tupungato/iStock Editorial via Getty Images

Introduction

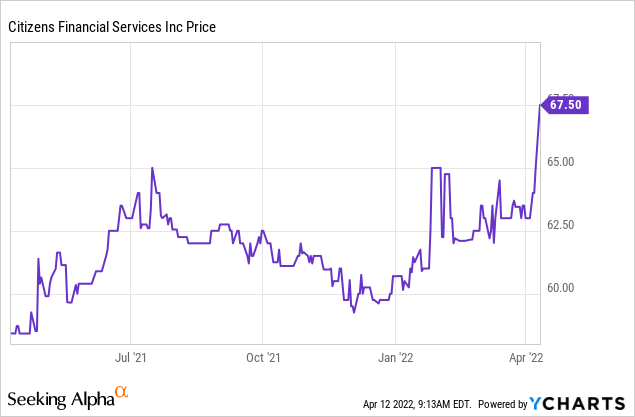

Some regional banks and community banks don’t get the attention they deserve simply because they’re listed on the OTC or pink sheets, which immediately makes them a “no go” zone for a lot of investors. In some cases, the banks make the (smart) decision to pursue an uplisting and that’s exactly what Citizens Financial Services (OTCPK:CZFS) is now pursuing. This small Pennsylvania-based bank has outgrown its pink sheets listing as its balance sheet size now exceeds $2B and is pursuing a Nasdaq listing. This should put the bank on a lot more radar screens and I wanted to see if I should go long before the uplisting actually happens.

A look back at the 2021 results shows very satisfying results

Citizens Financial Services is the holding company for the First Citizens Community Bank in Pennsylvania, where it operates about 30 branches with a specific focus on agricultural lending on top of the normal real estate loans and commercial loans.

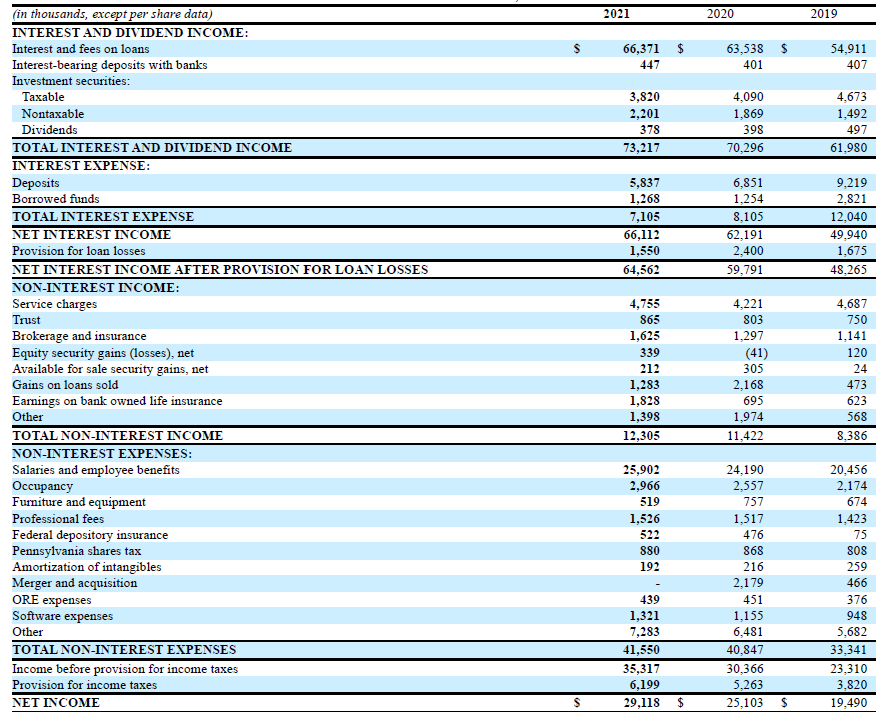

Thanks to the bank’s expanded asset base (the total size of the balance sheet increased from less than $1.9B as of the end of 2020 to in excess of $2.1B as of the end of 2021), the reported interest income also increased, from $70.3M in 2020 to $73.2M in 2021. And despite the expanded balance sheet, the interest expenses decreased, which further boosted the net interest income from $62.2M to $66.1M.

Citizens Financial Investor Relations

The bank also was able to report a stable net non-interest expense of approximately $29.2M, resulting in a pre-tax and pre-loan loss provision income of approximately $37M. We also see Citizens Financial Services recorded a provision of $1.55M for loan losses. That’s interesting for two reasons: First of all, despite recording a relatively low provision in 2020. And despite the increased balance sheet size, it’s very intriguing to see the loan loss provisions are now actually lower than in 2019, when the bank ended the year with a total balance sheet size of less than $1.5B. I will discuss the bank’s loan book in the next section of this article.

The bottom line shows a net income of just over $29.1M which represents $7.38 per share based on the average share count of 3.95 million shares throughout the year. The bank is currently paying a dividend of $0.47 per share on a quarterly basis and while this means the dividend yield is just under 3%, the dividend also is very safe as the payout ratio is just around 25% of the financial results.

The total amount of non-performing assets has decreased, and the majority is related to just three borrowers

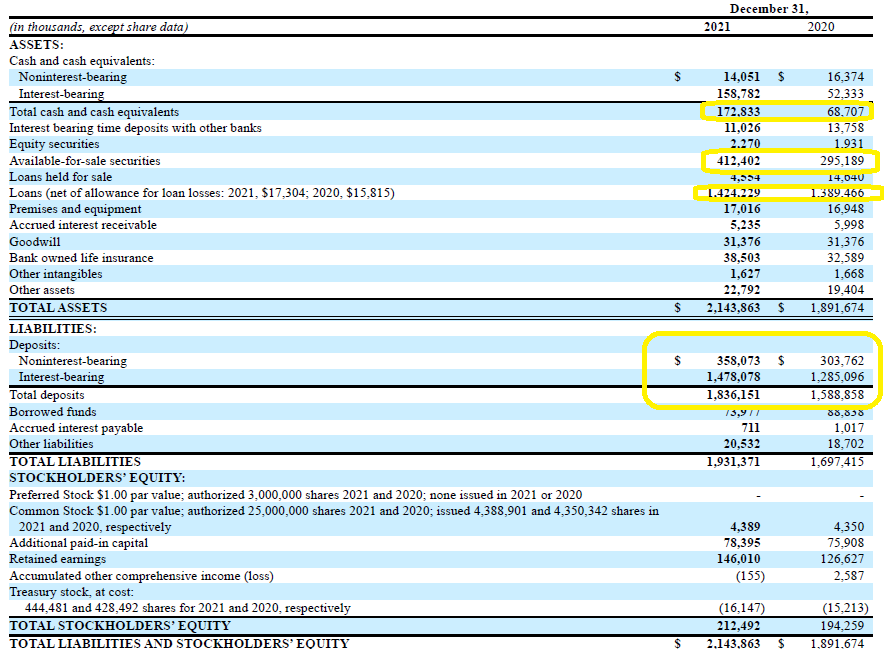

I like local and regional banks as I’d like to think they have a better understanding of the local markets and are able to service their customers (both on the deposit side as well as on the borrower’s side) better, with a personal service. It was very interesting to see the bank barely increased the size of its loan book in 2021 despite seeing an inflow of almost $250M in deposits. The vast majority of the cash inflow was either kept in cash or invested in securities. Those tend to be more liquid and thus safer, and this also made the balance sheet of the bank safer. As of the end of 2020, “only” 20% of the assets were held in cash or debt securities, but this increased to almost 28% as of the end of 2021.

Citizens Financial Investor Relations

That also explains why the interest income didn’t increase despite seeing a deposit inflow of hundreds of millions of dollars. Holding the inflow in cash and securities is safer, but that also means the interest income will be lower.

The image above shows the total size of the loan book increased from $1.39B to $1.42B, which is just a very small increase.

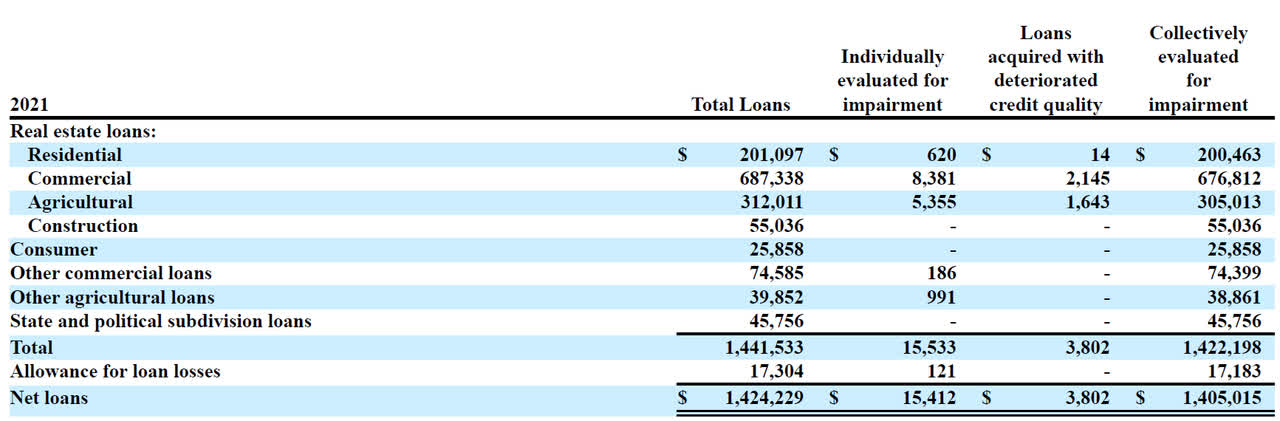

My next step is to always have a look at the breakdown of that loan book. The vast majority of the $1.42B consists of real estate related loans and commercial real estate plays a very important role. That being said, I also like the $201M in residential real estate and the in excess of $300M in agriculture-related real estate assets.

