Darren McCollester/Hulton Archive via Getty Images

The Charles Schwab Corporation (NYSE:SCHW) has been extremely volatile over the past year, leading to its stock having flat returns in the past year. We think that investors are too hyper-focused on the linear decline between client assets and the markets, as well as tough trading revenue comps after a record 2021, ignoring the win-win proposition for recession and post-recession growth.

Benefitting From A Rising Rate Environment

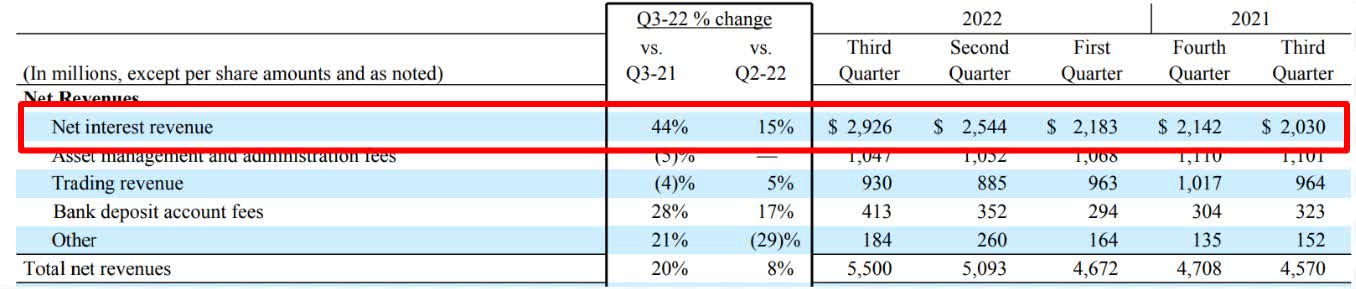

Charles Schwab Q3 2022 Earnings Report Charles Schwab Q3 2022 Earnings Report

Net interest revenue accounts for about 60% of total revenues with 44% Q3 and 30% first 9 months y/y growth. Across the board, Schwab was able to charge a higher yield (average yield was 52 basis points higher than Q3 2021) on an increasing amount of interest-earning assets (total interest-earning assets were 6% higher than Q3 2021), driven by higher rates.

These numbers excite us because we believe both net interest margin (“NIM”) and average interest-earning assets will expand, helping to power stronger revenue growth across the short, medium, and long term.

