Eva-Katalin

Investment Thesis

Coursera (NYSE:COUR) maintained strong growth momentum in the latest quarterly results. However, it is still overvalued due to negative EBITDA and operating income. We don’t think the stock has reached its bottom yet.

Company Overview

Coursera was launched by two Stanford professors, Andrew Ng and Daphne Koller, in 2012. Both of them are experts in Artificial Intelligence and Computer Science. After teaching their very popular classes in the classroom and online with many followers, they started expanding the platform to cover more content in the technology space. The company now has over 275 leading university and industry partners to offer a broad catalog of content and credentials, including courses, specializations, professional certificates, guided projects, and bachelor’s and master’s degrees. Its platform has three business segments: Consumers, Enterprises, and Degrees.

Strengths

Coursera went public at $53 per share on 3/31/2021 and has been on a downward trajectory for most of the time since then. Currently, it is priced at around $13’s, only valued at about 20% of its IPO valuation. Has it reached its bottom? When will it become a screaming buy?

When you think about the customers that are taking classes on Coursera, you are probably thinking about someone more or less as pictured above – male in the 20-35 age group, into tech and artificial intelligence, and potentially has the other skill sets that they want to combine with the improved tech skills they learn from Coursera to seek a higher paying job. The keywords here are “high-paying” and “tech”. From the recently passed CHIPS ACT, we can expect the next few years, the U.S. will need even more high-tech workers to develop all aspects of the tech sector. Coursera is well-positioned to cater to that demand.

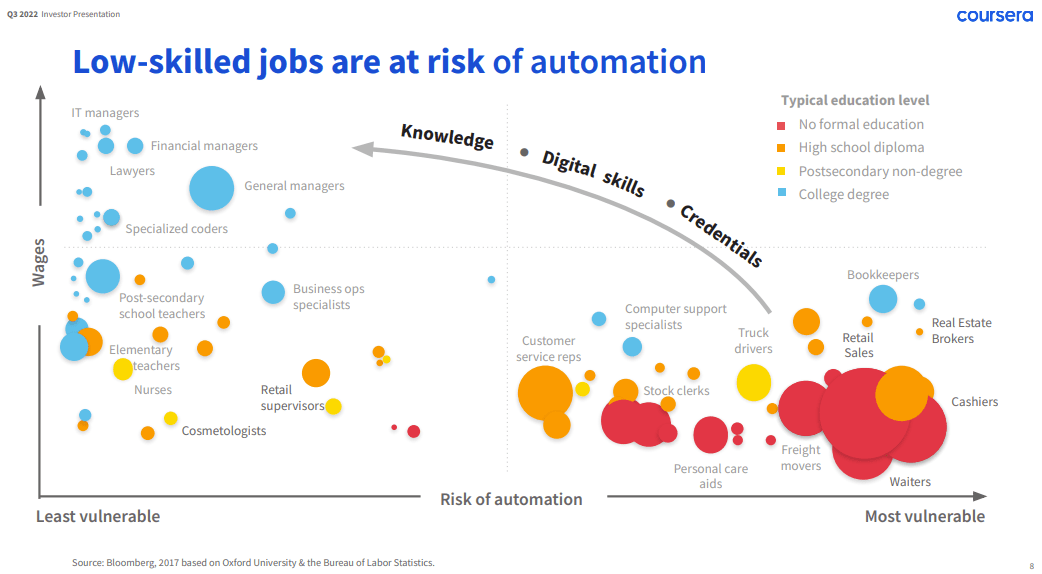

Coursera has some of the best content in the Tech Ed space, as it not only has some cutting-edge courses in tech but also partners with solid academic programs from university partners and leading industrial tech brands to diversify the resources available to learners. It positions itself in two ways to disrupt the education space: continued professional education and formal-degree education. The big picture is that the company presents its platform as a disrupter to the education space largely from the demand to upskill the workforce that otherwise would be at risk of losing jobs due to automation. It can be shown in a chart from its Q3 investor presentation. (See Chart Below).

Coursera: Job security vs Automation (Coursera Q3 Investor Presentation)

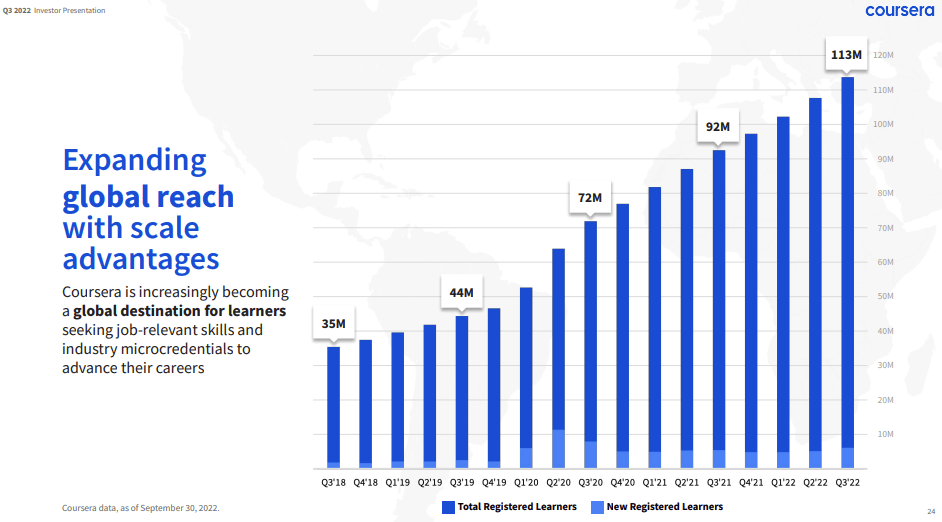

Coursera has developed a global footprint in its customer base. Mostly OECD countries or high-growth emerging market countries that contributed to its overseas expansion, such as Australia, India, France, Germany, Mexico, Turkey, the UK, and the US. The benefits of this customer base can be seen with a scaling effect from the number of registered learners below.

Coursera Number of Learners Growth (Coursera Q3 Presentation )

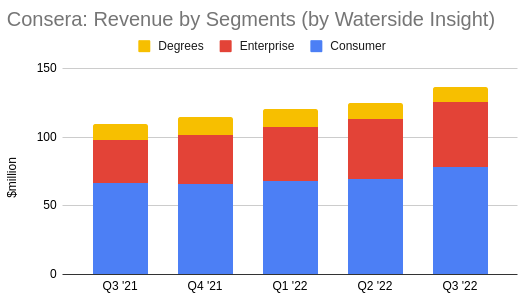

Most learners go to Coursera for reskill, upskill, and career advancement. In the Consumer segment category, both the revenue and margin are growing every quarter since. This is the biggest revenue driver of its growth. In this segment, learners can access freemium content, courses, and certification programs with job-relevant, hands-on projects. Overall, the combination provides a price-to-cost effect for learners to choose from.

In the Enterprise segment, Coursera has a large network of corporations and universities participating in their programs. Through the Coursera Campus Response Initiative, more than 4,000 colleges and universities used content from its platform to launch online learning programs that ran for free through September 2020. And it has most of the leading universities in the U.S., such as Stanford University, MIT, and Harvard, associated with its online learning content or certification programs. Altogether, the company has over 275 university and industry educator partners in paid content programs. This core partnership is in a healthy growth trend.

To bridge these two largest segments, Coursera introduced “Career Academy”, an institutional offering that brings together Professional Certificates and guided projects into a solution that businesses, governments, and campuses can deliver at scale to help individuals with no college degree or prior work experience start a new career or switch careers into an entry-level digital job. These are the efforts the company has been making to promote more organic growth. It has experienced continued growth in its revenue every quarter since its IPO.

Coursera Revenue by Segment (Charted by Waterside Insight with data from Coursera)

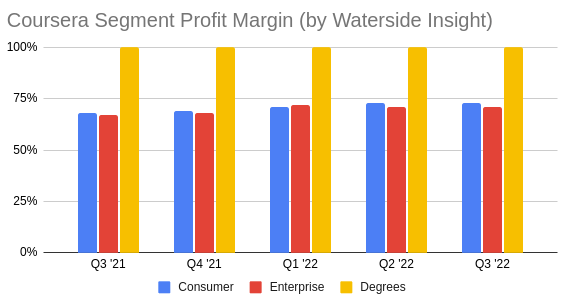

The profit margin of the Consumer and Enterprise is around 67-73%, respectively. Because the Consumer and Enterprise segment have borne the costs, the Degrees segment’s profit margin can be counted as 100%. So the net growth in this segment can be counted as the net growth of the total margin. This advantage was much discussed in its Q3 earnings call.

Coursera Segment Profit Margin (Charted by Waterside Insight with data from Coursera)

The question here is whether the Degrees segment has its unique growth path. The portfolio of its online degrees has been expanding every quarter, and it has branched out of only technological content to also include business & management, Cybersecurity, and public health as of late. The global higher education market was estimated to be at a size of $2.2 trillion in 2019, according to HolonIQ Smart Estimates. As Coursera explained in their 10-K, they carefully select top-tier educator partners, prioritizing quality, subject expertise, and geographical appeal. So far, the growth has been fluctuating. We want to see how Coursera differentiates itself from other online degree-offering platforms and increases its market shares.

