Amax Photo

The CBD space has mostly stalled over the last couple of years due to regulatory inaction. Charlotte’s Web Holdings (OTCQX:CWBHF) (‘CWH’), a once-promising stock, has become a disaster with years of no growth. My investment thesis is Bullish on the stock valuation, but CWH isn’t likely to rally much until the regulatory environment changes.

Going Nowhere Fast

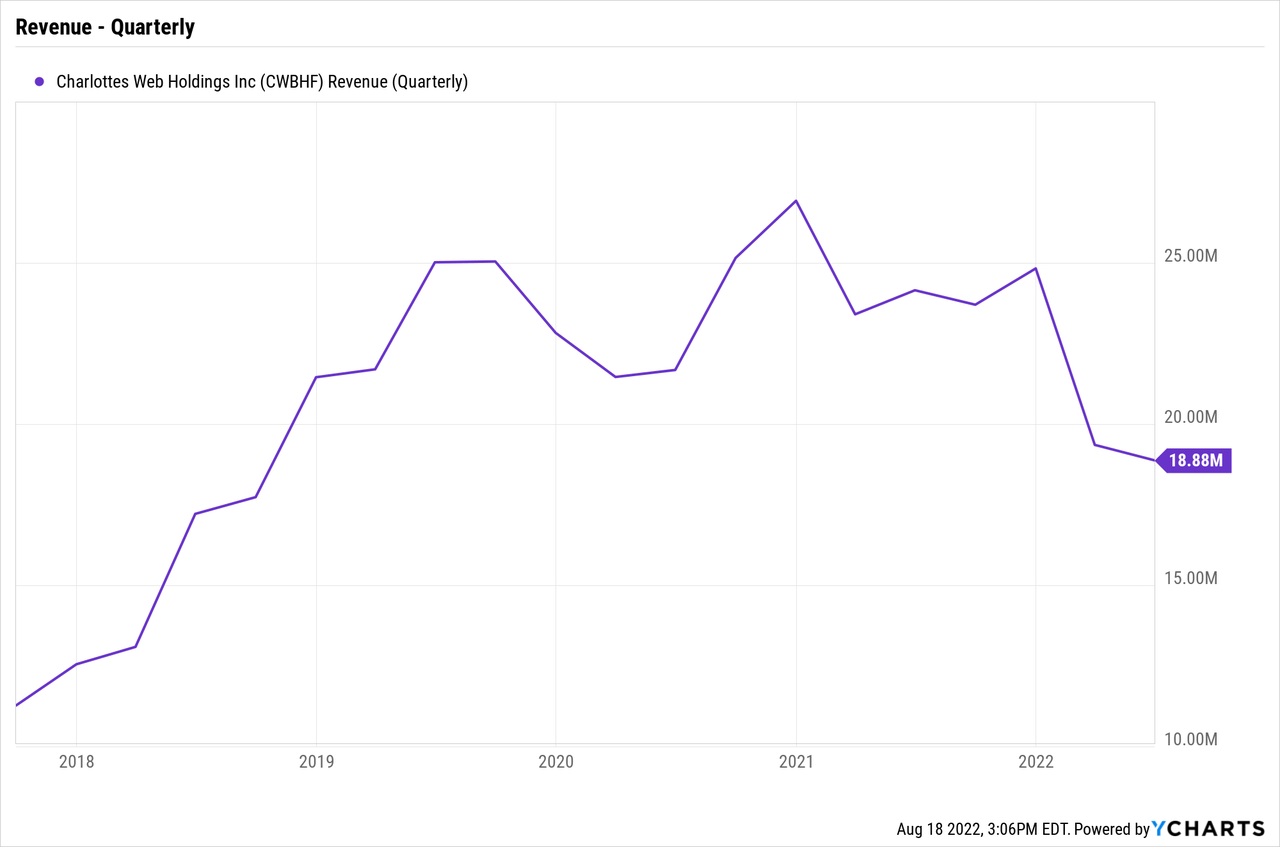

The full-spectrum hemp extract wellness company continues to watch sales stall, and even deteriorate while waiting on the FDA to make a decision. For Q2’22, revenues were $18.9 million, down $5.3 million from the prior year. When excluding $0.9 million for inventory returns from one customer, sales were up slightly from Q1’22.

CWH was a leader in online CBD sales, so the company likely got a disproportionate boost from online sales during Covid. The current weakness is partly related to lower e-commerce traffic as the U.S. economy fully reopened over the last year. In addition, B2B sales have virtually dried up dipping to just $5.6 million, or $6.5 million when excluding the inventory reserve.

The CBD specialist has done everything seemingly possible to alleviate sales declines, whether via entering international markets or new verticals. Either way, the lack of regulatory clarity has kept CBD sales stalled since after the Farm Bill was approved in 2019.

CWH has improved the ability of the company to achieve profitable operations on reduced revenues. The company cut SG&A expenses last year by 30% and the recent July reduction has those expenses down to $70 million annually, or what amounts to $17.5 million quarterly.

For Q2’22, CWH reported an adjusted EBITDA loss of $0.54 million without adjusting for the returned inventory and provisions. Though, some of these expenses should be considered as normal course operations in a cannabis business.

CWH will need revenues to approach $30 million with 60%+ gross margins to reach breakeven on an operating income basis. Naturally, the CBD leader will cut a substantial amount of cash flow losses via just topping $20 million in quarterly sales. CWH reports nearly $2 million in quarterly non-cash depreciation costs along with an additional amount for stock-based compensation.

Promising Opportunities

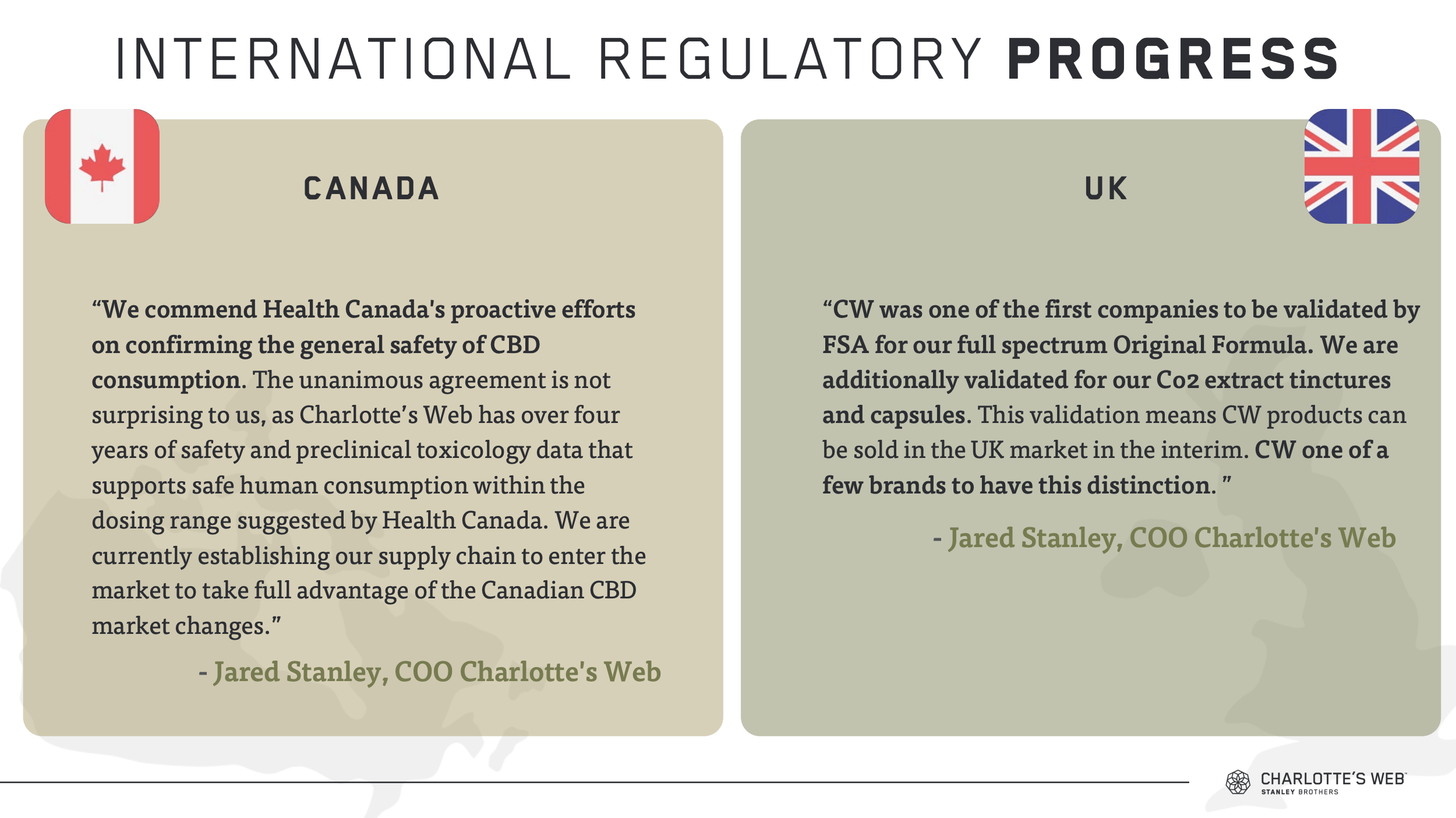

The reason to invest in CWH, or any CBD business, is the potential for regulatory changes allowing hemp in food products along with international and vertical expansion. The international expansion remains promising on multiple fronts, with initial approvals in Canada and the UK. CWH has already entered Israel and has a distribution agreement in Greater China via Energy Hemp Biotechnology.

CWH Q2’22 Presentation

All of these countries add potential avenues for growth, but our view has always been skeptical that foreign firms will capture large portions of these markets. Of course, any revenues will be a positive for a company failing to maintain current revenue levels.

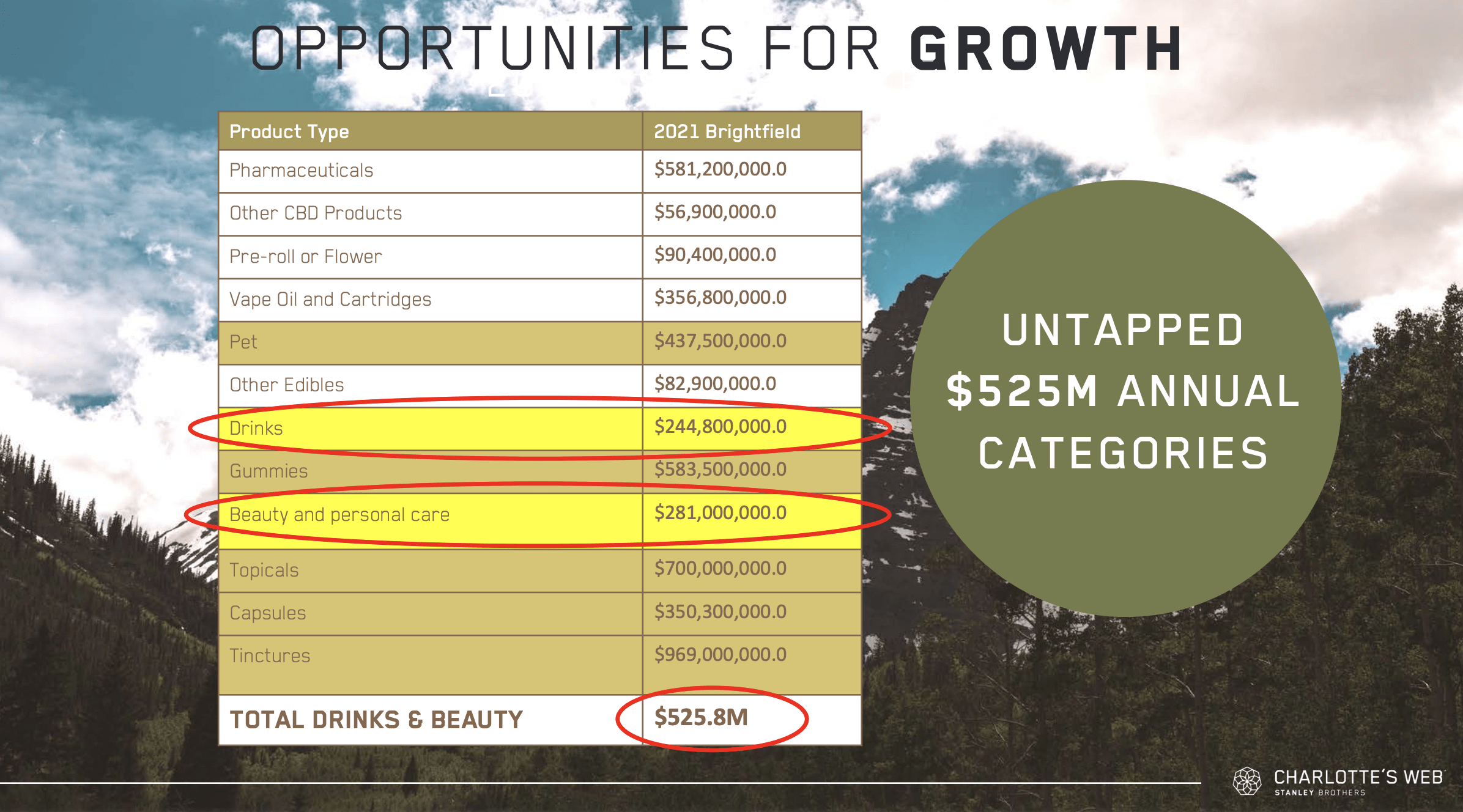

CWH has promising opportunities to enter the drinks and beauty segments, where over $526 million worth of market opportunities exist. The company entered the pet segment recently and bought into other segments without these additional categories helping to improve sales as demand shifts and pricing pressures lowered sales from other previous verticals.

CWH Q2’22 Presentation

The Brightfield Group forecasts U.S. CBD sales to remain mostly flat into the future without any FDA regulations. The research firm estimates CBD sales will surge to $11 billion by 2027 with FDA regulations starting in 2024.

CWH has ~$17 million in cash on the balance sheet following some IRS refunds. The company needs to reach positive cash flows in order to prevent material dilution via raising additional capital for the business.

The market cap is only a minimal $105 million now with 153 million diluted shares outstanding. The stock trades at a minimal P/S multiple, but CWH isn’t likely to rally much until the CBD market no longer has regulatory restrictions, or an international location provides actual material revenue growth.

Takeaway

The key investor takeaway is that CWH is a difficult stock to own, with the business story mostly stalled until the FDA makes a regulatory decision. Investors aren’t likely to lose owning the stock here, but the best move might be to own a partial position with the intent to load up when the business climate improves.

Be the first to comment