We Are

Falling Markets Put Quality on Sale

Market Overview and Outlook

Equities reeled in the second quarter as persistent price pressures, global supply chain disruptions and rising recession risks soured sentiment on a post-pandemic recovery looking too big for its britches. The benchmark Russell 3000 Index fell 16.70%, weighed down by substantial declines in the consumer discretionary (-25.73%), information technology (IT; -21.37%) and communication services (-21.02%) sectors.

Disruptions in global supply chains stemming from COVID-19 lockdowns in China, the Russian invasion of Ukraine and commodity shortages continued to propel inflation higher. A worse than expected 8.6% Consumer Price Index reading for May caused the Fed to raise rates 75 bps in June, the most aggressive hike since 1994, and project ambitious tightening through the rest of 2022. The 10-year Treasury yield climbed 67 bps to finish the quarter at 3.01%, near its highest level in four years. The U.S. economy contracted in the first quarter and the outlook for GDP growth has tempered as more liquidity leaves the financial system.

While consumer demand has mostly held up, a shift in spending patterns from goods to services led to big first-quarter earnings misses and lowered outlooks for several retailers and social media platforms that are leading digital advertisers. This drove much of the retreat in the consumer discretionary and communication services sectors, while higher interest rates weighed on technology shares, along with the broad fears of a recession and demand destruction that hit cyclical financials and materials stocks.

The health care, consumer staples and utilities sectors showed their characteristic defensiveness, outperforming handily in a down market. While our consumer staples and utilities holdings held up less than we hoped (high energy costs in Europe hurt Hain Celestial’s (HAIN) margins and outlook, while higher interest rates weighed on Brookfield Renewable (BEP)) individual health care standouts were the top contributors for the quarter, driven by a mixture of market sentiment and stock-specific news. UnitedHealth Group’s (UNH) high-quality traits made it attractive while higher-multiple, more speculative stocks sold off. While biotechnology got a bid from increased M&A interest, our biotech holdings also showed fundamental strength: Gilead Sciences (GILD) beat bottom and topline estimates driven by strong sales of its HIV and COVID-19 drugs; BioMarin Pharmaceutical (BMRN) was up as Japan granted approval for its Voxzogo injection to treat achondroplasia in children and received conditional approval for its hemophilia gene therapy in Europe.

We reinforced our defensive capabilities during the quarter with the addition of Johnson & Johnson (JNJ), a diversified health care company with a strong balance sheet, attractive profitability and return metrics and the ability to generate steady moderate growth. It has one of the more diversified and attractive pharmaceutical portfolios and an improving medical technology business, and it will soon be exiting the lower-growth consumer business. We believe new management has sharpened the strategy to improve execution in the medical device business and look for more meaningful capital allocation opportunities, which the balance sheet can easily support. Johnson & Johnson’s products and services have a clear positive impact on human health. The company’s long-held credo sets the tone for ethical business practices and considering all stakeholders in guiding its decision making and prioritizing patients and caregivers. The company also contributes to 11 Sustainable Development Goals (SDGS) through its Health for Humanity 2025 goals.

Prologis (PLD), another addition, performed well. Prologis is a global leader in logistics real estate. We believe the company should benefit from long-term demand growth for warehouse space due to increasing e-commerce penetration and increasing focus on supply chain resiliency. Prologis’s portfolio is focused on markets characterized by large and growing population densities and high barriers to entry, typically near large labor pools and extensive transportation infrastructure, which should translate to strong operating performance over the long term. Part of Prologis’s competitive differentiation is its sustainability leadership, which helps customers achieve their own sustainability goals. For example, the company has committed to achieving green building certification for 100% of its new development and its top 25 customers have chosen green-certified space for over half of the square footage they lease. The company also works closely with customers to implement efficiency improvements and install onsite solar with no upfront costs to the customer (through its onsite solar program Prologis has become the third-largest corporate owner of solar capacity in the U.S.).