Coursera Degrees Programs Portfolio (Coursera Q3 Presentation)

Weakness/Risks

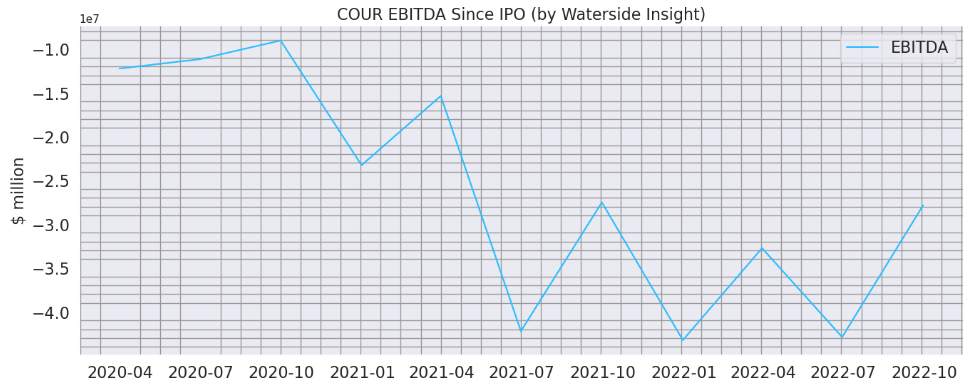

The biggest risk is obviously the negative EBITDA that Coursera has been having. The company’s EBITDA has been in negative territory since its IPO. With its revenue growing every quarter, so are its operating expenses. Although recently, it seems the bottom of the earnings downward trend has been reached.

Coursera EBITDA (Charted by Waterside Insight with data from Coursera)

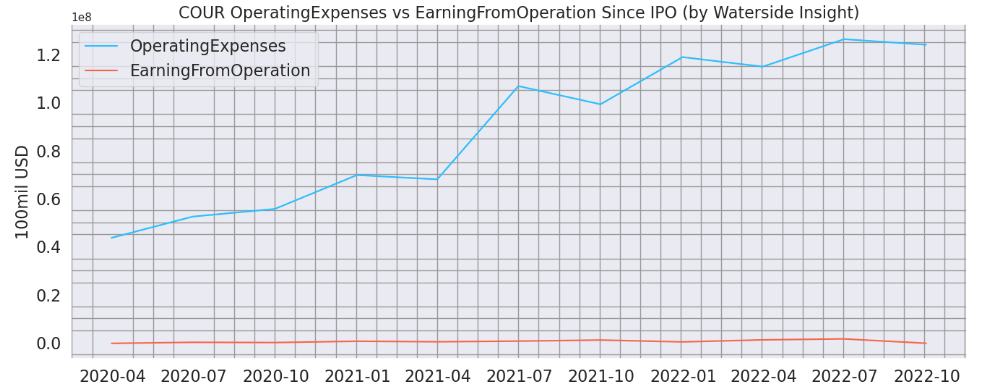

In Coursera’s Q3 earnings call, it mentioned that the QoQ margin expansion was due to learners consuming a larger proportion of industry-partnered content, which has a lower cost to Coursera as it’s part of promoting partner brands in its sales and marketing efforts. It is good to see the company looking to combine its different parts of a revenue stream for organic growth, but it still has a lot of work to do in terms of balancing expansion and cost control of the operation. Its Earnings from Operations remain stagnant while Operating Expenses have been growing. It remains to be seen if the expenses are front-loaded to lay a long-term foundation that will yield sustainable growth in the future or if the operation needs to spend more than it earns continuously.

Coursera Operating Exp Effectiveness (Calculated and Charted by Waterside Insight with data from Coursera)

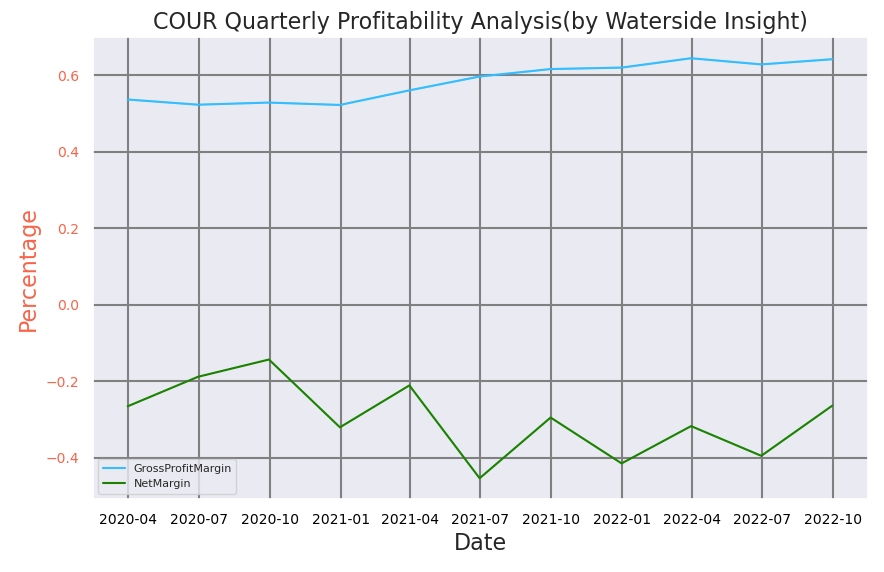

The upside potential of the company should come from an organic growth that combines all segments to create a virtuous cycle: the learners access freemium and then upgrade their skills with content from both universities and companies that help them get higher-paid job offers, which in turn, they use more of Coursera’s program to continue learning and improving, such as enrolling in degree programs or provide enterprise leads, in a way that builds brand recognition and resulting in more learners and more high-quality contents. So far, its upsell ratio was over 60% of the registered individual learners in 2021. While its Gross Profit Margin has been at a similarly high level of 60-70%, its negative Net Profit Margin has been gradually improving. When layoffs come as the byproduct of slower economic growth, would Coursera prove to be gaining traction among the job-seekers? Or does the higher cost continue to erode its bottom line?

Coursera Profitability Analysis (Calculated and Charted by Waterside Insight with data from Coursera)

This is why we asked the question, is the bottom near?

Financial Overview

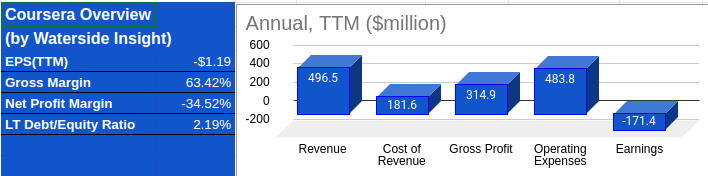

Coursera reported a net loss of $0.25 per diluted share, compared with a loss of $0.23 per share a year ago. The company’s revenue increased by 9.3% QoQ to $136.3 million, up from $109.0 million a year ago, maintaining a consecutive growth trend. The company’s levered free cash flow was at $14 million in Q3, which continued a recovery trend from the negative cash flow in Q1, although it is a 7.8% decline from Q2 and a 40% decline YoY. Its net change in cash was an increase of $44.8 million, 2.39 times more than the change in Q2. And it has a current ratio of 3.77 times. It reported a Net Income of negative $36 million, although better than the negative $49.3 million in Q2. Its Debt-to-Equity ratio remains low at 2.19%, more or less the same level since its IPO.

Coursera Financial Overview (Calculated and Charted by Waterside Insight with data from Coursera)

Valuation

Incorporating all the analysis above, based on our proprietary models to project a ten-year growth for Coursera, we assessed the fair value of its stock price. In our most bullish case, the company is maintaining its growth momentum into 2023 without much impediment from the economic slowdown and keeping steady growth with costs under control, it is priced at $9.65. In our most bearish case, where it got hit on both growth and costs fronts next year but recovered to a higher growth rate, it is priced at $5.89. In our base case, it will attract a growing number of learners in 2023 with cost control still a challenge, and it can gradually become more profitable; the company is priced at $7.48. In all scenarios, it is overvalued at the current mid-teen price range.

Coursera is still a very small company with the landscape it is trying to disrupt. It is a busy space with many competitors with different competitive advantages. But Coursera has one thing that stands out from others, and that is its in-house expertise in Artificial Intelligence and related subjects. Its founders have contributed to bringing this subject en masse with online programs during the past ten years or more. What we will buy into is the company can solidify its leading position in this niche field with great potential to branch out to disrupt the whole online learning space. And the price premium from this vision is incorporated in our valuation. The company has managed a reasonable balance sheet without excessive debt while maintaining sufficient liquidity and growth momentum. It is not unimaginable that it could become more profitable in the near future. In our opinion, that will come from it providing more high-end, quality content than other LPMS (Learning Platform Management Systems) and growing a strong ecosystem with a healthy cash conversion cycle.

Conclusion

Overall, we see Coursera has great potential but also with necessary infrastructure spending overhead to build out a differentiable content portfolio. It has been doing a good job at maintaining growth momentum, a reasonable balance sheet with sufficient cash, and low debt. However, the catalyst for the stock’s upside hinges on whether the cost control would be effective while maintaining the growth momentum. For investors looking for a better entry point post-sell-off, we recommend waiting until the price comes down to $9.65 or lower.

Be the first to comment