It is no secret that legendary tech investor Cathie Wood of ARK Invest (“ARK”) owns a big chunk of Roku, Inc. (NASDAQ:ROKU). In fact, it is reported to be her third largest holding, comprising 8.1% of the weight of her main fund, ARK Innovation ETF (ARKK). This article posits that another company, Chicken Soup for the Soul Entertainment, Inc. (NASDAQ:CSSE), is an even more attractive way to play the same sector.

First, let’s take a quick look at what these companies do. ROKU is the leading TV streaming platform in North America. While the company does offer hardware, its main business is its operating platform enabling TVs to be connected and the associated digital advertising and revenue share agreements with content streaming services associated therewith. We believe ROKU is undervalued at its current price, but that there may be a better way to play this sector for smaller investors as outlined below.

CSSE is a leading ad-supported streaming company that owns and operates a number of streaming apps including Crackle Plus, Popcornflix, and its eponymous Chicken Soup for the Soul. We believe this stock to be significantly undervalued for the reasons outlined in this article below.

Back to Cathie Wood and why she owns so much ROKU and why is she so bullish on the space in which it operates. Wood and her analysts, who are known for their deep and original research, have determined that Advertising Video on Demand, or AVOD, is an extremely attractive sector of the media industry with significant growth ahead.

First, what is AVOD and why is it well positioned for growth? Advertising video-on-demand entertainment platforms are, importantly, free to consumers because they are funded by advertisers (much as has been the case with traditional television for decades). While the Subscription VOD companies, like Netflix (NFLX) and Disney+ (DIS) have gotten most of the investor attention over the past several years, these companies have started to play in an ever more crowded space and one in which the consumer tolerance for subscription fees has started to wane. This shift from paid streaming to AVOD is expected to accelerate as the economy slows and consumers look for ways to trim expenses.

ARK’s Analysis On $ROKU:

ARK has conducted extensive research on the AVOD sector in generally and on ROKU in particular.

ARK’s base case projection results in an increase in ROKU’s share price of nearly 700%, while the Bull Case results in an increase of over 1600%. These are shockingly high numbers, and they boil down to just how bullish these analysts are on the AVOD sector.

” we believe video advertising revenue is likely to be the most significant contributor to the company’s growth during the next five years.”