In a severe market selloff driven by macro worries it is not surprising to find mega caps like Apple (AAPL), Microsoft (MSFT) and Amazon.com (AMZN) among the main detractors, although there is no change in our long-term theses on these companies. Apple is one of the largest technology platform companies in the world, with a very large, sticky installed base of users. Despite potential iPhone delays due to China-related supply issues, we continue to view promotional activity from global carriers and share gains versus Huawei in China and Europe as important markers for how resilient iPhone demand can be heading into the iPhone 14 cycle. In the case of Microsoft, a weakening macro environment notwithstanding, we are positive on its demand profile and a very long tail of growth for the markets in which it participates, such as cloud, as well as the potential for the company to benefit as customers consolidate providers in a weaker economic environment.

Inflationary pressures and overcapacity in e-commerce delayed margin improvement for Amazon.com, although passing on inflationary impacts to consumers is an industry-wide issue rather than a company-specific one. We also believe Amazon is well-positioned to emerge stronger from this difficult operating environment of higher costs. There is a visible path to margin expansion driven by a positive mix shift as the more profitable businesses of third-party sellers, cloud and advertising become the largest contributors. Amazon’s improved delivery speeds should help revive its trajectory of steady market share gains.

Market volatility often provides compelling opportunities for active investors to step in when good companies are trading at a discount. Such was the case with online search and advertising leader Alphabet (GOOG, GOOGL), which we have owned previously, sold in late 2020 due to a regulatory overhang, and bought again this quarter at an attractive valuation. We believe Alphabet will maintain its leading position in search and will benefit from growth in other businesses such as YouTube and cloud. While we acknowledge Alphabet’s scrutiny from regulators, we believe that in relation to social media, search is less problematic and of lower priority. Alphabet has been carbon neutral since 2007 and has focused on maximizing the efficiency of its data centers. It also has invested heavily in data privacy and security.

Looking ahead, we need to balance the worsening outlook for the economy with greatly improved valuations in many areas of the market. The underperformance of growth relative to value has left many high-quality companies with excellent sustainability profiles much more attractive. We think that area of the market could be beneficial as we look out over a longer time horizon.

Portfolio Highlights

The ClearBridge Sustainability Leaders Strategy outperformed its Russell 3000 Index benchmark during the second quarter. On an absolute basis, the Strategy had losses in all 10 sectors in which it was invested (out of 11 sectors total). The main detractors were the IT, consumer discretionary and financials sectors, while the real estate, utilities and materials sectors detracted the least.

On a relative basis, overall stock selection and sector allocation contributed positively to performance. Stock selection in the IT, consumer discretionary and financials sectors, a health care overweight and an underweight to the communication services sector helped relative results the most. Conversely, stock selection in the consumer staples, industrials, utilities and health care sectors and a lack of energy holdings were detrimental.

On an individual stock basis, BioMarin Pharmaceutical (BMRN), Gilead Sciences (GILD), Prologis (PLD), Progressive (PGR) and UnitedHealth Group (UNH) were the largest contributors to absolute performance in the quarter. The main detractors from absolute returns were positions in Apple, Microsoft, Amazon.com, Bank of America (BAC) and Walt Disney (DIS).

During the quarter, besides portfolio activity discussed above, we exited positions in Lam Research (LRCX) in the IT sector and Comcast in the communication services sector.

ESG Highlights

Analyst-Led Engagements Uncover Value

Environmental, social and governance (ESG) investing has made much progress over the last two decades. Investors in public equities and corporations have taken more ownership of the impact they can have mitigating climate change and making progress on social goals such as diversity, equity and inclusion; ESG data and investment products have proliferated; and ESG assets under management have continued to grow, with most continuing to be actively managed.

Amid such growth has come scrutiny over potential differences between the claims and realities of ESG investing. This has come on the part of regulators, asset owners and increasingly in the public eye, among business and government leaders.

In this environment we think it worthwhile to highlight the value added by ClearBridge engagements and their role in our investment process and stewardship activities. We have made steady improvements and progress in our process, marked by several milestone years, from 2005, when we established a central research platform that began integrating ESG factors by sectors, to 2012, when we explicitly incorporated ESG analysis in analyst compensation and performance reviews, to 2014 when we formally introduced proprietary ESG ratings, which capture company-specific drivers of risk and return related to sustainability. Currently, 100% of our actively owned companies have an ESG rating assigned.

A key through-line in our history of ESG integration, and a key point of differentiation, is that it is carried out by our analysts: we think there is immense value in having the same person responsible for covering a company’s fundamentals and its ESG characteristics. Company engagements, therefore, are likewise led by ClearBridge sector and portfolio analysts, an approach that we believe gives them insights that might not be top of mind for other investors and a fundamental edge, gained through long-term discussions with CEOs and CFOs of portfolio holdings.

Transforming Climate Risks to Opportunities

In many cases, ClearBridge engagements have specific objectives, such as encouraging the retirement of fossil fuels and increasing use of renewables. Such has been the case with electric power company AES (AES), with whose executives and board members we have been engaging for several years on the company’s path to reduce its carbon footprint. We believe our voice, as a top shareholder, has been a valuable addition to AES’s decision making along this path, and our engagements have helped us identify where climate-related risks in a company’s operations could be climate-related opportunities.

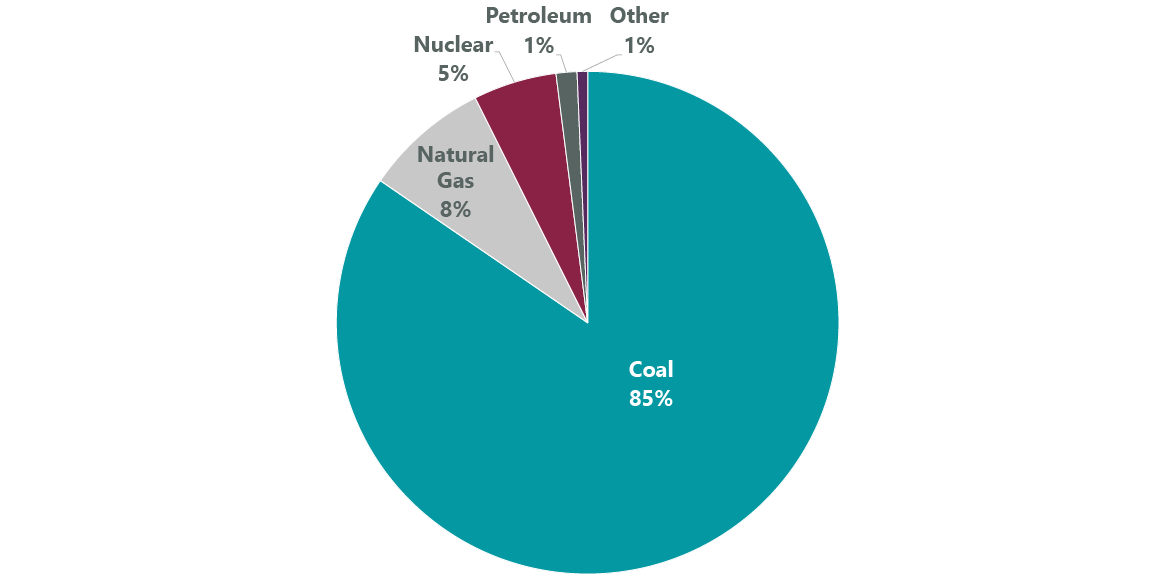

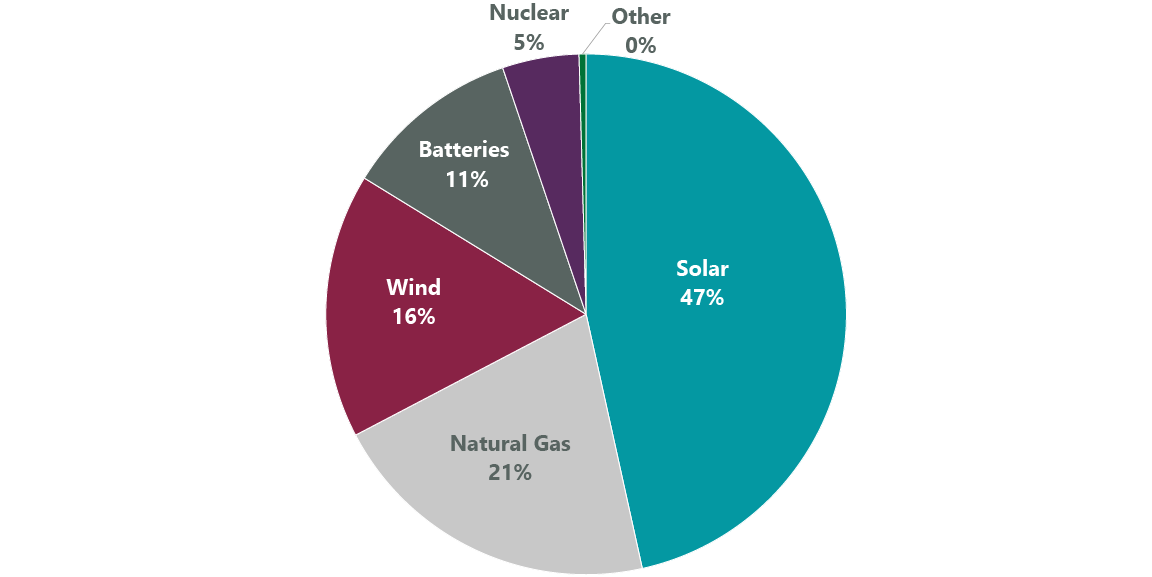

Several years ago, we began discussing with AES the lack of terminal value from coal (Exhibit 2), and we expressed how coal-related ESG concerns were weighing on AES’s valuation multiple, as the ESG risk premium was rising. We helped convince AES to stop investing in coal plants and start shutting down existing coal capacity. The next step was to add renewable energy exposure in the form of wind, solar and industrial scale battery storage (Exhibit 3), in line with U.N. Sustainable Development Goal (SDG) 7: Affordable and Clean Energy (we discuss how an investment framework may further the SDGs in our 2022 Stewardship Report). We shared our belief that any lost near-term operating earnings would be made up with a higher valuation multiple.

Exhibit 1: Planned U.S. Utility-Scale Electric Generating Capacity Retirements 2022 (14.9 GW Total)

As of Jan. 11, 2022. Source: U.S. Energy Information Administration.