Citizens Financial Investor Relations

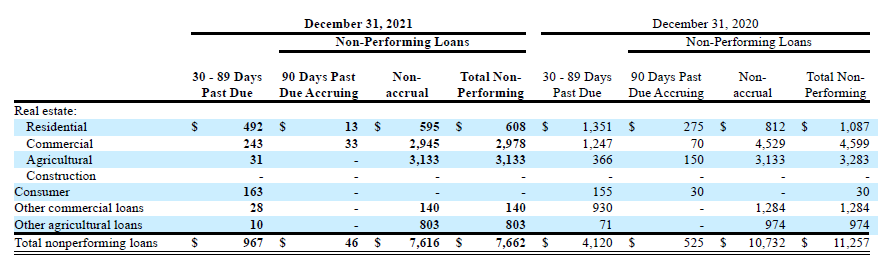

We also see the bank has already put $17.3M aside as a provision to cover loan losses which is an increase of about 10% compared to the previous financial year. Despite seeing a higher amount of provisions, the total amount of loans that are no longer classified as performing has actually decreased on a YoY basis. We see the total amount of non-performing loans decreased from $11.3M to $7.66M.

Citizens Financial Investor Relations

That’s good news for CZFS. Not just because the total amount of non-performing loans has decreased, but also because the increased provision now results in a much improved coverage ratio. As of the end of 2020, the total amount of provisions was $15.8M for $11.3M in non-performing loans for a coverage ratio of 140%. As of the end of 2021, the total provision increased to $17.3M while the total amount of non-performing loans dropped to $7.66M which increased the coverage ratio to 226% and that obviously is a much healthier situation to be in.

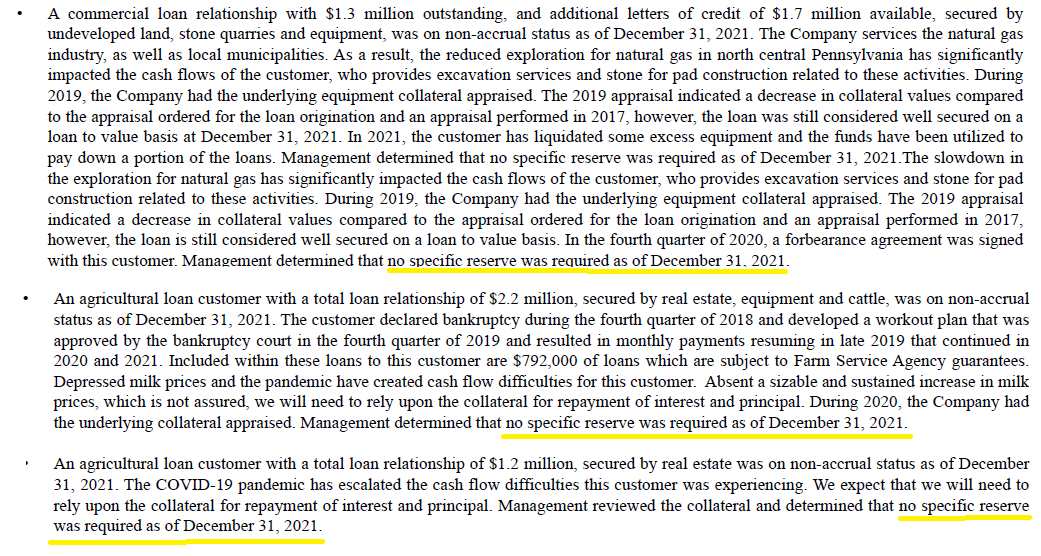

I also appreciate the color provided by CZFS on the non-performing loans as the majority of these loans (61.4%) appear to be caused by three borrowers, and CZFS confirmed in its annual report no specific reserves are needed for these three loans.

Citizens Financial Investor Relations

We should obviously continue to keep an eye on the credit quality as about $68M of the loan book is classified as “special mention” or “substandard.” While that’s a substantial decrease from the almost $75M as of the end of 2020, I would expect the bank to continue to record provisions in the foreseeable future to make sure it can continue with the potential fallout from additional loans going sour.

Investment thesis

Seeing loans go bad is part of the banking business and there’s not a single bank in the world that has never recorded a loan loss. So if there’s something you cannot avoid, it’s important to see how one deals with it and the strength of CZFS is keeping its loan book under control. I like the bank’s move to further beef up its position in cash and liquid assets and while the coverage ratio of the non-performing loans has improved, we need to keep in mind that about 5% of its non-residential mortgage loan book is classified as “special mention” or “substandard.”

I like CZFS for its financial performance and its rapid increase of the tangible book value thanks to the low payout ratio of the earnings. While the 2.8% dividend yield by itself isn’t something to get very excited about, the bank adds in excess of $5/share to its tangible book value which stood at $45.55 as of the end of 2021. The current P/TBV of 1.5 is relatively high, but considering the bank will likely end 2022 with a TBV of over $50, I don’t mind paying 1.35 times the year-end TBV for a bank trading at less than 10 times earnings.

I think CZFS will pop up on a lot more radar screens once the uplisting will be completed and I may be looking to initiate a small initial long position over the next few weeks while I get more familiar with the bank’s performance and wait to see it’s Q1 and H1 performance.

Be the first to comment