Clear Secure, Inc (NYSE:YOU) is a technology company that was able to capitalise on the 2021 IPO craze which saw the company become public on the 29th of June 2021. YOU operates as a technology company that enables frictionless and safe travels using one’s biometric identity. As will be discussed in more detail below, the technology has the capability of providing streamlined services in a wide array of industries such as; events, healthcare, and sporting stadiums. The main use for the CLEAR brand however is within airports. Its identity platform connects passengers to the cards in their wallet transforming the way passengers live, work, and travel.

Company Website

CLEAR allows for a quick identity verification experience. In which a user would step right up to a CLEAR pod and verify you are you with your eyes or fingerprint instead of waiting to show government issued photo I.D.

Members enroll in CLEAR to create an unbreakable link between their identity and biometrics (e.g., eyes, face and fingerprints). CLEAR’s current offerings include: CLEAR Plus, a consumer aviation subscription service, which enables access to predictable and fast experiences through dedicated entry lanes in airport security checkpoints nationwide; the flagship CLEAR App including Home to Gate and Health Pass; and Reserve powered by CLEAR, our virtual queuing technology that enables customers to manage lines.

Given the startup nature of the business, and the lack thereof a fundamental catalyst for investors to consider, the uptake in ownership, adds credibility to the sentiment around YOU.

While 2022 has been a year to forget for many companies built on the qualitative aspect of investing (as opposed to quantitative earnings), given the company’s short tenor as a public company, YOU may see growth in the near term as travel demand resurges to pre-covid levels. This, coupled with record revenue earnings reported by airlines, could be the catalyst that sees the company move from the 2022 lows.

We were expecting a very busy summer travel season, which we had at Clear had termed, ‘travel to lose us’.

Ken Cornick, CFO

The Current State Of The Company

The macroeconomic environment will continue to cause headwinds for most companies on an aggregate level. This is ever-more-so seen within the ‘loss-making-tech-stocks-of-2021’. This unfortunately is the classification in which Clear Secure has been aggregated into. It is often forgotten that the stock market and the economy can become disjointed. Rising interest rates, coupled with crippling inflation, will continue to pressure consumers into reducing spending, directly affecting the industries that YOU services the most.

These are still early days at Clear and while there is plenty of discussion in the market about a recession, our business has not experienced any evidence of a travel or economic slowdown… We are also well-equipped to manage through various economic environments as evidenced by Clear financial performance during the pandemic, when travel declined by almost 100%. Our bookings declined by about 10% while our margins and free cash flow expanded.

Ken Cornick, CFO

Looking further than the immediate short term, the opportunity is significant for YOU. The technology is proven and currently in place, and with institutional backing from some of the largest players within the travel industry, uptake in a system that increases consumer utility in an environment which has seen it disappear, will prove to be vital for companies attempting to navigate multi-decade low consumer confidence.

As reported throughout 2022, airlines are “slashing flights due to staffing shortages” and will need to reduce costs to fight off inflation. The streamlined nature of the technology and the potential to reduce labour costs for companies will be the catalyst necessary for growth.