Exhibit 2: Planned U.S. Utility-Scale Electric Generating Capacity Additions 2022 (46.1 GW Total)

As of Jan. 11, 2022. Source: U.S. Energy Information Administration.

As our discussions have progressed, AES has been increasingly aggressive in reducing its carbon intensity by lowering coal capacity and investing in renewable energy, as evidenced by its declining GHG emissions. As we had anticipated, AES’s valuation multiple recovered as its product mix shifted from coal to renewables.

ClearBridge encourages companies to align their net-zero goals with the Science Based Targets Initiative’s (SBTi) standards, which clearly define pathways for companies to reduce carbon emissions in line with the Paris Agreement goals. In April 2022 we met with AES Investor Relations and its General Counsel to discuss setting science-based targets as the latest step in this path, and in line with SDG 13: Climate Action. At the meeting, AES confirmed it is exiting coal in 2025. The company continues to develop as a leader in renewable energy, in June 2022 announcing the formation with other leading U.S. solar companies of the U.S. Solar Buyer Consortium, which will invest more than $6 billion in solar panels to scale up domestic solar manufacturing.

Grasping Realities Behind Net-Zero Targets

Environmental impact is a major issue for the transportation industry, including logistics and freight companies such as portfolio holding United Parcel Service (UPS). Recent engagements with the company have given us a better understanding of the challenges in lowering emissions in transport as well as where innovations may be coming from in the years ahead. In ESG-focused engagements in March and May 2022, we discussed UPS’s path to net-zero using science-based targets.

Though it has a 2050 net-zero goal in line with SBTi, UPS has issues complying with SBTi standards because aviation constitutes 60% of UPS’s Scope 1 and 2 emissions. This is an area over which UPS has little control, however, and the maximum exclusion for a source of emissions for SBTi approval is 5%. UPS has committed to a 2050 carbon neutral goal, which is the same as the SBTi’s goal, although UPS takes a different view of the first 15 years of the path, finding existing technology unable to warrant as aggressive a path as SBTi’s.

Over the course of our engagements, we discussed the technical challenges facing the logistics and freight industry and the state of several key technological developments that will be crucial to helping the industry continue to lower emissions. For example, UPS is looking to sustainable aviation fuels, which are biofuels used to power aircraft with a smaller carbon footprint than jet fuel; however, planting to create the enormous amount of feedstock required to replace crude oil is not sustainable. Electric aircrafts are another potential solution, and UPS will have the first of 10 electric aircraft by Beta Technologies delivered by 2024, with an option for 1,400 more. While these planes help time-sensitive health care deliveries and benefit small and medium-size businesses, they have a range limited to 250 nautical miles. A more sustainable path, particularly for long-range transportation, could be the use of hydrogen, but the technology and infrastructure is in nascent stages of development and largely out of UPS’s control. We have encouraged the company, however, to increase pressure on its suppliers to accelerate the development of these technologies. ClearBridge also has ongoing active discussions with aerospace manufacturers on these issues.

Connecting Governance and Long-term Shareholder Value

In addition to finding value in engaging on climate risks, net-zero targets and new technologies, we also add value to our investment process with engagements on a variety of governance topics. For example, we have long supported toy and game maker Hasbro’s (HAS) management and board on strategic, operational and ESG-related topics; the company ranks highly on almost all areas of ESG evaluation, including diversity at board and all-employee levels. We maintain long-term relationships with Hasbro management, and in April 2022, after an activist shareholder started pushing for strategic change at the company, we stepped up our dialogue with senior management and the board.

While we appreciate some of the concerns raised by the activist, we were against most of its suggestions, which we believed would be destructive to long-term shareholder value. We did not believe it was in our best interest to replace three board members with activist-nominated board members — the existing board is replete with talent from the media, technology, content, gaming, entertainment and social media industries.

Over multiple meetings with Hasbro’s CEO and CFO and as many as three board members, our strong relationships helped us better understand what changes would be made where appropriate, and what strategies would remain intact. We had frequent opportunity to share our thoughts on board composition, long-term strategic priorities, compensation, capital allocation and disclosures. All of these became import topics for review during this time. In June 2022 the activist’s proposals were rejected by shareholders. We remain in support of management as it continues on its path of brand-building and growing digital content for its customers.

Advancing a Smart Farm Future

In our engagements with farm equipment maker Deere (DE), we have followed new technology as it has developed from early promise of environmental and social benefits to market reality. In March 2022, Deere’s Chairman & CEO and CFO met with ClearBridge’s investment team in our New York offices. While prior to the pandemic we had regularly hosted the company, this meeting was among the most interesting as the relatively new CEO outlined a bold plan that placed improved environmental stewardship squarely at the center of the company’s future.

Industrial farming, at its core, is not an especially environmentally friendly enterprise. Agronomic practices have improved over time, but fertilizer, herbicide and pesticide applications and water usage remain problematic. Deere believes its precision farming technology can drive down chemical and fertilizer volumes materially — possibly by as much as 70% — as sensors and cameras attached to tractors, sprayers and combines help determine the exact level of chemicals that might be required. This more precise methodology is expected to: 1) improve crop yields; 2) reduce farmer input costs; and 3) improve overall land management capabilities. Farmers will make more money and grow more food to support global populations while at the same time better caring for the soil. There are also substantial environmentally positive knock-on effects because fertilizers largely are either carbon-based or mined.

There are also social benefits to Deere’s precision farming, such as increasing access to cost savings for smaller, non-commercial or family farms, and the contribution of improved crop yields toward SDG 2: Zero Hunger. This is in addition to its benefits for SDG 15: Life on Land through promoting sustainable use of terrestrial ecosystems. Deere’s technological strength also includes bringing connectivity to farmers in emerging markets, for example improving Wi-Fi access for farmers in Brazil.

New equipment pricing has moved much higher recently as Deere upgrades its offerings to support this effort. That said, the company has introduced substantial aftermarket packages so farmers using older equipment, who may not be able to afford completely new items, benefit from this technology.

Lastly, we discussed a timeline for transitioning large farm equipment away from diesel to an alternative fuel. At present, however, there is no viable alternative that has the power requirements necessary to drive a tractor for an hour, much less a full day, making any such transition a more distant opportunity.

Overall, we had been waiting to have this discussion for several years, and we were pleased the company’s technologies finally appear to have caught up to precision farming’s initial promise.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment