{kind=link}

Columbia Care has seen sequential revenue growth in eleven consecutive quarters and had 97% revenue growth in 2019. Source: Author based on company filings.

Summary

Columbia Care (OTCQX:CCHWF) is a somewhat under-the-radar U.S. cannabis company which has licenses to operate in sixteen states. As with most cannabis companies, their growth has been driven by the growing regulated U.S. cannabis market. Thanks to both organic growth and acquisitions, Columbia Care nearly doubled their revenue in 2019 and trades at approximately 4x trailing sales and 2x forward sales guidance.

However, Columbia Care has relatively poor gross margins and high operating costs compared to their peers and compared to their revenue, respectively. These costs have prevented the company from generated profits even by the very forgiving adjusted EBITDA metric. Management is aiming to hit adjusted EBITDA profitability by the fourth quarter of this year, although that guidance may be disrupted due to the global pandemic.

While Columbia Care has attractive growth and zero debt, I shy away from investing in the company due to its poor gross margins and relatively high operating costs.

Growth

Columbia Care is a vertically-integrated cannabis company which operates in state-regulated markets in the United States. Their business is federally illegal, which means that they are unable to trade on a U.S. Stock exchange and they are subject to onerous Section 280E taxes. Columbia Care shares trade on the minor Canadian Securities Exchange as CCHW and trade on the over-the-counter OTCQX market as OTCQX:CCHWF.

Columbia Care’s growth is driven by growth in the regulated U.S. cannabis industry and by the company’s continuing expansion both organically and through acquisitions. Since the end of September, Columbia Care has grown from 26 to 35 dispensaries open across the United States and Canada. This includes ten dispensaries in Florida, four dispensaries in each of Ohio and New York, and three dispensaries in each of Delaware, Massachusetts, and Pennsylvania. Most recently, the company earned an approval to operate in Virginia earlier this month.

Columbia Care has also been expanding through acquisitions. Most notably, the company agreed in November 2019 to pay $140 million to acquire The Green Solution, a vertically-integrated Colorado cannabis operator. That deal will add 23 Colorado dispensaries to Columbia Care’s network of dispensaries. Columbia Care for pay for this purchase using $110 million of their own stock and $30 million of debt, pending regulatory approval and other closing conditions. After this acquisition is closed and when Columbia Care completes their build-out, they plan to have more than 90 dispensaries nationwide and in Puerto Rico.

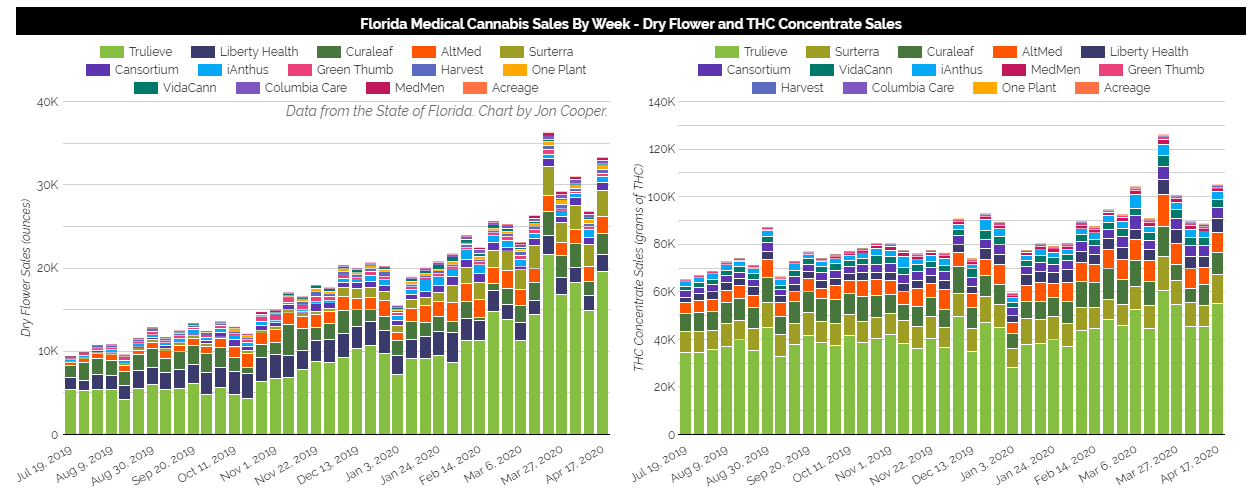

Columbia Care’s growing footprint had contributed to growing top-line revenue. In 2019, the company reported $77.5 million of revenue, up 97% from the previous year. The fourth quarter of last year was the eleventh consecutive quarter in which Columbia Care saw positive sequential revenue growth, with revenue growing 5% sequentially to $23.2 million as they added more dispensaries in key states including Florida, where Columbia Care opened four dispensaries in the fourth quarter and has subsequently added five more dispensaries to grow to eleven dispensaries.

Despite the outbreak of COVID-19, state-legal cannabis continues to thrive. The State of Florida reported its strongest-ever weekly cannabis sales on the week preceding March 20, 2020. Results since then have tailed off a bit, but continue to show a strong upward trend and the results released on April 17 were the second-strongest sales ever despite, or perhaps because of, the ongoing pandemic.

At the beginning of the COVID-19 crisis, Columbia Care provided a detailed operational update describing strong sales growth. During the week of March 14, the company earned record weekly revenue in either states and set single-day revenue records in seven different dispensaries. They had also generated $23.6 million in revenue-to-date through March 14, already higher than their fourth quarter revenue of $23.2 million.

Profitability

Columbia Care is not profitable. While the company has been able to increase revenue for eleven consecutive quarters, they have not had a profitable quarter during their life as a public company or since 2017.

Columbia Care has not generated an operating profit since at least 2017 despite considerable revenue growth. Source: Author based on company filings.

Columbia Care gross margins fell 15 percentage points during 2019, declining to 27% from 42% last year. For comparison, other top U.S. cannabis companies like Curaleaf (OTCPK:CURLF), Cresco Labs (OTCQX:CRLBF), and Green Thumb (OTCQX:GTBIF) reported gross margins of 54%, 32%, and 52%, respectively. Columbia Care gross margins appear to be significantly those of their peers, which may allow for considerable improvement.

In addition to low gross margins, Columbia Care also has high operating costs which preclude profitability. Columbia Care’s operating costs have exceed their revenue in six consecutive quarters with fourth quarter operating costs 1.5x higher than revenue. The company will need to either cut operating costs or significantly improve their revenue (without added operating costs) in order to generate operating profits.

Columbia Care has significant adjusted EBITDA losses over the past two years. Source: Author based on company filings.

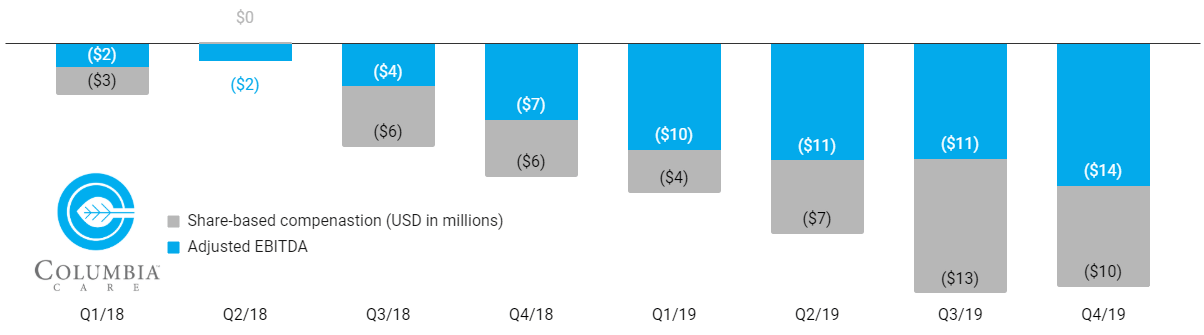

Owing to high operating costs and low gross margins, Columbia Care has significant adjusted EBITDA losses over the past two years. As reflected in the figure above, these losses exclude share-based compensation which dilutes shareholders. During 2019, Columbia Care lost $47 million in adjusted EBITDA excluding $12 million of one-time costs. The company gave a further $34 million of stock to employees, with $22 million of this stock-based compensation going to “key management personnel.”

In total, Columbia Care generated annual adjusted EBITDA margins of -61% in 2019 or -105% when including the cost of share-based compensation.

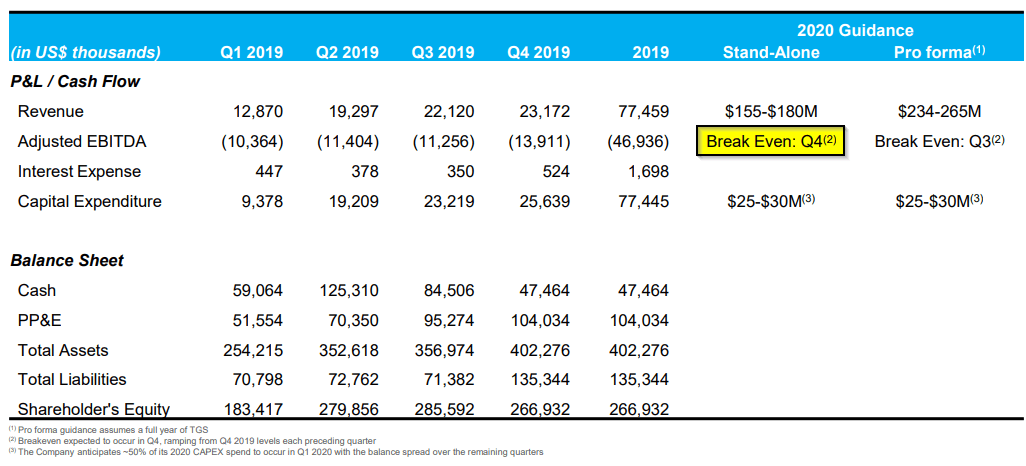

Source: Columbia Care investor presentation from March 2020.

Columbia Care hopes to hit adjusted EBITDA profitability, excluding share-based compensation, in the fourth quarter of 2020. However, it is not immediately clear whether this guidance will be achievable in the wake of the global pandemic. While medical cannabis dispensaries have been found to be essential in most states, the pandemic may hurt sales and may slow development and expansion efforts. Several cannabis companies have backed off their guidance in light of the pandemic.

Adjusted EBITDA profitability tends to be the easiest form of profitability for cannabis companies to hit. This will not immediately lead to “real” profitability in the form of positive net income and positive cash flow, as adjusted EBITDA excludes the costs of onerous Section 280E taxes and excludes both depreciation and capital expenditures.

Stability

Recently, cannabis companies have often been falling by the wayside due to shaky balance sheets and other operational issues. For example, CannTrust (formerly OTC:CTST) filed for creditor protection, MedMen (OTCQB:MMNFF) diluted its shareholders and gave its lenders control of the company as I previously wrote about, and iAnthus (OTCQX:ITHUF) recently defaulted on its debt which will likely lead to significant dilution or worse as I previously covered on this platform.

With that in mind, it is useful to analyze the stability of a cannabis company’s balance sheet and how much cash they have, as in my analysis of the risks of insolvency across the U.S. cannabis sector.

Columbia Care ended their fourth quarter with $47 million in cash and no debt. This includes proceeds from a sale-leaseback transaction in late 2019. During their fourth quarter earnings call on March 10, the company said they planned to close a further sale-leaseback funding deal in the first quarter but it is unclear if this has been completed.

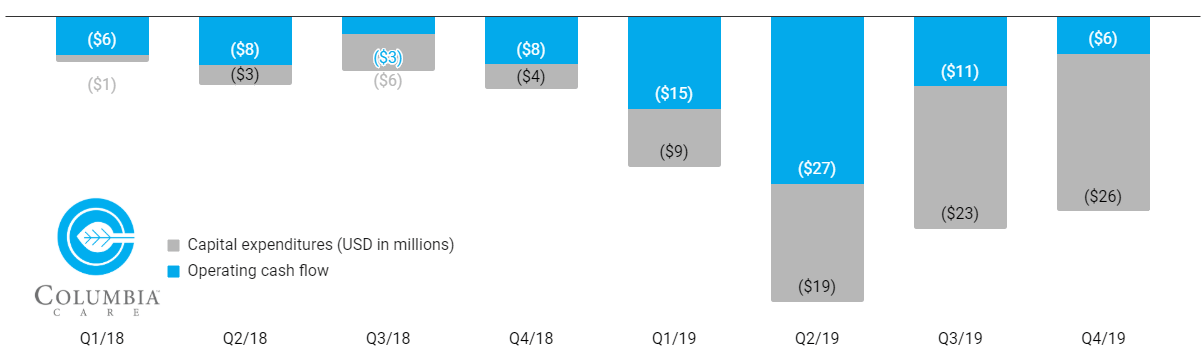

During the past year, Columbia Care burned through $60 million on operating costs and invested another $77 million into capital projects. Source: Author based on company filings.

Columbia Care burned through $60 million on operating costs and spent a further $77 million on capital projects during the past fiscal year for a total cash burn of $137 million. Approximately 23% of this cash burn occurred in the fourth quarter, suggesting relatively stable expenditure rates. On its face, this suggests that current cash resources may last Columbia Care until approximately May 2020 without additional funding.

That figure is likely to be an under-estimate given that Columbia Care plans to spend significantly less on capital expenditures this year. Based on their investor presentation, Columbia Care anticipates $12.5-15 million of capital expenditures in the first quarter of the year and $25-30 million of capital spent for the full-year. Given their fourth quarter operating cash burn, this suggest Columbia Care has sufficient capital to operate until approximately October 2020 without additional funding.

Based on my previous analysis, this suggests the Columbia Care’s capital position is approximately akin to those of Harvest Health (OTCQX:HRVSF) or Green Thumb (OTCQX:GTBIF). Unlike both of those companies, however, Columbia Care does not have any debt.

Thoughts

Columbia Care has a market cap of ~$360 million and an enterprise value of ~$315 million based on a $1.67 share price and not including the 34 million shares that will be issued to The Green Solution. This reflects a trailing EV/sales ratio of 4x, which is comparable to Trulieve or Harvest Health, cheaper than Green Thumb or Curaleaf, and more expensive than MedMen, Acreage, or iAnthus.

If Columbia Care hits the midpoint of its revenue target of $155-180 million and if they complete their acquisition of The Green Solution, the company trades at approximately 2x forward sales. This is a little cheaper than the marquee U.S. cannabis companies but is comparable to operators like Harvest Health and more costly than MedMen and iAnthus.

In my view, Columbia Care’s current share price seems about right. They are priced a bit cheaper than the marquee names in the sector like Green Thumb and Curaleaf but are priced a bit higher than struggling companies like MedMen and iAnthus.

Personally, I am not inclined to invest in Columbia Care right now. Cannabis is always an exceptionally risky industry so I limit my exposure to the sector by only investing in a few companies and by keeping most of my investments in safer sectors. Columbia Care doesn’t make the cut for me because:

- Their revenue growth is slower than that of many of their U.S. peers like Curaleaf, Green Thumb, and Trulieve;

- Their gross margins (at 24% last quarter) are less than half of those of top U.S. cannabis companies;

- Their operating costs remain significantly higher than revenue; and

- They fly a little under-the-radar which may hurt their ability to raise capital through debt and equity moving forward and thus limit potential growth rates.

For those reasons, I am neutral on Columbia Care at this time and do not plan to initiate a position in the company.

Happy investing!

Make better cannabis investments with better information

The Growth Operation is the largest community of cannabis investors on Seeking Alpha. During difficult market conditions, our active chat room and daily news updates help investors make sense of the rapidly-evolving cannabis market. The Growth Operation also includes interactive data, illustrating market sales trends and highlighting companies with best-of-breed financial performance.

Disclosure: I am/we are long TRUL, MMEN, GTII, CURA. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment