Ceri Breeze/iStock Editorial via Getty Images

Background

Citigroup Inc. (NYSE:C) (“Citi”) will release its Q4 2022 earnings on Jan 13 (pre-market), along with a few large banks, including JPMorgan Chase & Co. (JPM), Bank of America (BAC), and Wells Fargo & Company (WFC).

Bank earnings often have an overwhelming amount of information. I lay out 4 areas that I believe are most critical to help readers assess Citi’s results.

Net Interest Margin (NIM)

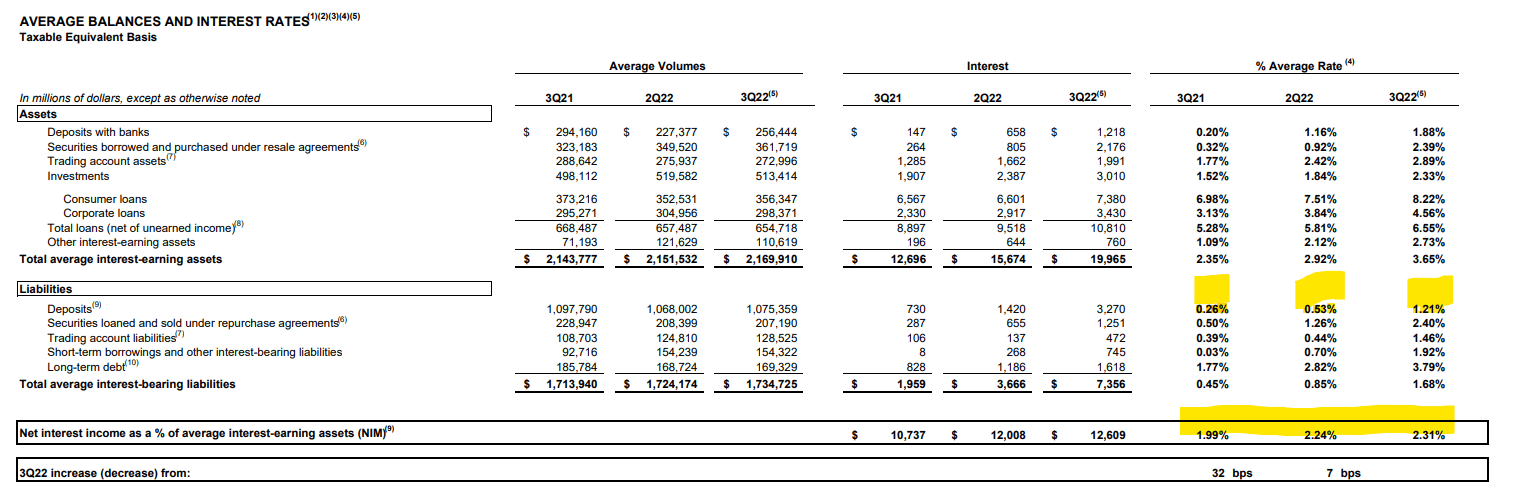

As a member of GSIB, Citi has over $1.7T interest-bearing liabilities (incl. ~$1T deposit), and 2.1T interest-earning assets (incl. ~650B consumer / corporate loans). Its Net Interest Margin was 2.31% in 3Q22.

3Q22 ER (NIM)

Why is NIM so important? Let me put some perspective into these big numbers. For Citi, every 10bps NIM improvement equates to ~$2.5B extra annual net interest income, which, by and large, goes straight to EBT.

If we use 6x MCap/EBT (a quite forgiving) valuation, everything else being equal, that equates to $6/share appreciation, ofc assuming it is somewhat sustainable interest income going forward.

The math is rough, but the point is a small change is a big deal here.

Now let us talk about deposit beta. Deposit beta, in its simplest term, means the amount of deposit interest that must go up in response to a rise in market rates. Thus, the lower the deposit beta, the more interest income that a bank can keep in its pocket.

Citi’s deposit rate has been increasing from 0.26% (3Q21) to 1.21%(3Q22), while the Fed effective rate increased from 0% to 2.3% during the same period. This is close to 50% deposit beta during that period.

if we look at the past history, as you might see from the table below, during the rate hike period, deposit beta for large banks (e.g. >$100B deposit base) ranges from 30% – 55%. Often, the faster the rate hike, the higher the deposit beta.

Deposit Beta (southstatecorrespondent.com)

It also makes intuitive sense. As rates increase rapidly, consumers will get more competitive offers from various banks and are more sensitive to bank interest rates.

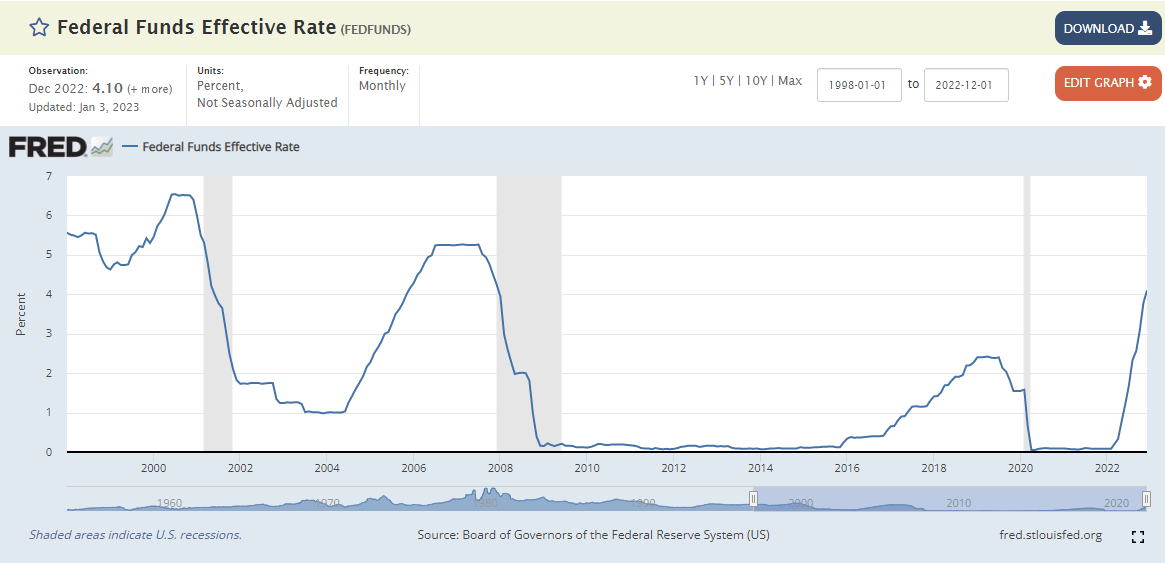

In 4Q22, the Fed effective rate continued to hike and reached 4.3% by the end of Y22. I model deposit beta at ~50%, thus projecting Citi’s avg deposit rate at 2.25% (+/- 0.25%)

FRED fed effective rate chart (1999-2022)

Certainly, a low deposit rate would indicate a sticky/strong customer relationship and a very positive signal.

One might be curious whether that means we will get a 100bps NIM bump in 4Q22? (200bps fed rate increase vs 100bps projected deposit rate increase)

That would be too good to be true. Let’s dive into that.

~1/3 of its assets (mostly its deposits with banks, and repo) would almost fully get the rate hike benefits.

~1/3 of its assets (mostly consumer and corporate loans), given the rapid speed of the rate hike, the loan portfolio would likely lag behind in its interest rate recalibration.

In summary, I would expect a 10-20bps increase in its NIM, which would be an extra $0.6-$1.2B net income interest for the quarter.

