Sundry Photography

In a challenging environment for tech and software companies, Cloudflare (NYSE:NET) delivered remarkably strong numbers for Q4, with revenue exceeding expectations and record cash flow generation.

Cost discipline is great to see and much appreciated, especially because Cloudflare has not overexpanded during the bull market in tech, so the company does not need to fire employees in a more challenging environment. The business model is proving to have operating leverage, as revenues are outgrowing expenses and profit margins are expanding.

Going forward, Cloudflare has excellent opportunities for growth in key areas such as AI, where the business is even outperforming management expectations.

Top Level Execution

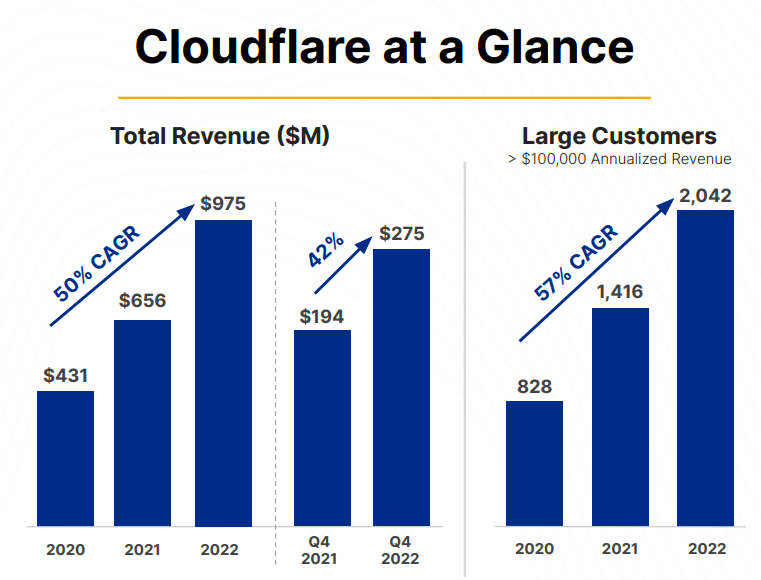

Total revenue reached $274.7 million during the fourth quarter, growing 42% year-over-year. Revenue from large customers increased by 56%, and these large customers now contribute 63% of Cloudflare’s total revenue.

Cloudflare

Both revenues for the fourth quarter and guidance for the full year 2023 came in slightly above Wall Street expectations. The guidance for the full year 2023 looks comparatively stronger than the guidance numbers for the first quarter, implying that Cloudflare could be modeling an acceleration in the second half of the year. This scenario would be consistent with the guidance provided by other tech and software companies in recent weeks.