NIM

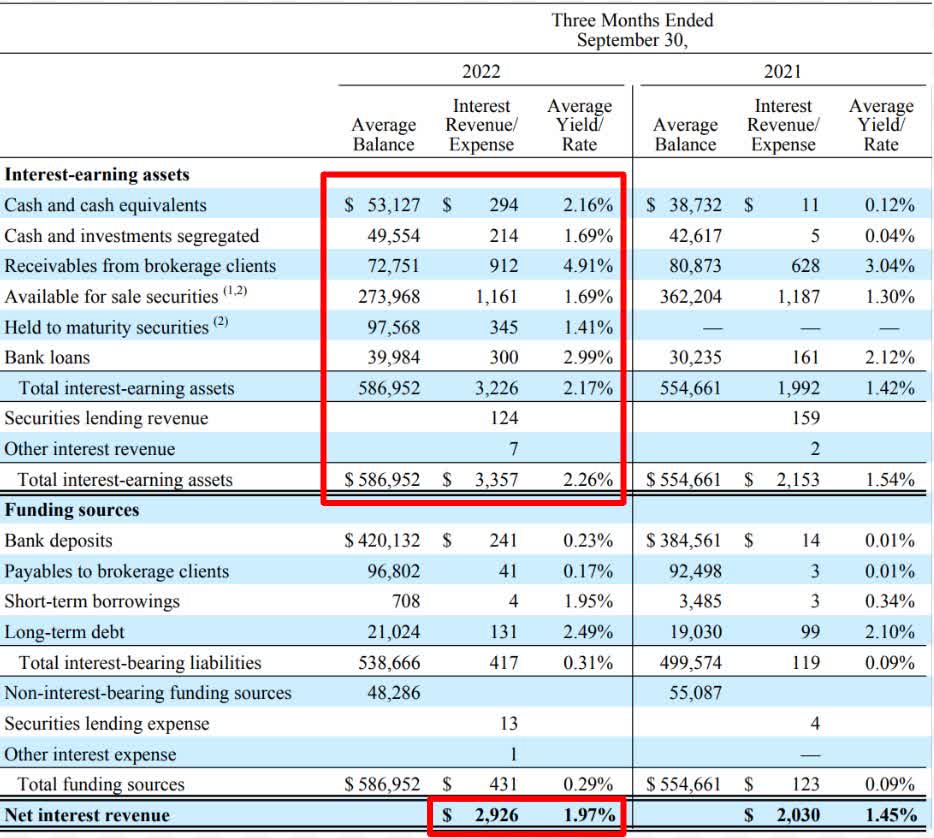

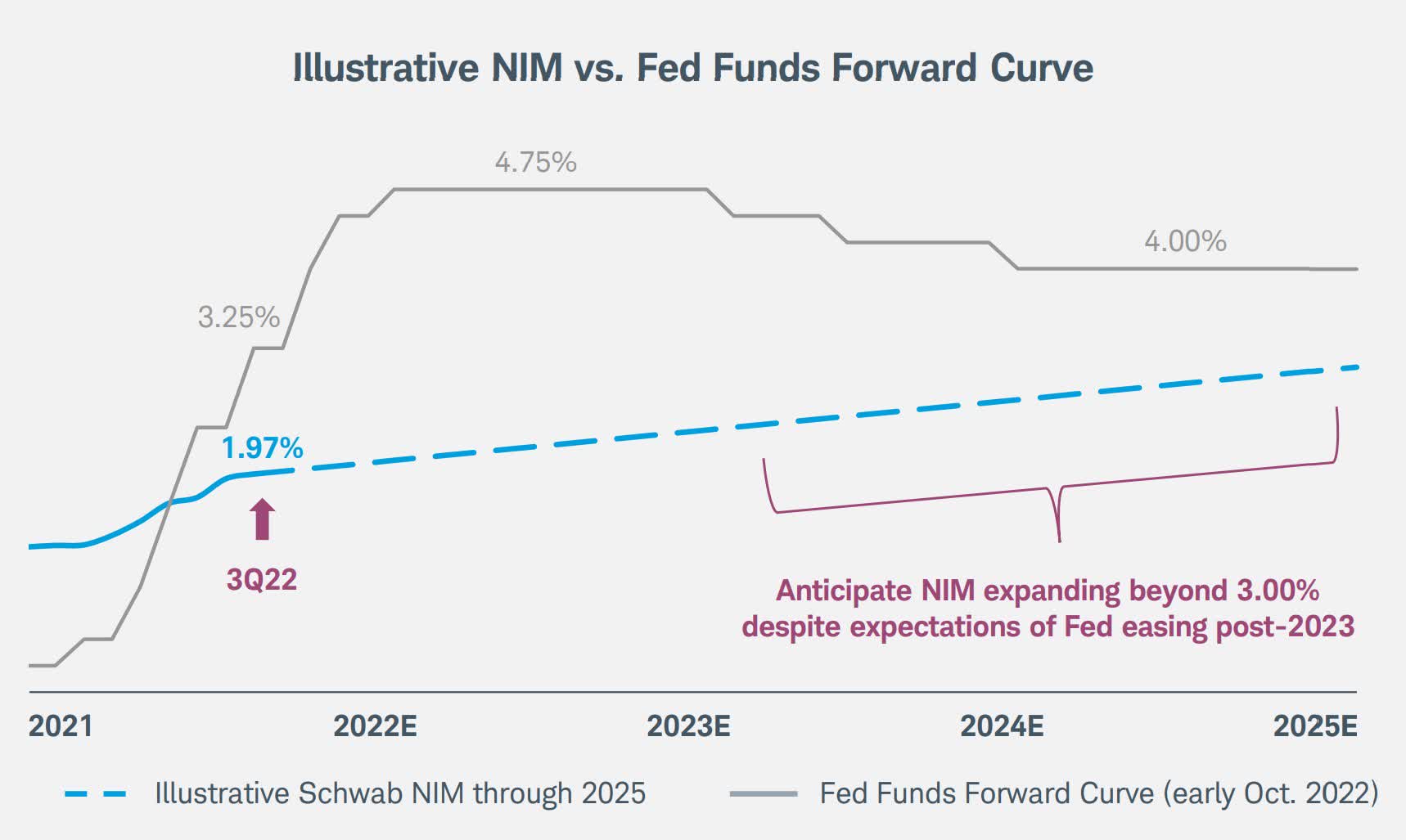

Charles Schwab Fall Business Update Charles Schwab Fall Business Update

NIM is the percent difference between the interest earned from loans or cash investments, and the interest given back to clients or paid on debt. Because the fed’s rates determine rates for loans; treasuries; and other securities, while Schwab controls the interest it gives back, the company can expand this spread to make more money.

