grandriver

Investment thesis: Chesapeake (NASDAQ:CHK) was thought of externally, as well as internally as a major shale player that got the short end of the shale acreage lottery in the last decade. Chesapeake used to proudly highlight the growing percentage of liquids production, as well as any liquid-rich acreage acquisitions as a way to try to assure investors of its viability. As we know, it did not help, because it did enter bankruptcy. The odds of success following its re-emergence are greatly bolstered by the global natural gas market situation, with Russia taking a very significant cut in natural gas exports, even as the US has been ramping up its net exporter status with growing LNG shipments. The latest news in this regard is very bullish for US natural gas producers. At the same time, mild weather in the Northern Hemisphere this winter is causing some temporary softness in US natural gas prices, making for a decent opportunity to buy Chesapeake stock on long-term fundamentals this quarter.

Chesapeake is showing strong financial results and has decent natural gas acreage, which can pay off for the foreseeable future, given current market prices

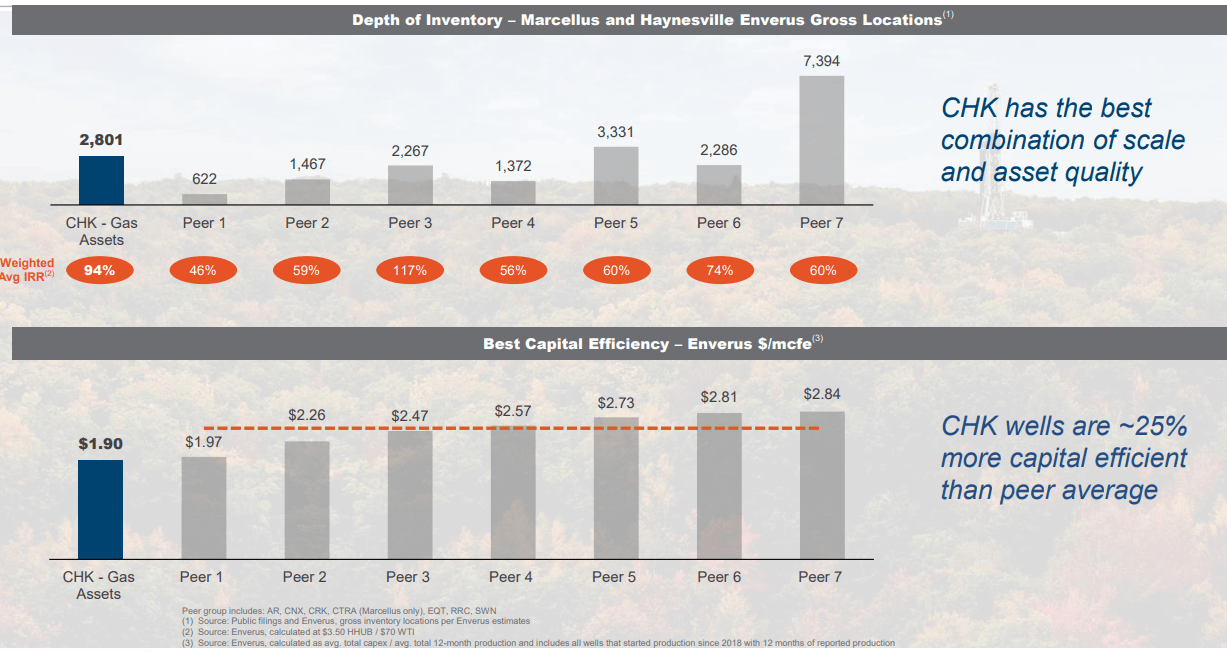

While its gas acreage was under-rated last decade, it turns out that Chesapeake has some decent drilling prospects in its acreage portfolio, as judged based on current natural gas market prices.

Chesapeake

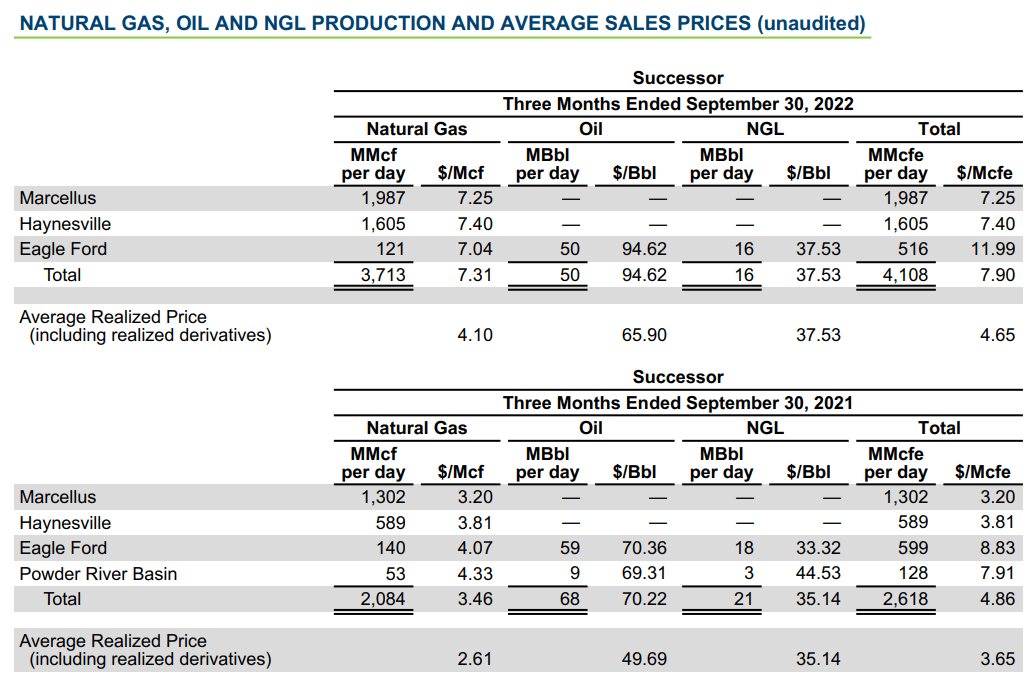

With ample and profitable reserves, on top of a decent natural gas price environment, Chesapeake has been putting in some solid quarterly financial results. For the latest quarter, it produced revenues of $3.16 billion, with a net income of $883 million, for a profit margin of almost 28%. It is a very significant leap from the same quarter from the previous year, when it lost $345 million, on revenues of $890 million. A major aspect of the massive leap is the significantly higher price of natural gas, which is extremely important for Chesapeake since its production is currently overwhelmingly natural gas.

Chesapeake

As we can see, the massive increase in natural gas prices, even with the effect of derivatives dampening the full effect on its average realized price has had a significant effect on its financial results. We should keep in mind that the longer the higher-price market environment for natural gas prices, the less likely it will be that future hedging will be done at price levels we have seen in previous years. In other words, we should see improvement in the realized price in coming quarters, even if natural gas prices will continue to hover around recent averages.

The case of the missing 100 Bcm/year Russian gas from the global market

A few years back, Russia set a record in exports at around 200 Bcm/year (6.4 Trillion cubic feet.) As of November 15 of last year, it exported 93 Bcm, meaning that for 2022 it probably exported no more than around 100 Bcm. All indications are that 2023 will be much of the same. Russia has the capacity to export about 35 Bcm to 40 Bcm via LNG. There is about 50 Bcm capacity to send towards Turkey via the Turkstream and Bluestream pipelines. There is also the growing flow of gas to China through the Power of Siberia pipeline. Russia may once more reach 200 Bcm in natural gas exports by around 2030, mostly on the back of growing LNG capacity, as well as a new proposed pipeline to China, which might reach a capacity as high as 50 Bcm/year if or when it will be completed. Russia is also likely to expand its own petrochemical exports, thus it may indirectly displace some global demand from elsewhere in that way. In the meantime, there is a gaping hole in global supply, which US LNG exports will partially try to fill for the foreseeable future.

The investment case in favor of Chesapeake within the global geopolitical context

For the context of just how much of an impact the missing cubic meters of gas from Russia are set to have on the market in the next few years, the decline in exports is almost equivalent to Norway’s production, which ranks as the 7th largest producer globally. The inevitable net effect of this reduction in Russian exports will be many years of high natural gas prices in the Europe-Asia region. Just a few years ago, this would have had very little impact on America’s mostly regional gas market. Years of LNG export capacity expansion have changed all that. American LNG now rivals Qatar for the top exporter crown.

America also gained a more or less permanent dependent client for that LNG, given that Russian natural gas will probably never flow again to the EU in anything but minute volumes through some LNG and Turkstream. A lesser-known long-term problem for the EU and the UK is that Norway, which exports about 100 Bcm/year of natural gas, with all of it headed for the UK and the EU can potentially see a peak and then a permanent decline in production at any point in the next few years. Despite a forecast increase in Norwegian oil production this year, natural gas production is forecast to decline by 1%. It could be just a blip, or this year could mark the beginning of Norway’s natural gas production decline, given that it now has many very mature producing fields.

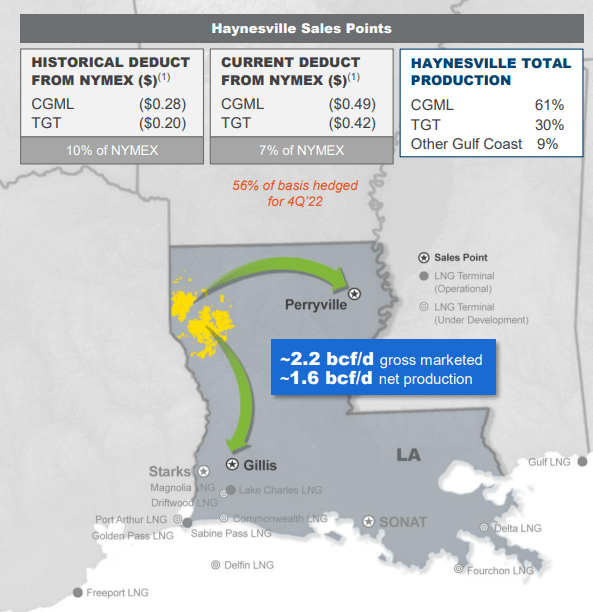

All indications are that American natural gas will have to play a prominent, constant role in supplying Europe from now on, just to keep the continent from plunging. There will be better times for the embattled EU economy, like now when a very warm winter relieved the pressure on supplies. There will also be winters when more natural gas imports will be solicited. Sometimes it will be more than American suppliers will be able to provide. The net effect is a new price floor for American natural gas, which pretty much ensures that Chesapeake will succeed and thrive this second time around, thanks to the same resources that drove it to failure last decade. It has the resources to do so. It is strategically located, with its Louisiana production at its Haynesville field operations being directly affected by the LNG trade.

Chesapeake

A number of projects are on the way, which will turn the Louisiana coast into a major LNG export hub. Chesapeake’s prominent position in Haynesville is particularly valuable, given the overall big picture. The price outlook for the Marcellus area may be less uncertain, but indirectly, higher prices along the Gulf Coast should also help the natural gas price there. Overall, Chesapeake is increasingly looking like a good long-term investment bet, with major factors lining up in its favor.

Some words of caution in regard to the shorter-term outlook, we also have to take the possibility of a prolonged global economic slowdown into account, as well as weather factors that may cause a period of low natural gas prices. There are also longer-term issues to consider, mostly general to most shale producers. Prime acreage availability may become an issue, raising the possibility of higher production prices going forward, and even production decline. At the same time, there seems to be upward pressure on drilling services costs, which can cut into profitability. For these reasons, I prefer to see the stock price drop close to $80/share or even lower before I consider buying. I do see such an investment opportunity potentially arising this quarter.

Be the first to comment