nimis69

(Note: This article was in the newsletter on December 10, 2022.)

Management of Chart Industries, Inc. (NYSE:GTLS) in effect doubled down on the Howden acquisition by doing a second supplemental presentation of the benefits of the acquisition. But that part of the acquisition does not appear to be what bothers the market the most. Instead, the financing appears to be the source of the market angst because that financing proposal left the company far too leveraged after the merger.

Management had originally proposed a fast deleveraging. But most of us have been down that road enough times to know how risky that can be. There are a lot of fears about a recession that make the quick deleveraging untenable in the eyes of the market. That is true even though this company has a fair number of customers with projects that continued right through fiscal year 2020.

Stock Price Action

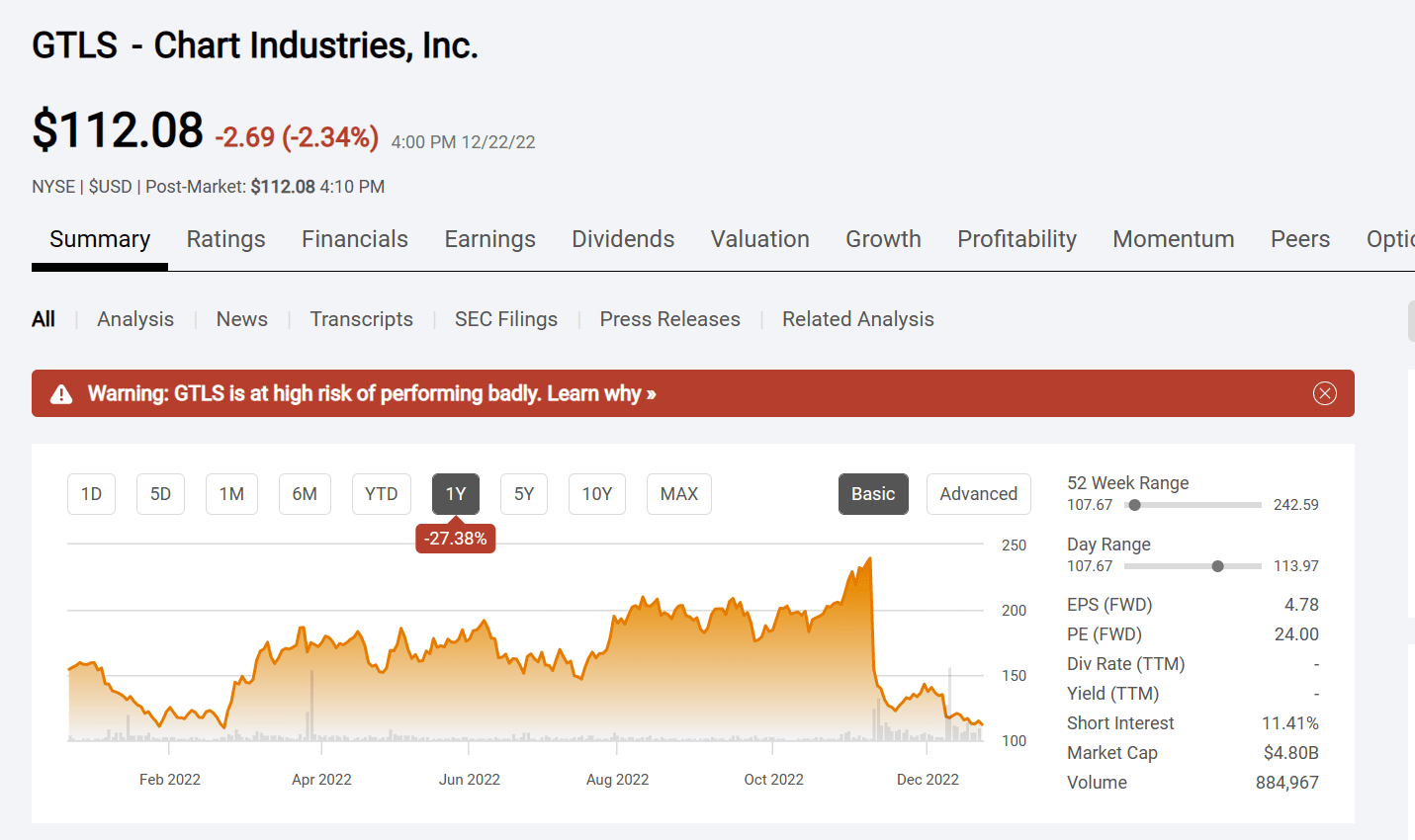

Mr. Market frankly did not care and decimated the stock price.

Chart Industries Common Stock Price History And Key Valuation Measures (Seeking Alpha Website December 22, 2022)

The market completely ignored the long lead times of this business and the fact that there were not massive cancellations in the backlog in fiscal year 2020. The stock price followed all other stocks straight into the garbage can.

But Chart has large projects with long lead times. Those projects often move forward during the worst of times unless those “worst of times” hang around for years. The company amply demonstrated that orders did slow a very little bit. But the backlog remained essentially intact and order activity quickly picked up during the recovery. That sent this stock soaring from the teens to a ridiculously high price as Mr. Market went overboard the other way.

Financing

But Mr. Market can be really stubborn when it comes to making exceptions. Despite the ample demonstration of a recession resistant business, the market is just not giving way on conservative financing for this company. The minute the original proposal for financing came out, the stock price dove. Management managed to wipe out nearly 50% of the stock price value with one ill-considered announcement.

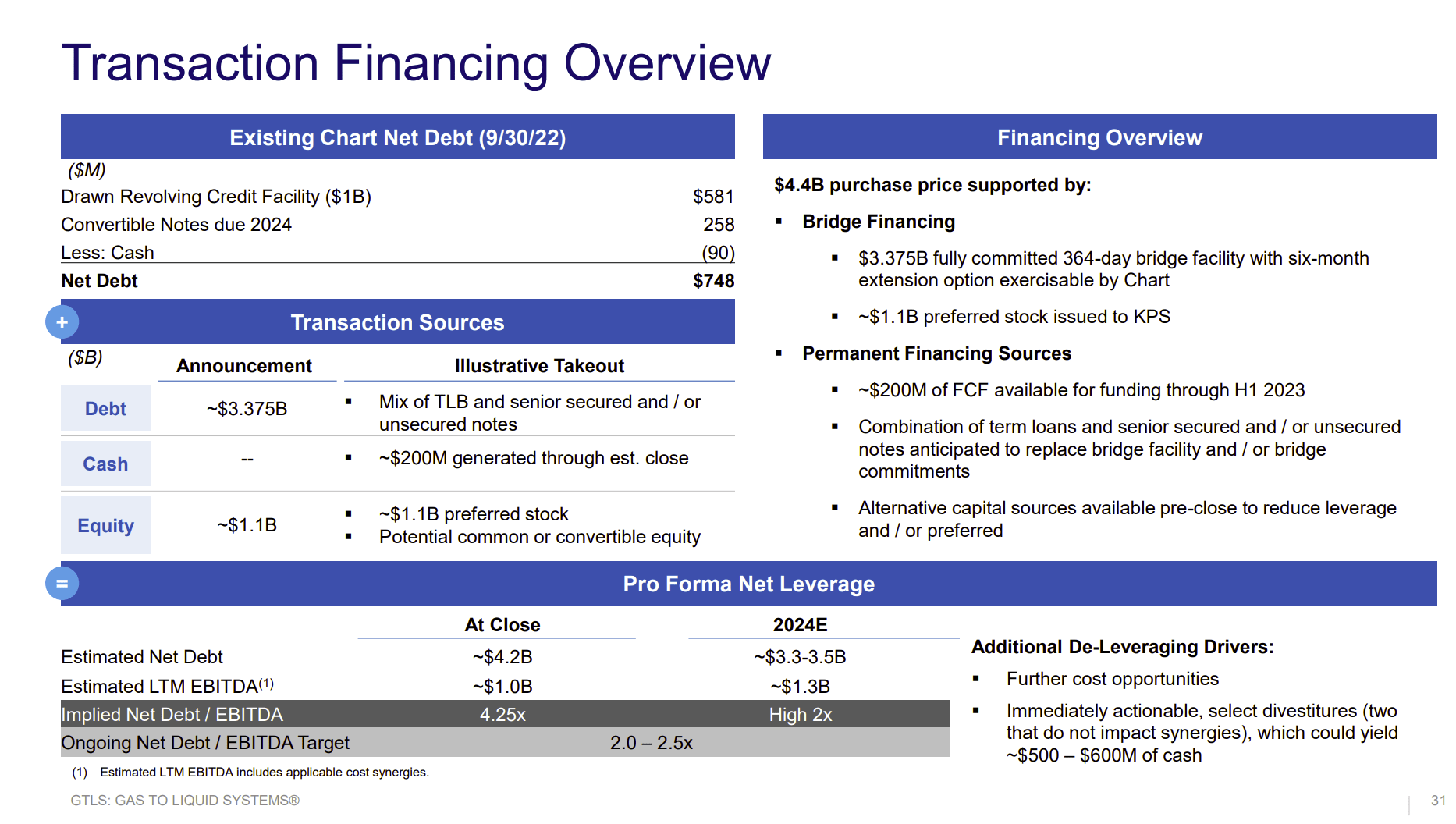

Chart Industries Financing Description Of Howden Acquisition (Chart Industries Supplemental Howden Acquisition Presentation November 14, 2022)

The whole problem is that for common shareholders there is both preferred stock and debt. Even though management is satisfied with the leverage as shown above, common shareholders will likely include the preferred stock in that leverage because it has superior claims. The resulting leverage is unacceptable to shareholders.

Management did “bend” a little bit by offering some common shares to the public to reduce the leverage somewhat shown above. However, it is still a highly levered deal, and the late decision meant more shareholder dilution because the shares were sold to the public after the big price drop.

Admittedly, the convertible notes were a “sure thing” to convert until management hatched the current proposal. It would have behooved management to entice the convertible notes to convert before making this announcement. Every little bit helps.

Any stock will be weak after a public offering. In this case, it may remain weak for a while because the convertible debt will put more stock in the market by 2024 and the preferred sold is also convertible at 97% of the share price at closing. It may necessitate a dividend to entice the preferred stock to convert. This company generally uses all the cash generated to grow.

The other thing is the debt is relatively expensive. In the past this company issued convertible debt above the current market price in order to finance acquisitions. So, repaying debt is yet another thing that this company has really not done lately.

The relatively high interest rate of the debt (compared to the convertible debt) as well as the preferred stock dividend combined with the large size of the acquisition still make this a very risky proposal going forward from a financial standpoint. Of course, management is confident, but we have all been down that road before with confident managements. It makes one wonder if management should admit their mistake and just back out of the whole mess. But things are too far along for that to happen.

Acquisition Benefits

Chart has a long history of making acquisitions. Generally, management keeps much of the company personnel and plants in place. The sales force and other administrative items are combined where possible to allow a comprehensive sales presentation to a wider variety of customers. In this way, Chart has grown successfully in the past.

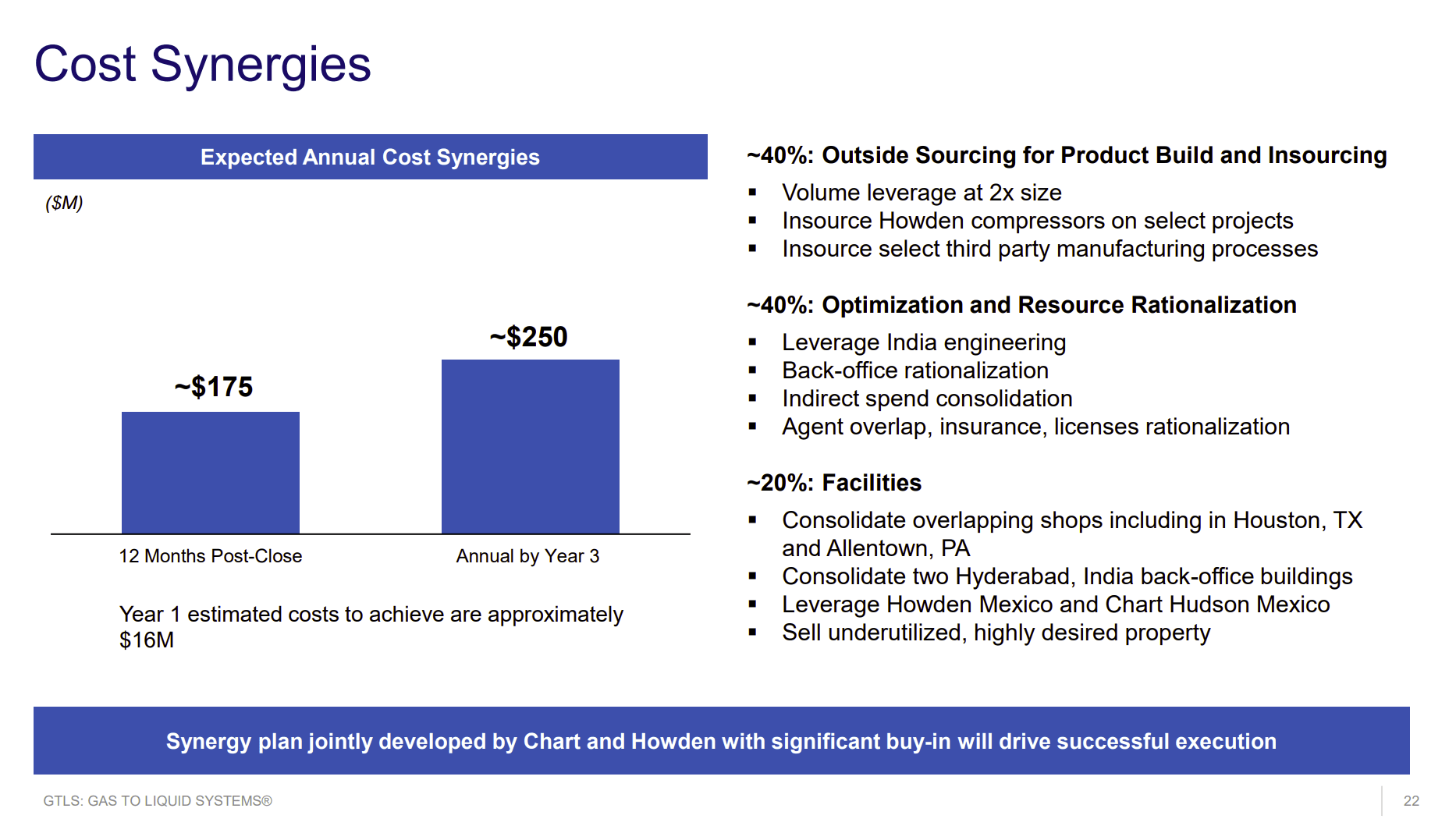

Chart Industries Description Of Howden Acquisition Synergy Savings (Chart Industry Presentation Of Howden Acquisition Supplemental November 14, 2022)

It is easy to see from the presentation and the notes above that there are not going to be a lot of cost savings. Instead, management is banking on making the benefits from increased sales. There is a bunch of products that Chart does not have that Howden makes that would increase the benefits of the combination materially.

Of course, the market is concerned about a potential recession in the immediate aftermath of the acquisition straining company finances to the point where the company becomes a zombie corporation. Frankly, this is something that management should have anticipated.

I had noted in previous articles that the one risk of a company with a history of acquisitions is that they make one that is too large and too leveraged. I had no idea it would happen this fast (and with devastating stock price consequences as well).

The Future

What probably needs to happen is another sale of about $1 billion of common stock. After that, Chart Industries management will need to go to some lengths to assure the market that they will never present a deal like this to shareholders in the future.

Management could have avoided this by announcing a sale of common stock of at least $1 billion when they announced the acquisition. $2 billion would have been ideal, but it is a legitimate question as to whether or not that much stock could have been sold. The stock price decimation would have been nothing close to the current reaction.

The interest rate on the debt alone should have clued management in about the financial riskiness of the situation. This is a company that has issued convertible debt in the past while paying 1% or 2% interest. So, the latest deal is a far cry from that interest rate along with forcing conversion of the debt.

The other thing is that the market reaction to this deal may force an end to the acquisition strategy for new products for the time being. Frankly, debt was getting a little bit too high for me in the first place, which was why I sold my shares a while back. I do not like debt and this company had a very bad experience with debt many years ago. One would think they would have not forgotten that.

Nonetheless, there are adventuresome investors who may be interested in this company with its attractive growth record and heavy concentration of “green” products. To me, the sale of some common stock combined with the sharp decline makes this a speculative issue for risk taking investors only. There is a good chance that management meets its goals.

However, any investors should wait for the Chart Industries stock price to settle before thinking about getting in. Clearly Mr. Market is in “freight train” mode, and I do not as an investor stand in front of stock price “freight trains” heading south. So, the first order of business is for Mr. Market to get the negative sentiment out of his system and then consider a speculative investment.

This is a good management that has done a lot of right things. If they recover from this, then hopefully Chart Industries management learned how to keep a good thing going in the future. But in the meantime, it will be a rocky ride in the near term because management has made a big financial mess.

Be the first to comment