Cloudflare

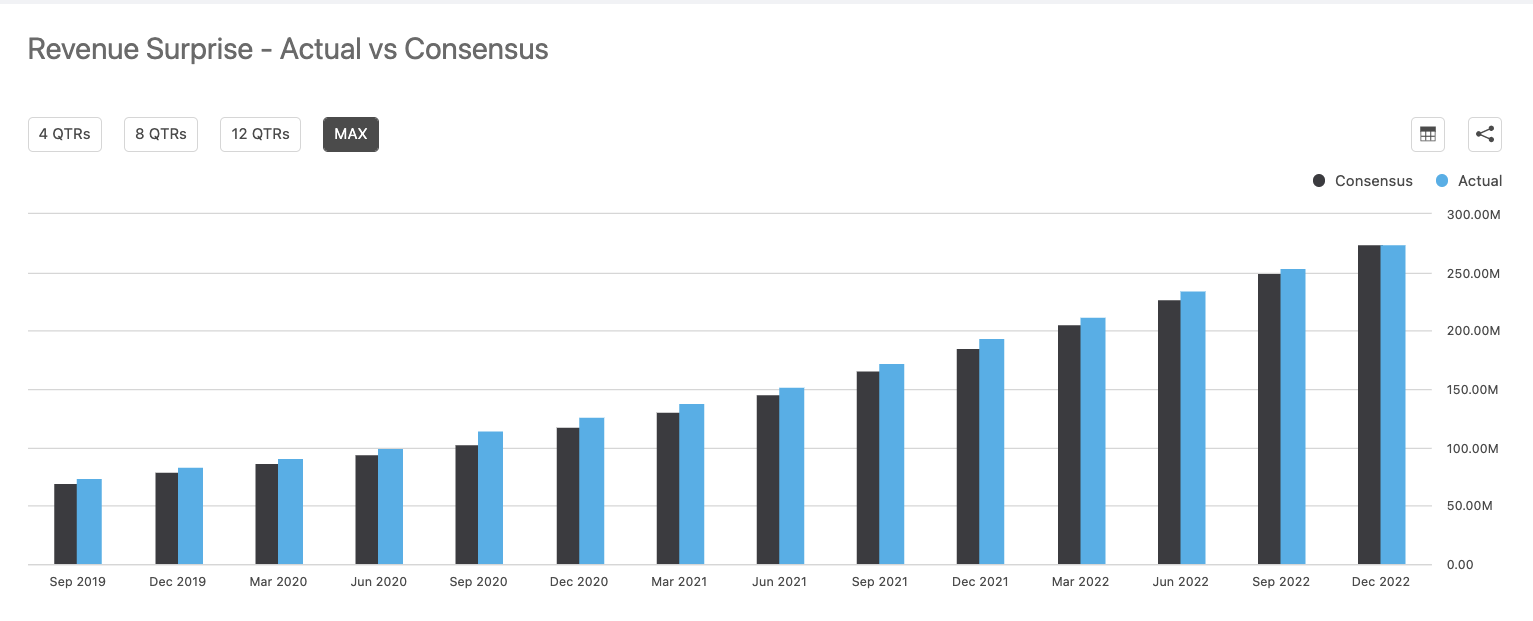

Cloudflare has an impeccable track record of consistently outperforming expectations over the long term. The revenue beat in Q4 is not as large as it was in prior quarters, but this is still a very strong performance considering the environment.

Cloudflare

Management explicitly said in the conference call that they are being conservative with guidance. Cloudflare is not assuming any improvement in macro conditions, and guidance is not incorporating any expectations for accelerating performance due to Cloudflare’s revamped go to market strategy.

In the words of CEO Mathew Prince:

We stick to our rule of trying to be prudent and thoughtful on how we think about the future, especially in a rather uncertain environment. I think that the important takeaway in the guidance that we put forward is that we did not assume any help from the macroeconomic environment. We did not plan that things would get better. And we have a lot of initiatives that will accelerate sales productivity and accelerate growth, things that we can control.

Many companies in tech have been hurt by excessive spending and too much hiring during the expansionary phase of the cycle. That is not an issue for Cloudflare, though, as management detected the economic slowdown early and made the necessary adjustments.

We were fortunate that given our visibility into the overall Internet traffic and the e-commerce trends, we started to see a slowdown in the economy all the way back in December of 2021. Based on that, around this time last year, we began slowing our pace of hiring to ensure we didn’t get over our skis. That’s paid off and kept us from having to take more drastic actions like many of our peers.

It’s also given us the ability to sensibly invest in our team as amazing talent comes on the market. To give you some sense, in 2022, we had over 400,000 people apply for approximately 1,300 positions at Cloudflare. That demand to work at Cloudflare has allowed us to continue to hire incredible talent or any discipline in overall compensation. We are committed to incremental equity compensation dilution well below many of our peers, targeting less than 3% net burn rate annually.

Management said that they are keeping share dilution at below 3%, but the real number seems to be lower, around 2.5% in recent quarters. This is typical of Cloudflare, underpromising and overdelivering.

The chart below shows the operating leverage advantages in the business: As revenue expands, different expense items grow at a slower rate than revenue, which has a positive impact on profit margins.

Cloudflare

Free cash flow generation was $34 million, a new record for Cloudflare and reaching 12% of revenue. Management reaffirmed guidance for positive cash flows in 2023 and beyond.

Cloudflare

The table below shows free cash flow and free cash flow margins over recent years as well as the forward-looking estimates from Wall Street. Cloudflare is already at the stage in which the company is expected to deliver positive and expanding cash flows in the years ahead.

TIKR

The Future

According to CEO Matthew Prince, Cloudflare has achieved great success because of its culture of permanent innovation and superior products, but the company has a lot of room for improvement on the commercial side.

Cloudflare is now focusing on that area with new talent on board, and management believes it has plenty of opportunities to accelerate growth with better execution on that side.

In the words of CEO Matthew Prince during the conference call:

If we’re honest with ourselves, our go-to-market organization hasn’t yet been fully optimized. As our products become more complicated and we are selling to larger and larger customers, it’s increasingly clear that we need to step up our game in marketing and sales. I introduced Marc Lore Detsky who joined last quarter to lead our sales organization. Last week, we briefed me and Michelle on his first 100 days.

My initial reaction, if I’m honest, was embarrassment over some of the basic things we should have been doing better, but my second reaction was excitement as there are so many opportunities for us to improve.

Once again, the company is not incorporating any expectations of improvement in sales or marketing efficiency in its guidance.

Cloudflare also obtained FedRAMP authorization for most of its products recently. The company’s first contract after certification is a $7.2 million 5-year deal to operate the .gov registry. Given the strategic importance of cybersecurity in times of escalating geopolitical tensions with Russia and China, it is easy to see how the government sector could be a sizable opportunity for Cloudflare going forward.

Management also highlighted the long-term opportunity in Artificial Intelligence, which is not only a powerful trend from a fundamental perspective but also an area generating a lot of interest among investors.

Cloudflare’s R2 product allows large amounts of unstructured data to be stored without the high costs associated with typical cloud storage egress fees, and it is gaining popularity among AI companies.

Cloudflare did not specifically mention ChatGPT in the conference call, but the reference was not too hidden either.

A leading generative AI company signed a 1-year $1 million deal. The company had been a user of our free tier since 2017. And this deal originally started out as a relatively small gateway DS opportunity to replace Cisco umbrella. However, when their browser-based application debuted in late November, demand for the company’s AI-generated content absolutely exploded with unprecedented rates of adoption.

We saw success with other AI companies in the quarter as well… AI companies, in particular, need to find wherever it’s most cost effective to run their models across multiple different cloud providers. They are, by their very nature, multi-cloud, but the data egress policies make it prohibitive to move large training sets between the cloud and our Cloudflare workers.

What we’re finding with these AI companies is that R2 and other workers’ products naturally become the glue at the center of a multi-cloud ecosystem. R2 has become the natural neutral place for these AI companies to store their training data in order to make sure it can be inexpensively and efficiently accessed from anywhere. It’s obvious in retrospect. But it’s a use case we didn’t anticipate.

Today, our largest R2 customer is another AI company using us for exactly the purpose of being a neutral place to store their training data. And of course, an neutral network super Cloud that stitches together the traditional public cloud isn’t a problem exclusive to AI.

Timing And Valuation

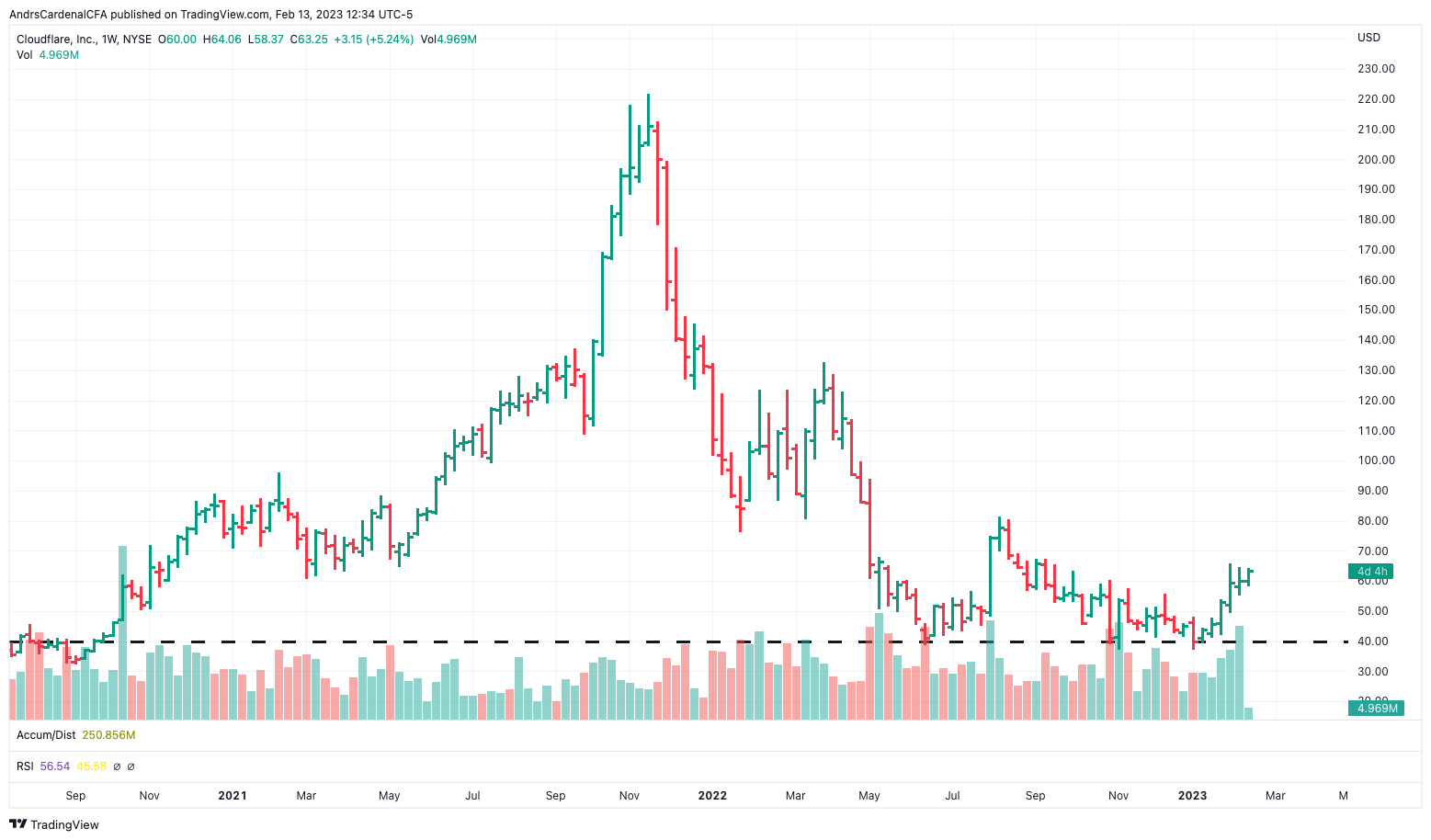

After a vicious selloff in 2022, Cloudflare stock has been trying to base above $40 per share since June of last year. The stock price is reacting well to earnings news in the short term, but the current macro environment is intensely driven by economic news and top-down considerations.

TradingView

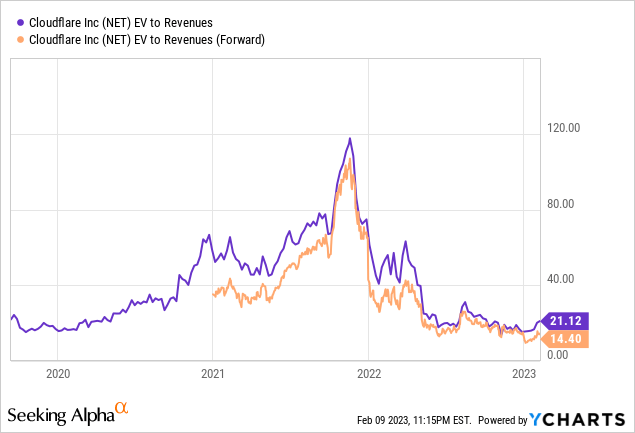

Cloudflare does not have a long track record as a public business, but valuation levels as measured by Enterprise Value to Revenue are at the low end of the historical range.

YCharts

Valuation is always very dynamic for a company of this quality. Even if the valuation ratios look comparatively high versus other companies in the sector, we also need to consider the company’s ability to outperform expectations. In the particular case of Cloudflare, it has a pristine track record in that regard.

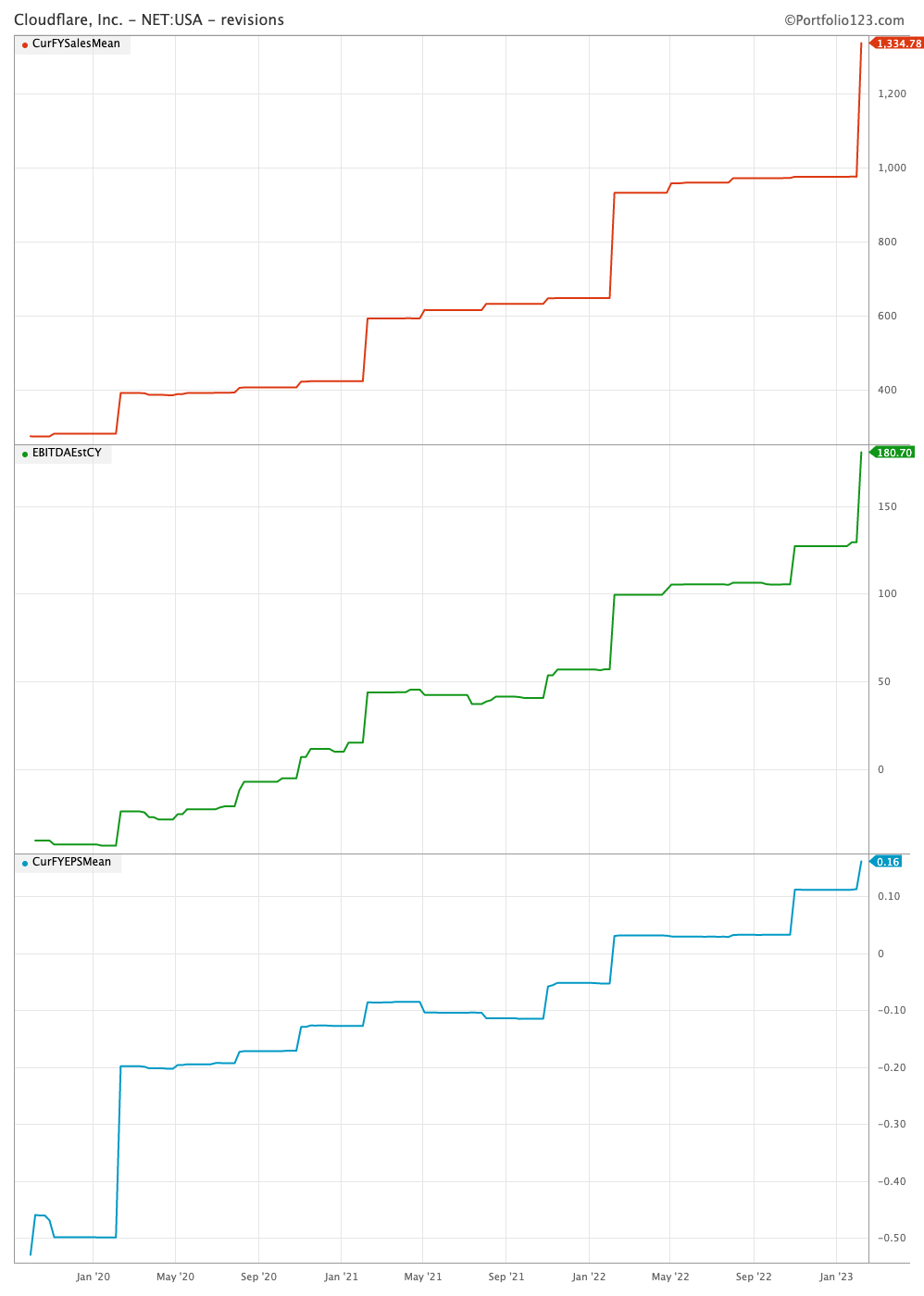

The chart below shows Wall Street’s expectations for revenue, EBITDA, and earnings per share in the current year. We are looking at how those estimates have evolved over time. In red we can see revenue estimates for 2023, with EBITDA in green and EPS in blue.

In September 2019, Wall Street was calculating that Cloudflare was going to make $279 million in total revenue for the year 2023, and now they are estimating more than $1.3 billion in sales. Estimates for EBITDA and earnings have improved from negative values to positive numbers and growing.

Portfolio123

Imagine if we were trying to value Cloudflare in the year 2019 using Wall Street estimates for the year 2023. We could easily say that the stock was too expensive using a revenue estimate of $279 million. However, the numbers are very different when you know that the business is on track to make $1.3 billion for that same year.

Valuation is always relevant and should never be disregarded. However, if you are a long-term investor with a plan to slowly dollar cost average into positions over 3 to 5 years, then buying the right company is far more important than paying the lowest possible price.

The Bottom Line

It was a strong quarter for Cloudflare, with vigorous revenue and healthy profitability. Management is making the right moves and the company has enormous room for growth in the years ahead.

Valuation is still expensive in comparison to other companies in the sector, but Cloudflare is a superior company that deserves an above-average valuation. The company is also trading at the low end of its historical valuation range.

When we look at future cash flow estimates and the company’s proven track record of outperforming those estimates, valuation could even be quite attractive from a dynamic point of view.

In the short term, the stock price will fluctuate based on general market conditions and investor sentiment toward growth stocks. Over the long term, however, the fundamental drivers behind Cloudflare are stronger than ever.

Be the first to comment