marketlan

Earlier this week, I wrote an article on Permian Basin Royalty Trust (PBT), giving a basic overview of the company explaining why the stock made it onto my watchlist as a potential beneficiary from higher energy prices. One of the things that I have been watching for a couple weeks has been the continued selloff in natural gas and related equities. Antero Resources (AR) was the first stock I started watching as it dipped into the mid-20s, but one of the stocks I started looking at more recently is Comstock Resources (NYSE:CRK). It’s just a watchlist stock for now, but I think the natural gas price will eventually bounce back, and companies like Comstock or Antero are likely to follow.

Investment Thesis

The natural gas price has been beaten down recently, and investors expecting a bounce in coming months might want to take a look at some of the stocks in the sector. A couple on my watchlist are Comstock Resources and Antero Resources. Comstock is well-known to investors because of Dallas Cowboys’ owner Jerry Jones owning a significant stake in the company. The company has a very low cost to produce and easy access to export facilities. The company has a cheap valuation and recently reinstated its dividend, which is a sign of things to come in the way of capital returns in my opinion. I try to be contrarian in my investments, and the natural gas producers look like an attractive contrarian investment opportunity with the decline in the natural gas price in recent months.

Someone’s Getting Liquidated

I have a contrarian tendency with most of my investments and I prefer to buy something when most people would look at me like I’m crazy for considering an investment in a certain sector. That is what natural gas, and the related stocks are starting to look like for me right now. I think over the next couple years we are headed for structurally higher commodity prices for several reasons, but we will see how things play out in coming years.

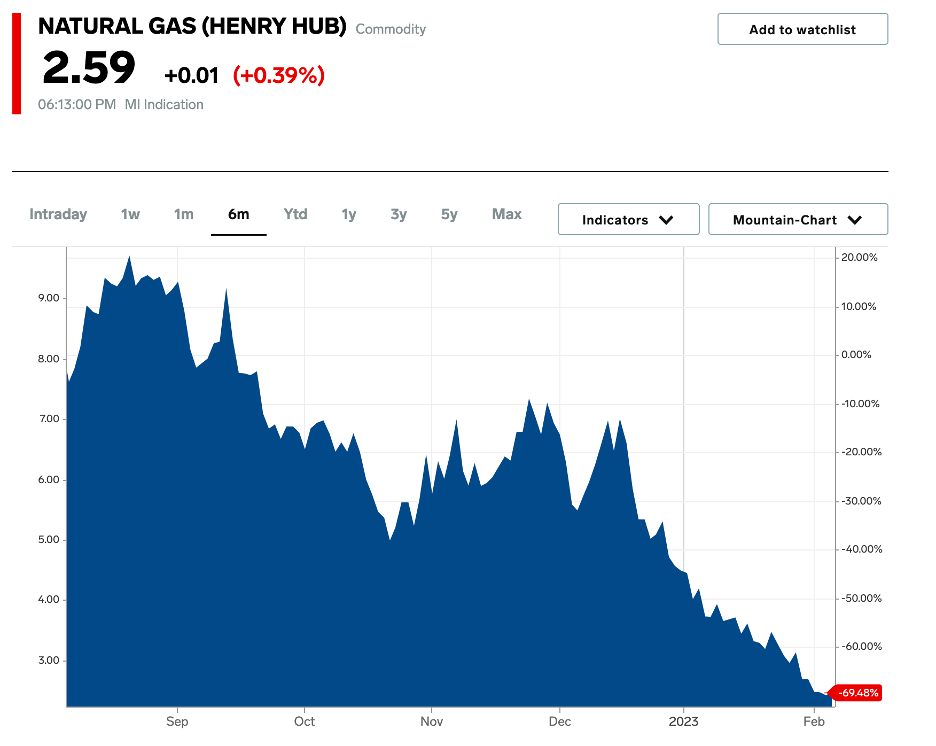

Natural Gas Price (businessinsider.com)

Natural gas prices are notoriously volatile, but they are down almost 70% in the last six months, and the price has been basically headed straight down since the start of 2023. I think we will see higher prices by the second half of the year, but it’s hard to predict commodity price movements, so take that prediction with a grain of salt. I listen to a ton of different podcasts on investments and other topics, and natural gas came up on one of them a couple days ago.

Nat Gas continues to get punished here. This is definitely forced liquidation. When you have funds that are piling in at the highs and they’re in leverage, it looks like they’re just getting margin called and margin called. What will happen, though, is once those funds liquidate, you will have a lack of sellers, and there will be nothing left but buyers. Also, the numbers don’t add up, we talked about this last week, price is now below the cost of production for lots of producers. So there are some imbalances here, and to me this is an absolute no brainer at this point… I think seasonally, Nat Gas is coming into some favorable tailwinds here.

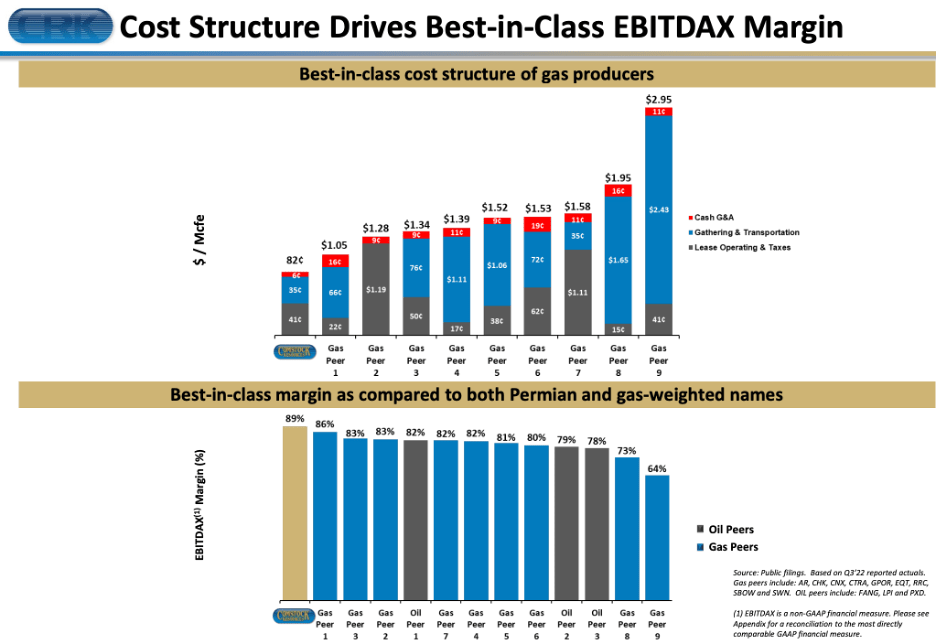

If you have some spare time to research investments, I can highly recommend Wall Street For Main Street. He has thought provoking guest interviews and the weekly chart review on This Week In Charts is interesting, even for an investor like me who focuses more on fundamentals than technicals. One of the other reasons I like Comstock is their low-cost structure relative to other natural gas producers.

Comstock Cost Structure

One of the reasons that I think the natural gas price below $3.00 is a temporary short-term problem is that the cost of production is above the current price for many producers. That is not the case for Comstock, which has some of the lowest production costs in the industry.

Comstock Cost Structure (comstockresources.com)

They also have good access to export facilities in the Gulf, which is going to be very important to meet demand from Europe and other international economies in coming years. While the selloff in natural gas and Comstock’s low cost of production are two obvious reasons to be bullish, I also think Comstock’s valuation is too cheap today.

Valuation

Comstock (and Antero) are going to be correlated to natural gas prices in the short term, but I think the selloff in both makes them attractive. Shares of Comstock started to selloff in December, but they spent most of the previous months in the high teens and low-20s. A company like Comstock isn’t as easy to value as a REIT or other stocks in less cyclical industries, but I think Comstock is undervalued today. Their cash flows will obviously be down in the first quarter of 2023 due to the drop in natural gas prices, but they did $1.2B in operating cash flow in the first nine months of 2022 with the higher commodity prices.

The current market cap of Comstock is $3.3B. It doesn’t take a genius to point out a company that did well over $1B in cash flow in 2022 with that market cap is cheap. For long term investors, I think it’s possible that Comstock could easily have cash flow in excess of their current market cap in the next three years. That will be determined by the natural gas price, which I don’t think will stay depressed for long. As long as the natural gas price doesn’t stick below $3 for most of the year, I think Comstock will have impressive cash flows this year as well. Another reason to be optimistic about Comstock is the reinstatement of their quarterly dividend.

Capital Returns

The company recently initiated a quarterly dividend for the first time since 2014. The quarterly payout was $0.125, which comes out to a 4.2% yield if the payout is held steady in 2023. The company’s balance sheet has improved dramatically in the last couple years, which will allow them to continue and increase dividend payouts, repaying debt, and start buying back shares. Over the next couple years, I think we will see significant capital returns which will in turn drive the share price higher.

Conclusion

The main risk to a bullish thesis on natural gas producers like Comstock or Antero is that we see the natural gas price languish for months. However, balance sheets in the sector have improved dramatically in the last couple years, and Comstock and Antero are no exception. I find Comstock to be attractive today after the recent share price decline and the valuation looks cheap to me. It’s a low-cost producer with solid margins, and the recent dividend announcement is a sign of things to come in my opinion. An investment in the natural gas sector might not be for every investor, but I find the risk/reward compelling today for Comstock Resources.

Be the first to comment