Zolnierek/iStock via Getty Images

Investment thesis

Church & Dwight (NYSE:CHD), in my opinion, is a company that has been successfully expanding its brand portfolio, making acquisitions that add value, etc. for many years. In spite of the challenges encountered in FY22, I am confident in the company’s ability to emerge from this period as an even more formidable business. I believe the company will be successful once we move past the current challenging macro environment and the negative aspects of this quarter’s results.

Results

CHD’s $0.62 EPS beat consensus estimate of $0.60, thanks to stronger organic sales growth and higher gross margin. Gross margin of 42% was pretty much in-line with consensus estimate, while organic sales came in better than expected. CHD consumer domestic segment drove the stronger organic sales growth, while the specialty products fell short. When looking at the bottom line, a rise in marketing and SG&A costs counteracted a rise in gross profit. As a result, EBIT was more or less the same as consensus estimates, while EPS increased thanks to a lower tax rate.

Demand trends

The trade down to value laundry detergent continues, and as a result, the U.S. business experienced growth in 13 of its 17 categories in 4Q22, leading to a record high market share. Additional brands that saw double-digit consumption growth and market share gains during the quarter include Zicam, TheraBreath, and Hero. ARM & HAMMER Clumping litter and Batiste dry shampoo both also reached record market share highs. However, a -4% headwind to organic sales was caused by the continued weakness in demand for CHD’s discretionary products and the vitamins business.

On discretionary product, management observed a downward trend in inventory. In the vitamin business, low fill rates caused volume losses as CHD had trouble keeping plants staffed, but things have since improved. That said, January continues to see a 10% drop in sales of vitamins, likely due to the category’s nature as a discretionary purchase and the challenging comparisons from the prior period with Omicron variant. It was also mentioned that spending on advertising has gone up. Since CHD volumes may come under pressure in 1Q23 in addition to pricing headwinds, I believe that promotional spend will be a key metric that investors pay attention to given it impact margins.

Qualitative highlights

For the initial half of FY23, I expect CHD to go through the pain of a tough comp consumers downtrade from premium brands. This effect should taper off as we enter 2H23. In my opinion, CHD reaps some benefits from consumers’ downtrading because the company’s product lineup features value products, especially in the categories of laundry, deodorant, and litter. However, I do not anticipate a speedy recovery in the more troubled segments (discretionary). Despite the “triple-pandemic,” management claims that sales of vitamins were down 10% in January due to the consumer’s newfound caution and the fact that vitamins are a non-essential category. Another indicator of the intensifying competition is the rise in advertising expenditures seen in many product categories.

Other than that, with product innovations being a big contributor to the top line, management mentioned that there is a series of innovative launches planned. “HardBall” appears to be the center of attention, as management declared it a “litter revolution” because of the product’s revolutionary potential in the category. Management also revealed plans to introduce additional product innovations in FY23, such as laundry detergent, condoms, acne patches, and dry shampoo. Given CHD history of innovation, I believe this new products will help in gaining share.

Thoughts on Hero acquisition

Management foresee rapid growth for Hero as it plans to target CVS pharmacies as distribution hubs across the country. With this goal set, I believe there are factors to consider, such as logistics, installation, and promotion are all extra expenses that should be factored in if CHD wants to enable national distribution. I’d like to bring up the fact that, while the Hero acquisition is expected to boost CHD’s top line, I think it also comes with some additional expenses, as evidenced by management’s guidance of other expenses of $110M for FY23, which is attributable to both the Hero acquisition and CHD’s debt.

Guidance

CHD announced an EPS guidance for FY23 in the range of $2.97 and $3.09. My interpretation of CHD’s EPS guide is that, despite spending more on advertising, the company will still post operating profit growth of 4-8%. Moreover, management expects a 2 to 4% increase in organic sales and a gross margin expansion of one hundred to one twenty basis points over the prior year. However, they foresee softer first-half volumes compared to last year due to continued weakness in its discretionary categories and higher pricing, followed by a return to volume growth in the second half.

For 1Q23, management guided lower-than-expected EPS of $0.75 vs. $0.79 (consensus) for 1Q23, while the 1% increase in organic sales was in line with expectations. More specifically, management expects continued softness in its discretionary brands to have a negative impact on revenue and profits in 1Q23. In my opinion, management is leaning on the side of caution for 1Q23 guidance, as is typical of their style.

Valuation

Model walkthrough:

- Revenue should continue to grow at mid-single digits level, similar to historical levels

- There should be no surprises to margin as well, as management has implicitly guided to 4 to 8% EBIT growth

- CHD currently trades around its average valuation over the past 10 years, as such I think it will be range bound within +/-1x range

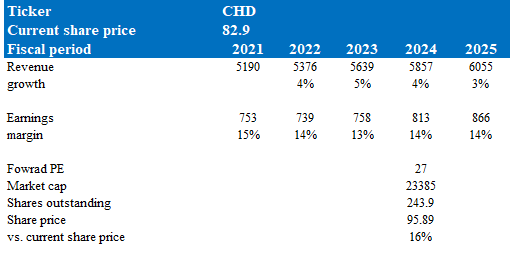

Own estimates

Conclusion

In conclusion, CHD is a well-established company that has been expanding its brand portfolio through innovations and acquisitions. Despite the challenges faced in FY22, I expect CHD to emerge as a stronger business. As for 4Q22, CHD showed a beat in EPS with stronger organic sales growth and a higher gross margin. The demand for CHD’s value brands, especially in laundry, deodorant, and litter, has increased due to consumers downtrading from premium brands. However, the discretionary products and vitamins segment may face a slowdown in demand. CHD guidance for FY23 is an EPS range of $2.97 to $3.09 with a 2-4% increase in organic sales and gross margin expansion. However, 1Q23 may face softer volumes due to weakness in discretionary brands and higher pricing.

Be the first to comment