CHUNYIP WONG

Introduction

I have covered energy giant Cheniere Energy (NYSE:LNG) several times in energy-focused articles. However, I’ve never solely focused on Cheniere Energy, which I will do in this article. I found at least three good reasons to write this article.

- Cheniere Energy shares have dipped for the first time since early 2022.

- The decline is caused by pricing and demand headwinds from Europe.

- Long-term fundamentals remain terrific.

While some of this is bearish, the bigger picture remains incredibly bullish. Hence, I’m starting this article by explaining why I expect natural gas and LNG prices to rebound again. After that, I will tell you why Cheniere is one of the best no-nonsense investments for long-term (dividend?) investors.

So, let’s get to it!

Side note: I usually use tickers to refer to companies. I won’t do that in this article. At least not when it comes to Cheniere. After all, its ticker is LNG, which is the abbreviation of Liquid Natural Gas, which we will discuss in this article, as well.

The LNG Bull Case Is Paused, Not Dead

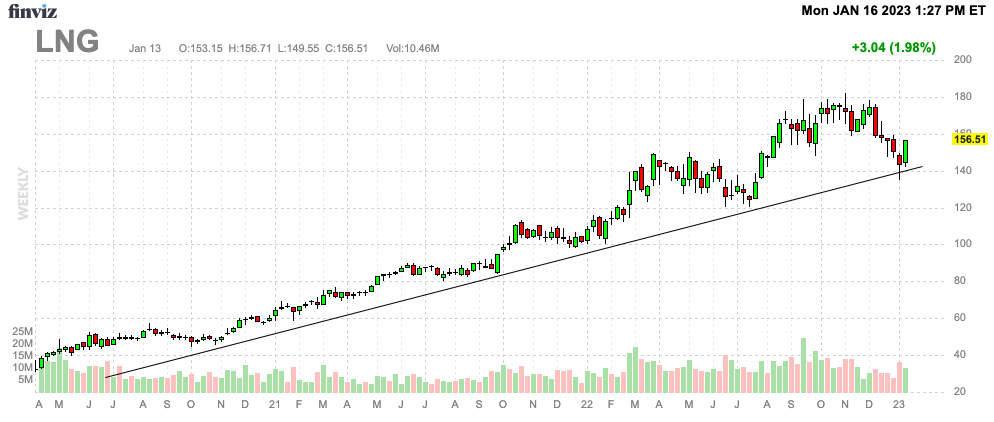

Cheniere Energy has entered a correction. The Houston-based LNG giant is currently 14% below its 52-week high. Yet, the stock remains in a perfect uptrend that started in early 2020. In other words, as soon as global energy demand reached rock bottom.

FINVIZ

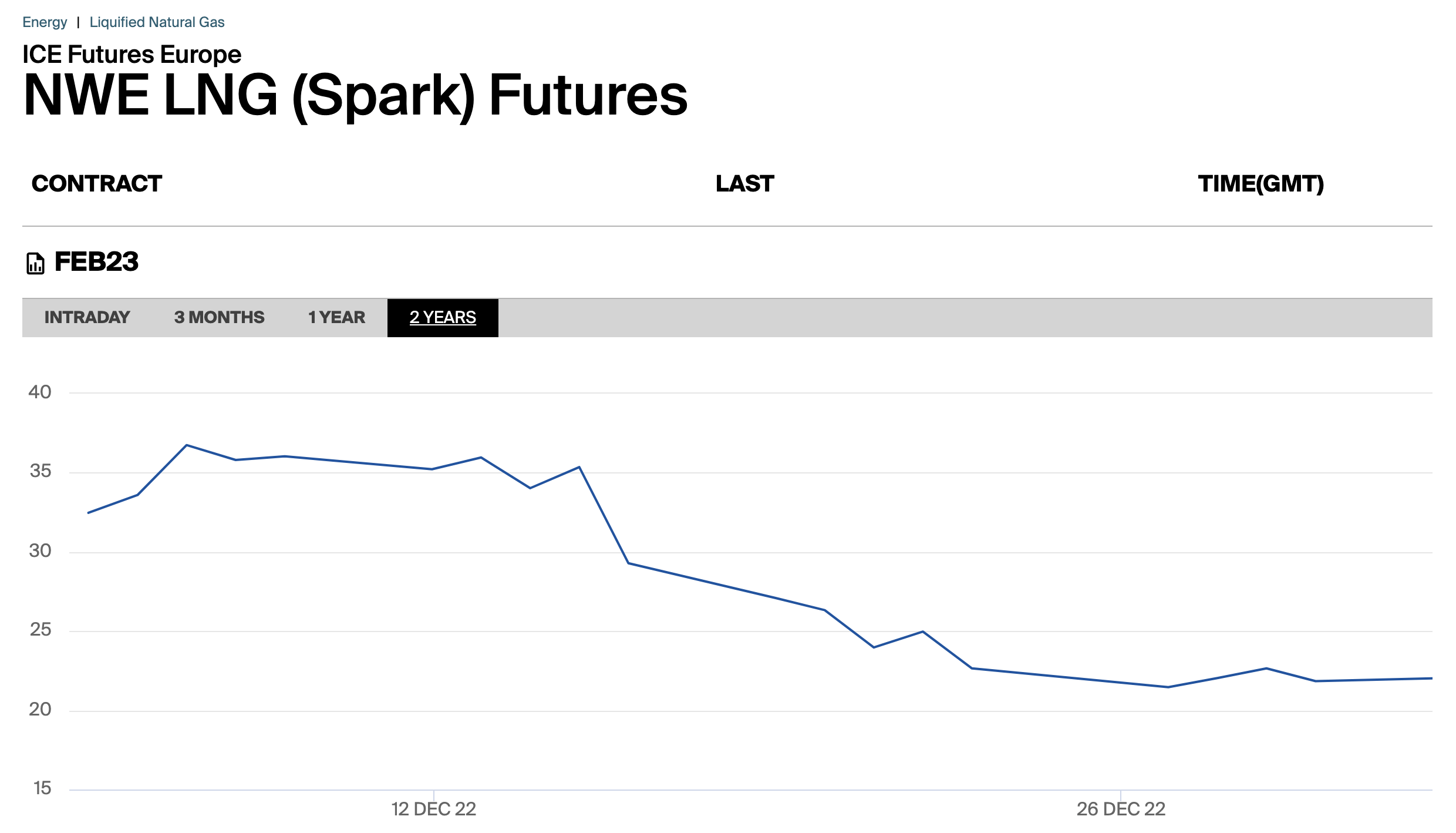

The reason why Cheniere and related stocks have weakened is that the bull case has taken a breather. The chart below shows the price of Northwest European Liquid Natural Gas Prices. It’s the first major LNG futures contract, which means its history doesn’t go back very far. However, it goes back far enough to show that prices have been hit – hard. In early December, NWE LNG was trading at $36 per MMBtu. Since then, prices have come down to $20, which is a decline of 44%. That’s a big deal.

Intercontinental Exchange

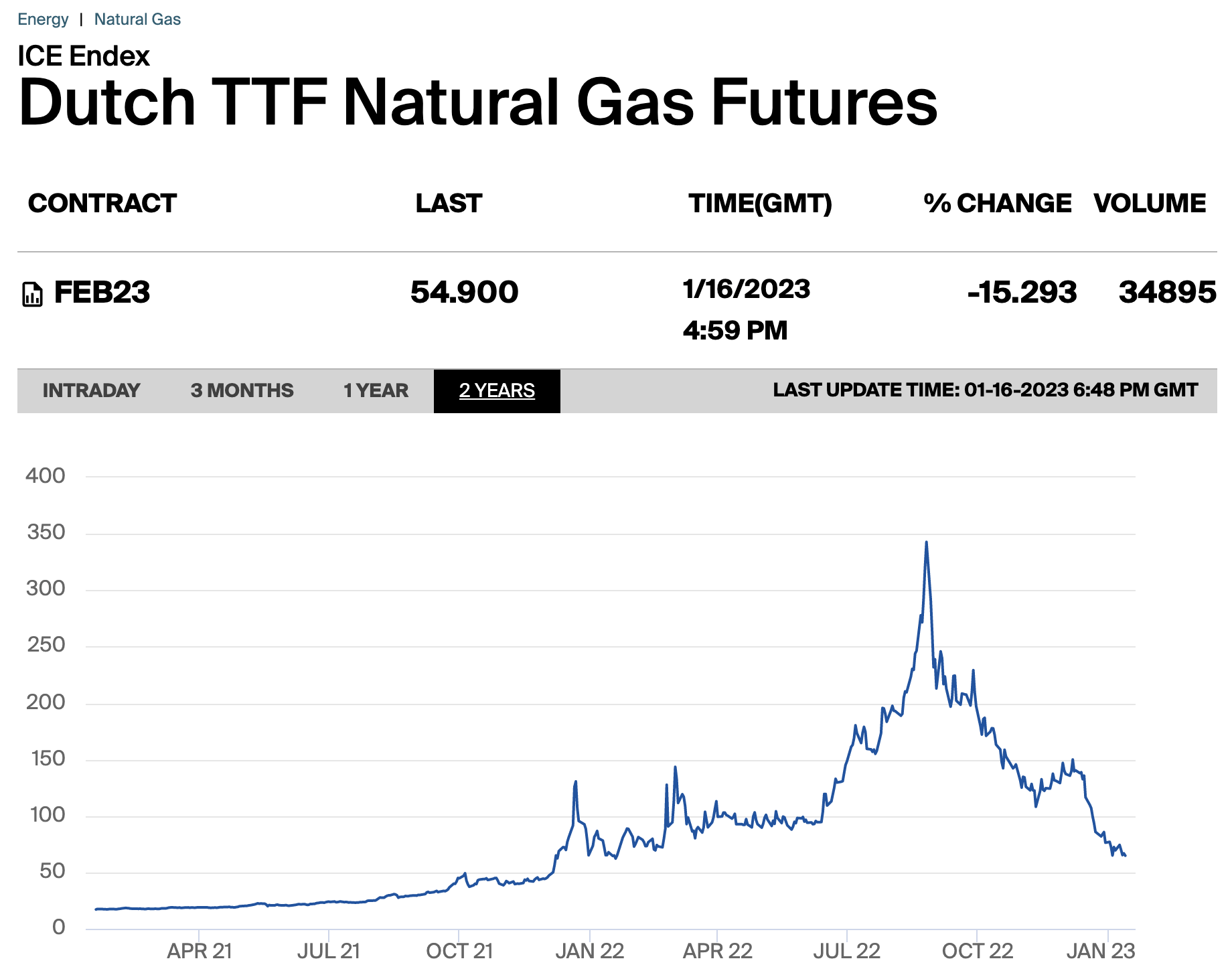

The same goes for European TTF Natural Gas Futures, which have come down a lot since peaking at EUR 350 last year.

Intercontinental Exchange

Unfortunately for Europeans like myself, this is temporary instead of the end of the bull market in natural gas and LNG.

A mix of unforeseen tailwinds has given Europe a break in its battle for long-term LNG supply after Russian natural gas exports have imploded since early 2022.

S&P Global

European gas demand benefits from two things:

- Economic-related demand destruction.

- Warm weather.

Economic-related demand destruction is a result of much lower economic growth expectations and measures to reduce natural gas demand ahead of the winter months.

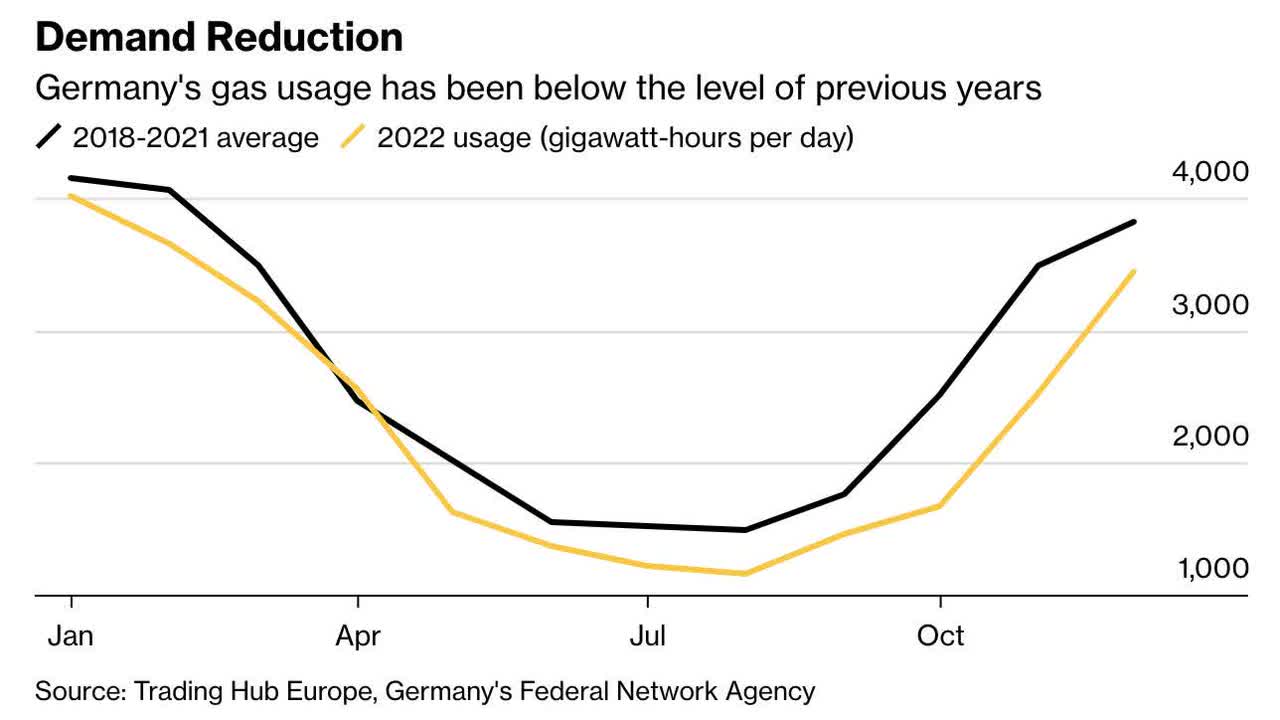

For example, in Europe’s industrial heart, Germany, 2022 demand was already much lower in the Spring and Summer months, as the graph below shows.

Bloomberg

Going into the winter, tailwind number two started to impact demand. Temperatures in Europe have been above-average for weeks. More recently, temperatures have been up to five degrees above the long-term average.

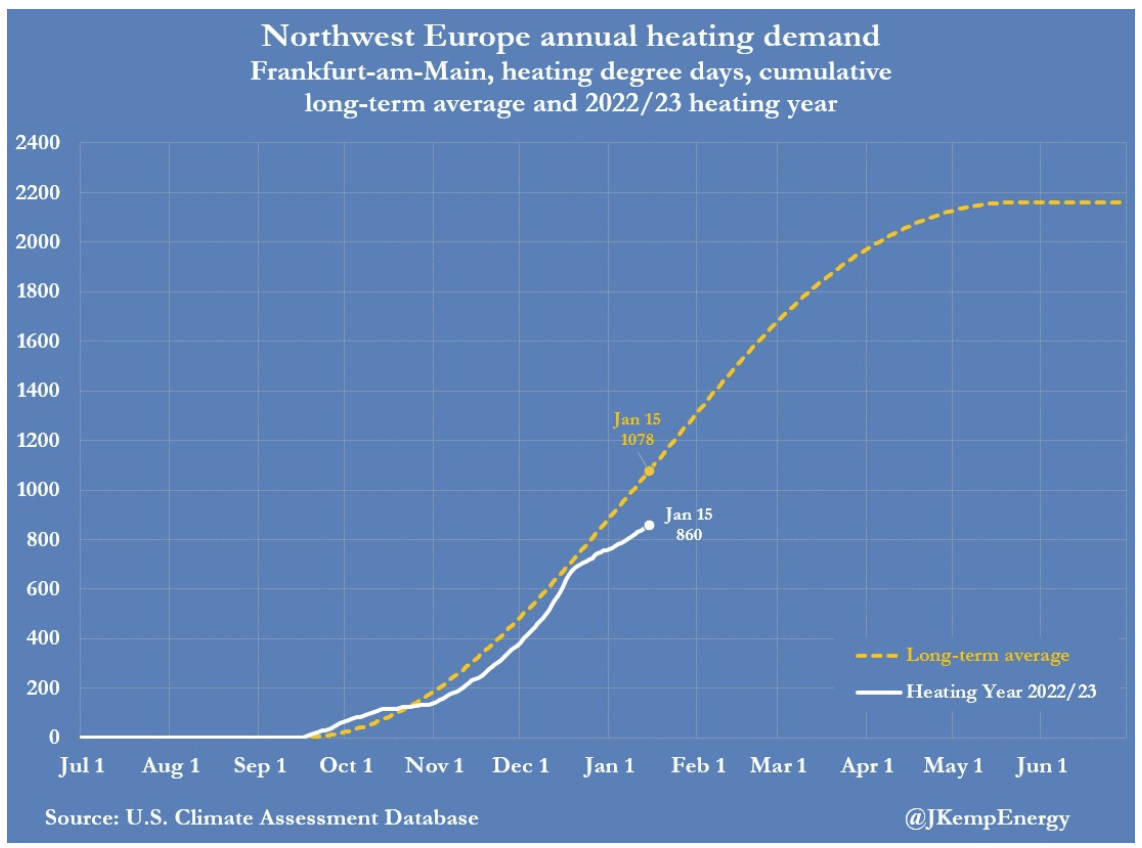

Energy expert John Kemp perfectly visualized what this did to cumulative long-term natural gas demand in Northwest Europe. We’re now well-below levels one might expect to see under normal circumstances.

John Kemp (Raw Data: U.S. Climate Assessment Database)

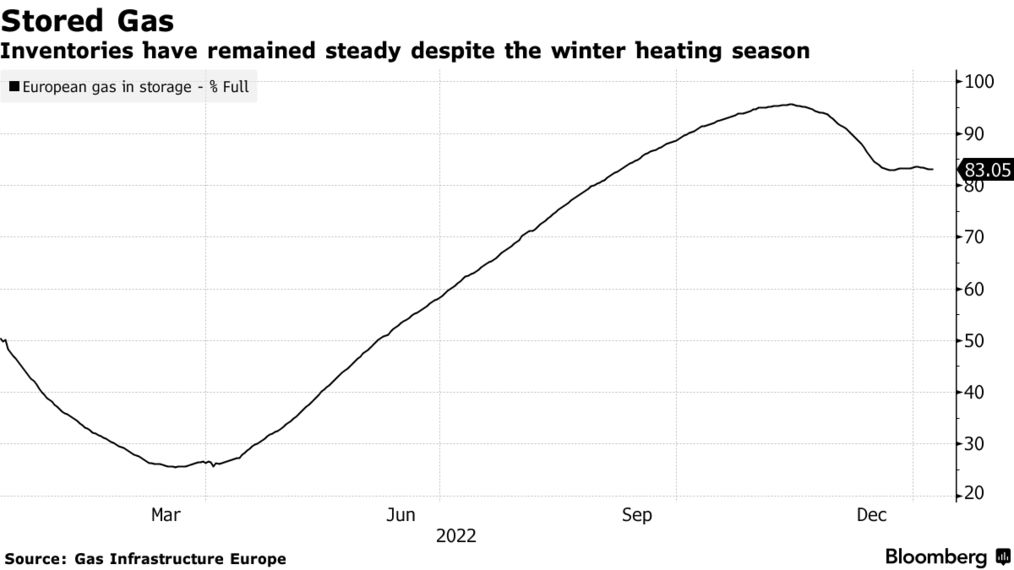

This allowed natural gas storage to remain unchanged in December and January. That’s something that buys Europe a lot of time.

Bloomberg

Moreover, Europe continues to benefit from a lot of LNG from the United States. In the first week of this year, 68% of LNG exported by the United States was headed to Europe. Only 27% went to Asia, despite fading price premiums and the expected demand spike after the Chinese government ended its Zero-COVID policy.

With that said, I’m still extremely worried when it comes to 2023 and beyond. Unless a miracle happens, Europe will have to rebuild its inventories next year without Russian gas. In 2022, it still benefited from Russian gas flows until the second half of the year. If Chinese LNG imports return to 2021 levels, we could see a natural gas shortage of 27 billion cubic meters in 2023.

With supply tight, businesses and consumers have been asked to reduce usage. The EU managed to curb gas demand by 50 billion cubic meters this year, but the region still faces a potential gap of 27 billion cubic meters in 2023, according to the International Energy Agency. That assumes Russian supplies drop to zero and Chinese LNG imports return to 2021 levels.

Also, given the US’ ability to export LNG (it all depends on infrastructure), it’s unlikely that Europe will see a price normalization before 2026. Note that even after the price slump, prices are still almost 3x as high as they were before the market started to price in a Russian invasion in 2021.

So, as much as I enjoy the warm weather and how much time this buys Europe, I’m sure it won’t last.

It’s why I believe that the decline in Cheniere’s stock price is buyable.

Why Cheniere Is The Way To Go

Liquid Natural Gas is, as the name already reveals, natural gas in a liquid state. It’s not something we invented recently, as it dates back to 1820 when British scientist Michael Faraday successfully chilled natural gas, turning it into a liquid. Roughly 100 years later, the first LNG plant was constructed in West Virginia.

Liquifying natural gas costs energy. Hence, the only reason to do it is to transport it more easily. The US cannot use pipelines to export natural gas to Asia and Europe. It needs to use ships filled with LNG.

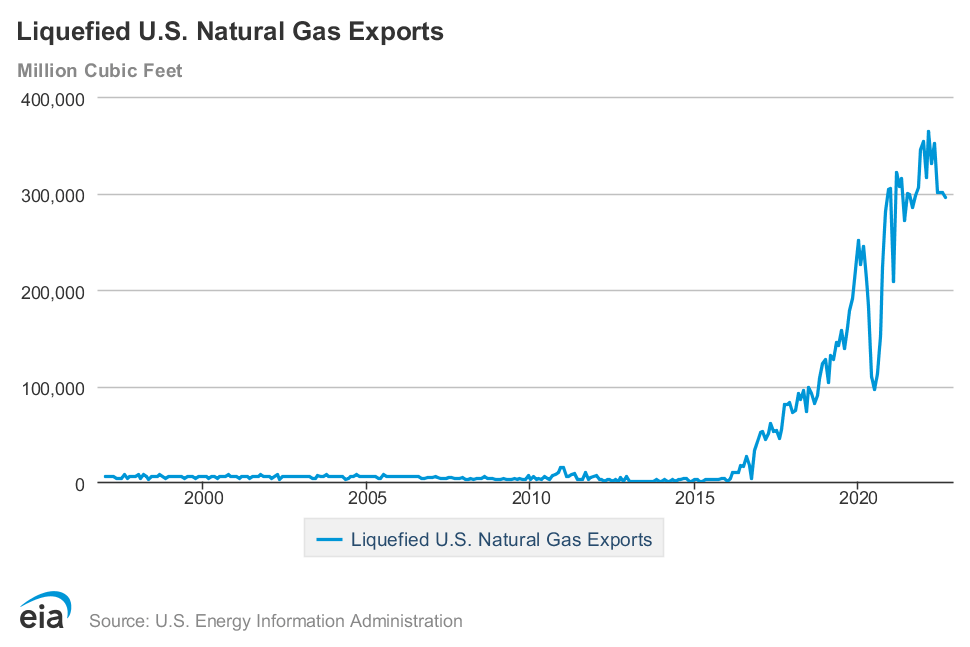

In 2016, the US exported almost no LNG. Now, it exports roughly 300 thousand million cubic feet per month.

Energy Information Administration

As the LNG boom is relatively young, there are a lot of companies that are not yet mature and dealing with high funding risks and everything related to that. I choose to ignore these companies more often than not.

Cheniere Energy isn’t a startup anymore. Founded in 1996, Cheniere became the first US company to export LNG in 2016. The company owns the Sabine Pass LNG facility, which was the sole driver of LNG export capacity for more than four years. Now, it’s still the number one LNG export facility.

Energy Information Administration

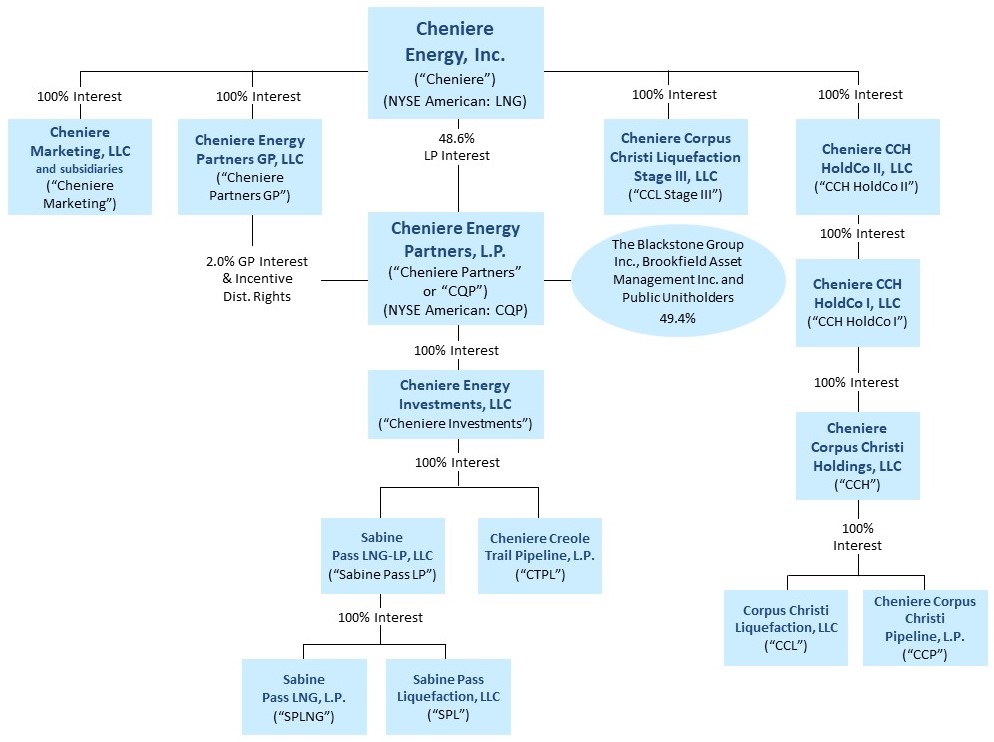

Cheniere also owns the Corpus Christi LNG facility, as its rather complex holding structure below shows. The company also owns 100% of the general partner interest and 48.6% of the limited partner interest in Cheniere Energy Partners (CQP).

Cheniere Energy

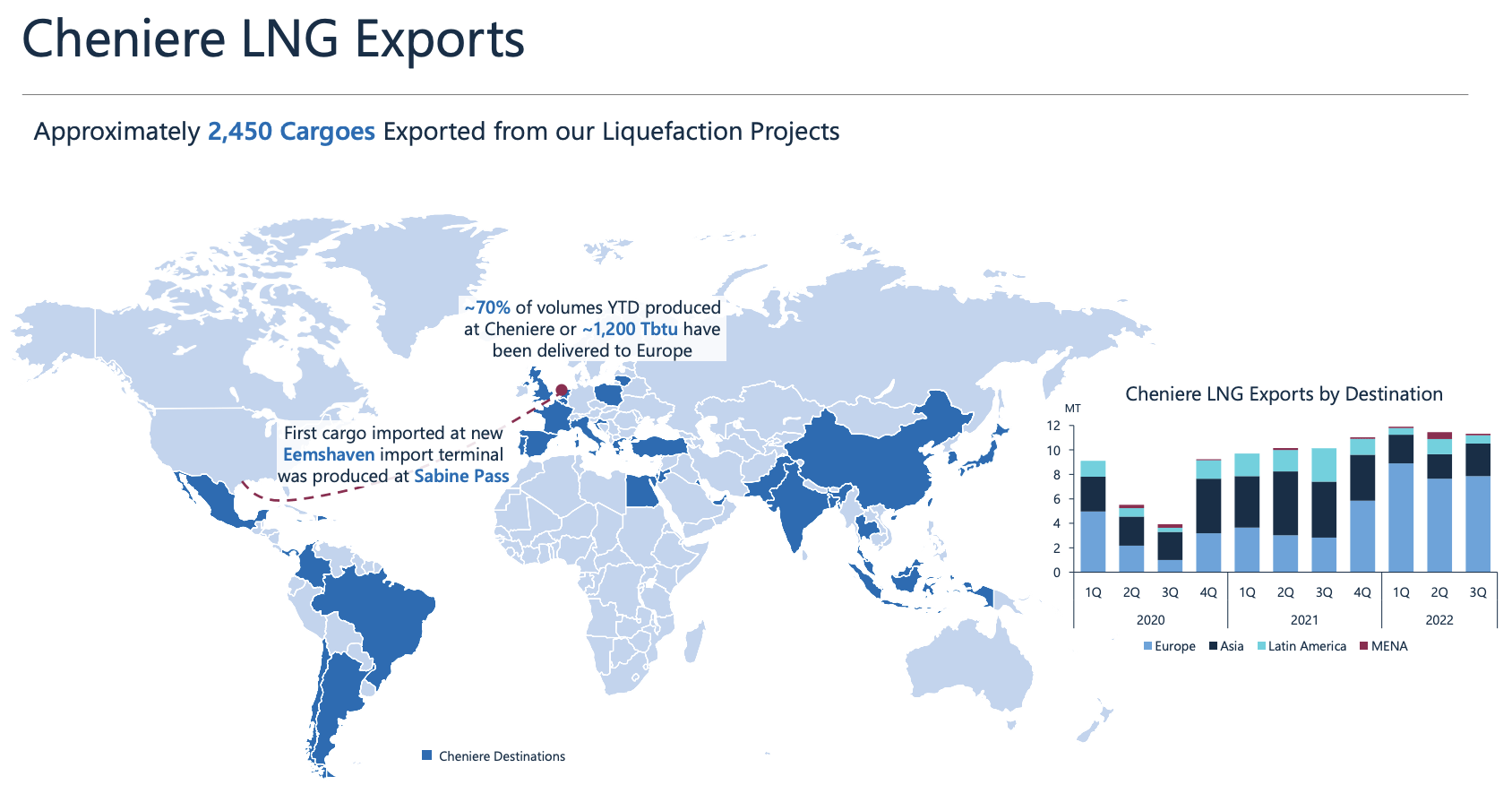

Cheniere’s massive footprint means that it is a major pillar when it comes to Europe’s energy security. In the third quarter, the company produced and exported 156 cargoes of LNG from its facilities. 70% of that ended up in Europe. In 3Q21, that number was just 30%.

Cheniere Energy

Europe, which has boosted LNG imports by 87% in 2022, heavily relies on this Texas-based company. According to the company:

[…] Cheniere alone was responsible for approximately 1/4 of Europe’s LNG imports this year. As the top middle chart illustrates, U.S. LNG volumes surged over 200% year-on-year in the third quarter as Nord Stream flows came to a halt by the end of the quarter.

Moreover, exports could have been higher if it weren’t for Europe’s missing infrastructure. As Europe didn’t expect to be forced to shift to LNG so quickly, it did not invest in sufficient infrastructure to turn LNG into natural gas again. After all, nobody predicted the Ukraine war a few years ago. And even if some did, good luck using these theories to get funding for multi-billion dollar LNG projects.

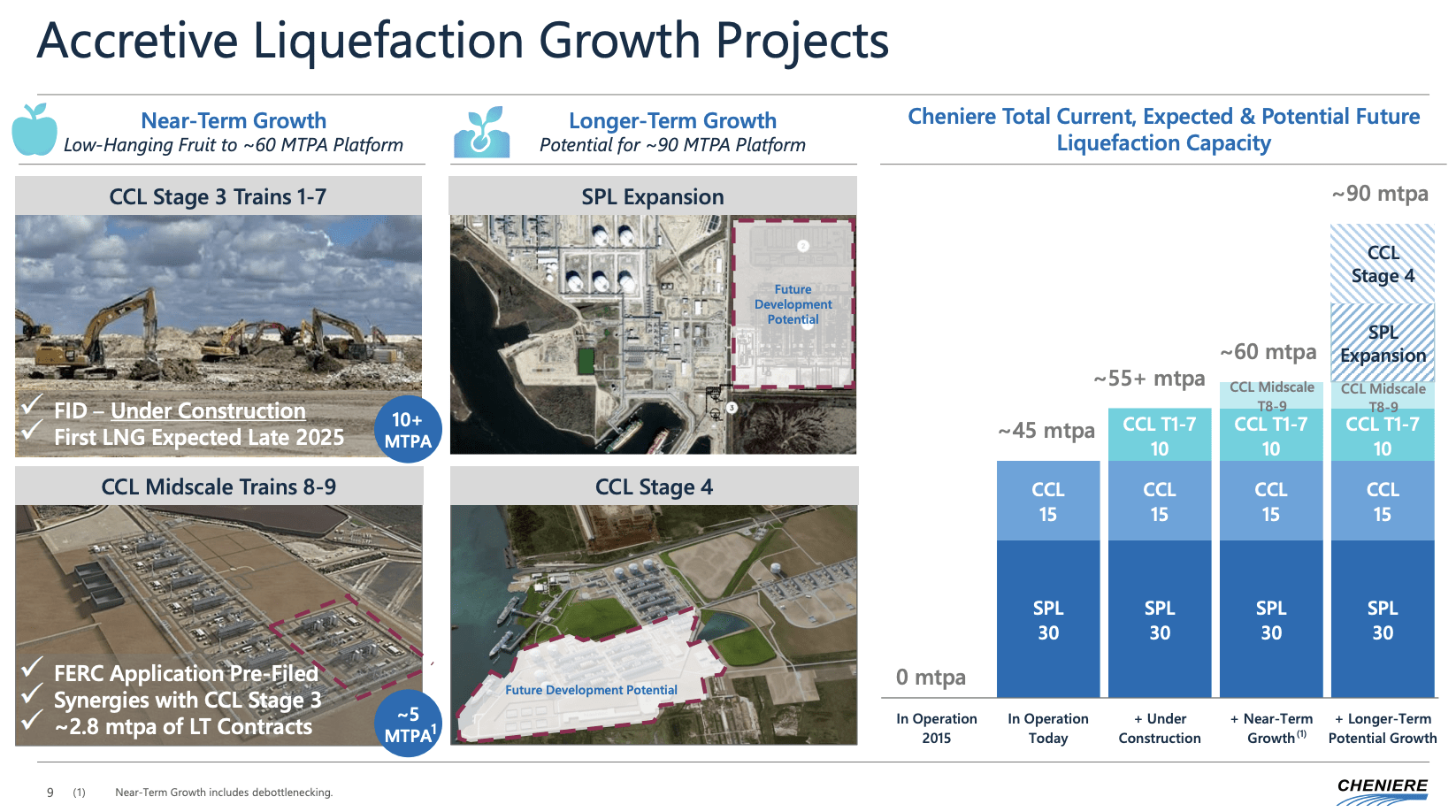

Anyway, Cheniere, which accounts for more than 10% of global liquefaction capacity (turning natural gas into LNG), is further expanding. The company currently has 45 million tons per year of liquefaction capacity. 15 of these 45 million tons are in Corpus Christi. The other 30 are in Sabine Pass. For now, the company has another 10 million tons under construction. This is an expansion in Corpus Christi, expected to be completed in late 2025. After that, it has room to add more “trains” (part of the liquefaction process) with a 2.8 million tons per year capacity. On a longer-term basis, Cheniere could double its current capacity to 90 million tons per year.

Cheniere Energy

As I mentioned earlier, these capacity expansions are expensive, and they take time. However, the company is mature. It has efficient operations and high free cash flow. Hence, the company isn’t sucking in cash but actively distributing cash, maintaining a healthy balance sheet, and investing in future growth.

Sure, this likely means that Cheniere shares have less potential upside than small startups that may make it in the industry. However, the risks are also much lower, making Cheniere a suitable stock for long-term investors.

