Editor’s note: Seeking Alpha is proud to welcome Garuda Stocks as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

bwancho

Chipotle Mexican Grill (NYSE:CMG) released fourth-quarter earnings on Tuesday, Feb. 7. It missed guidance for only the second time in five years. In my opinion the stock is ripe for revaluation, and in this article I will present the argument for shorting Chipotle. I believe that its famous burrito might be more of a discretionary item than the market believes, and this article seeks to examine the viability of its expansion plans. Enjoy the grilling!

Overview

In investing, as in life, validation is essential. It is comforting that our views are shared. It gives our investment decisions authority. From a stock-picking perspective, three of the most powerful sources of validation are a rising share price, earnings per share growth, and beating Street estimates. This is a powerful cocktail of reassurance for the man on the street and a drink equally hard to resist for Wall Street.

That’s not without reason. Many successful momentum strategies have been devised on such metrics. However, we do know that successful investing is not a popularity contest. Investors are successful in the long run by having contrarian views to the market. In the short run the market is a voting machine, but in the long run it’s a weighing machine, as Warren Buffett said.

After last year’s market correction, safety in consensus has taken a beating. However, there are still stocks suspended in disbelief. As many of the market darlings fell to earth last year, Chipotle has been treading water. This price performance is particularly impressive considering that Chipotle is not just considered a growth stock, but also a “pandemic stock.” That is, its growth and its narrative were accelerated by the pandemic. Such stocks have in particular fallen back to earth. One only needs to look at the outdoor segment, examples being Thule (OTC:THLPF) and Clarus (CLAR); or big tech, examples being Google (GOOGL), Facebook (META), Apple (OTC:APPL) and Amazon (AMZN); or “stay at home” stocks, examples being Weber (WEBR), Peloton (PTON), DraftKings (DK), Netflix (NFLX), Zoom (ZM), and DoorDash (DASH) for evidence of this.

Chipotle, in this sense, is an outlier. Over the past five years the share price has compounded at 32% while earnings per share have grown at 38%. Revenue growth meanwhile has been around 14% over the same period, and restaurant growth only 10%. Even before its illustrious pandemic run, Chipotle beat earnings estimates for eight straight quarters. In fact, this quarter was only the second time in five years Chipotle has missed estimates. The stock trades at over 50 times its recently announced 2022 earnings and around 5.5 times expected sales. This in a market where frothy valuations are being cut down. So, what’s really going on here? Is its outlier valuation justified? The clues here, I believe, lie in the company’s history.

Background

Chipotle is the operator and owner of a fast casual restaurant chain serving burritos and other Mexican food. Its success and differentiation from other fast-food chains is that, in its own words, it serves fresh and wholesome food, without preservatives, that is prepared and cooked on site and sourced responsibly. Two of its trademarks are “responsibly raised” and “food with integrity.” Its mantra is high-quality fast food at a reasonable price.

In 2015/2016, Chipotle was a business on the brink, according to media reports. The company, which predominantly serves burritos made from its casual dining restaurants, suffered a number of compounding food scares. The result was declining sales and profit margins, and a significant revaluation downward.

Brian Niccol, previously of Taco Bell, led a turnaround strategy very successfully. The key pillar of his strategy, aside from an upheaval of hygiene and food safety processes, was to digitalize the business, growing ancillary revenues through pickup and takeaway orders. These now constitute just under 40% of sales in 2021. Of particular success was the Chipotlane, a drive-up window attached to conventional restaurants. According to the latest earnings release, 571 of Chipotle’s 3,187 restaurants have a Chipotlane. Additionally, like many others, the company partnered with third-party operators to offer delivery. Some of this delivery is through the third-party’s app, but much is also through Chipotle’s app. It is here that they have had much success with their reward program, as they have signed up 30 million customers and can offer targeted promotions.

The pandemic, with government support, afforded Chipotle a testing ground for the scaling of its new digital business. As a large restaurant chain with a resilient supply chain and delivery and pick-up infrastructure, Chipotle was extremely well positioned to benefit from the pandemic. And benefit it did. The pandemic significantly hastened its multichannel turnaround strategy. The aftermath of the pandemic was also a once-in-a-generation opportunity to pick up leases on the cheap.

Currently, Chipotle is firing on all cylinders. It had appeared perhaps that during the pandemic, its customers had simply moved from eating in its restaurants to ordering online. However, in fact, Chipotle managed to build a new customer base and, as restaurants reopened, it benefited from both its newly formed digital business and its returning conventional diners.

Chipotle appears to be a very healthy business with a strong track record. In fact, that’s why I believe it’s an interesting short – for the very reason of its success over the past five years. This is based on its extremely high valuation. At over 50 times earnings, the market is pricing Chipotle to deliver significant earnings growth, just as the economic climate in the U.S. is cooling. To justify its very high multiple, Chipotle will have to continue growing its earnings at very high rates. However, its restaurant margins are already around its previous peak margins before its food scares.

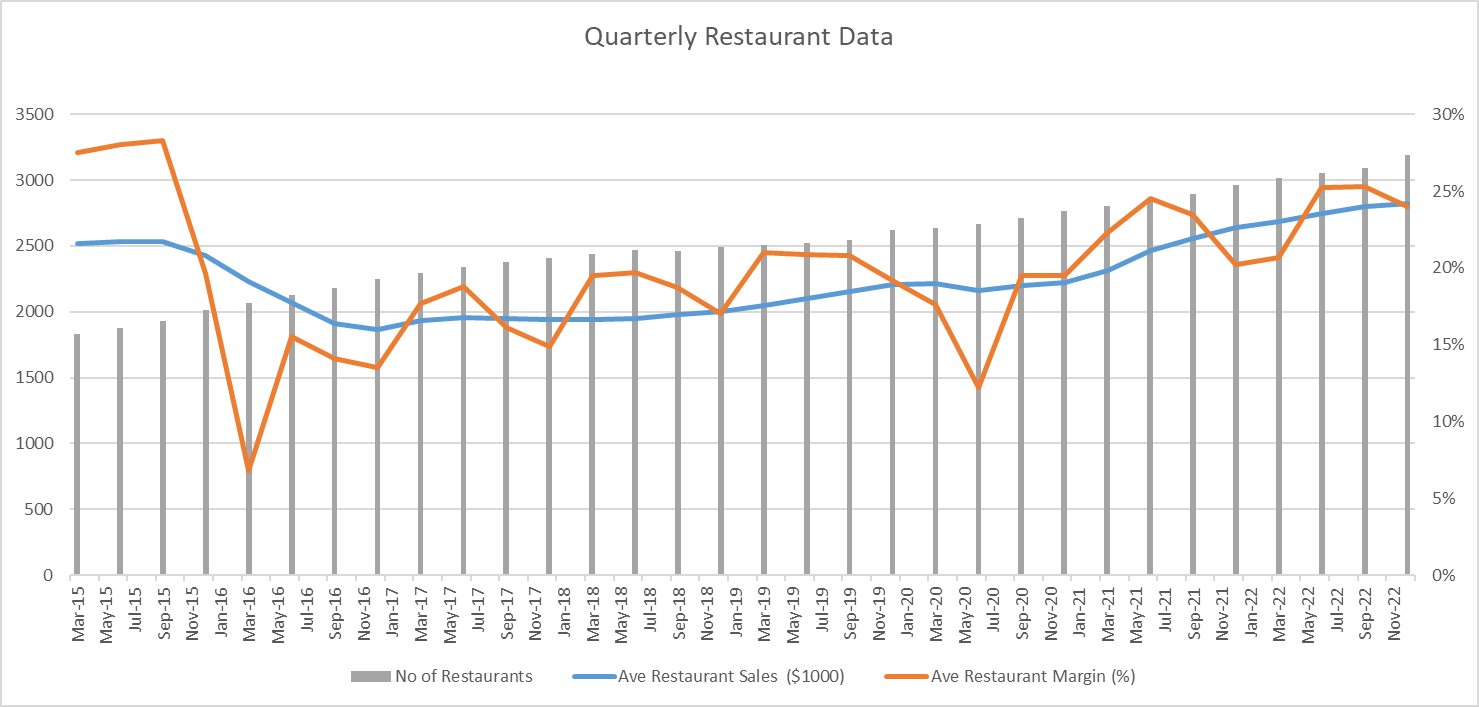

Quarterly Restaurant Data (Earnings Releases)

Can Chipotle Become More Profitable?

One force working against this valuation is inflation – in particular, food and wage inflation. Chipotle is at a relative disadvantage to other major fast-food companies in that it serves fresh ingredients. Avocados, taco shells, and beef – core ingredients in its menu – have, in particular, increased in price. In 2022, the company increased prices a whopping 13%. The year before that it increased prices 8%. This is in line with the company’s food inflation, which has been around 20% over that period. With a basic burrito now costing around $10, before expensive add-ons such as guacamole, the question is how much more pricing power does Chipotle have. A pillar of Chipotle’s strategy is good value, after all. There have also been “hidden” price increases; for example, menu prices for delivery are higher than in the restaurant. This does not include delivery, which is an additional expense. How much room is there for additional price increases?

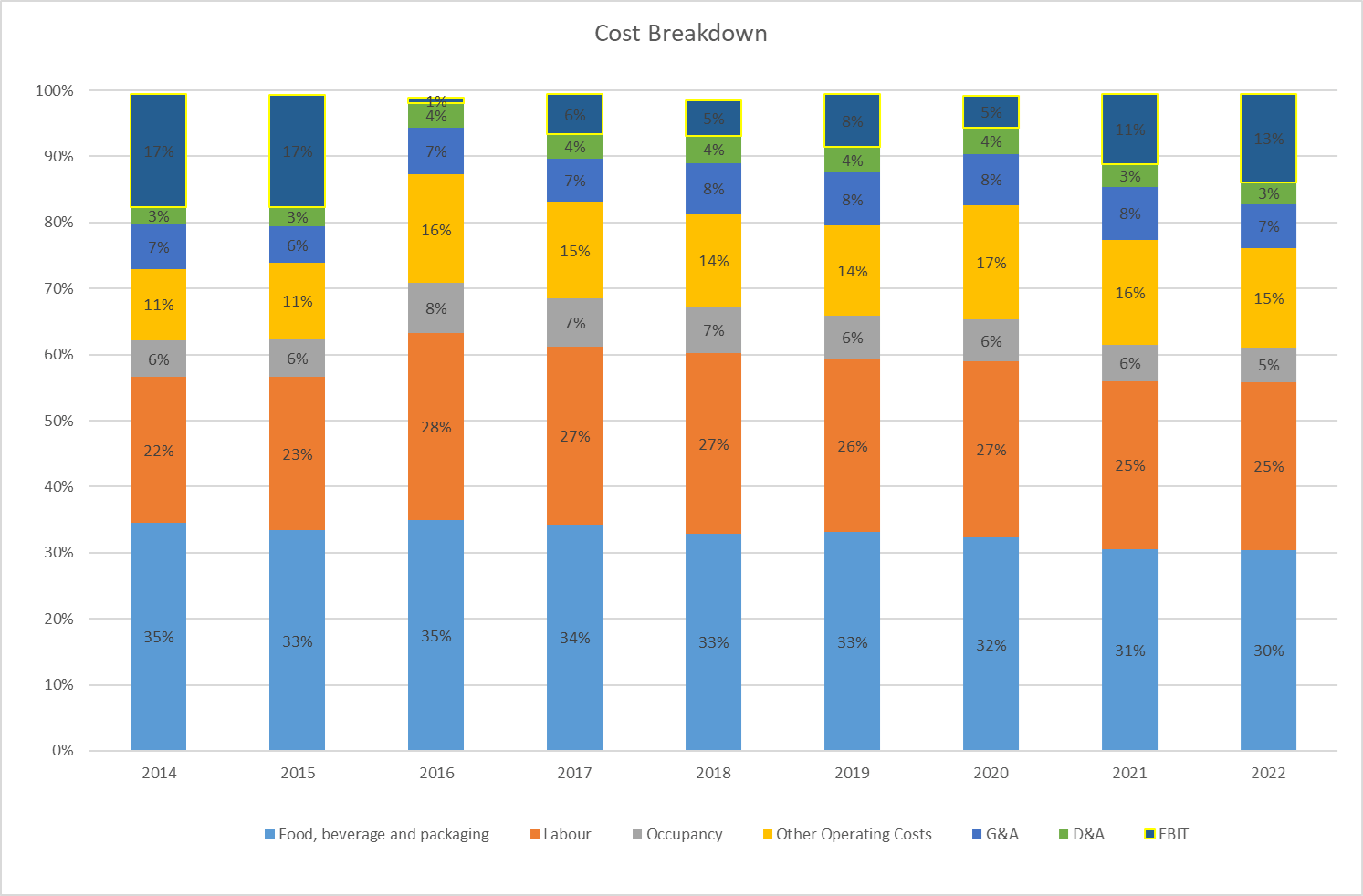

On top of food inflation, Chipotle is facing wage inflation, around 25% over the past two years. It raised average restaurant wages above $15 an hour in 2021. Recently, employees in different states have attempted unionization. Inflation is, of course, also present in its delivery channel. One thing Chipotle has in its favor, relative to independent competitors, is its ability to absorb food and wage inflation. This is because, like other large fast-food chains, staff and food costs are a lower percentage of sales than at independent restaurants. Occupancy costs are also only 6% of revenues.

Cost Breakdown (10K Filings)

Note: Other operating costs includes marketing and promos and delivery expenses paid to third-party apps. Around 3% of sales is spent on marketing.

Price increases have been a successful signaling technique the past year to show Wall Street that a company has pricing power. However, the jury is still out for Chipotle. Customers might be price inelastic in the short term because they might habitually consume Chipotle. They could be used to going there every Tuesday with work friends, for example, or picking up a burrito on their way back from the gym. The rewards program has also made customers stickier. Chipotle now has 32 million customers enrolled in its reward program. In the medium term, however, customers are price elastic as these habits can be broken down. In other words, there might be a time delay between price increases and a drop in demand.

