VioletaStoimenova

Maintaining Rating

We published an initial coverage article on September 3rd, 2022 with a “BUY” rating on the Compass Diversified (NYSE:CODI). We cited strong financial performance, reasonable valuation, and safe distribution metrics as reasons to purchase the stock. Since the time of our initial coverage, the stock is up 4.33% (~7% with dividend distribution) compared to S&P 500’s gain of 3.27%. We are writing to reaffirm our rating in wake of recent earnings announcement and new buyback program.

Q3 2022 Earnings

Q3 2022 earnings have been strong in our view. Sales were up 22% YoY along with adjusted EBITDA and adjusted earnings. The company reported strong performance in its branded consumer and niche industrial subsidiaries as drivers of top line growth. Net income actually went down a bit on a YoY basis, but management cited that the decline is largely driven by a gain in August 2021 from the sale of Liberty Safe. Nevertheless, the top line and adjusted EBITDA growth affirm our view that the company’s financial performance is strong.

Buyback Announcement

The most major news concerning the company is management’s announcement of a $50 million share repurchase program on January 19th of this year. We believe that management’s decision to repurchase shares during this time demonstrates their belief in long-term value of the company’s stock as well as their perceived undervaluation of its stock. CEO Elias Sabo announced:

CODI continues to produce strong financial and operational results, and the implementation of our first share repurchase program reflects our confidence in the future of the Company… CODI’s long-term ownership of leading middle market businesses using our permanent capital base has been a proven driver of shareholder returns, and we believe this new repurchase program is another tool to opportunistically maximize this value.”

Management has indicated its strong commitment to shareholder return once more despite less than ideal economic conditions, and this affirms our initial belief that the company will remain generous to its shareholders regardless of the circumstances.

Investor Day

The company affirms its target dividend of $1.00 per share, which equates to ~4.66% at current levels for 2023. The company also forecasted a 12% to 15% earnings growth target until 2028, which should translate to dividend increase prospects in the next few years as the economy improves. Furthermore, management also announced the launch of a new healthcare vertical, which may provide additional growth tailwinds for the business. Management’s continued efforts to diversify its portfolio and find additional levers to grow the company are good to see. The commitment to maintaining its dividends along its strategic plans for the coming years have provided us additional confidence in our thesis: the company’s stock will provide substantial dividend distribution along with capital appreciation opportunities.

2023 Investor Day Presentation

Risks and Balance Sheet

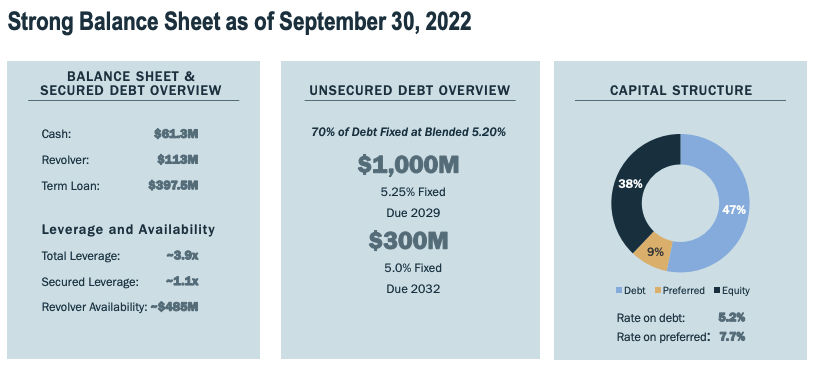

Similar to other financial services firms, CODI is subject to macroeconomic risks. The company reported slowdown in M&A activity which has had material impact in the company’s bottom line. Nevertheless, as dividend-focused investors, we remain more vigilant on the company’s balance sheet and its access to liquidity. The company remains healthy in its balance sheet, with the following balance sheet metrics.

Q3 2022 Earnings

The company has around ~$600 million in liquidity, and has debt maturity schedule that is far out — in 2029 and 2032, respectively. We believe this amount of liquidity along with business profitability will help protect the company from worse than expected economic downturn, and maintain its capital return program. The company has also increased its retained cash position over the last couple of years, which also demonstrate management’s active balance sheet management.

Conclusion

The recent earnings announcements and news support our thesis first discussed in our initial coverage. We believe the stock will continue to provide reliable yields during periods of uncertainty and provide potential upside in the event of a rebound in economic activity. Thus, we maintain our “BUY” rating on the stock.

Be the first to comment