Teera Konakan/Moment via Getty Images

Thesis highlight

Clarivate (NYSE:CLVT) has 32% upside. The company has an attractive business model with high barriers to entry, which includes high pricing power and excellent top-line visibility due to its recurring revenue model and high customer retention rates. Additionally, CLVT has recently undergone restructuring and improved its profitability, which I expect to continue in the future.

Company overview

CLVT is a leading player in the global information services and analytics industries, focusing on the scientific research, intellectual property, and life sciences verticals. It helps its customers safeguard their content, patents, and brands by providing them with structured information and analytics that facilitate the discovery and commercialization of new ideas.

Positive trends in the industry

CLVT is a part of the worldwide information services and analytics industry, which is flourishing for a number of reasons. The predictive power of analysis is increasingly important in today’s business world, and as a result, more and more organizations are in need of services like CLVT to help them make better decisions based on data and analytics. Accelerating change in the businesses of CLVT’s customers has also increased demand for the service and opened up new opportunities for it to be put to use.

It’s clear that consumers of data and analytics products are taking novel tacks when it comes to making intricate managerial choices. Predictive and prescriptive analytics, in my opinion, are becoming increasingly important to these clients as they seek to incorporate them into their decision-making procedures. Customers like these are using what I call “smart data” to look into the future and make predictions rather than relying on “traditional” historical data.

Leading position in the industry

CLVT provides its target industries with an array of cutting-edge information and analytical products and services. They meet the worldwide need for in-depth, sector-specific content and analytical tools by implementing CLVT solutions. Management claims that their flagship products are unrivaled in their fields.

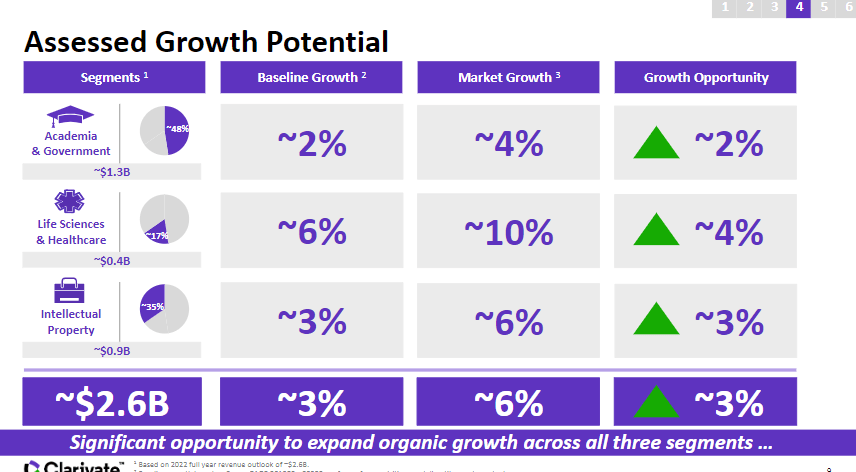

Aside from that, I believe CLVT’s growth prospects are compelling due to customer demand for curated high-quality data and the support of positive trends in final markets. Increases in international spending on research and development, demand for information services in developing economies, the speeding up of electronic commerce, and the rising number of patent and trademark applications are all examples of such trends.

Attractive business model with high barriers to entry

As a result of the one-of-a-kind nature of the content and the high costs associated with replication, businesses providing information services are typically of a higher quality and more difficult to enter. These companies have high pricing power and excellent top-line visibility as a result of their recurring revenue models and high customer retention rates. Companies specializing in information services also enjoy a high profit margin of their own. New customer acquisition costs are low relative to overall sales revenue, leading to substantial incremental margins. Because of their low capital requirements, these businesses are able to convert their revenues into substantial amounts of free cash flow.

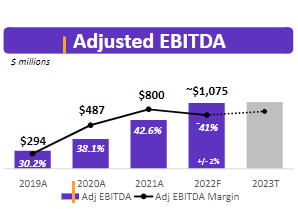

CLVT belong to this category of business. The company’s subscription and recurring revenue share is relatively high (80% of total revenue) and its churn rate is relatively low (>90%). In addition, CLVT’s profitability has been significantly enhanced as a result of several restructuring actions taken since the merger with Churchill Capital. From the most recent earnings report in 3Q22, we can see that CLVT has already improved margins to low 40s, (which is over 1,000 bps higher than 2019 levels) and management is targeting an EBITDA margin in the low 40s for the foreseeable future,

Since the company’s incremental margins are so high, I anticipate that the natural operating leverage will continue to yield positive results going forward. As the company de-levers following a period of heavy M&A activity, I expect the FCF conversion rate, which is currently around 50%, to rise.

3Q22 earnings

Pricing power

Thomson Reuters’ ownership period coincided with a decline in new product development funding and an increase in reliance on third-party contractors. In addition, CLVT lacked the essential components to track product consumption and combine disparate data sources for insightful new insights. Although many of the data sets were essential and embedded in customer workflows, pricing had previously been under-utilized. CLVT has invested 5-6% of sales in capital expenditures and R&D since its split from Thomson Reuters, allowing the company to build the necessary infrastructure and significantly reduce its reliance on outside contractors for development. As a result, the company’s management has been able to steadily raise prices as the pace of new product development quickens. Given the essential nature of the role played by CLVT’s product, I anticipate future price increases. Indeed, in 3Q22, CLVT mentioned that they had delivered healthy pricing gains of 4% and that retention rates continued to hold strong at 92%.

New sales team should improve cross-selling opportunities

Since a large portion of CLVT’s customer base is held over from its legacy operations and was previously poorly served by the previous team of sales reps, the company has experienced higher than average customer churn and has earned a well-deserved reputation for being difficult to do business with. The new CLVT has expanded its in-house sales team in order to better meet the needs of its clientele, and I anticipate this will result in higher levels of client satisfaction and increased cross-selling of related products. I think there is room to increase retention rates from their current 90%, as customers who use two or more products are notoriously loyal.

Core organic growth continues to meet expectations

Results for CLVT’s organic revenue growth in 3Q22 fell short of expectations due to lower-than-expected revenue from large transactions in the Life Sciences & Healthcare business. That said, CLVT reported that 95% of its operations met or exceeded expectations in the third quarter, and that overall subscription revenue growth was 4% in 3Q22.

I believe that the inconsistency of consumer spending that is unrelated to macro or competitive factors makes it challenging to predict the smooth flow of transactional revenue and to plan for its future impact. The good news is that management wants to stop counting one-off deals as part of their guidance and focus instead on growing their stream of recurring revenue. What matters is that growth in recurring and subscription income is sustained on the strength of price increases, customer loyalty, and new business generated through creative upsells and other means. Over the next few years, I anticipate an acceleration in organic revenue growth as a result of management’s efforts to innovate products and better align commercial channels, resulting in market growth of 6%.

3Q22 earnings

Streamlining portfolio

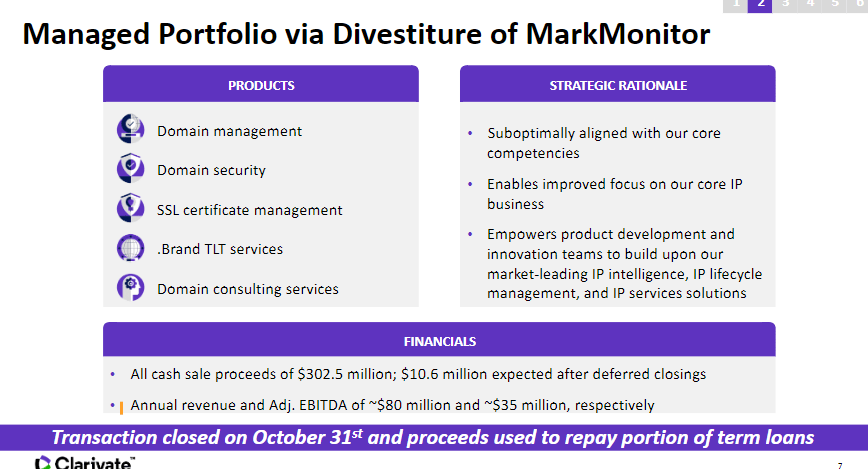

Having sold MarkMonitor for $302 million, CLVT has been able to streamline its portfolio and allow its management to prioritize investments in its core portfolio supporting IP lifecycle management.

3Q22 earnings

Valuation

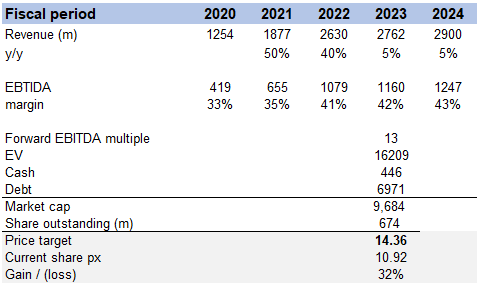

According to my model, CLVT is worth $14.36 in FY23. The core of my thesis is that CLVT can continue to accelerate organic growth by leveraging its pricing power and seizing new growth opportunities. Furthermore, I expect CLVT’s profit margins to improve as it scales, resulting in higher FCF conversion. CLVT should be able to continue reducing its debt profile as its profitability and FCF improve, which could act as a catalyst to improve its valuation.

If CLVT continues to grow at its current rate, it should be able to generate $1.2 billion in EBITDA in FY24. While I expect valuation to improve due to a lower debt profile, we could see 32% upside even at the current forward EBITDA multiple.

Own valuation

Risks

New CEO

The previous CEO clearly did an excellent job in turning around the CLVT business, as evidenced by all financial metrics. More importantly, the CEO had a solid reputation in the company’s previous line of business, which I believe contributed significantly to investor confidence in him. A change in CEO, like any other business, introduces execution risks. If the new CEO fails to deliver right away, it will undoubtedly undermine investor trust.

M&A

M&A has been a core strategy for the company, which raises the possibility that they will overpay, under-deliver, or mis-execute on integrating those acquisitions. This risk is heightened by the new CEO, whose strategies will require more time to validate.

Conclusion

CLVT has a leading position in the global information services and analytics industry, focusing on the scientific research, intellectual property, and life sciences verticals. I believe the industry is flourishing due to increasing demand for predictive and prescriptive analytics, and CLVT provides cutting-edge information and analytical products and services to meet this demand. On top of this, CLVT also has an attractive business model with high barriers to entry, resulting in high pricing power and excellent top-line visibility due to recurring revenue models and high customer retention rates. Additionally, CLVT has recently undergone restructuring actions and improved margins, targeting an EBITDA margin in the low 40s for the foreseeable future.

Be the first to comment