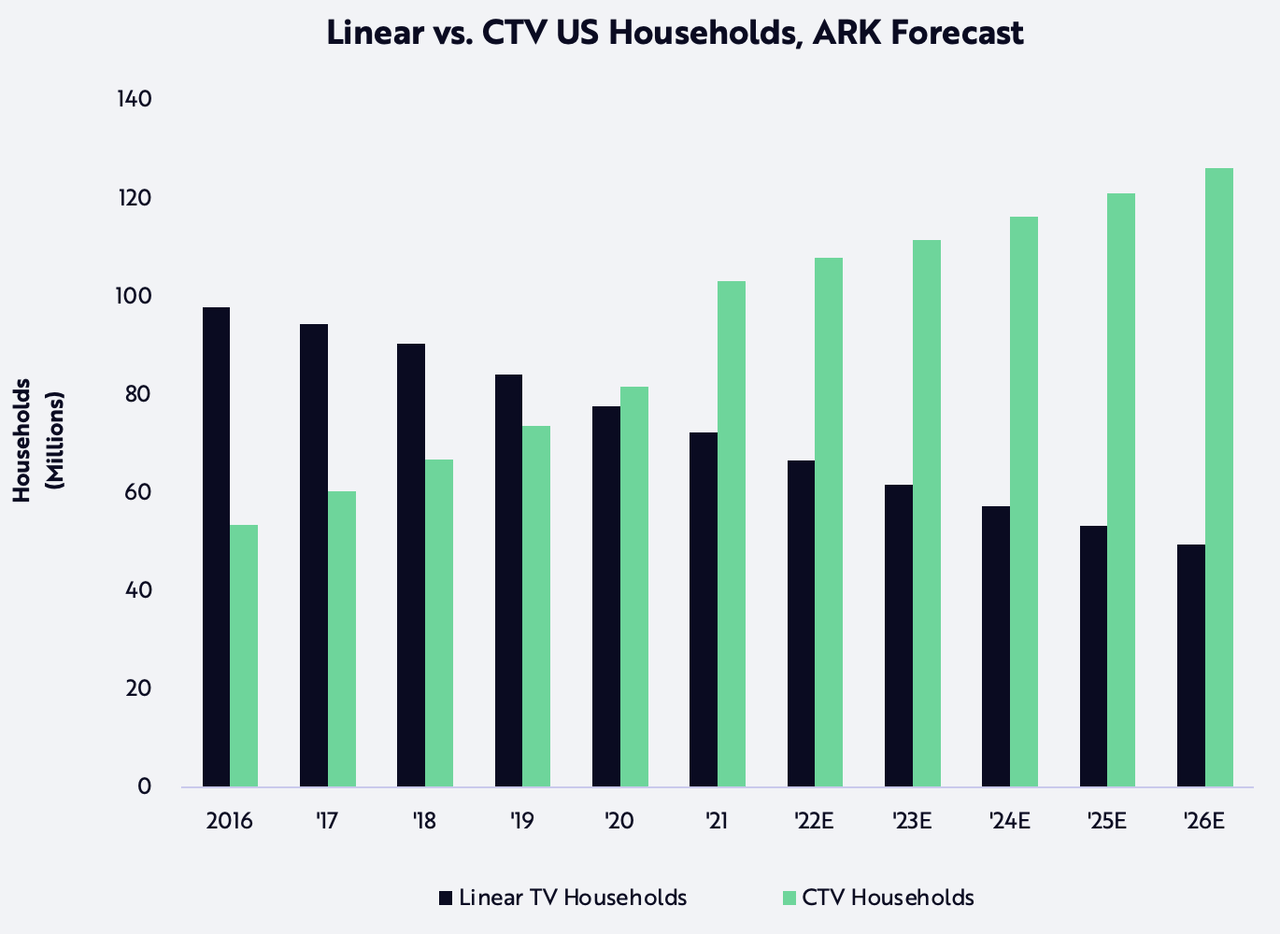

“… we detail the decline of linear TV relative to the rise in CTVs [connected TV’s] in the US, as shown below.

From the ARK report (ARK Investment Management LLC)

ARK Investment Management LLC, 2022; S&P Global Market Intelligence; US Census Bureau.

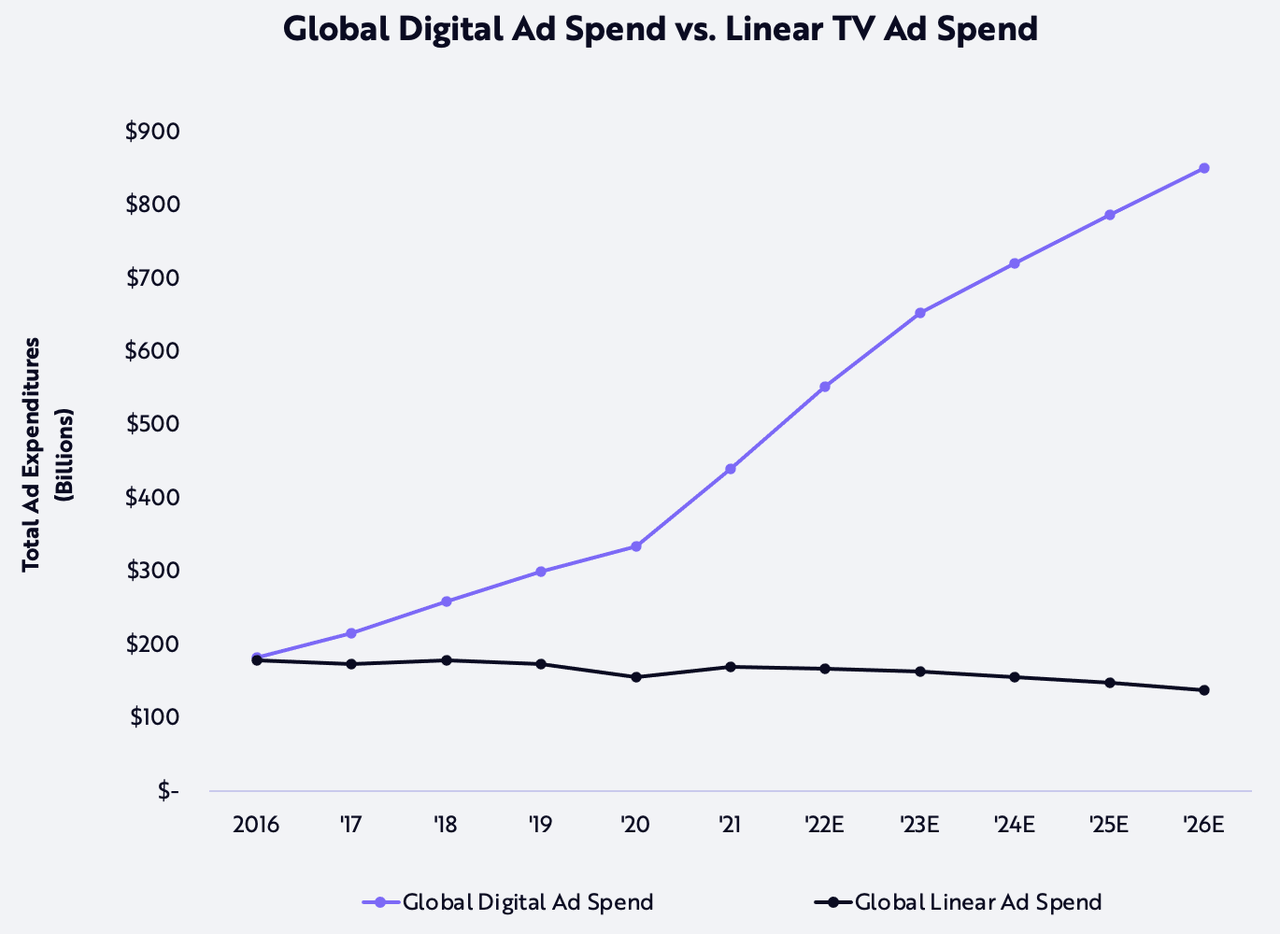

From the ARK report (continued):

“Advertising’s shift from linear to digital TV has lagged the consumer’s shift. In Roku’s first quarter earnings call, CEO Anthony Wood reiterated that US audiences spend 46% of their TV time on streaming while advertisers spend only 18% of their TV ad budgets on streaming.[21] Our research suggests that the decline in global linear TV ad spend has just begun: during the last five years, it has declined only 1% at a compound annual rate, from $178 billion in 2016 to $169 billion in 2021, while digital ad spend has increased 19% at a compound annual rate from $182 billion to $439 billion. According to ARK’s research, global linear TV ad spend will shrink 4% at an annual rate during the next five years, from $169 billion to $138 billion, while total digital ad spend grows 14% at an annual rate from $439 billion to $850 billion, as shown below.

ARK Investment Management LLC, 2022; S&P Global Market Intelligence.

From the ARK report (ARK Investment Management LLC 2022)

ARK’s analysis above is quite compelling for the AVOD vertical. It may be instructive, therefore, to look for what other companies are in that same sector to determine if these, too, might be in a position to experience substantial upwards moves in the future. One such company is Chicken Soup for the Soul Entertainment. Despite the rather clunky name, the company is better known for Crackle, the AVOD platform it owns, as well as its upcoming acquisition of Redbox Entertainment (RDBX).

The AVOD sector that ARK is so bullish on is at the core of CSSE’s operations. With its well-known Crackle/Crackle + video streaming platform and its soon to be acquired Redbox Digital, CSSE has a substantial and growing presence in the AVOD ecosystem. Even prior to the Redbox addition, Crackle currently has more than 40 million monthly active users.

Valuation Comparison

From a valuation standpoint, CSSE looks attractive relative to ROKU. Specifically, TTM revenue for Roku was $2.924 BN and it currently has an enterprise value of approximately $12.4BN for an EV to Sales ratio of about 4.24x.

CSSE’s TTM revenue was $116 MM and it currently has an enterprise value of approximately $180MM for an EV to sales ratio of about 1.55x.

CSSE would have to appreciate by 274% just to be at an equivalent EV to Sales ratio as ROKU is currently. Such an appreciation wouldimply a current price for CSSE of $22.41, which is still less than half of its 52-week high.

ARK’s bull case for ROKU implies a share price by 2026 of $1493 per share. A similar appreciation in the share price of CSSE would imply a price of $140. Even just half of the appreciation expected for ROKU’s bull case would put CSSE at a share price of around $70, which is an 8-fold increase from current levels.

One might wonder why ARK wouldn’t have invested in CSSE if it’s so much more attractive from a comparative valuations basis. The answer is simply that they are too big relative to CSSE’s market cap to put enough money to work given the size of their multi-billion dollar funds. This is where smaller, individual investors actually have an advantage over the large funds to acquire higher value assets for lower prices.

Tiny Float

Additionally, while both companies offer a compelling opportunity to participate in the growth of the AVOD sector, the technical aspects of CSSE actually make it a far more attractive investment than ROKU. Specifically, CSSE has a float of only 6.3 million shares compared to 118 million shares for ROKU.

Meanwhile, CSSE has a 35% short interest vs. only 5.18% for ROKU, so the potential for a short squeeze for CSSE is significant, particularly if the market re-rates stocks in the AVOD sector as we believe is likely.

From a technical standpoint, CSSE shares would seem to have a quicker and easier time rapidly increasing in value relative to ROKU (which we still think is attractive at current levels). Specifically, CSSE’s stock chart shows its 10-day moving average having crossed over its 50-day moving average, which is not the case with ROKU.

In summary, CSSE finds itself in an attractive growth sector with an underappreciated valuation and a compelling technical setup. We think the risk-reward for this stock is among the best in the sector and the share price increase could be rapid given the tiny float. That said, if shares increase to over $60 we would recommend scaling down position size accordingly.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment