Justin Sullivan

A Tasty Investment

Chipotle Mexican Grill, Inc. (NYSE:CMG) reported Q4 2022 earnings yesterday after the market close. The company delivered slight misses in both revenue and profit. There were, however, tasty nuggets for investors within the report, and we believe that the next year outlook for the company remains bright.

By The Numbers

Despite the miss, growth was still on the menu at Chipotle. Year-over-year growth was 11%, with top line revenue coming in at $2.18 billion vs average analyst estimates of $2.21 billion.

The numbers under the top line painted a positive picture, however. Reported EBITDA came in at $376 million, a healthy 17% of earnings, while net profit was $223 million, providing a double-digit net margin of 10%.

Overall transactional volume was down for the quarter, which was somewhat expected given the softening macro environment and the reports from other retail operations this earnings season. Chipotle did raise its prices, however, in response to higher input costs of cheese and tortillas, while the price of avocados softened a bit.

Investors initial reactions have been to chafe at the news, with the stock down more than 5% as of this writing. However, we believe that any near-term pressure CMGI stock faces presents a buying opportunity for investors.

Life On The Margins

It’s no secret that Chipotle raised its prices during the quarter—management reported that prices were up about 13.5%. Investors and customers alike, however, should breathe easy that company leadership reported that they have no further plans at this time to raise prices.

While consumer-facing price increases often take up the majority of headlines, we want to point out that, under the hood, Chipotle seems to be firing on all cylinders.

For example, the fourth quarter results saw restaurant-lever operating margin at 24%, which is a 3.8% increase over the prior year. This margin bump in the face of rising labor costs (which were actually down year over year) presents, in our mind, a bit of solid evidence that management is sincere in saying that prices will remain stable in the near term.

Operating costs at the company level also decrease by about 60 basis points to 15.7%, and management guided to an operating margin of close to 15% in Q1.

In addition, Chipotle continues its rapid expansion. The company opened a record 100 stores in Q4, and it continues to project aggressive growth in 2023.

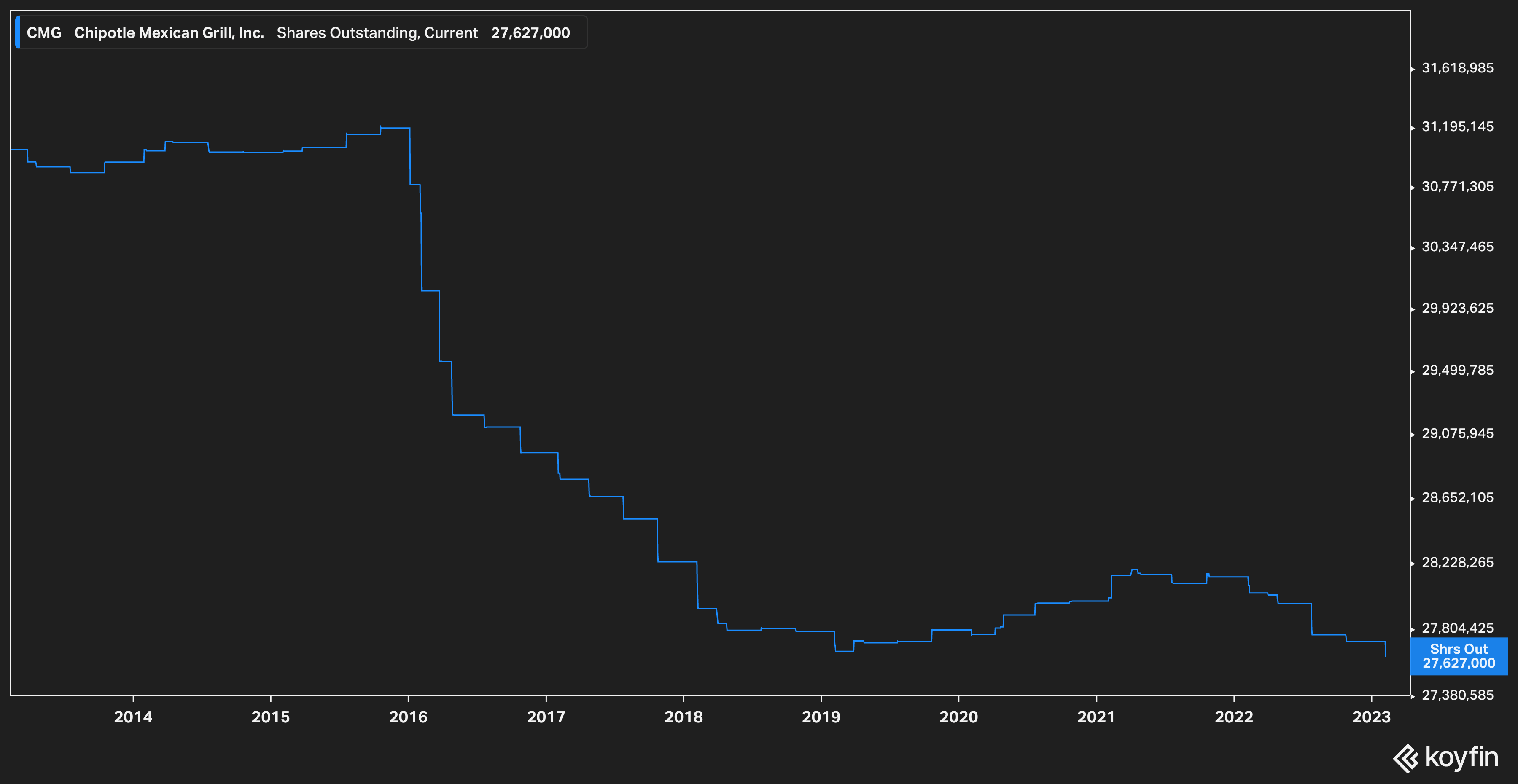

The company also contained its share repurchases, opportunistically buying back a total of $827 million worth of shares in 2022. The company has $414 million in authorized repurchases remaining. Needless to say, we are fans of this, and we point to management’s commitment on the buyback front by observing the company’s steadily falling shares outstanding.

CMG Share Count (Koyfin)

To us, this paints a picture of capable and competent management that can balance intense operating pressures and demands with growth and still deliver impressive results.

Relative Value

Critics of Chipotle argue that the stock isn’t cheap. Spoiler alert: they’re correct. However, we believe the premium is justified.

CMG NTM P/E (Koyfin)

Chipotle currently trades at 39x forward earnings, which sounds expensive until you consider that it’s on the lower end of its 5-year valuation, and well below the 5-year average NTM P/E of 54x (the 10-year average is 48x).

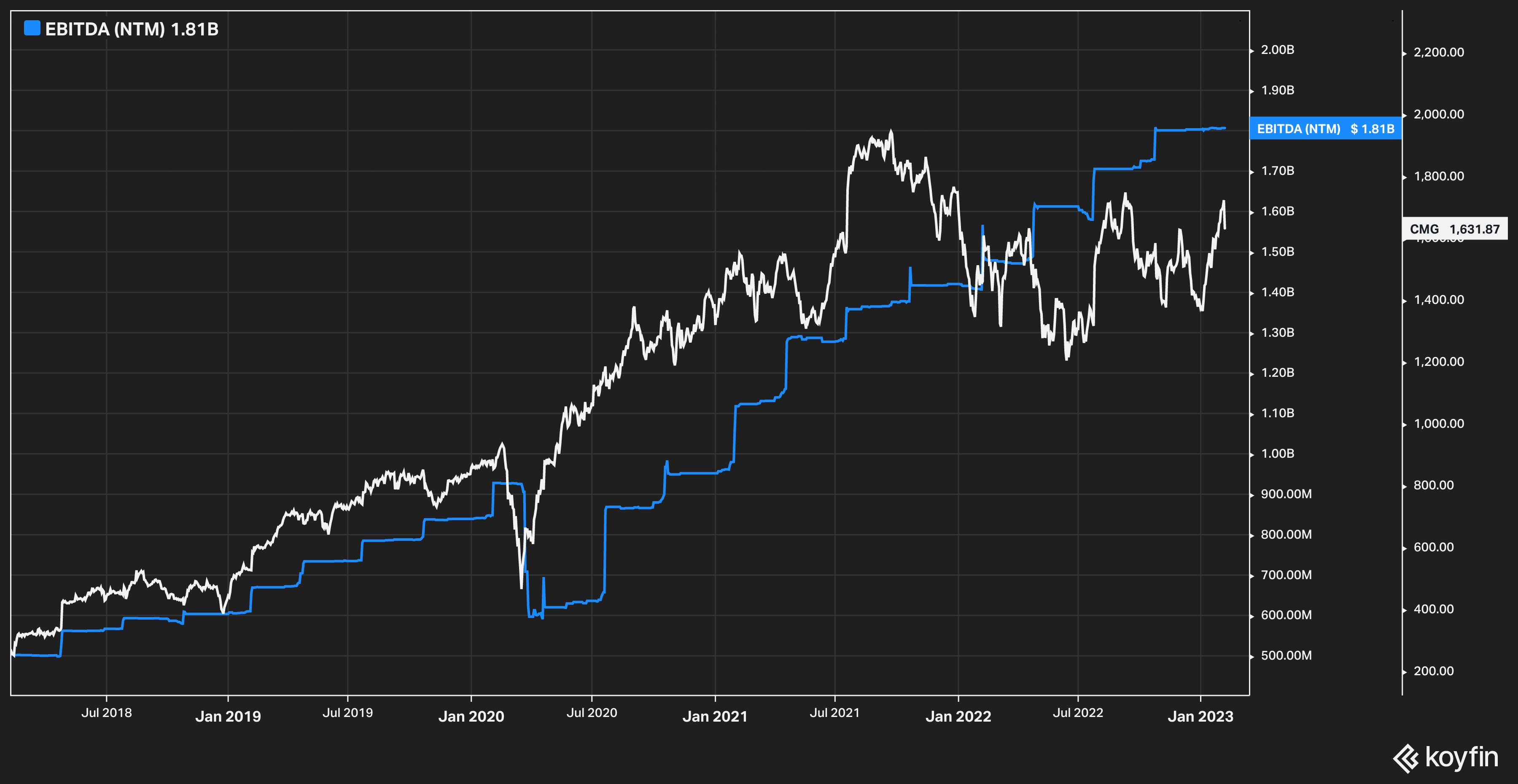

Further, Chipotle has historically traded at a slight premium when compared to EBITDA. In recent months, that relationship has broken down despite growth forecasts remaining healthy.

CMG Price vs EBITDA (Koyfin)

This discount, combined with the temporary macro headwinds the company faces, presents to us a buying opportunity.

For those still skeptical of the high Chipotle Mexican Grill, Inc. valuation, we understand. However, it isn’t based simply on good feelings and vibes—valuations are derived from an expectation of future returns, and Chipotle believes it can hit a long-term goal of 6,000 restaurants, double its current 3,000 locations.

The Bottom Line

Chipotle Mexican Grill, Inc. missed earnings in Q4, but we don’t believe this is indicative of the long-term health and prospects of the business.

Analysts apparently agree with our assessment of Chipotle Mexican Grill, Inc.. The morning after the earnings were announced, Raymond James, Wells Fargo, Baird, Truist, and Cowen raised prices targets on the stock.

We think investors should give serious consideration to making a tasty addition to their portfolio with Chipotle Mexican Grill, Inc.

Thank you for reading our article. If you enjoyed, it please consider following Ironside Research.

Be the first to comment