bin kontan/iStock via Getty Images

After the close of Tuesday’s session, niche OTT content provider Cinedigm (NASDAQ:CIDM) reported Q3/FY2023 results well above analyst expectations.

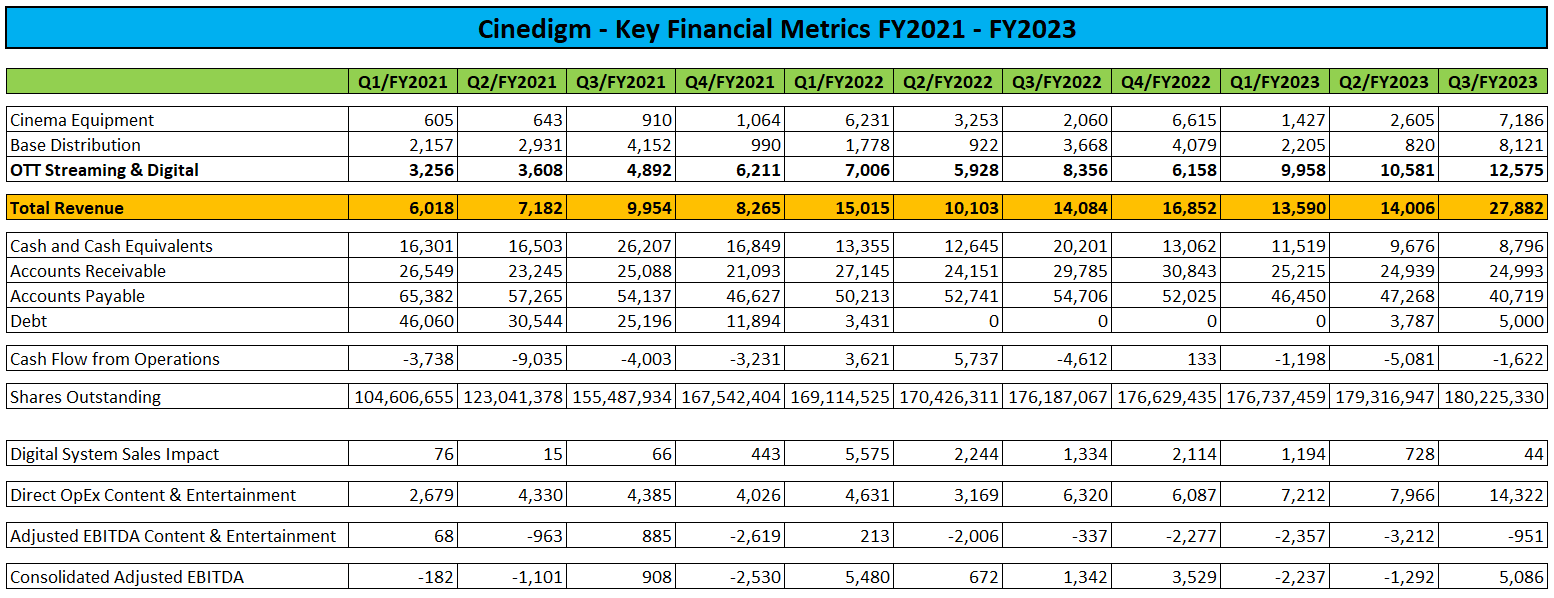

Total revenues of $27.9 million came in more than 40% above the two analyst consensus. In addition, Cinedigm reported positive earnings of $0.03 while the street was looking for a small loss.

Company Press Releases and SEC-Filings

But on closer scrutiny, the numbers look much less impressive as most of the outperformance was the result of a massive $7.4 million recognition of Virtual Print Fees (“VPF”) in the legacy cinema equipment segment while the core Content & Entertainment business which includes Cinedigm’s streaming and base distribution segments continued to operate at a loss:

Quarterly Report on Form 10-Q

That said, the recent box office success of low-budget slasher movie Terrifier 2 is clearly reflected in the strong revenue contribution from the Base Distribution segment which was up very significantly both sequentially and year-over-year:

Quarterly Report on Form 10-Q

In addition, streaming revenue was up a healthy 19% quarter-over-quarter to $12.6 million but the business continues to hemorrhage cash.

After giving effect to the $2 million minimum liquidity covenant governing the company’s fully drawn $5 million revolving credit facility with East West Bancorp (EWBC), available liquidity at the end of Q3/FY2023 was down to just $6.8 million.

In contrast to management’s claims on the conference call, the company will likely have to raise additional capital sooner rather than later.

The company also reiterated its long-term growth objectives:

- targeting at least 50% annual revenue growth in streaming

- growing annual revenue to $150 million through both organic and acquired revenue

- growing the content library to 75,000 titles

- attaining engagement of two billion Connected TV minutes

- growing podcast portfolio to more than 100 podcasts

Please note that the company will likely be required to conduct a reverse stock split until April 3 to regain compliance with the Nasdaq’s $1 minimum bid price requirement.

Bottom Line

Adjusted for the massive VPF top- and bottom line contribution, Cinedigm’s Q3/FY2023 financial performance was just slightly above expectations despite the much-touted success of Terrifier 2.

With available liquidity down to a paltry $6.8 million at the end of the quarter, the company will likely have to raise additional capital in the not-too-distant future.

Given mixed Q3/FY2023 results in combination with ongoing cash consumption and the likely requirement to conduct a reverse stock split until April 3, I am downgrading the company’s shares from “Speculative Buy” to “Sell“.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment