VV Shots/iStock Editorial via Getty Images

Introduction

Citigroup (NYSE:C) does not need a long introduction as this US-based financial institution enjoys a worldwide brand recognition. Several Seeking Alpha authors have provided a look under the hood and the general consensus appears to be quite positive. Banks should benefit from increasing interest rates which should boost the net interest margins and net interest income, but it will be interesting to see how the weaker economy is impacting the loan loss provisions.

In this article, I will zoom in on the J-Series of the Citigroup preferred shares as these preferreds can be called later this year. And if they don’t get called, odds are Citigroup will have to pay an 8.5% dividend on these securities.

A look at the 9M 2022 results as starting point

Citigroup will report its FY 2022 earnings in a few weeks, but I decided to have a look at the Q3 2022 results to see how profitable the bank is. Profitability is an important element to determine how interesting a preferred security is. I prefer to look at the Q3 earnings instead of the 9M 2022 earnings for two specific reasons. First of all, the increasing interest rates are obviously more visible in the Q3 results than in the 9M 2022 results. Additionally, the bank recorded a $1.33B loan loss provision during the third quarter, which is more than 50% higher than the average reported loan loss provisions in the first half of this year.

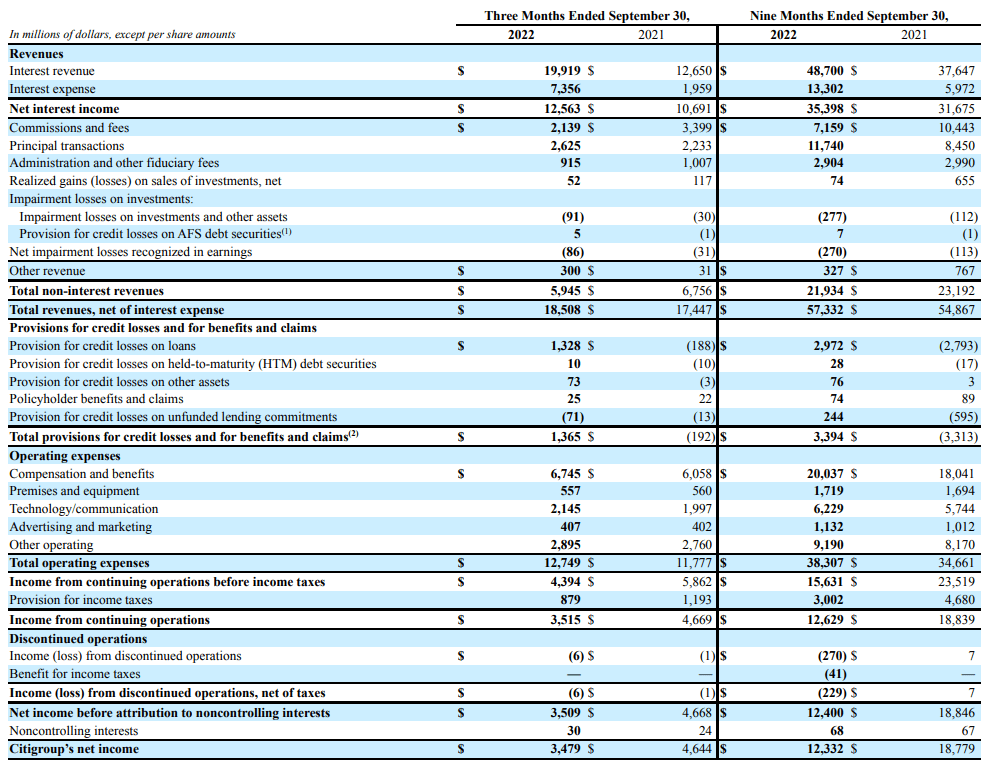

During the third quarter, Citigroup reported a net interest income of approximately $12.6B, an increase of in excess of 15% compared to the third quarter of last year. Although a sharply increasing net interest income usually is a good proxy for higher earnings, this wasn’t the case for Citigroup.

Citigroup Investor Relations

As you can see above, the strong increase in net loan loss provisions (a $1.37B provision vs. a $192M provision reversal in Q3 2021) and this caused the pre-tax income to drop from $5.86B to $4.4B. Despite this, the reported net income of $3.52B was still pretty strong and after deducting the losses related to discontinued operations and the $30M in income attributable to non-controlling interests, Citigroup’s bottom line shows a net income of $3.48B.

We know the bank paid about $277M in preferred dividends which means the preferred dividends are very well-covered despite the $1.3B+ in loan loss provisions recorded during the quarter.

The J-Series are an attractive Fix-to-Float security

I’m interested in Citigroup’s J-Series as this series of preferred shares offers a high base preferred dividend and even when the preferred dividend starts to float later this year, the preferred yield remains attractive.

Citigroup issued the J-Series, trading at (C.PJ) in 2013 and during the first ten years, the preferred dividend remained unchanged at US$1.78125 per year, for a preferred dividend yield of 7.125%. From September 2023 on, the preferred dividend will be variable based on the 3 month LIBOR plus 404 basis points. As the SOFR rate is replacing the traditional LIBOR interest rate and considering the current 3 month SOFR rate exceeds 4.5%, it’s starting to look that the preferred dividend may come in at 8.5% from September on. This would result in an annual preferred dividend of $2.125 per preferred share, payable in four equal quarterly payments of just over $0.53.

The main question now is whether or not Citigroup would be interested in paying 8.5% on a preferred equity security. Even though the bank can clearly afford it, it may result in a negative perception as some market participants may start to think that “if Citigroup is willing to pay 8.5% in preferred dividends, which is much higher than the 6% yields its peers are paying, something must be wrong.”

If the 3M SOFR rate doesn’t come down, I would actually expect Citigroup to call these securities which makes the yield to maturity calculation more interesting as it likely is the most realistic outcome.

The current preferred share price is $25.20 and we know there will be two preferred dividend payments totalling $0.89 before Citigroup can call the preferreds at $25, thereby generating a capital loss of $0.20 per preferred share. Despite this, the yield to call is approximately 5.48% and in absolute numbers, someone who buys the preferred shares now at $25.20 will receive a total of $25.89 by the end of June (assuming a timely call by Citigroup before it has to pay the floating rate preferred dividend from September on). That’s an absolute return of approximately 2.7%. It sounds pathetic, but it could be an option for an investor looking for a temporary home for its cash.

Investment thesis

I think it will be very interesting to see what Citigroup decides to do with the J-Series of its preferred shares. I think there’s a strong likelihood Citi will just call these securities to avoid the optics of having to pay a 8%-plus preferred dividend on its capital securities.

Of course, the situation can change quite drastically and dramatically if the 3M SOFR would suddenly come down but even with a 3 month SOFR at 3.25%, the preferred dividend yield would still be in line with the current dividend yield.

While a call is definitely not guaranteed and as there are other preferred shares with different qualities, this specific Citigroup preferred share could be an interesting option for investors speculating on a call within the next six months and who are willing to accept the risk the securities may remain outstanding.

Be the first to comment