andresr/E+ via Getty Images

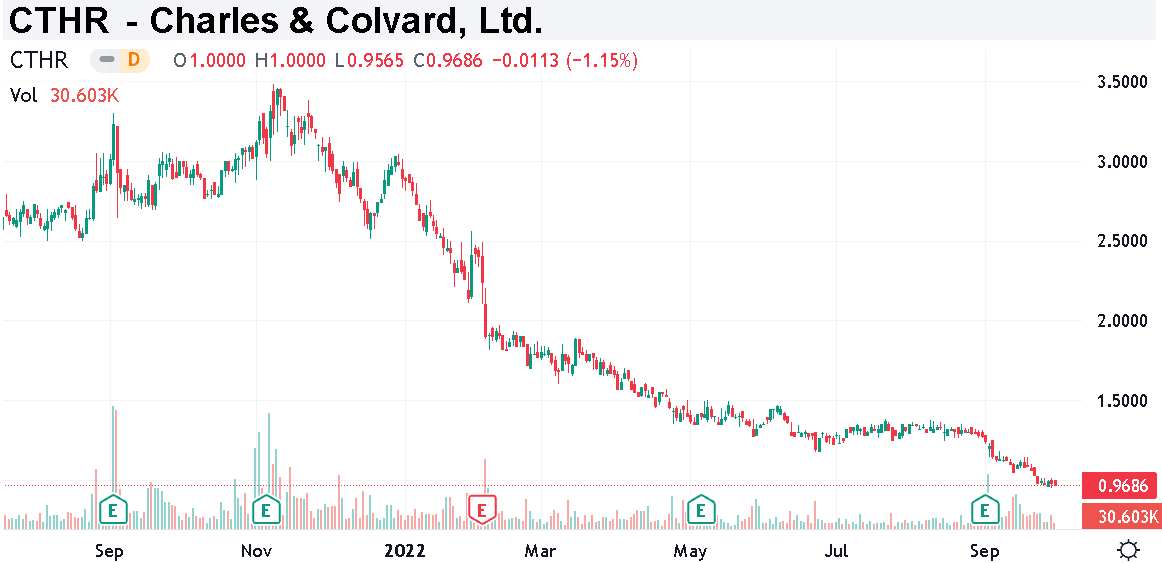

Charles & Colvard (NASDAQ:CTHR) specializes in lab-grown diamonds and moissanite fine jewelry. The “made, not mined” gemstones have gained popularity in recent years as a more affordable alternative to natural diamonds. Indeed, the company has benefited from this trend driving record sales and eight consecutive quarters of profitability. That being said, the trading action in the stock has been terrible with shares losing two-thirds of their value over the past year.

The challenge here considers a reset of expectations compared to some exuberance at the highs in 2021 into the more challenging economic environment and broader market volatility. Recognizing the ongoing macro headwinds, we like the stock which is supported by overall solid fundamentals and a positive long-term outlook.

CTHR Key Metrics

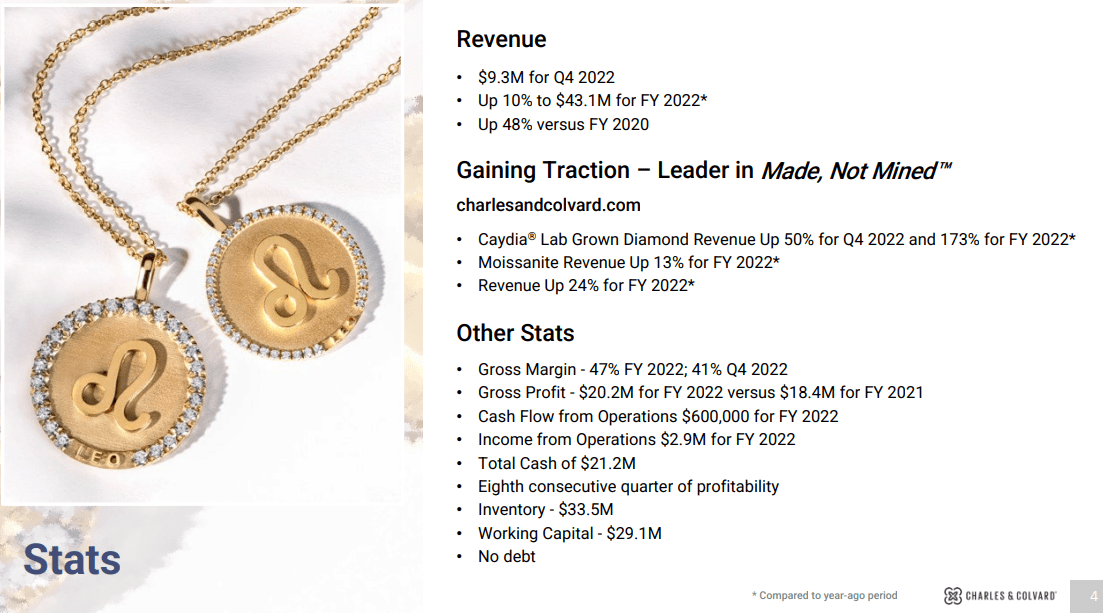

The company last reported its fiscal Q4 earnings in early September with a net income of $41k or EPS of $0.00, which was $0.01 ahead of the consensus. Revenue of $9.3 million was also ahead of estimates although 4% lower than the period last year in the context of a particularly strong quarter for consumer spending in 2021. This impact also resulted in a lower gross margin this quarter at 41% compared to 47% in Q4 fiscal 2021.

The full-year trends painted a more favorable picture with 2022 sales reaching $43.2 million, up 10% over 2021, and also 48% higher over 2020. The full-year gross profit of $20.2 million was also up from $18.4 million in 2021.

source: company IR

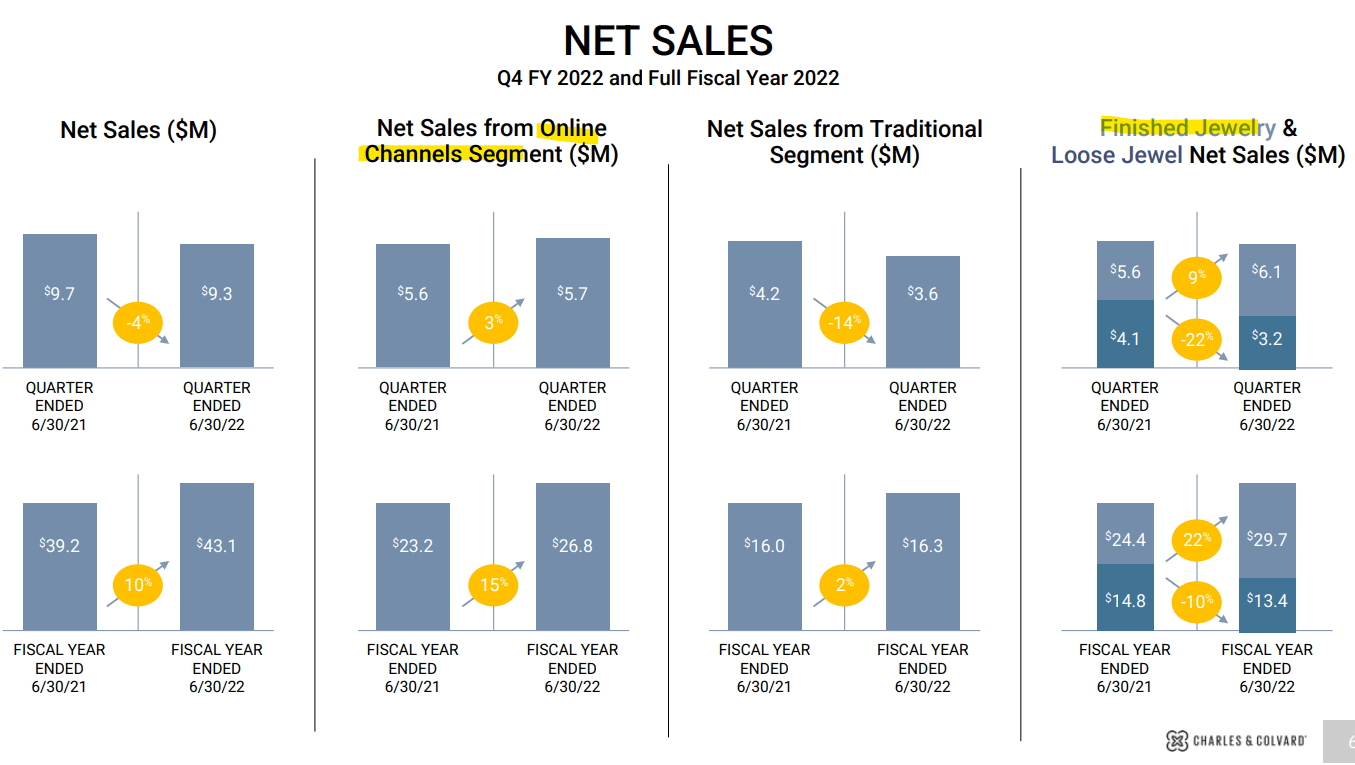

There are two sides to the business across the “Online Channels Segment”, which includes the company-run website, along with the “Traditional Segment” that captures the wholesale business into brick-and-mortar retailers. In this case, the online business has been stronger with 3% y/y sales growth in Q4 while the traditional segment posted a 14% decline.

Within those amounts, management explains that the top line decline is largely related to weakness in “loose jewel” sales which fell by 22% y/y in Q4 reflecting lower demand for the category worldwide as a broader industry trend.

The company intends to focus more on finished jewelry going forward which has been able to sustain momentum with sales up 9% y/y. Ultimately this effort should support higher margins as finished goods add value compared to more commoditized loose diamonds.

source: company IR

The other strong point here is the balance sheet position. Charles & Colvard ended the quarter with $21.2 million in cash and restricted cash against zero long-term debt. In May the company announced a $5 million stock buyback program effect over the next three years. Assuming repurchases of around $1.6 million per year, the implied shareholder yield is 5.5%.

While the company is not providing forward financial guidance, management projected optimism for continued operating momentum during the earnings conference call.

CTHR Stock Price Forecast

One of the most positive factors in its outlook is the data suggesting the market adoption of lab-grown diamonds is climbing. According to the independent industry group, International Gem Society (IGS), lab diamond’s market share of total diamond sales in the U.S. climbed from around 3% in 2020 to 7% by Q1 of this year. Charles & Colvard expects that figure to reach 12% by 2025.

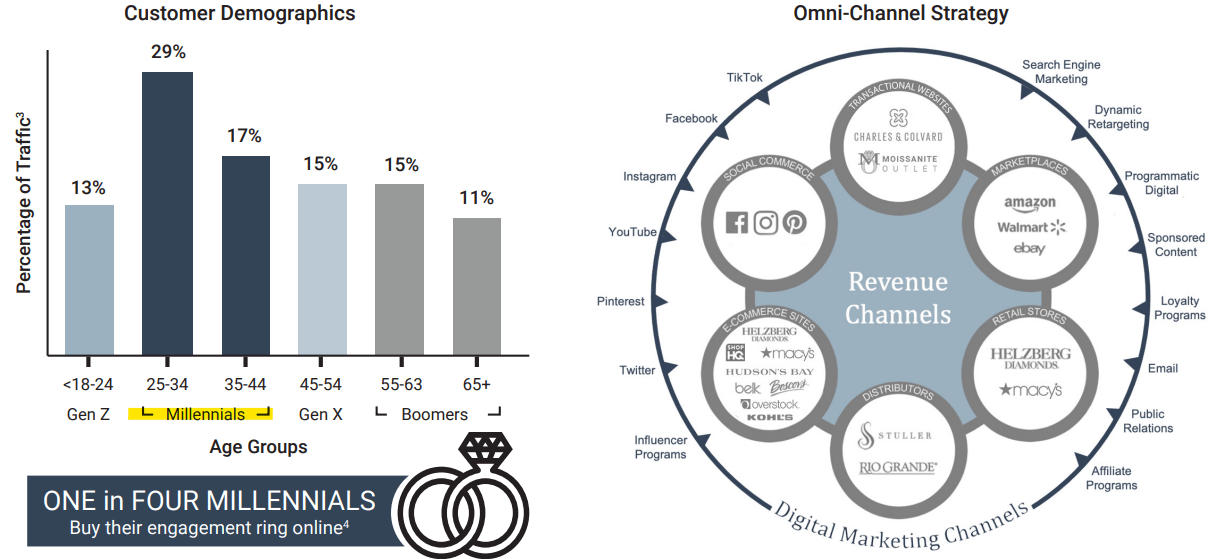

A large part of the growth is coming from the millennial age group between 25 and 44 that have embraced the technology. There is a sense that this group along with younger Gen Z buyers, which together currently represent 59% of total Charles & Colvard customers can support further growth opportunities. The company’s strategy is to reach new customers across various channels including through social media while also partnering with major retailers and fine jewelry store networks for distribution.

source: company IR

All that said, the concern right now explaining much of the weakness in the stock comes down to the economic environment defined by high inflation and rising interest rates. Naturally, an outlook for slowing consumer spending and higher unemployment should pressure demand for discretionary items including fine jewelry.

The other dynamic at play is an understanding that the market for “lab-grown diamonds” and moissanite is competitive with larger peers. 2021 IPO Brilliant Earth Group Inc (BRLT) has a current market share of around 20x larger than CTHR while generating 10x more sales in the past year. There are also several other private-owned players like “Clean Origin” that offer similar types of products with a focus on the socially-conscious and environmentally friendly aspect of made gems.

In other words, the market is contested, and CTHR’s weaker growth in 2022 compared to BRLT explains some of the poor sentiment towards the stock. Still, the argument we have is that the demand for lab grown diamonds has room for multiple players. The attraction of CTHR is its brand recognition and history, particularly with moissanite jewelry. The push towards more direct-to-consumer initiatives while the stock presents relative value.

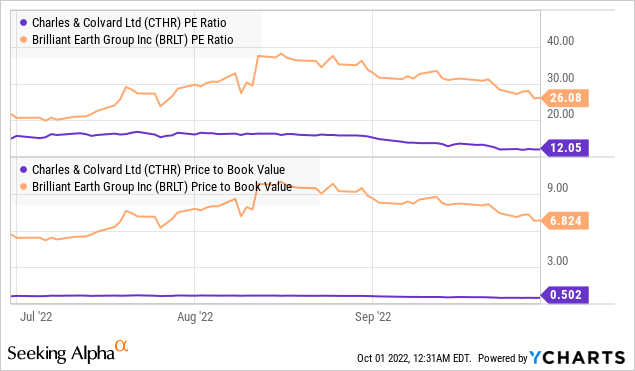

We mentioned CTHR being undervalued and even “cheap” trading at a 12x P/E representing a large discount to BRLT at 26x. The large cash position on the CTHR balance sheet also leads to a current price to book value for the stock at 0.5x, a fraction of BRLT at 7x, which in our view, makes it too cheap to ignore.

It simply appears the market is pricing in a deteriorating of the company’s financials going forward, with an expectation that sales decline further and losses accelerate. We’re a bit more optimistic, focusing on the strength in online sales and finished jewelry segments that continue to be growth drivers. There is also a case to be made that even in a scenario where the economy weakens further, the affordability aspect of lab-grown jewelry relative to natural diamonds keeps sales supported.

Seeking Alpha

Final Thoughts

Despite the market cap of just $30 million and even lower enterprise value at $18 million, our take is that CTHR is more than just another “penny stock”. The long-term growth history, the solid balance sheet, and the underlying tailwinds for lab-grown diamonds and gemstones keep this stock interesting.

The bullish case for Charles & Colvard is that sales growth can re-accelerate supporting stronger earnings momentum. It will likely take a few quarters of positive financial and operating trends for shares to sustain a major reversal higher in the stock. CTHR is speculative, but the allure here is the potential that the stock reclaims its levels from Q2, above $1.50 per share representing more than 50% upside from the current level.

It’s fair to assume the stock will remain volatile in a more uncertain operating environment through 2023. The main risk to consider is that sharply lower sales going forward requires a strategy pivot and begins to impact cash flow trends. Disappointing results through the rest of the year can open the door for more downside in the stock.

Be the first to comment