CET1 ratio

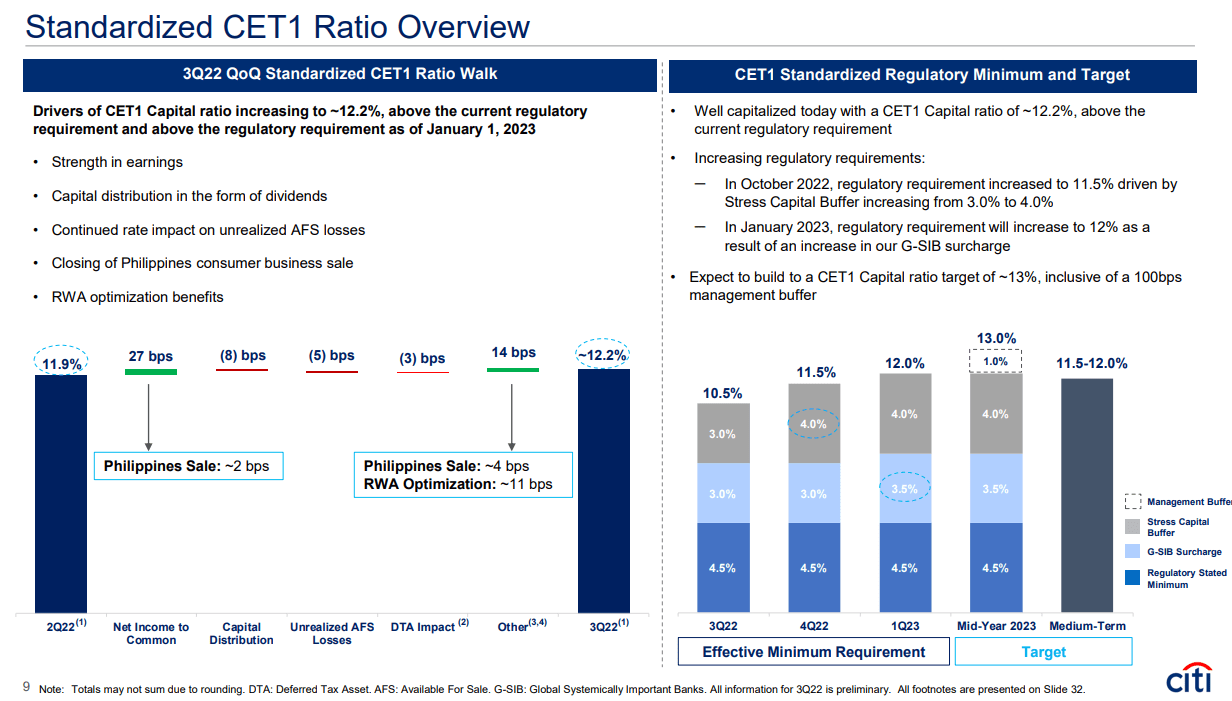

Citi ended 3Q22 at ~12.2% CET1 capital ratio.

As Citigroup’s SCB (stress capital buffer) increased to 4% (in 4Q22) after its 2022 CCAR test, and another 0.5% G-SIB surcharge increase in 1Q23, its regulatory minimum requirement would be 12% in 1Q23, plus its 1% management buffer guideline. The Street expects Citi to be in the capital accumulation stage for a while to meet its 13% CET1 ratio target.

That is certainly disappointing, as if you believe Citi is undervalued, then the most effective measure to narrow its price and value gap is via a share buyback.

Here are a few moving pieces to this story:

1. Divestiture: still has a few Asian countries and Mexico that should increase its capital (from sales proceeds) and RWA optimization.

2. Discussions about the necessity to maintain a 1% management buffer, the GSIB surcharge reduction lobbying efforts, and projected SCB re-evaluation (in June 2023).

Also bear in mind that its quarterly earnings increase by about 30bps in the CET1 ratio.

3Q22 ER (CET1 ratio)

Accelerated Growth Areas

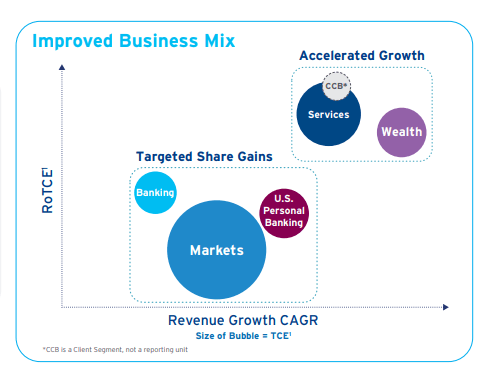

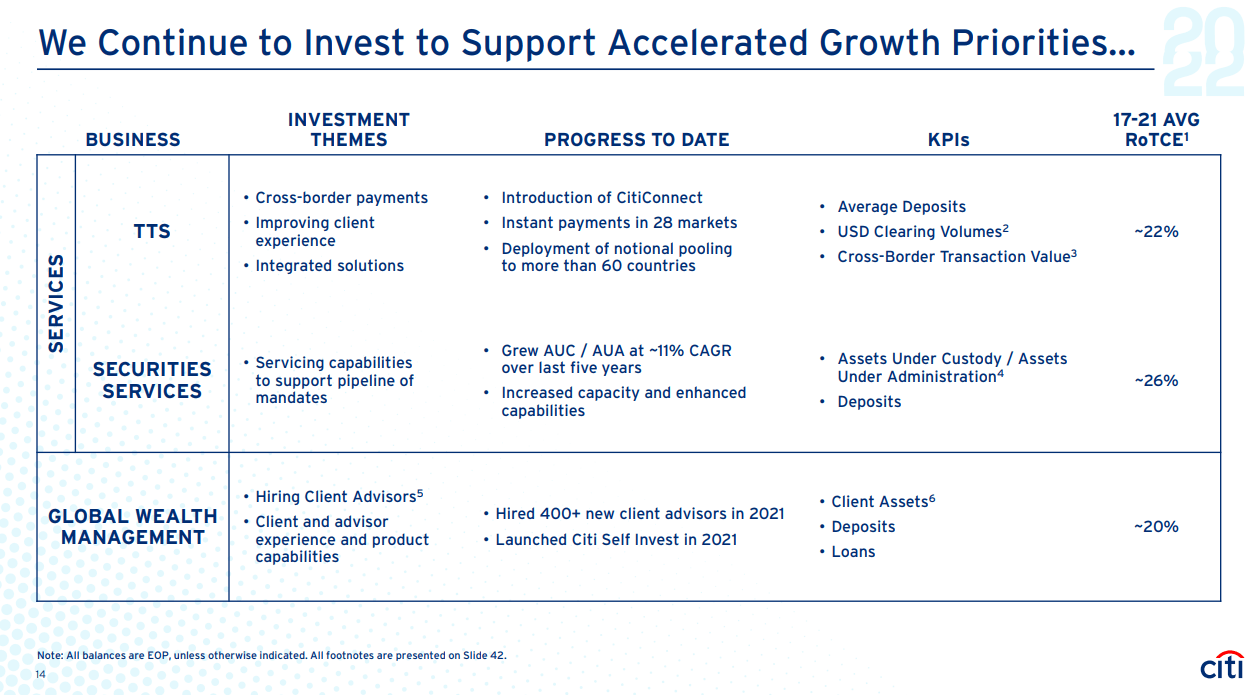

During Investor Day 2022, Citi categorized its businesses into 2 groups (see chart below) and stressed their focus on the high RoTCE and high revenue growth areas, such as TTS, securities services, and Global WM. The management stressed that the key contributing factor for Citi to improve its RoTCE from its current mid-8 % to medium-term 11-12% target is its ability to maintain a high single, low double-digit CAGR growth in these accelerated growth areas.

Investor Day 2022 (Growth Areas)

It also provided clear themes and most importantly relevant KPIs to keep track of its progress.

Investor Day 2022 (PPT)

I will pay extra attention to deposits in all 3 areas, and Assets (AUC/AUM) in securities services and Global WM business.

Note: TTS and Global WM are the primary low-cost deposit source, combined with ~75% of Citi’s total deposit.

NCL and Credit Reserve

Its NCL (Net Credit Loss) was ~$900M+/-50M/qtr for the last 5 quarters, while it released nearly $3B covid-related reserve till 2 quarters ago, then it started to build reserves at a ~$500M/qtr pace.

3Q22 ER (3Q22ER)

This accounting math could significantly change its headline numbers (e.g., EPS, Net income). Some have speculated that this could be the end of the CEO honeymoon period (nearly 2 years), thus it might be a tad more aggressive in credit reserve to set up a favorable foundation and easy comp next year.

I am not sure about that, but will keep it in mind, and compare its NCL and Credit Reserve to JPM and BAC tomorrow to identify any irregularities.

Valuation

Citi currently trades at ~0.6x TBV, with an adjusted RoTCE of ~8.2% (excluding divestiture/covid credit reserve release impact).

As a reference, JPM RoTCE ~15%, and valued at 1.8x P/TBV

My default, admittedly conservative, formula, is 10% RoTCE deserves a 1x PBV, then adjusted with premium/discount based on a bank’s moat, growth, loan quality, etc.

Citi, in my view, usually deserves a 10-15% discount, thus 0.6x TBV is slightly undervalued from a static lens today.

Now, from a dynamic lens, I like the changes made in the last 2 years since CEO Jane Fraser took over. She sold/is selling underperforming overseas retail branches, and has focused growth on high RoTCE business. That laid a solid foundation to achieve Citigroup’s 11-12% medium-term RoTCE target.

I think the progress made so far gives me reasonable hope that Citigroup has a good chance to hit or get close to 11% RoTCE in ~2Y, and these improvements might also justify removing the Citi discount (10-15%).

Thus, I see Citigroup Inc. being valued at 0.9x-1x TBV in 2 years, a 50% upside potential. Certainly, it gets to deliver what it promised.

Be the first to comment