In fact, there is already evidence of this drop in demand. Transactions at Chipotle declined in 2022 compared to the year previous in both the third and fourth quarters. Additionally, transaction values are declining with more customers eating at the restaurant post-pandemic and paying independently, as opposed to ordering as a group digitally. In the last-quarter results, comparable restaurant sales were up 5.6% while pricing was up 14%. What gives? On the last earnings call, management broke this down as a combination of transactions (-4%) and mix (-3%).

Revenue growth over the past few years has been coming from the digitalization of stores, Chipotlane additions, store growth, and price increases. Revenue per restaurant is back to an all-time high. Earnings per share is being driven by huge returns on investment associated with digitalization and Chipotlane additions. These have provided significant increases in revenue and profits for low cost. With almost all of their kitchens digitalized, how much additional low-hanging fruit exists to drive growth? As mentioned, Chipotle’s restaurant growth has only been around 10% per annum.

Can Chipotle Drive Growth Through New Restaurants?

To drive growth and justify its multiple, in my opinion, Chipotle will have to successfully open new stores. This strategy is now evident as management has increased the number of potential stores from 6,000 to 7,000. In addition, talk of business in Europe has crept into the discussion as per the last earnings call. This remains an area of speculative expansion. Regarding its intended expansion in the U.S., the return on investment will be lower than the digitalizations and conversions, especially considering the inflationary pressures on construction, staff hiring, and leases – not to mention bottlenecks in sourcing kitchen equipment. Additionally, competitors are catching on and the competition for appropriate drive-through sites is fierce.

Increasing the store count does not come without risk. The question is what is the appetite in the U.S. for more Chipotles, and at what point does the market become saturated. As Chipotle is larger than it was five years ago, to drive comparative growth the sheer number of stores must be much larger as well. 10% growth means upward of 300 new restaurants a year, as opposed to 200, five years ago. And this with a potentially cooling U.S. economy.

Perhaps investors believe that Chipotle will fare well in a recession. Certainly, management believes this to be the case as has consistently been discussed on its earnings calls. The logic is that Chipotle has largely higher-income customers (defined by management as having an income greater than $75K a year). These customers are believed to be less price sensitive. Management has also said that in a recession there will be a substitution effect. Those dining at full-scale restaurants will drift into eating at Chipotle, the fast casual alternative, giving it resilient sales.

The narrative that Chipotle is recession-proof might come from its resilience during the pandemic. But this was a very particular set of circumstances. Most notably, for customers, many of the alternative options to Chipotle simply weren’t available. Bolstered by free money, the consumer had an increase in disposable income with limited ways to spend it. The situation in an oncoming recession will be the exact opposite – a squeezed consumer (higher rates on mortgages and credit cards, and other debt and potential unemployment) with full choice. At the margin, Chipotle’s lower income customer might simply decide to cook at home to save money. The result is likely to be heavy discounting. There is perhaps already evidence of this discounting with Chipotle offering greater incentives to its rewards customers (an incentive called Freepotle by management).

More than 20% of Chipotle’s sales are now delivery (through their own or a third-party app; delivery is always executed by a third party), where its menu items are priced higher. Delivery, when taking higher menu prices and delivery costs into consideration, offers less value and is more discretionary. In the case of a recession there is likely to be a price war between restaurants on delivery apps. These “digital” restaurants have proliferated significantly. At the very least, in order to maintain sales, Chipotle would have to give up significant margin on these sales. Pick-up sales (from Chipotlanes) are also likely to be lower if a struggling consumer spends less time driving, particularly if gas prices rise. There is already, in my opinion, some evidence of a slowdown in the digital channel on the last earnings call. Delivery transactions are in fact down 15%. This is likely not just a substitution to eating at the restaurant, but also a tightening consumer.

Investor Strategy

So, how can investors take advantage of this opportunity? The obvious way is by shorting the stock. Buying put options also gives one exposure to price declines while limiting the downside.

Insurance on Chipotle is still cheap. Out-of-the-money put options for January, with an expiry of next year and a strike price of $1,000, trade at $15. If Chipotle’s share price were to half to around $850 by then, there would be a nine-to-one pay off. If the share price decreases two-thirds to $600, the payoff would be 25-to-one. Put options with an expiry of January next year with a strike price of $700 trade at $3.20. If the share price loses two-thirds to around $600, the payoff is 30-to-one. Put options for January 2025 expiry are more illiquid, but also attractive. Put options at a $700 strike price trade at $10. If Chipotle loses two-thirds, the payoff is nine-to-one.

The final point worth mentioning with out-of-the-money put options is Chipotle’s food scare history. This is something the company is hyperaware of – you only need to read the risk disclosures in the company’s 10-K filing. Because of its history with food scares, if another were to occur – which is out of Chipotle’s control – they can minimize the risk, but they can never eradicate it. As such, it could lead to irreparable reputational damage and a loss of customer faith and trust in the brand. This is something that doesn’t appear, in my opinion, priced in to the insurance market.

The risk with put options is that the thesis described above does not play out within the time frame of the option. In this case, the option will expire worthless. This could be because the U.S. economy proves more resilient or takes a greater amount of time to enter a recession. The key will be job losses and whether these transpire.

The solution to these problems is to directly short the stock. However, that brings in the risk of not having a limited downside to the trade. Additionally, as can be seen in the first handful of weeks this year, growth stocks have been on a tear. As there is a high correlation among such stocks (somewhat due to the large part played by ETFs in the market and the non-valuation buying and selling that accompanies this), share prices can remain irrational for longer than anticipated. Therefore, a continued return of the risk-on/speculative trade is a risk to shorting the stock – especially via put options, which have a specific time horizon.

Finally, if Chipotle was able to export its business model abroad or even develop a new restaurant franchise – both unlikely events in my view – that could justify its valuation. One final point to note is that this is a relatively illiquid stock, and management is buying back shares in the market.

Conclusion

If Chipotle is not able to increase its store count and maintain current profitability into a cooling U.S. economy, its multiple will have to contract dramatically. Certainly, I believe the 20%-plus growth being priced into the stock is overly optimistic. Five years ago, this was a business on the brink. It now has the highest market cap in the restaurant space besides McDonald’s (MCD). The reality of Chipotle is likely somewhere in between. Indeed, in my opinion, it’s possible that if it were to stop growing in a recession, its share price could easily lose two-thirds of its value.

In light of the above discussion, my suggestion is to short the stock directly and, additionally, purchase a number of different put options at different expiry dates and strike prices, preferably with longer durations. This eliminates the risk, to a certain extent, of being right but at the wrong time.

Be the first to comment