Balance Sheet, Free Cash Flow & Valuation

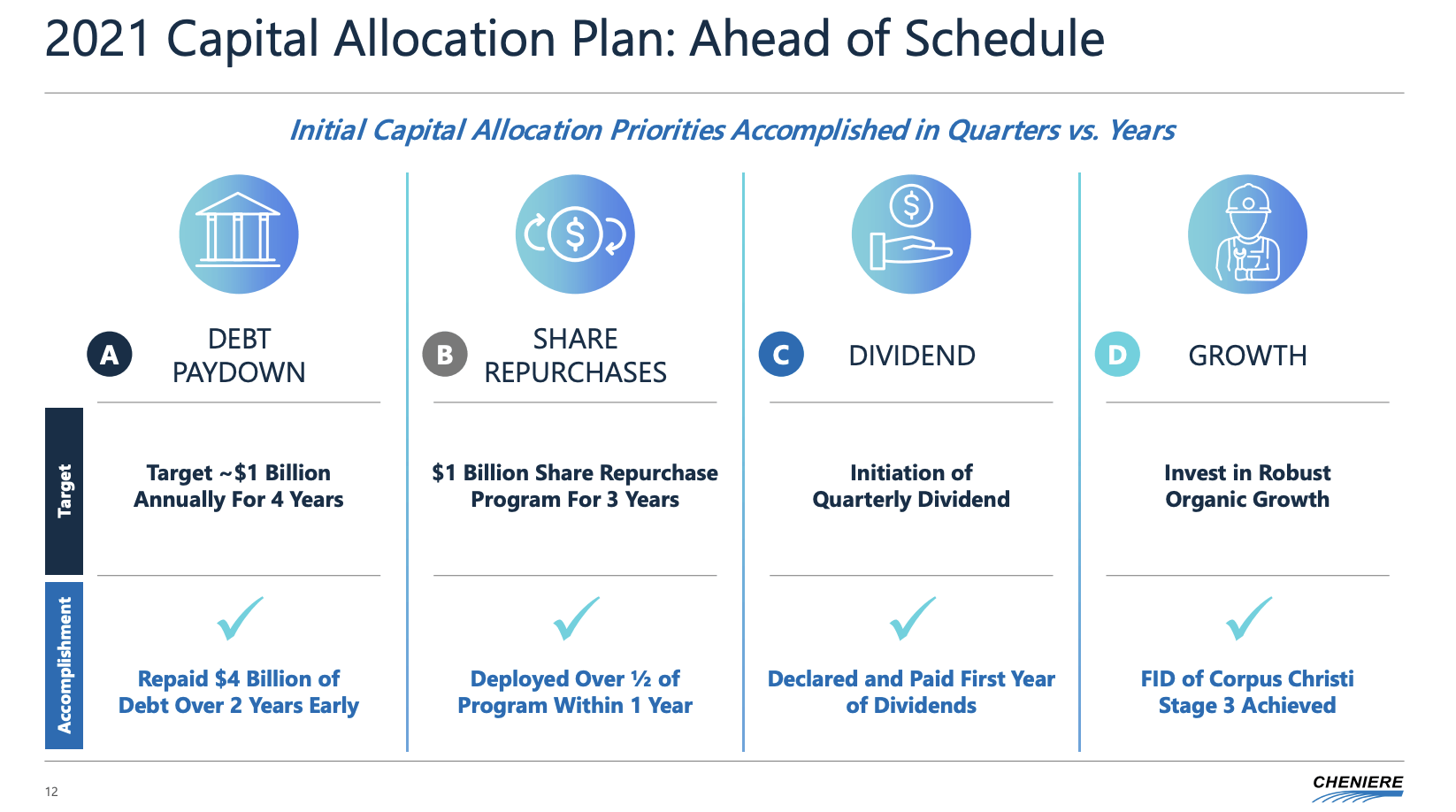

Thanks to conservative management and the massive LNG tailwinds of 2022, the company is in a good spot. It has achieved all of its capital allocation plans, established in 2021.

The company paid down $4 billion in debt instead of $1 billion. It took the company just two years instead of four. It bought back $500 million worth of shares in less than one year, declared a dividend for the first time, and achieved a milestone in growing Corpus Christi’s capacity.

Cheniere Energy

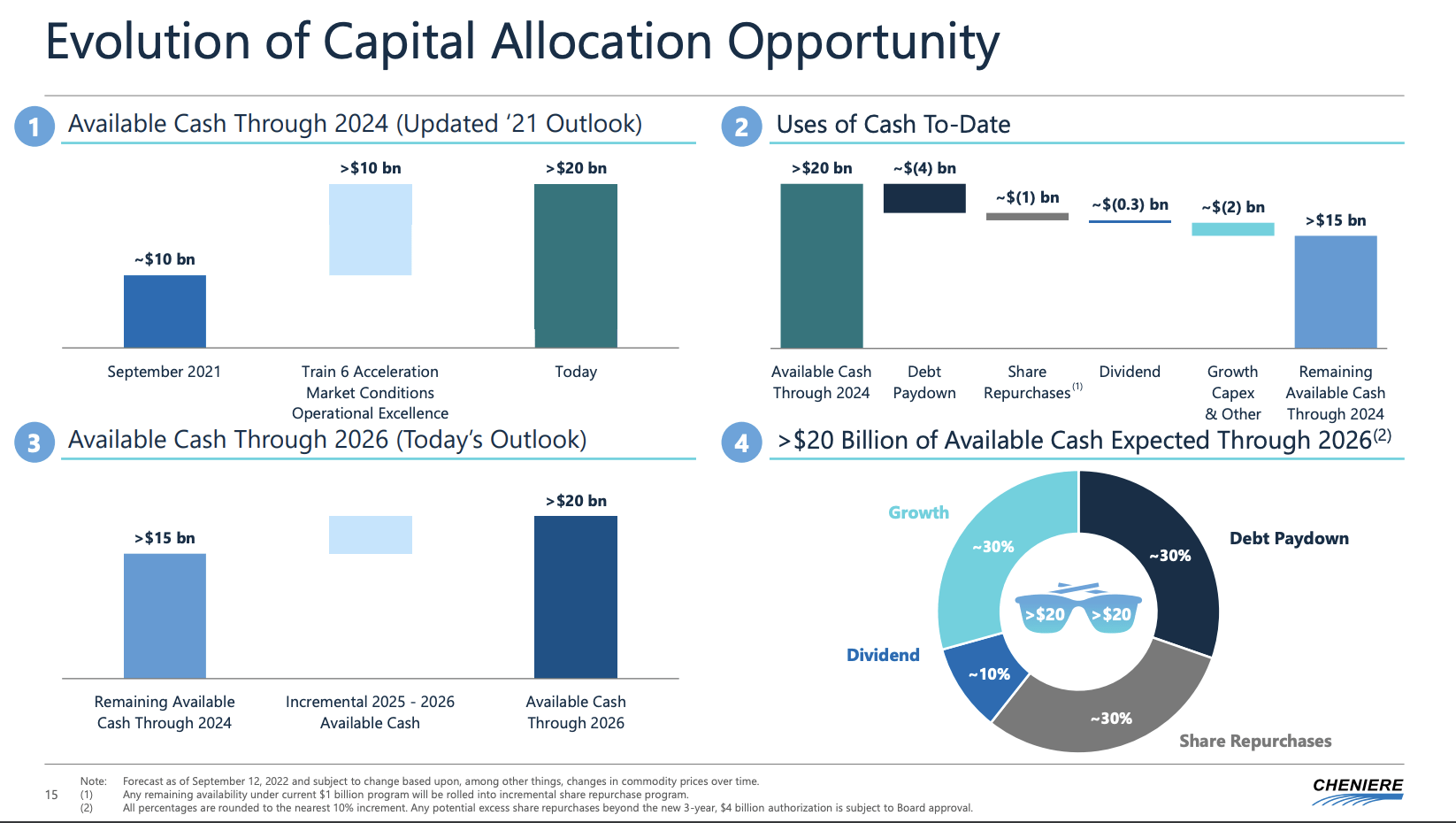

The visualization below is quite fascinating, as it shows that growth is now just 30% of the company’s available cash spending through 2026. That’s equal to debt repayment and share repurchases.

Cheniere Energy

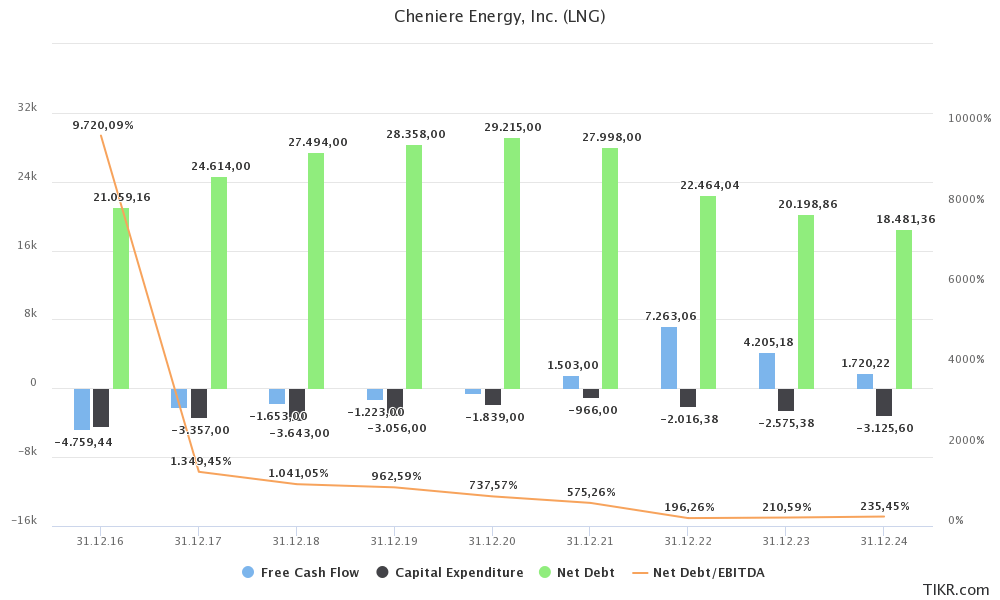

The chart below visualizes this as well. What we see is that net debt started to decline in 2021. Net debt is expected to go from $29.2 billion in 2020 to $18.5 billion in 2024, resulting in a sub-2.5x leverage ratio. Since 2021, the company is not expected to operate with an elevated leverage ratio anymore. The company has a BBB-rated balance sheet, which is just one step below the A range, and a high score for a company that is still investing billions in new infrastructure (which comes with additional risks). I expect the company to be A-rated at some point in the 2-4 years ahead.

TIKR.com

This is only possible due to improving free cash flow. While capital expenditures are expected to rise again due to the aforementioned projects, free cash flow is not expected to go negative again.

Note that even in 2024, the company would generate $1.7 billion in free cash flow, implying a 4.4% free cash flow yield (based on its $38.9 billion market cap). I even think that 2024 numbers will be way higher than estimates, as sell-side analysts seem to incorporate a quick normalization of LNG prices.

This also means that Cheniere remains attractively valued. The company is trading at 6.3x 2023E EBITDA of $9.6 billion. This is based on its $60.9 billion implied enterprise value, consisting of its $38.9 billion market cap, $20.2 billion in expected net debt, and $1.8 billion in minority interest.

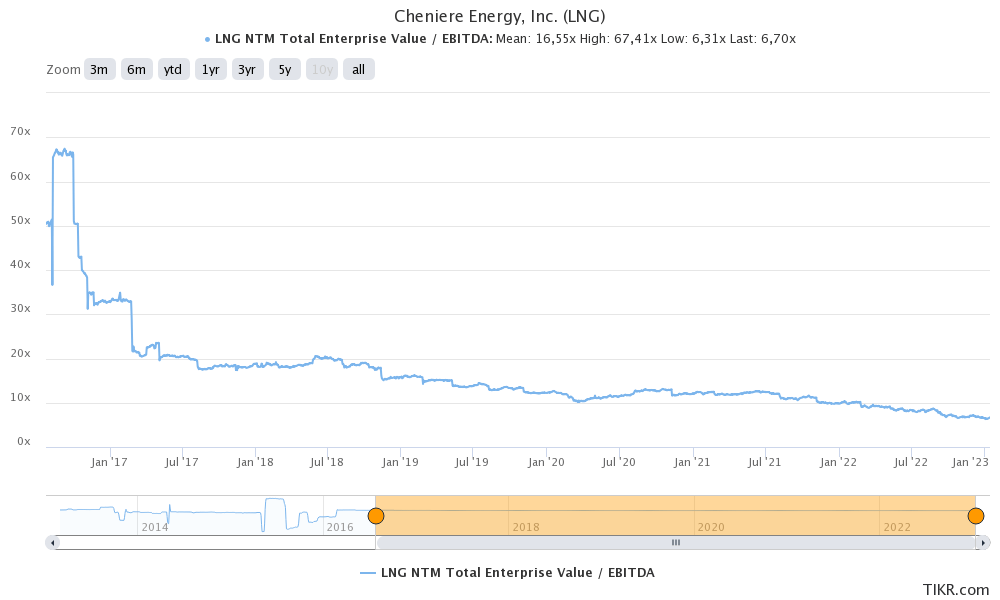

Using historic valuations is hard because the company has been unprofitable and reliant on external funding more often than not in the past.

In 2017 and 2018, the company was trading at 20x NTM EBITDA. Now, that number is consistently below 10x.

TIKR.com

If we incorporate somewhat moderating EBITDA (due to lower prices in the two years ahead), I think Cheniere should trade at 10x EBITDA. This would imply between 40% to 50% more potential upside, giving the stock a price target range of $215 to $235. This makes me a bit more bullish than the average analyst. The company’s current average price target is $206. The most recent buy ratings are:

- Citigroup $205

- Jefferies $210

Risks

The company has become the epicenter of global geopolitics. After all, it ships and produces the commodity that fuels the European and Asian economies at a time when Russia has been isolated from doing business with Western nations.

- Major risks include a rapid end to the war in Ukraine and new business relationships with Russia. Don’t get me wrong, I’m rooting for an end to the war, but it needs to be said that this would quickly reduce natural gas prices if it were to come with new business relationships with Russia.

- Cheniere’s ability to fund its operations and expansion. I believe this risk is contained thanks to 2021/2022 tailwinds and the fact that the company is now gradually expanding instead of building an entirely new business.

- Catastrophic weather events could impact the company’s ability to produce and ship LNG. The same goes for other events like the ones Freeport LNG experienced.

Takeaway

In this article, we discussed Cheniere Energy, which has turned into one of my all-time favorite LNG plays. The company remains in a good spot to remain the king of LNG exports, benefiting from high prices, sky-high (and further rising) demand, and its ability to use cash for buybacks, dividends, and debt reduction.

Due to short-term weather and demand tailwinds in Europe, I believe that Cheniere shares offer a buyable correction. While cyclical risks continue to exist, I believe that Cheniere remains significantly undervalued.

(Dis)agree? Let me know in the comments!

Be the first to comment