While NIM is only at 1.97%, it is playing catch up to the extraordinary pace of rate hikes, an attractive position that leaves a significant runway for growth over the next few fiscal years. NIM could expand another 100 basis points and move upwards of 3.00% despite easing tightening policies that are expected sometime next year.

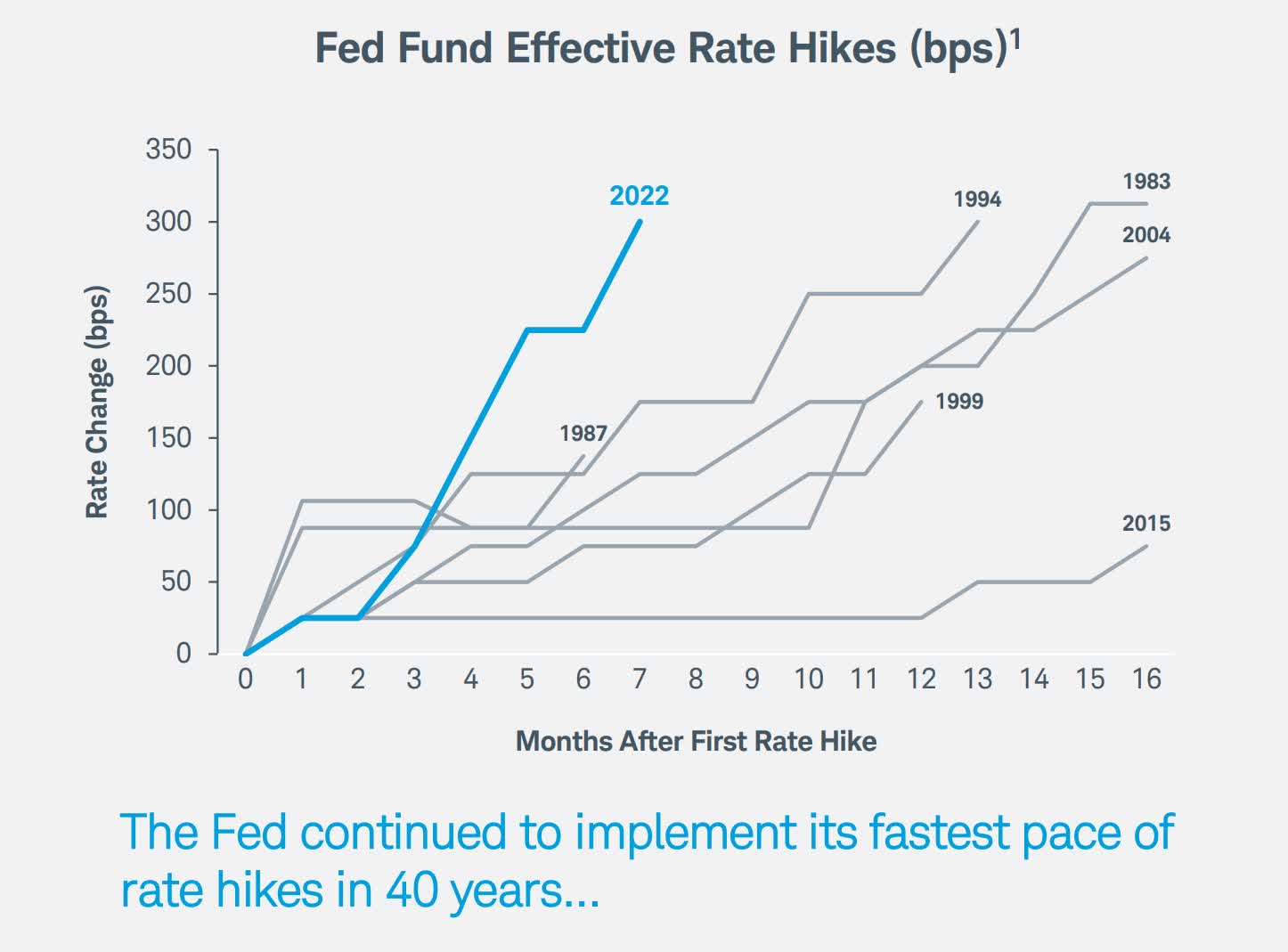

Current fed estimates indicate that rates will be 5.1% next year, 4.1% in 2024, and 3.1% in 2025, all numbers materially higher than any fed funds rate since 2009. The company can leverage a larger spread to boost its average yield by charging more on loans and receivables, supporting our thesis of sustained growth in interest revenue.

Average Interest-Earning Assets

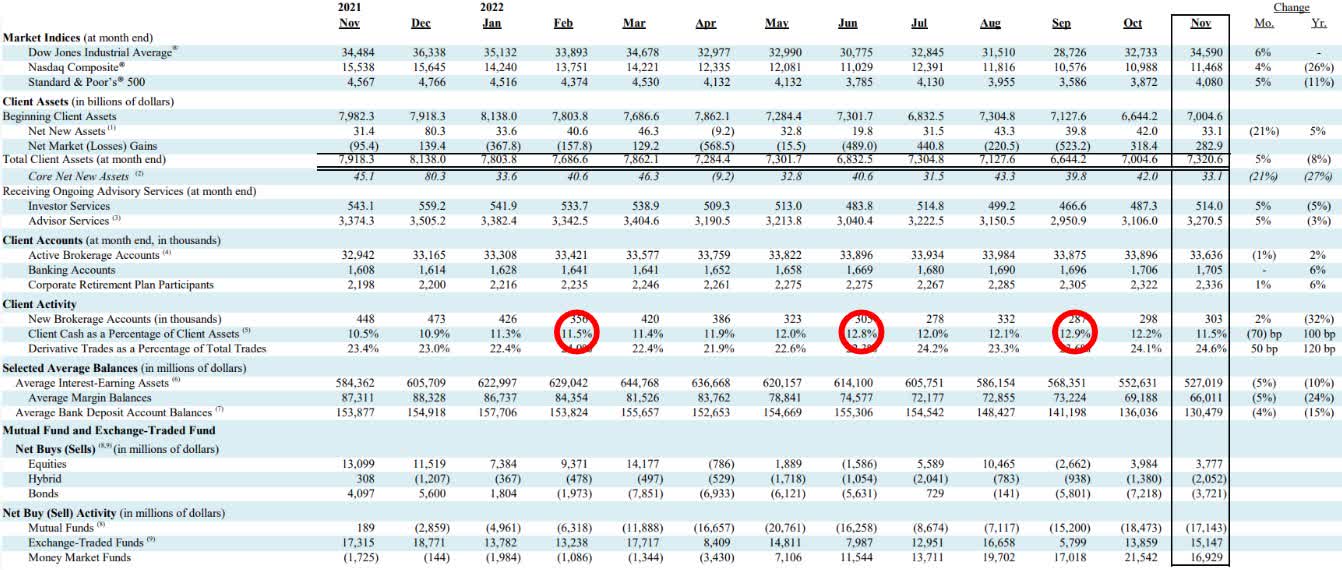

Charles Schwab November Activity Report Author, Yahoo Finance

Average interest-earning assets are assets that Schwab can invest such as client cash inflows and bank account deposits. Schwab said in their Q3 2022 10-Q that:

average interest-earning assets for the third quarter and first nine months of 2022 were higher by 6% and 15%, respectively, compared to the same periods in 2021. These increases were primarily due to growth in bank deposits and payables to brokerage clients, which resulted from net new client asset inflows as well as transfers of BDA balances to our balance sheet in the third quarter of 2021 and the first nine months of 2022

reflecting client confidence in the company, but we believe there is another tailwind at play.

In September, the S&P VIX Index (VIX) jumped above 32, and looking at the company’s November report, client cash hit a high of 12.9%. A similar story is seen in June when the VIX reached 34 and client cash hit a then-high of 12.8% as well as February with a VIX of 36 and client cash of a then-high 11.5%.

