Guillaume/iStock via Getty Images

Introduction

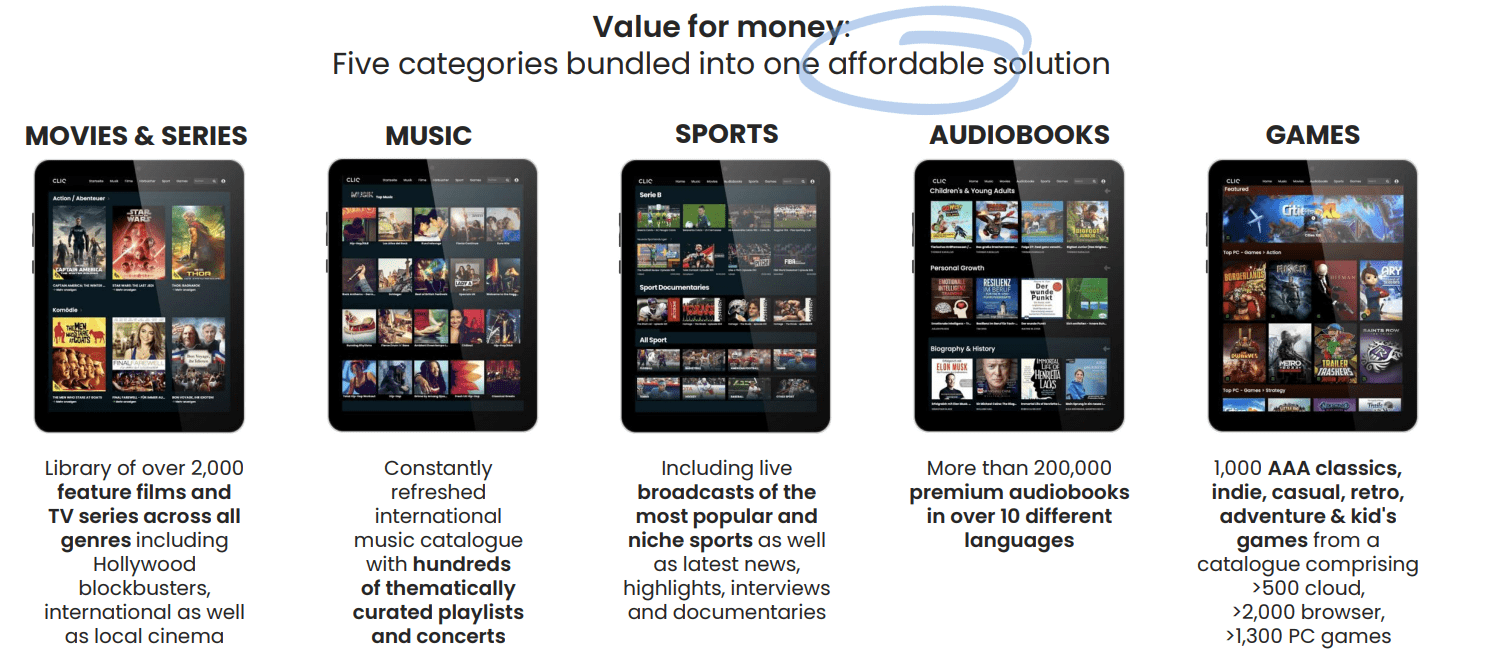

Cliq Digital (OTCPK:CLQDF) is a German company offering streaming services for its customers at a flat rate per month. Although the streaming business isn’t new and Cliq is basically competing against Netflix (NFLX), Amazon Prime (AMZN), Disney (DIS) and other local initiatives, the focus on marketing and gaining market share is paying off as the company is growing at a double-digit percentage on a quarterly basis. Cliq offers a 30-day free trial, where after a subscriber gets converted into a fully paying membership. This means the revenue growth is ‘real’: its customer base appears relatively sticky considering renewal is needed on a monthly basis.

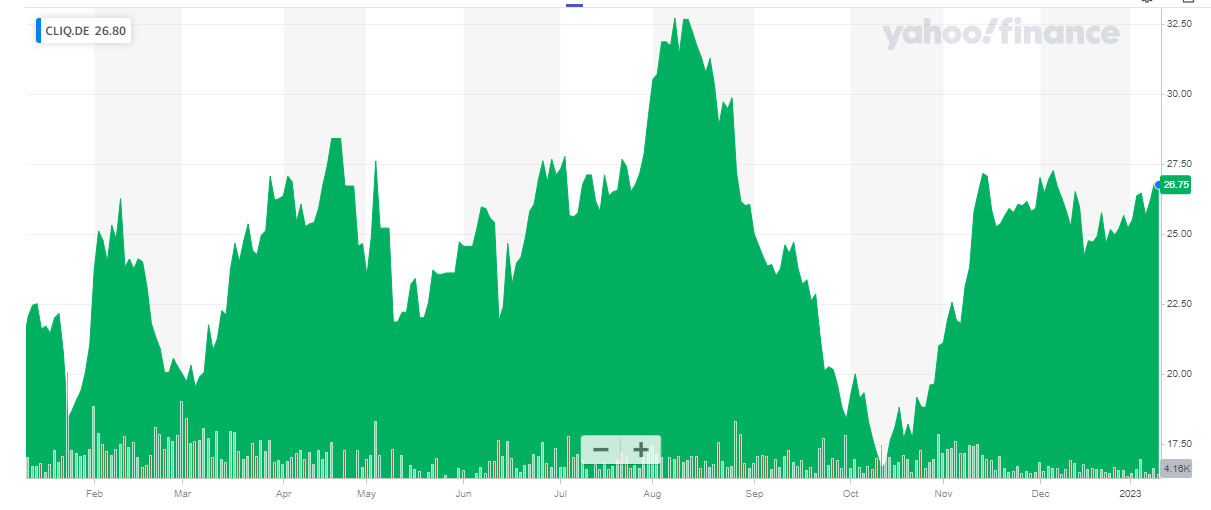

Yahoo Finance

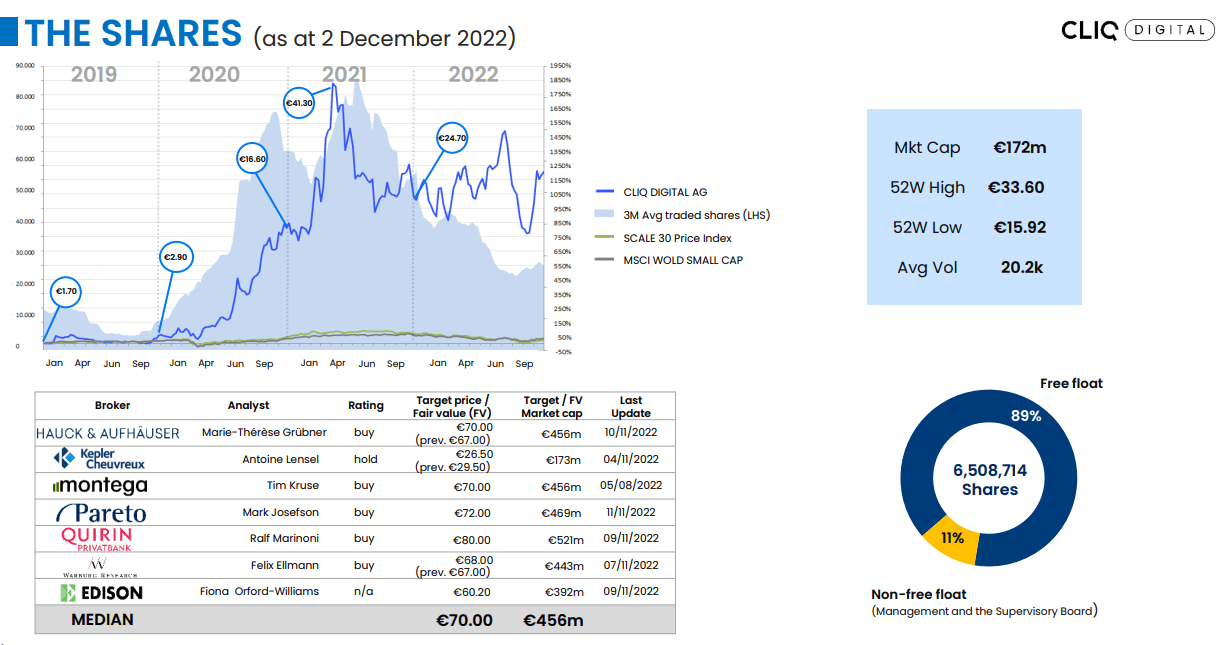

Cliq Digital has its main listing in Germany where it is trading with CLIQ as its ticker symbol. The average daily volume in Germany exceeds 15,000 shares, representing a monetary value of 400,000 EUR. There are currently 6.5M shares outstanding which means the company currently has a market capitalization of just over 170M EUR. For liquidity reasons, I’d strongly recommend to use the German listing to trade in Cliq’s shares.

The Q3 results were impressive

Fellow author Carles Diaz Caron has done an excellent job in breaking down the business model of the company so I’d like to refer you to his article to get a better background on the company – I couldn’t have explained it better myself.

Cliq Digital Investor Relations

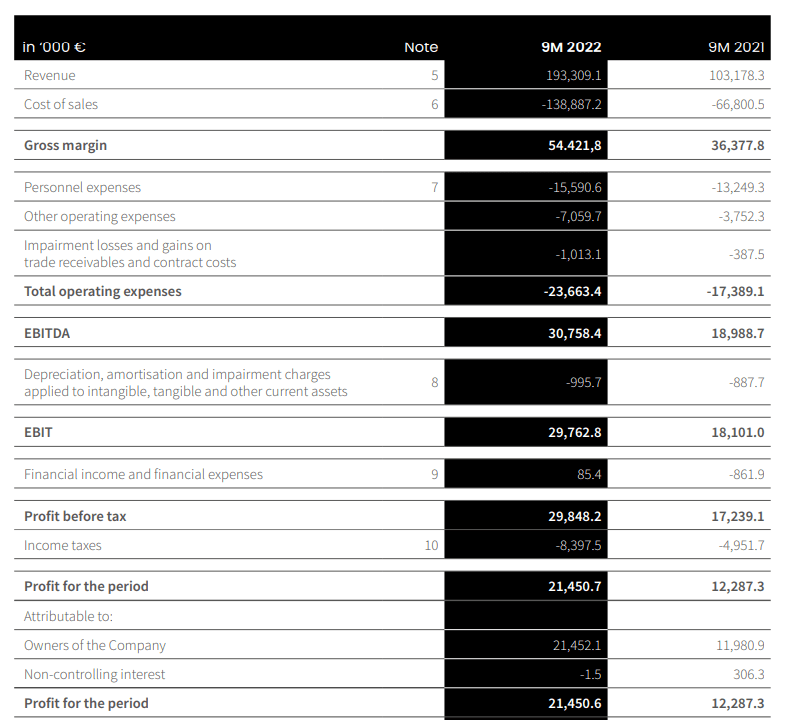

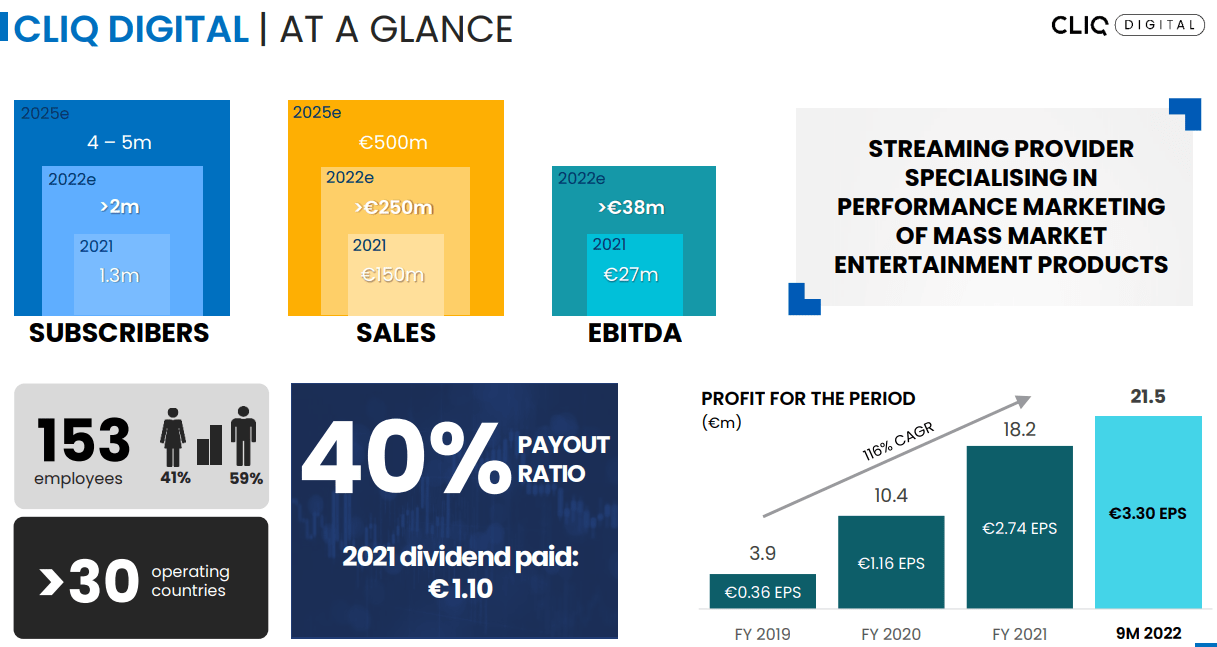

The total revenue in the first nine months of the year was approximately 193M EUR, and this resulted in a gross margin of 54.4M EUR. After deducting the personnel expenses and other operating expenses, the total EBITDA in the first nine months of the year increased by in excess of 60% to 30.8M EUR.

Cliq Digital Investor Relations

As Cliq runs an asset-light model (most of its investments are related to intangibles like broadcasting rights), the EBIT came in at just under 30M EUR. As Cliq has a net cash position, its interest expenses and finance expenses are negligible and this allowed the company to report a net income of 21.5M EUR, representing an EPS of 3.30 EUR per share.

The acceleration of the earnings is pretty clear as the Q3 EBITDA for instance, exceeded 12M EUR. Which means that about 40% of the 9M 2022 EBITDA was generated in just the most recent quarter. In its outlook for FY 2022, Cliq mentioned it anticipates a full-year EBITDA of in excess of 38M EUR. As this would imply the company needs a Q4 EBITDA of just over 7M EUR to meet this target, I’d argue there’s a good chance Cliq’s full-year EBITDA may actually be closer to or even exceed 40M EUR.

Cliq Digital Investor Relations

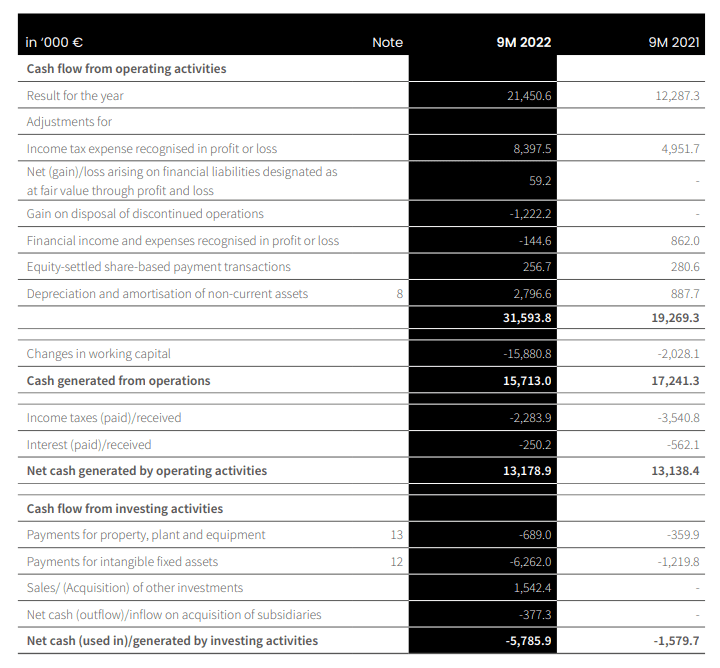

The total operating cash flow during the first nine months of the year came in at 13.2M EUR. This included 2.3M EUR in income taxes although the company owed in excess of 8M EUR based on its income statement (see above). The reported operating cash flow also includes about 15.9M EUR in working capital investments and excludes the (negligible) lease payments. On an adjusted basis (and taking a correct cash tax payment into account), Cliq’s operating cash flow was 22.9M EUR.

Cliq Digital Investor Relations

The total capex was almost 7M EUR and this was mainly related to the acquisition of intangibles 3.3M EUR was invested in the platform and new licenses to stream movies were acquired for 3M EUR). The underlying free cash flow was roughly 16M EUR or just under 2.5 EUR per share.

Cliq Digital Investor Relations

The very clear dividend policy means investors will be rewarded

Cliq Digital plans to use 40% of its net income to reward its shareholders with a dividend. Assuming an 8M EUR EBITDA in Q4 (I expect the Q4 EBITDA to be higher), the net income will likely be 5-5.5M EUR for an additional 80 cents per share (based on the midpoint).

That would bring the full-year earnings to 4.10 EUR per share, and the dividend would subsequently be 1.64 EUR per share.

Cliq Digital has ambitious growth plans. It aims to reach 500M EUR in annual revenue by the end of 2025 and assuming the EBITDA margin of 15% doesn’t change much (although I would expect marketing expenses to decrease as Cliq reaches critical mass), this would imply an EBITDA result of 75M EUR from FY 2025 on.

Cliq Digital Investor Relations

We already know the depreciation and amortization expenses are almost non-existent and given the strong cash-rich balance sheet, Cliq could actually earn money on its cash position. But let’s assume it doesn’t and let’s assume the average corporate tax rate will be 30%. In that case, the company’s net income would come in at 50-51M EUR for an EPS of 7.5-7.75 EUR per share. Applying the same 40% payout ratio would imply a dividend of at least 3 EUR per share.

Cliq Digital Investor Relations

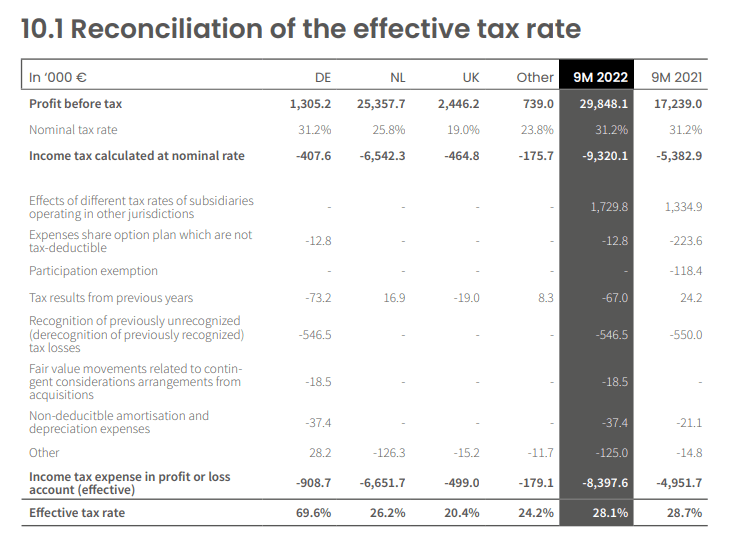

The company is followed by seven analysts of which Kepler Cheuvreux likely is the most credible name and it is not a surprise Kepler also has the most conservative target price.

Cliq Digital Investor Relations

Investment thesis

This would imply the stock is currently trading at just 3.5 times the anticipated 2025 earnings, and at an EV/EBITDA of just 2.5. It looks like the market still has issues to trust and believe Cliq Digital’s performance and outlook, and I have to admit I am also a bit skeptical, mainly because I don’t have direct experience with its streaming catalogue and product offerings, and because it may not be easy to compete with the big boys. That being said, Cliq Digital has been around for a few decades and has a track record of increasing revenue and earnings.

Its financial statements for the FY 2021 annual report were audited by Mazars, a well-respected French firm and you may remember the name from the fight over the disclosure of president Trump’s financial records. More recently, Mazars was hired by Binance to audit the company subsequent to the collapse of FTX, but before it could complete the task, Mazars stopped dealing with crypto-related companies. So although Cliq Digital isn’t audited by one of the Big Four, its auditor is not just an accountant in a windowless office above a pizza place, which strengthens my belief the financial statements can be relied on.

I’m on the sidelines for now as I will be looking for customer testimonies.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment