Peach_iStock

Investment Thesis

Despite the fact that Cloudflare’s (NYSE:NET) price has dropped over 10%, as we previously predicted (published on Dec 6th, 2022), we believe the bottom is not in yet. We reiterate our previous valuation target and offer further analysis of the dynamics of the company’s prospects.

Review

In our previous article, we pointed out that although Cloudflare has grown significantly from its innovative business model by building a grassroots customer base, these are the low-hanging fruits it has reaped. It is entering a more fierce competition and more comprehensive demand in trending from the customers. Its offering has a feature of trading off fast and cheap over more costly fully-cloud services, and it needs a significant upgrade to realize that. But difficulties remain due to its current high debt load and continued negative net profit and earnings. Its current prices do not warrant a fair valuation from our analysis.

More Analysis

Here we want to focus on the “addressable market” Cloudflare presented in its Q3 presentation. In the presentation, it highlighted it had a $115 billion addressable market in 2022. That, compared with its current $894.1 million TTM revenue, is a huge growth potential. We believe a lot of lofty valuations were derived from this figure. The company explained that this estimate was the expected spending of the large customers based on IDC data. And this addressable market is climbing fast to $125 billion in 2023 and $135 billion in 2024 (see its slide 17). However, we beg to differ. As we pointed out in our previous analysis, the programmability of the edge has been there for a while with the CDN, Akamai EdgeWorkers (AKAM), Amazon CloudFront (AMZN) with Lambda@Edge, or Fastly Varnish (FSLY), and its recent acquisition of Glitch. This is not exclusive to Cloudflare. To say these customers’ spending is up for Cloudflare to break ground on is not an accurate description, as a lot of its competitors are not doing a bad job at satisfying their customers by offering similar services as well. In fact, for its existing customers who are not yet utilizing the full suite of the company’s services to switch fully, the cost and expenses would outweigh the benefits due to the restrictions of its platform and the efforts to rewrite the entire codebase, as we pointed out before. As we estimated before, the best market potential would come from brand-new customers who choose to utilize their entire services from the start or from incremental changes of the existing customers to migrate gradually. But the depth and fierceness of the competition run deep among these competitors. It is hard to say whether these customers would be better off or not if they migrate to its full suite, as the comprehensive cloud computing base is not there yet with Cloudflare. While some of its competitors already have the capacity to offer such. In this regard, we are still waiting to see how the experimental D1 database worked out in its next earnings report. What Cloudflare can bring is offering a lot of functions cheaper, faster, and closer to local customers, but currently with the trade-off of comprehensive full cloud service. And these are not exactly groundbreaking, either. Therefore, we feel the word “addressable market” isn’t entirely accurate for investors to fully understand the picture.

Simply put, Cloudflare does not have the hundreds of billions of dollars of the addressable market to address unless it could significantly upgrade its comprehensive cloud computing capacity, which will impose prohibitively high costs and expenses for the company to shoulder.

This is similar to something we saw in its recently published second impact report. In the report, Cloudflare claimed that it has been working on a beta version of post-quantum cryptography based on the U.S. government’s recently published standard on quantum computing that can block any future attack from quantum computers. But anyone remotely following the development of quantum computers knows that a commercially viable quantum computer has not yet clearly taken shape. Simply because the government has tried to set some early standards, it is far from establishing what the playing field would actually look like for quantum computing. To claim it can offer security against any future quantum computers is a boast far too early and far too bold to claim at this point. Just like how it was using the word “addressable market”, it is trying to offer an overly simplified cut on very complex technical problems that it is risking misleading investors and customers.

Reiterating Valuation and Target

We maintain the same valuation as we previously offered. With our most bullish scenario, where the company only suffered a slightly negative impact from the economic slowdown and eventually reached double-digit growth, the price is $43.72. While in the most bearish scenario, where the company continues its pattern of highly volatile free cash flow that eventually stabilizes into single-digit growth a few years out, the price is $25.32. And in our base case, where the company suffers some set back due to economic slowdown but eventually recovers into double-digit growth with less volatility than in the past six years, the company is valued at $30.37. Its current price of $38.91 is inching closer to our base case.

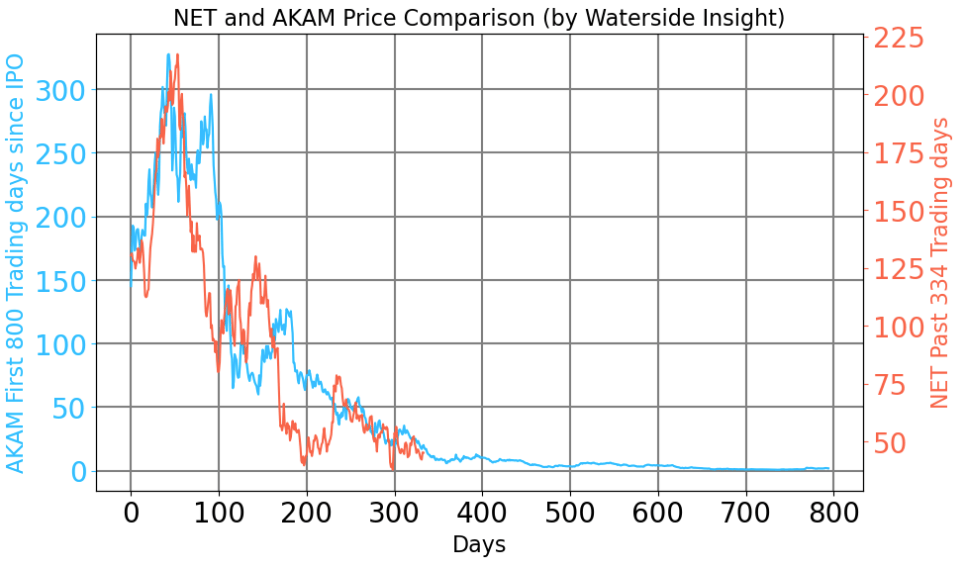

Since we previously compared Cloudflare with Akamai’s prices in its early days, we offer to refresh the chart. Since a month ago, it seems the trajectory continues.

Cloudflare vs Akamai (Calculated and Charted by Waterside Insight with data from NASDAQ)

Moreover, it seems the stock is on the cusp of breaking its previous low of $38.33. Once it is broken, technically, it could drop to as low as $20. In the last 90 days, insiders of the company have sold a total of 401,075 shares of the stock worth $19,687,059. Some of the selling prices were at $56.28. For the stock’s price to drop by more than half since its highs and the insiders were not buying but instead selling, some investors might want to take a clue there.

Conclusion

Investors have continued the price discovery journey since Cloudflare’s sharp drop from its all-time highs. As we pointed out a month ago that it was overvalued, we see its drop of over 10% since then is still not yet reaching the fair valuation of ours. Due to the high volatility, we continue to recommend investors who have not yet built a position in the stock look for a price of $25.32 or lower for a long-term holding. For the investors that heaped our advice not to buy earlier, we would say patience will pay off.

Be the first to comment