Both show that in times of market and economic uncertainty, clients are moving their assets increasingly to cash. With more volatility anticipated in 2023, expect more months like February, June, and September where new highs for “client cash as a percentage of client assets” will be set, leaving more assets for Schwab to invest.

Charles Schwab Fall Business Update

An increase in interest-earning assets combined with improved balance sheet liquidity should help the company’s cash allocation strategy of investing in shorter, risk-appropriate securities that should work well till the end of the recession.

General Banking Growth

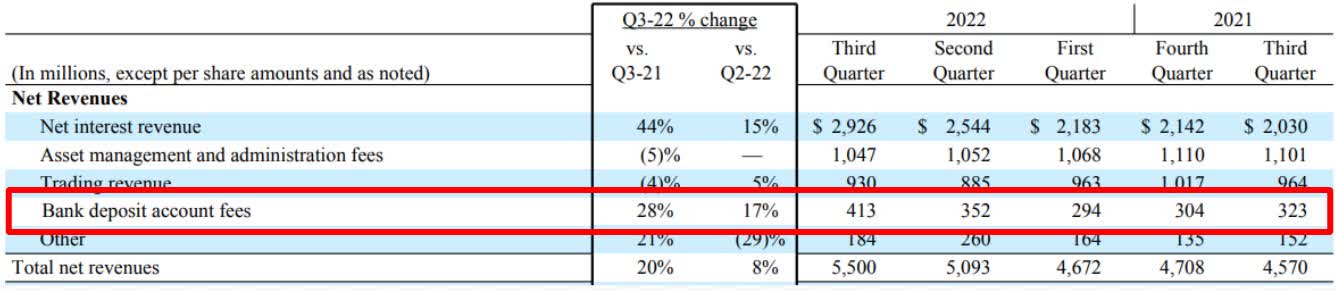

Charles Schwab Q3 2022 Earnings Report

Bank deposit account fee revenues have been impressive, growing 28% in Q3 and 5% in the first 9 months y/y, the second highest of all revenue streams.

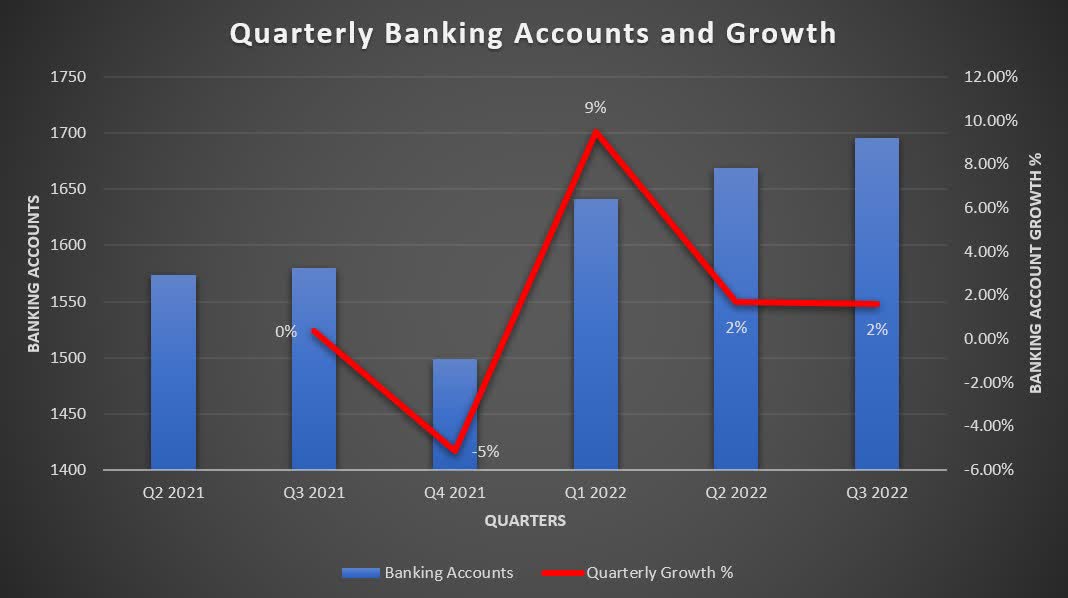

Charles Schwab Q2 and Q3 Earnings Report

Based on the number of banking accounts, Schwab makes profitable $243.51 per account in fees due to higher rates boosting the average net yield they charge clients to keep money with them.

This bodes well as Q3 banking accounts reached their highest total ever, settling into low-single-digit growth after a bumpy 2020 and 2021. There is also continued upside into mid-single-digit growth with an expanding client base through the TD Ameritrade acquisition.

Additionally, we expect this non-interest revenue source to continue to grow due to Schwab’s sticky client base. They target higher net individuals, having an average account balance of $82,253.54, who will choose a company they trust over others, regardless of product offering.

Future Risks

Charles Schwab Q3 2022 10-Q

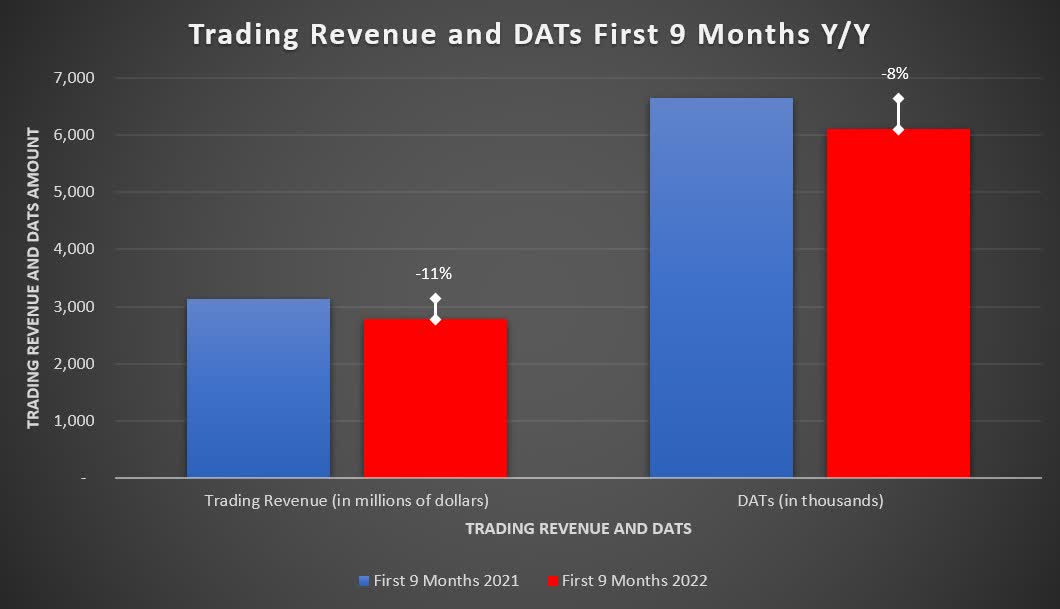

A bearish market down 20% YTD created concern about a drop in trading, however, the segment has been Schwab’s most resilient. Facing tough comps after a record 2021, overall trading revenue and DATs had moderate declines of just 11% and 8%, respectively, in the first 9 months y/y. Revenue per trade declined at a smaller amount of just 4%.

Schwab highlighted in their Q3 2022 10-Q that

the mix of client trading activity toward more ETFs and fewer single stocks, and toward more index options and futures and fewer single stock options, result[ed] in lower commissions and order flow revenue

as both had 13% revenue declines and that

lower client trading activity during the first quarter of 2022 relative to the extraordinary trading volume experienced during the first quarter of 2021, as well as changes in the mix of client trading activity

were also factors in the drawdown.

While we expect more of the same in 2023 due to heightened uncertainty, clients’ continued activity in non-single-stock investment types, especially fixed-income trading which caused principal transaction revenue to grow 121%, can help steady the ship. Moreover, easier future comps against 2022’s numbers provide some optimism against a gloomy market backdrop.

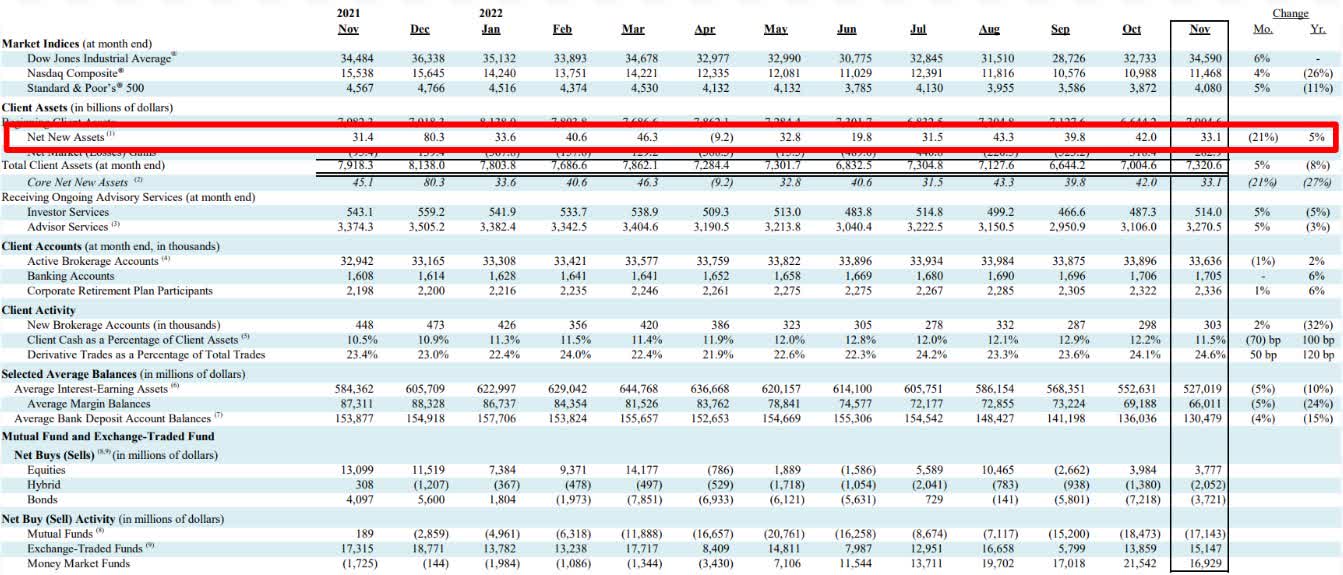

Charles Schwab November 2022 Activity Report

Another concern is that persistent market declines would discourage new asset inflows as total client assets decrease, offsetting potential growth in NIM and the amount of interest-earning assets available.

Schwab’s November report, however, offered some encouraging data to mitigate worries. Net new assets of $33.1B are still 5% higher y/y and above 2022’s average monthly inflow of $32.1B despite deteriorated market and economic conditions. Clients’ increased trust in Schwab during tough times keeps us positive on 2023’s new client asset outlook.

Valuation

Author, Seeking Alpha, Stock Analysis

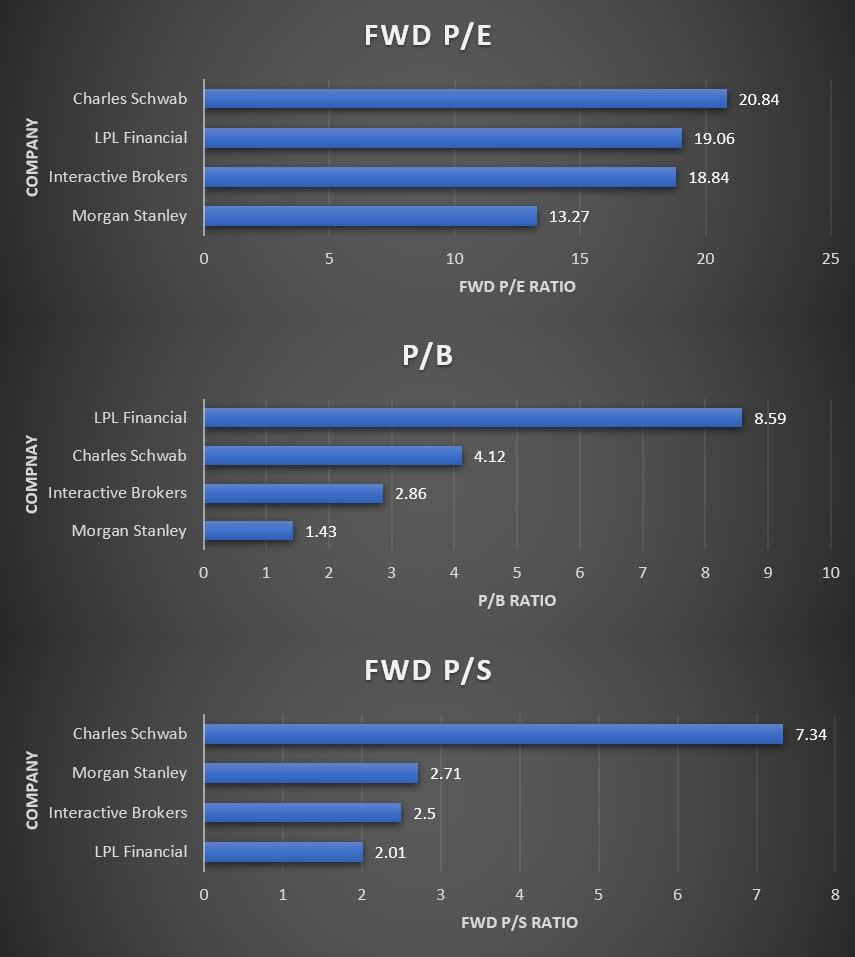

Schwab is richly valued at 20.84x forward earnings, 4.12x book value, and 7.34x forward sales, more expensive than its competitors for most measures. However, these valuations are justified given the higher, consistent revenue and earnings growth that Schwab provides, making us feel comfortable paying up for a higher valuation.

Additionally, Schwab has the best combination of business exposure and revenue diversity as Morgan Stanley (MS) and other big banks are exposed to a slowdown in investment banking; LPL Financial (LPLA) is facing headwinds in advisory assets and fees; and Interactive Brokers (IBKR) and other brokerage firms don’t have a banking or wealth management division to benefit from.

Author, Stock Analysis

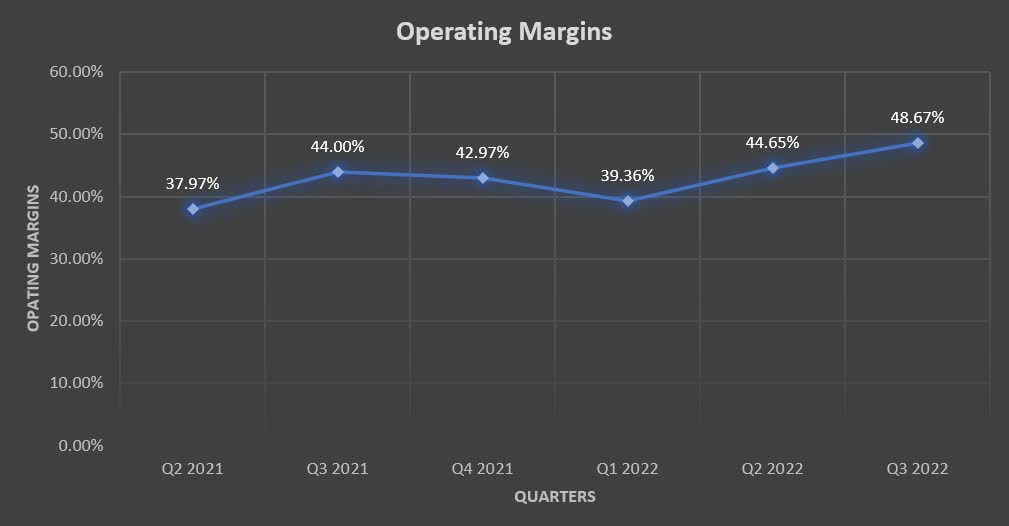

Another point of strength for the company has been operating margins. They grew to 48.67%, the highest since 2019, even with the acquisitions and integration costs of the TD-Ameritrade rising to $2.4-2.5B from an initial $1.8-2.0B due to numerous headwinds noted in their Q3 2022 10-Q including

increased costs resulting from incremental complexity in conversion work, due in part to the replacement of certain vendor resources following Russia’s invasion of Ukraine, as well as overall inflationary pressures.

Rising margins in an inflationary environment show that revenues are outpacing expenses, and while cost pressure will eventually subside, we forecast sustainable revenue growth for the foreseeable future.

Conclusion

The current macroeconomic environment has been a tailwind for The Charles Schwab Corporation as higher rates support growth net interest revenue and their banking division. With fears about trading revenue and client assets overblown, and justifiable valuation following a year of consolidation, The Charles Schwab Corporation stock looks like a portfolio winner for 2023 and beyond. Expect to see more buying opportunities in the 1H of next year, especially as investors misinterpret the Q1 result in January.

Be the first to comment