Sundry Photography

Investment Thesis

Cloudflare (NYSE:NET) is a founder-led, industry-leading, cloud-native CDN (content distribution network) and cybersecurity company, with a mission “to help build a better internet”. The company offers an efficient, scalable, global network that customers can simply ‘plug into’ in order to improve both their security and performance.

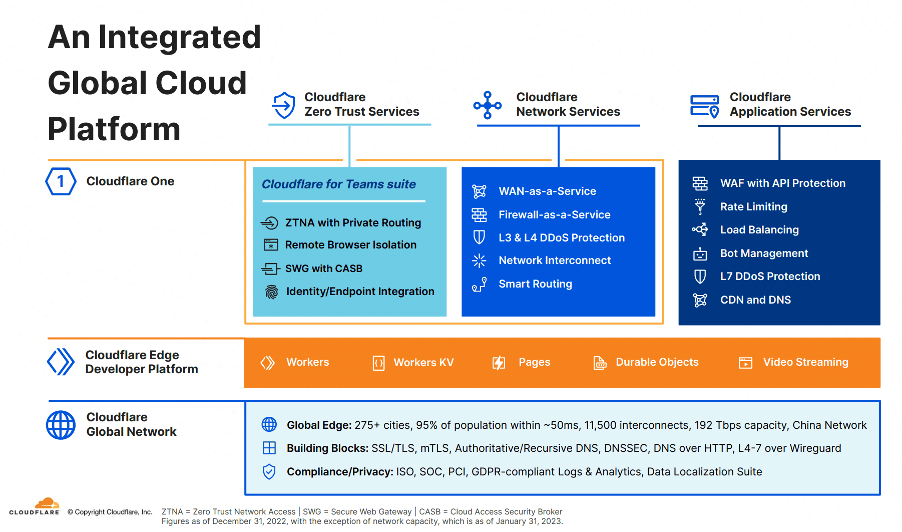

Cloudflare Q4’22 Investor Presentation

My personal thesis for investing in Cloudflare (laid out in more detail here) is the following: it is a leader in multiple growing industries that are transitioning to the cloud, from CDN to cybersecurity, and operates in business-critical areas, making Cloudflare more recession resistant than other companies. It has continually, successfully rolled out new products to existing customers (as evidenced by its high dollar-based net retention rates) and has seen substantial growth thanks to this. The company has an attractive long-term operating model, with operating margins expected to exceed 20%, and it has been growing rapidly over the last few years and should continue to do so in the future.

The company reported Q4’22 results last week and the market really liked what it saw, with shares jumping over 10% immediately after the release. So, should investors be excited? Let’s take a look through the highlights from Cloudflare’s results to find out.

Cloudflare’s Q4 Earnings Overview

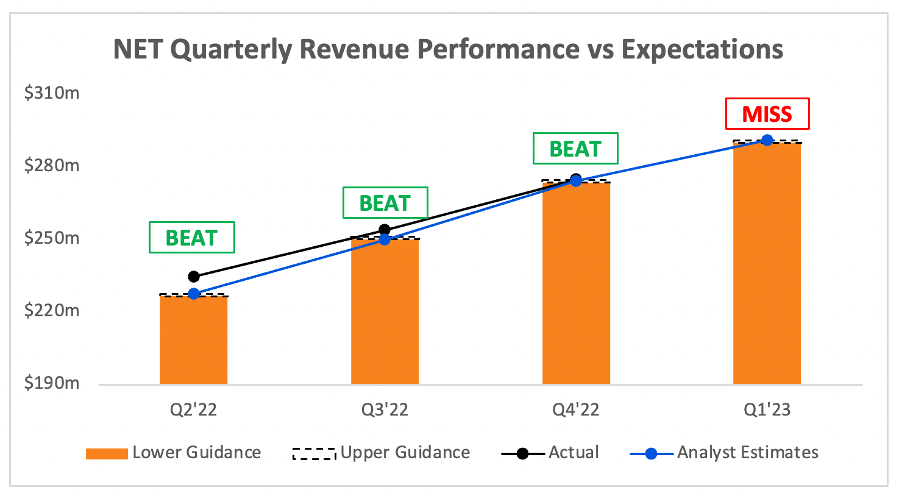

Starting from the top, Cloudflare’s Q4 revenue grew 42% YoY to $275m, coming in just ahead of analysts’ estimates of $274m. Such a ‘small’ beat on revenue would’ve probably knocked Cloudflare shares down by 15% in the market of 2021, but nowadays a ‘growth’ slightly exceeding revenue expectations can still be rewarded.

Author’s Work

Another thing that usually resulted in ‘growth’ stocks plummeting back in 2021 was revenue guidance being below estimates, and that’s what we saw here with Cloudflare – just.

Revenue guidance for Q1’23 was $290-$291m, with analysts’ expecting $291.02m, so it is a miss at the midpoint of management’s guidance.

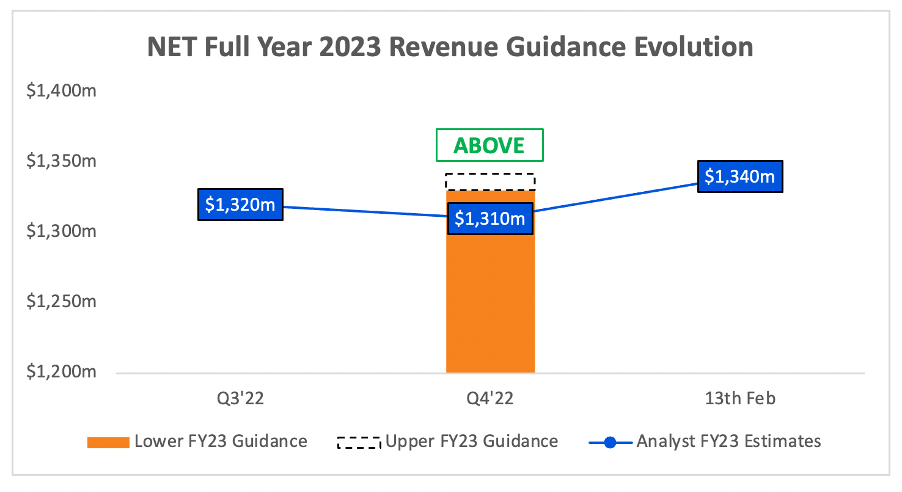

However, I think the reason for Wall Street’s enthusiasm with these results was not the Q1 guidance, but rather the guidance for Cloudflare’s 2023 full year revenue. Analysts had been expecting FY23 revenue of $1,310m, but management guided for a range of $1,330-$1,342m.

Author’s Work

Given that Cloudflare has a history of continually raising its full year guidance throughout the year, I think the market was very pleasantly surprised by this higher-than-expected FY23 revenue guidance.

Is Cloudflare being too optimistic given the difficult macroeconomic environment? Not according to CFO Thomas Seifert, who said on the Q4 earnings call:

In our guidance, we have not factored in any improvement in the macroeconomic environment or from our go-to-market initiatives.

So, this full year guidance range, which implies YoY revenue growth in 2023 of 37% at the midpoint, is nowhere near a best-case scenario? That’s very impressive if it turns out to be true, and I know Cloudflare is a company that tends to exceed its own guidance – a great sign for shareholders!

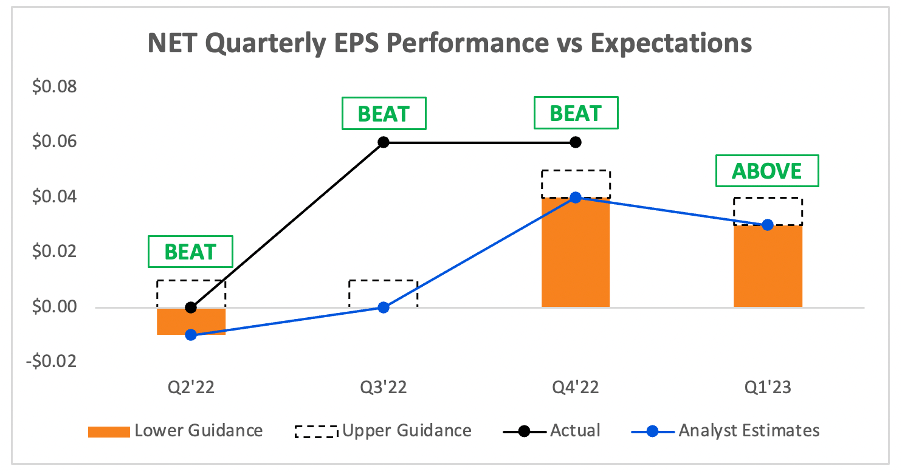

Moving onto the bottom line, and Cloudflare delivered adjusted EPS of $0.06 in Q4, coming in ahead of analysts’ expectations of $0.04.

Author’s Work

Looking ahead to Q1, and management’s EPS guidance of $0.03-$0.04 also comes in ahead of analysts’ expectations of $0.03. These are not particularly significant numbers right now, but I am happy to see Cloudflare becoming more and more profitable (albeit on an adjusted basis) and continuing to exceed analysts’ expectations.

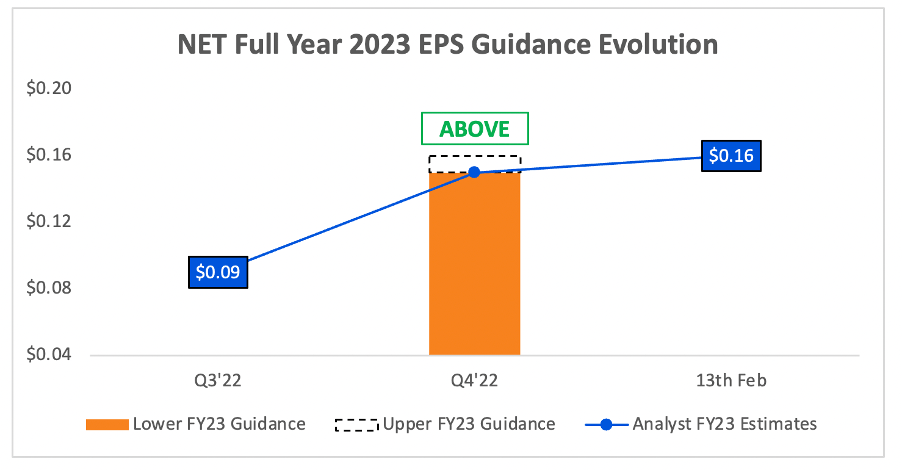

This was achieved once again with Cloudflare’s FY23 EPS guidance of $0.15-$0.16, which came in above the $0.15 that analysts were expecting.

Author’s Work

Out of all the headline numbers, the real standout for me was Cloudflare’s revenue guidance for 2023. The confidence of management to predict 37% revenue growth for this upcoming year in this extremely tough environment is either testament to Cloudflare’s strength, or overconfidence – only time will tell, but this management team has been proven right more often than they’ve been proven wrong.

Cloudflare’s Key Metrics

In my results preview article, I highlighted a few key metrics that I always like to watch with Cloudflare.

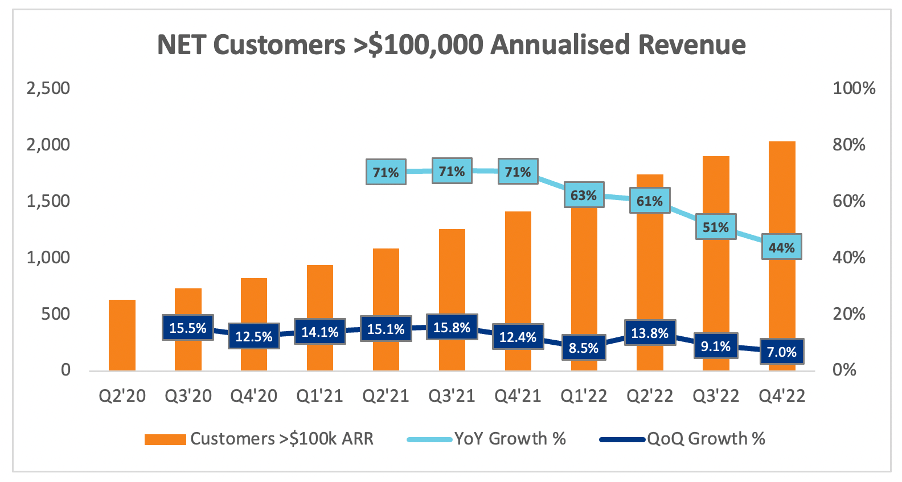

The first figure I look at is the large customer numbers, and Cloudflare has always reported its customers who bring in more than $100k in annualised revenue. This number grew to 2,042 in Q4, as Cloudflare added another 134 customers into this category during the quarter.

Author’s Work

This 2,042 figure represented growth of 44% YoY and just 7.0% QoQ, representing the lowest quarterly growth rate of the past few years. That should surprise no-one, as the current operating environment for businesses such as Cloudflare has been extremely tough as results from the likes of Amazon’s AWS (AMZN) have shown.

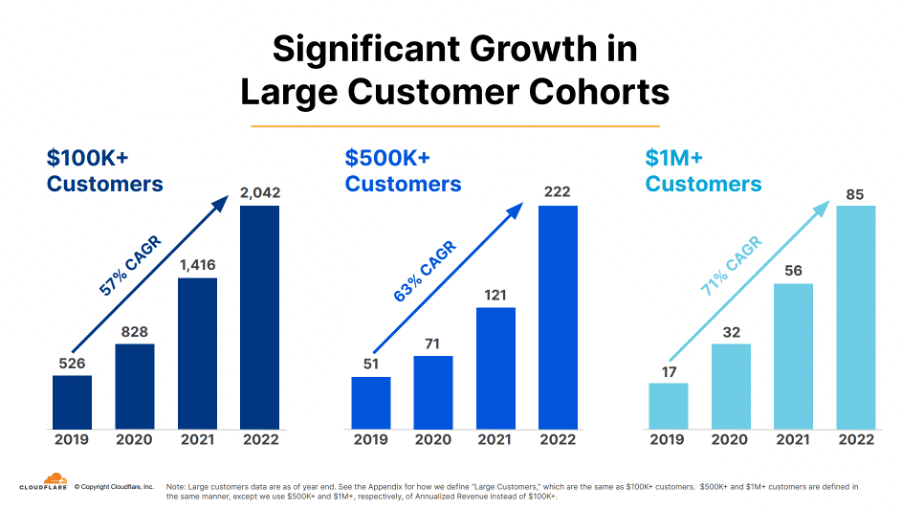

On the plus side, Cloudflare continues to grow rapidly with larger and larger businesses. As of Q4, it now has 85 customers contributing at least $1 million in annualised revenue, up from just 56 in 2021.

Cloudflare Q4’22 Investor Presentation

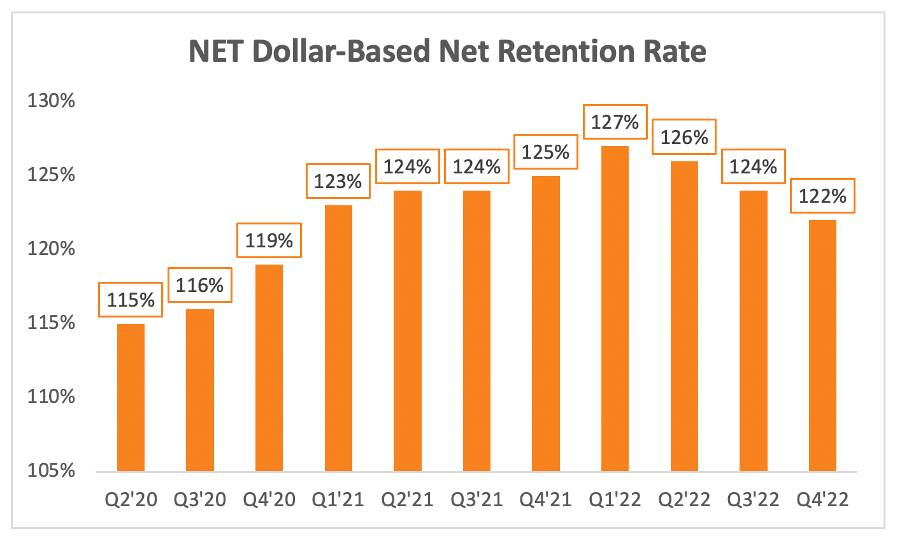

Moving onto another important metric for Cloudflare (and a crucial metric for any something-as-a-service business) – dollar-based net retention rate. This is a measure of how much spend has increased with existing customers over the past twelve months, and also takes into account customers who have left (known as churn).

Author’s Work

Despite the headwinds, Cloudflare still delivered a decent DBNRR in Q4 of 122% – previously I said I’d be happy with anything over 120%, so I’m happy!

CFO Thomas Seifert also added some colour on the earnings call:

Our dollar-based net retention rate was 122% during the fourth quarter, a decrease of 200 basis points sequentially and a decrease of 300 basis points year-over-year. We’ve not experienced elevated churn. Instead, similar to last quarter, the decline was primarily driven by less net expansion in customers spending less than $100,000 worth Cloudflare as well as pay-as-you-go customers.

In short, this lower DBNRR was driven by less upselling to smaller customers, which is understandable as smaller businesses are more likely to be fighting for survival in tough economic times.

Cloudflare’s Earnings Call Highlights

Cloudflare Co-founder and CEO Matthew Price isn’t one to hold back on an earnings call, and it’s always fun to see what he has to say – so, here’s some of the key items from the call.

Firstly, Prince spoke about how Cloudflare was ahead of the curve back in 2021 when it came to excessive hiring thanks to their insights into the economy:

We were fortunate that given our visibility into the overall Internet traffic and e-commerce trends, we started to see a slowdown in the economy all the way back in December of 2021.

Based on that, around this time last year, we began slowing our pace of hiring to ensure we didn’t get over our skis. That paid off and kept us from having to take more drastic actions like many of our peers. It’s also given us the ability to sensibly invest in our team as amazing talent comes on the market. To give you some sense, in 2022, we have over 400,000 people apply for approximately 1,300 positions at Cloudflare.

This has now put Cloudflare in a great position, where not only are they able to avoid mass layoffs, but they can now hire all of this newly available talent whilst offering much more reasonable compensation packages than we saw a year or so ago.

There’s also been a lot of talk about ChatGPT recently, and Cloudflare is the company that powers this hugely popular AI-chat platform. Prince also gave some colour on their relationship with a company that it’s fair to assume is ChatGPT:

A leading generative AI company signed a one-year $1 million deal. The company had been a user of our free tier since 2017. And this deal originally started out as a relatively small gateway DNS opportunity to replace Cisco Umbrella. However, when their browser-based application debuted in late November, demand for the company’s AI-generated content absolutely exploded with unprecedented rates of adoption.

Their Azure Front Door had quickly proved insufficient at handling the massive load on their services from legitimate users as well as keeping fraudulent users from exhausting their resources. They started off with CVM, DDoS, bot management, gateway DNS and more. We are actively exploring various paths for expansion to support their incredible growth as well as emerging use cases of their AI models and applications with Cloudflare Worker, API Shield, imagery sizing and more.

Reading through the tech jargon, this is an excellent case study in how Cloudflare can grow with a customer, whilst simultaneously demonstrating just how effective Cloudflare’s solutions are against the competition.

ChatGPT is partly owned by Microsoft (MSFT), and yet it couldn’t rely on Microsoft Azure’s own capabilities to manage its traffic, so Cloudflare stepped in. If ChatGPT really is the beginning of an AI boom, then this boom could be a huge catalyst for Cloudflare in the decade to come.

Finally, Prince spoke about Cloudflare’s ability to generate cash:

We delivered a record quarter in terms of operating profit, operating margin and free cash flow. I’m particularly proud of our free cash flow performance during the fourth quarter, and we are committed to continuing to scale free cash flow generation going forward.

Cloudflare’s negative free cash flow has always made me feel a bit uneasy, but I’m glad to see that they delivered $33.7m in free cash flow this quarter and plans to remain free cash flow positive in the future.

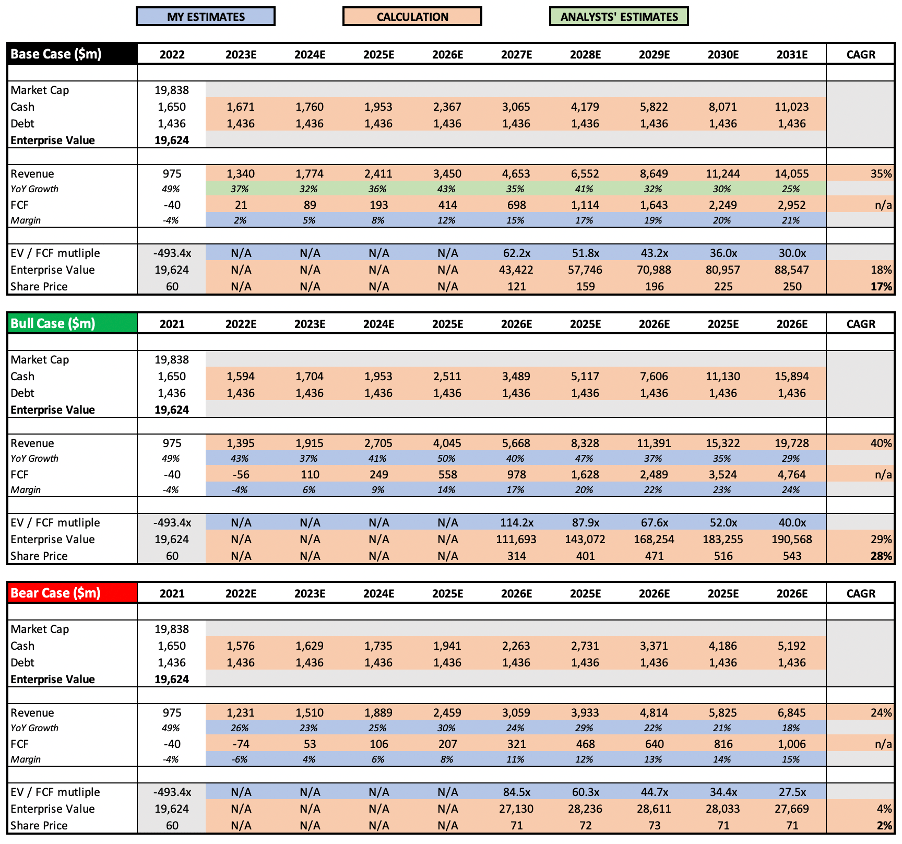

NET Stock Valuation

As with all high growth, disruptive companies, valuation is tough. I believe that my approach will give me an idea about whether Cloudflare is insanely overvalued or undervalued, but valuation is the final thing I look at – the quality of the business itself is far more important in the long run.

Author’s Work / Seeking Alpha

I haven’t changed too much since my previous article (which can be used for reference), other than rolling this model forward by one year. Thanks to management’s optimistic guidance, analysts have been raising their expectations for Cloudflare’s growth, and this has given a nice bump to expectations within my model.

Putting all this together, I can see shares of Cloudflare delivering a CAGR through to 2031 of 2%, 17%, and 28% in my respective bear, base, and bull case scenarios.

Bottom Line

This was the quarter where Cloudflare had to justify its premium share price, in an earnings season full of underwhelming results from other cloud-focused businesses. Thankfully for shareholders like myself, the company delivered once again and showed exactly why investors are putting faith in this team.

I still expect some short-term volatility, as Cloudflare’s share price looks very expensive based on short-term metrics, but I believe that this company has plenty of room ahead to reward shareholders despite its current premium price tag.

Given the strength of this business, and what I believe to be a reasonable share price given Cloudflare’s long-term potential, I reiterate my previous ‘Buy’ rating on Cloudflare shares.

Be the first to comment