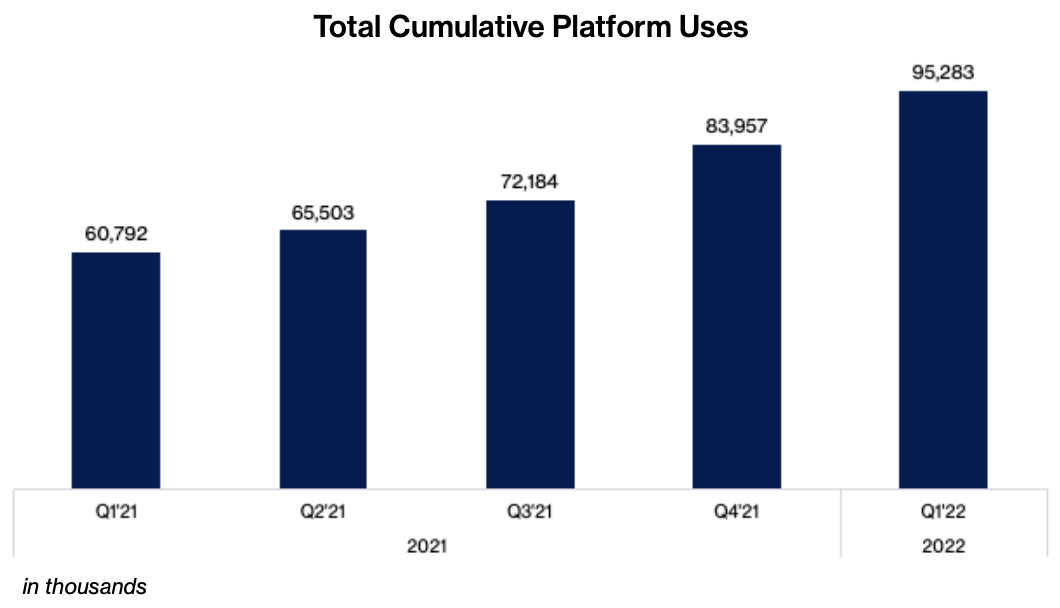

Company Presentation

Clear Secure has suffered a ~55% drop from its August 2021 high, dropping its valuation to relatively attractive levels. The company continues report negative earnings, however it is important to understand how US GAAP ensures companies recognise revenue when it is earned. Management spoke on this in more detail during their Q2 earnings call:

So as a reminder, so with a subscription business, since we’re an annual biller, we have GAAP revenue, which lags behind our cash receipt. So if a member pays us $189 today, that’s a booking of $189. The GAAP implication of that is it gets amortized or deferred over the 12-month period of the subscription. And so that’s why you see free cash flow exceed the GAAP metrics. Adjusted EBITDA while not a GAAP metric in and of itself is based off of GAAP revenue, and most — basically all of our costs, cash and GAAP are the same. So we recognize all the costs upfront cash and GAAP while the revenues are deferred and that’s why the adjusted EBITDA again, is based off of GAAP revenue and our free cash flows in excess. And in terms of, CapEx, we are fairly capital efficient business and so over time as GAAP catches up to bookings, those would converge, but since we’re, growing today, that is — there is that lag and therefore free cash flow is higher than the GAAP metrics.

Ken Cornick, CFO

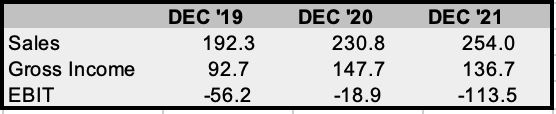

Company Financials

Relative Value

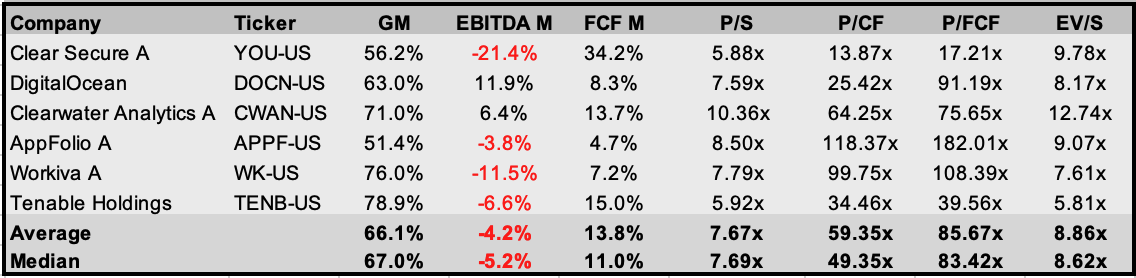

Clear Secure operates as a technology company, offering services to consumers to streamline processes that they undertake with other businesses. This causes a significant issue in considering peers to conduct a relative valuation. Considering this, I have assembled the below peers that see their revenue attributed to similar factors.

YOU does post lower gross margins than its peers, but as management attributed to above, Free Cash Flow and adjusted EBITDA are much more representative of the earning power of the company. This is evident in the materially higher FCF margin relative to its peers, more than doubling TENB – the second highest FCF margin.

Given the nature of the sentiment around the business, and the stigma around technology IPOs launched in 2021, YOU has found its share price at levels that present the vigilant investor with an opportunity. This is further made evident by the below average Price to Sales, Price to FCF and EV to Sales ratios below, placing YOU in an attractive position.

FactSet

Final Thoughts

There are many secular tailwinds that could be the catalyst for long term growth prospects for YOU. This however must be considered in conjunction with the headwinds that the short term macro environment presents. However, YOU is a well managed company. Businesses that introduce the technology often view it as a mechanism for cost reduction and thus can continue to be continually rolled out in the near term. I believe that there will be short term volatility in the share price, but believe that the distribution is skewed to the upside.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment