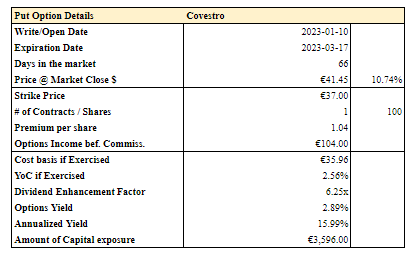

So, here’s the put I found for March.

Covestro PUT (Author’s Data)

Not exactly a bad put, but there’s a bit of volatility involved here. €37 wasn’t at all long ago that we saw – so be careful with this one.

For now, I’ll stick with my common shares for Covestro.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment