Difydave/iStock Unreleased via Getty Images

Investment Thesis

Corsair (NASDAQ:CRSR) has not done a good job of projecting their business growth. The company missed its bottom line expectations. On the top line, reported revenues slid over a heavily reduced projection. Management then cut guidance for the company’s top and bottom lines.

I believe a turnaround may be possible. Unfortunately, a high valuation and the risk of dilution make me want to avoid this stock.

Poor results and a heavy guidance cut

Corsair’s latest quarterly results were a disaster. The company reported sales of $294 million, down 40% year over year. Adjusted EBITDA was negative, and the company lost $0.62 per share during the quarter.

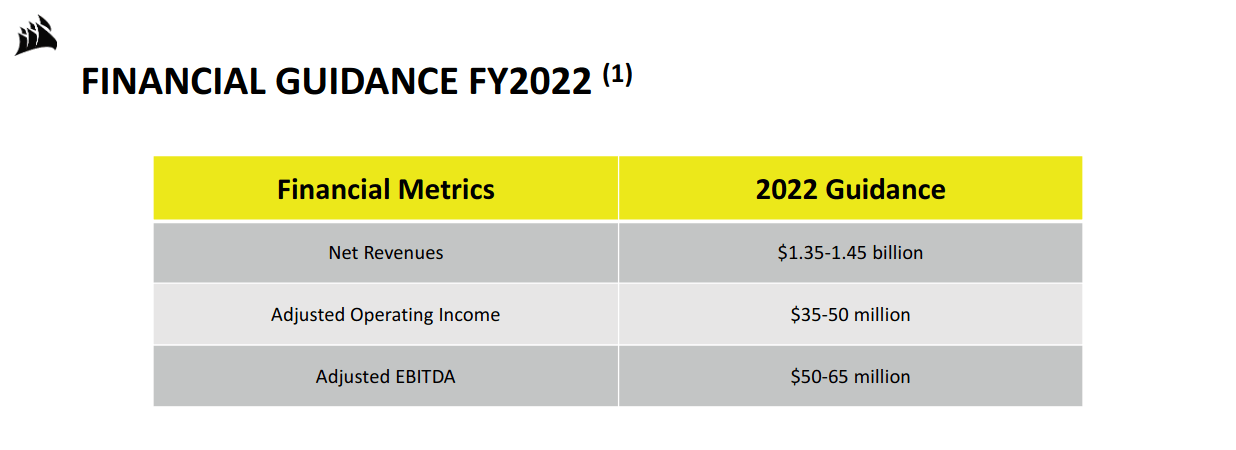

Corsair Q2 2022 Earnings Presentation

The company slashed revenue guidance to a range of $1.35 to $1.45 billion. This is down 30% from their Q4 2021 guidance. Adjusted EBITDA guidance was cut to a midpoint of $57.5 million, down almost 75% from six months ago.

The largest declines were in the company’s peripherals segment. This is Corsair’s most discretionary segment. Sales were down 43% year over year and by one third quarterly. The computer components segment also reported poor results. Revenues dipped almost 40% year over year and 21% sequentially.

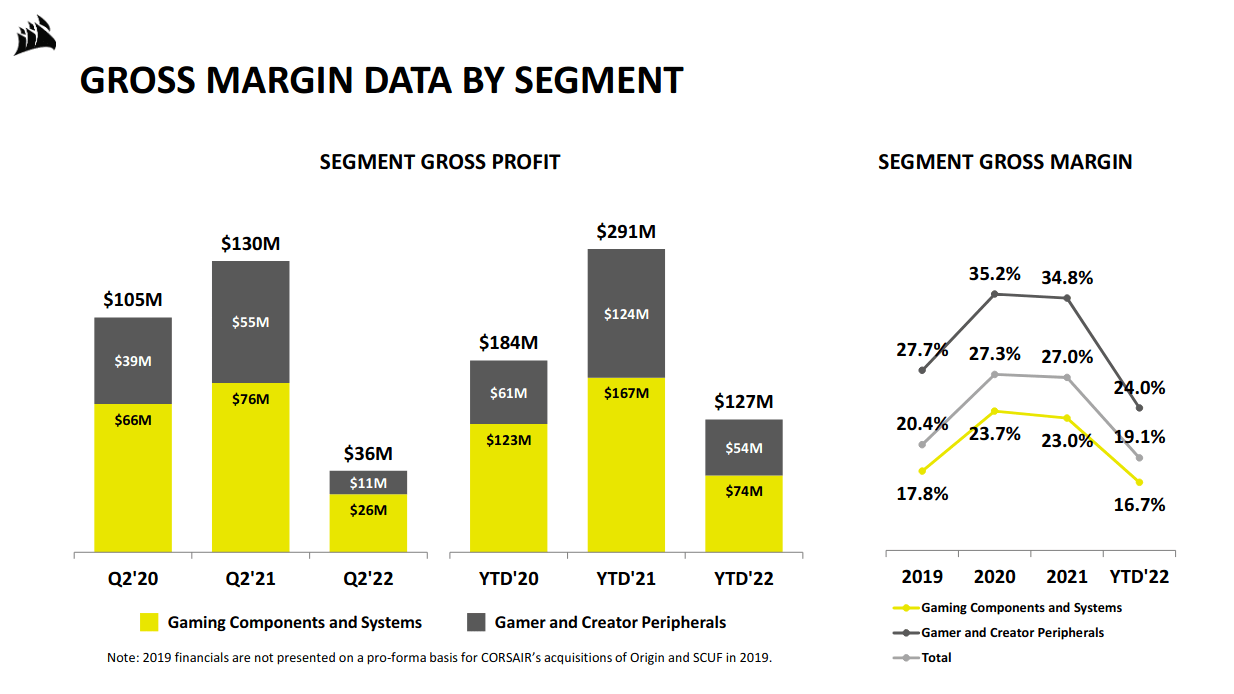

Corsair Q2 2022 Earnings Presentation

Corsair reported a total gross margin of 13% in the last quarter, its worst ever reported result. These margins are less than half of what they were during the same quarter last year. Across the business, the peripherals segment was the hardest hit. This is traditionally Corsair’s highest margin business. The segment’s gross margins tanked from over 35% to just under 12% year over year. This bottom line pressure pushed the company to lay off employees and cut operating costs.

Corsair’s balance sheet isn’t good

Corsair has a large inventory excess on its books. As of their last 10-Q filing, there were 109 days of inventory on their balance sheet. This is the highest number on record. Worse, supply gluts and demand downturns are causing issues across the industry. Management reports that competitors are issuing heavy discounts on their products. This added market pressure could further hurt Corsair’s top line.

The company’s net debt profile isn’t great, either. Corsair has $36 million in cash on hand and $240 million in long term debt. Most importantly, the interest on this debt is variable. As interest rates continue to march higher, the cost of the company’s debt will increase too.

It seems like management is setting the stage to dilute the company’s shares. The lack of cash on the company’s balance sheet makes it likely they’ll raise new capital by issuing equity. The midpoint of management’s guidance implies a 7% increase in shares outstanding between now and the end of the year.

Shares are still expensive

Corsair’s shares are down 70% from their lockdown highs. I still think they’re kind of expensive. Even during the last fiscal year, the company was free cash flow negative.

The business trades at a forward EV to adjusted EBITDA of 26. Forward EV/Sales is just under 1.1 times, which seems high for a business with this gross margin profile. The prospect of double digit annualized dilution makes this an even riskier play. I think that shares are expensive and pricing in a strong long term comeback.

Is there a light at the end of the tunnel?

While the short term outlook is poor, I want to assess Corsair’s long term prospects.

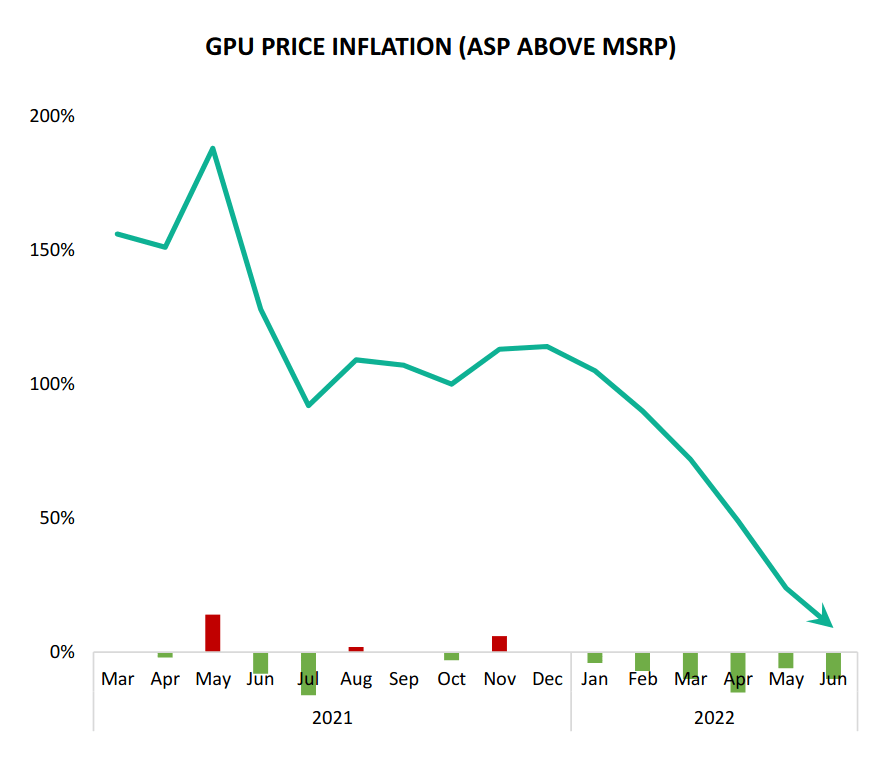

The company has pointed to a shortage of GPUs as a key factor holding back demand. GPUs are a key component in high end PC builds. Management has repeated that they expect this to be a major growth driver when the shortages end.

Corsair Q2 2022 Earnings Presentation

GPU prices have now returned to more normal levels. The company discussed this decrease on its earnings call.

We expect that the second half will show improvement over the first half, but at lower levels than we expected at the start of the year. In particular, GPU prices have moderated and GPUs are generally available now to our end customers. That coupled with the expected exciting product releases from us for our product lines, plus new AMD motherboards and NVIDIA GPUs, should provide a good foundation for improving results in our components business… If consumer end demand continues to hold up, we expect that the end of 2022 will provide a good foundation for 2023.

I think it’s possible for Corsair to make a meaningful comeback. The company turned free cash flow positive in the last quarter. Management looks like they’re stabilizing the business’s cash burn rate.

But a turnaround would rely on an increase in revenue and margins. Management has been consistently wrong with their outlook. Over the past year, investors have had to deal with repeated and unexpected guidance cuts.

Take a look at the company’s first quarter earnings call. Management expected GPU price drops to create “a surge of activity in the second half of 2022 and 2023.” It seems like the company is now trying to push expectations for any inflection point further out into the next fiscal year. This worries me. An economic pullback may result in these projections just getting pushed back further.

Final Verdict

Corsair’s quarter was abysmal. Margins and guidance were especially weak. The company keeps repeating an optimistic long term outlook. It’s possible that this could be a good deep value stock, but I’m not convinced. I think the valuation is too expensive for a good risk to reward.

I think management’s guidance has been vague and inconsistent. I want to see actual results before I’ll consider buying or holding this stock.

Be the first to comment