Bill Pugliano

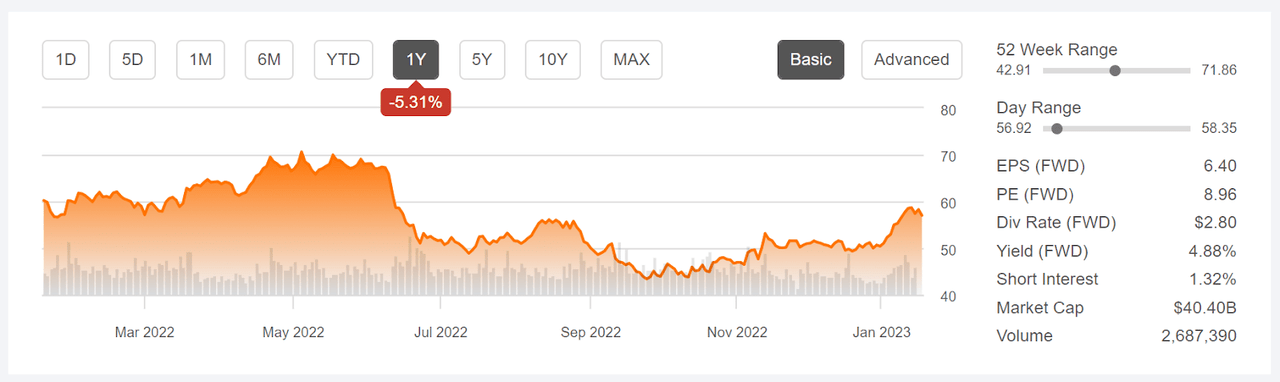

Shares of Dow Inc. (NYSE:DOW) were pummeled in mid-2022 on fears that increasing interest rates would send the economy into recession and curtail demand for industrial products. Dow fell 38.5% from the 2022 high closing price of $70.61 on May 4 to a 12-month low closing price of $43.39 on September 26, a period of about five months. After steadily rising from the 12-month low, the shares have rallied over the past month, rising 12.6%. Bank of America recently upgraded Dow from underperform to neutral, citing what appears to be rising confidence in better-than-expected economic conditions. Dow reports Q4 results on January 26.

Seeking Alpha

12-Month price history and basic statistics for DOW (Source: Seeking Alpha)

Dow’s earnings recovered rapidly following the pandemic-driven economic slowdown, and substantially outperformed expectations in 2021 and through Q2 of 2022, even though EPS was on a downward trend. Q3 earnings were lower than in any of the past six quarters. The expected earnings for Q4 are lower than the realized earnings for any quarter since Q3 of 2020, in the midst of the pandemic. The longer-term earnings outlook is weak, with a consensus EPS growth rate of 3.85% per year over the next three to five years.

ETrade

Trailing (4 years) and estimated future quarterly EPS for DOW. Green (red) values are amounts by which the EPS beat (missed) the consensus expected value (Source: ETrade)

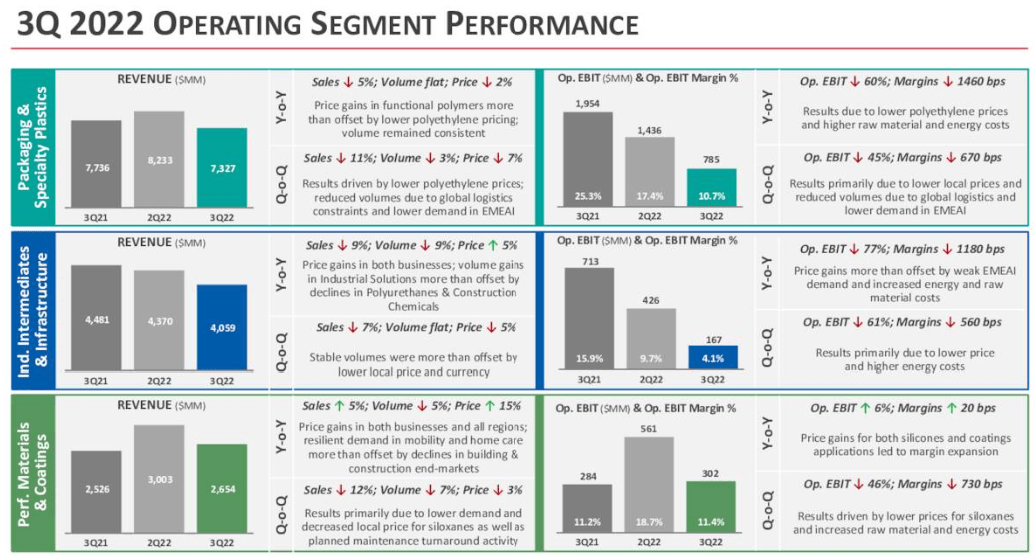

Dow’s revenue and earnings have been under stress from several factors. The Packaging and Specialty Plastics segment has suffered from lower prices for polyethylene, supply chain issues, and lower demand outside of the U.S. For Industrial Intermediates and Infrastructure, sales are down 9% YoY and the decline in volumes has only been partially mitigated by higher prices. In Performance Materials and Coatings, revenues and EBIT rose slightly YoY. The strong dollar has been a headwind for the full year. In addition, higher energy costs and commodity price inflation have reduced earnings.

Dow Inc.

Dow’s revenue and earnings on its 3 business segments in Q3 (Source: Dow)

Dow’s 4.78% forward yield provides some compensation for low growth expectations. The quarterly dividend has been constant at $0.70 per share since 2019, when Dow separated from DowDuPont.

I last wrote about Dow on August 30, 2022, about 4 ½ months ago, when I changed my rating from a buy to a hold, but suggested that a covered call strategy looked attractive, given Dow’s high yield and other properties. At the time of this post, the forward P/E was 6.7 and the forward dividend yield was 5.2%. The Q2 earnings, reported on July 21, were quite high and exceeded expectations. The Wall Street consensus rating was a hold, but the consensus 12-month price target, as calculated by Seeking Alpha, was 13.6% above the share price at that time, for an expected total return of 18.8% over the next year. I also considered the market-implied outlook, a probabilistic price forecast that represents the consensus view from the options market. The market-implied outlook for Dow was slightly bullish to January 20, 2023 (an options expiration date) and neutral with a bullish tilt to June 16, 2023 (another option expiration date). The expected volatility calculated from the market-implied outlook was 33.8% (annualized). As a rule of thumb for a buy rating, I look for an expected 12-month total return that is at least half the expected volatility. Taking the Wall Street consensus price target at face value, Dow met this criterion. With the consensus hold rating from Wall Street and the neutral-to-slightly-bullish results from the market-implied outlook to the middle of 2023, along with growing consensus on a 2023 recession, I downgraded Dow to a hold. In the period since this post, Dow has returned a total of 12.8%.

Seeking Alpha

Previous post on DOW and subsequent performance vs. the S&P 500 (Source: Seeking Alpha)

I also noted that “With the consistent expected volatility calculated from options prices and the high dividend yield, selling covered calls against a long position in DOW continues to look favorable.” By way of example, I noted that one could buy Dow at $51.91 and sell a call option with a strike price of $52.5, expiring on June 16, 2023, for $5.35. With the dividends that were expected over this 9.5-month period, the expected total income was 14.2% (the sum of the option premium and the dividends). Today, this call option is worth $2.06 (the midpoint of the bid and ask price) and Dow is trading at $58.68. The net position (long Dow/short call) has gained $0.59 (the price appreciation from $51.91 to $52.50) plus $3.29 (the difference between the price at which the options were sold ($5.35) and the current market value ($2.06)) plus the dividends received ($0.70), for a total of $4.58, a return of 8.8% ($4.58/$51.91).

For readers who are unfamiliar with the market-implied outlook, a brief explanation is needed. The price of an option on a stock reflects the market’s consensus estimate of the probability that the stock price will rise above (call option) or fall below (put option) a specific level (the option strike price) between now and when the option expires. By analyzing the prices of call and put options at a range of strike prices, all with the same expiration date, it’s possible to calculate the probable price forecast that reconciles the options prices. This is the market-implied outlook. For a deeper discussion than is provided here and in the previous link, I recommend this outstanding monograph published by the CFA Institute.

I have calculated updated market-implied outlooks for Dow and compared these with the current Wall Street consensus outlook in revisiting my rating as we approach the Q4 earnings report on January 26.

Wall Street Consensus Outlook for Dow

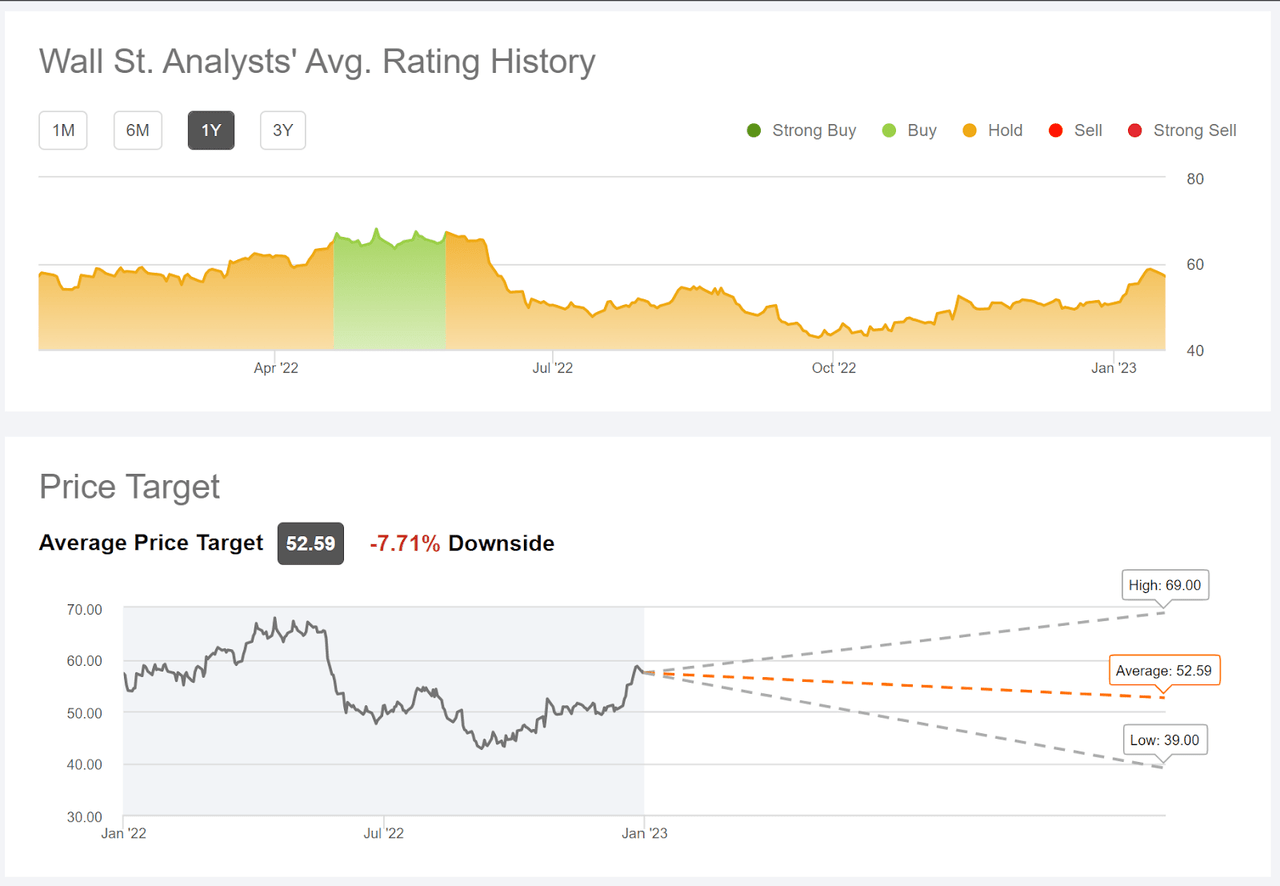

Seeking Alpha calculates the Wall Street consensus outlook for Dow by combining the views of 24 analysts who have published ratings and price targets over the past 90 days. The consensus rating continues to be a buy and the consensus 12-month price target is $52.59, 7.7% below the current share price. At the end of August, for my last post on Dow, the consensus price target was $58.53. The target price has fallen as the share price increased by 11.3%.

Seeking Alpha

Wall Street consensus rating and 12-month price target for DOW (Source: Seeking Alpha)

While the consensus rating for Dow is the same as it was at the end of August, the expected return implied by the consensus price target has changed dramatically. As of August 30, the consensus 12-month price target was 13.6% above the prevailing share price, as compared to the current consensus price target which is 7.7% below the current share price.

Market-Implied Outlook for Dow

I have calculated the market-implied outlook for Dow for the 4.9-month period from now until June 16, 2023, and for the 12-month period from now until January 19, 2024, using the prices of call and put options that expire on these dates. I selected these specific expiration dates to provide a view to the middle of 2023 and through the entire year.

The standard presentation of the market-implied outlook is a probability distribution of price return, with probability on the vertical axis and return on the horizontal.

Geoff Considine

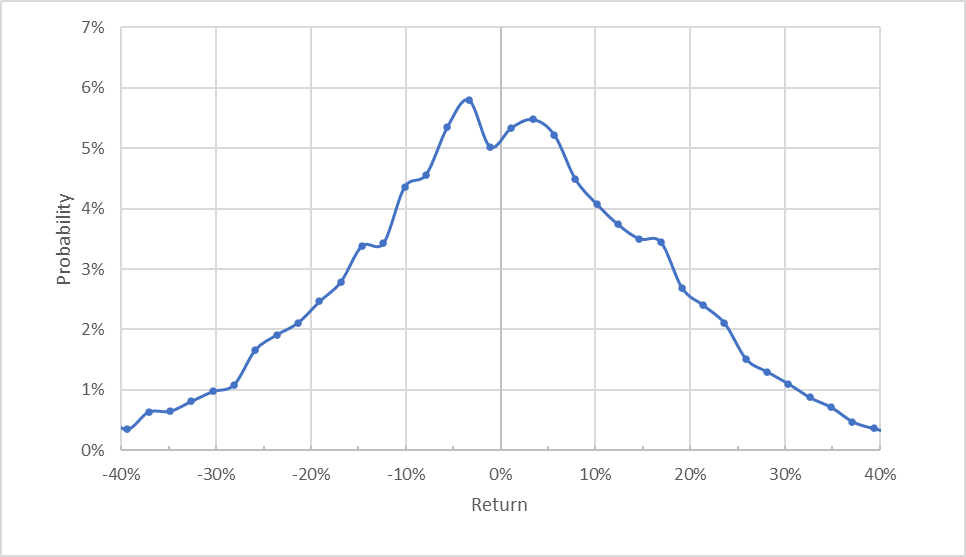

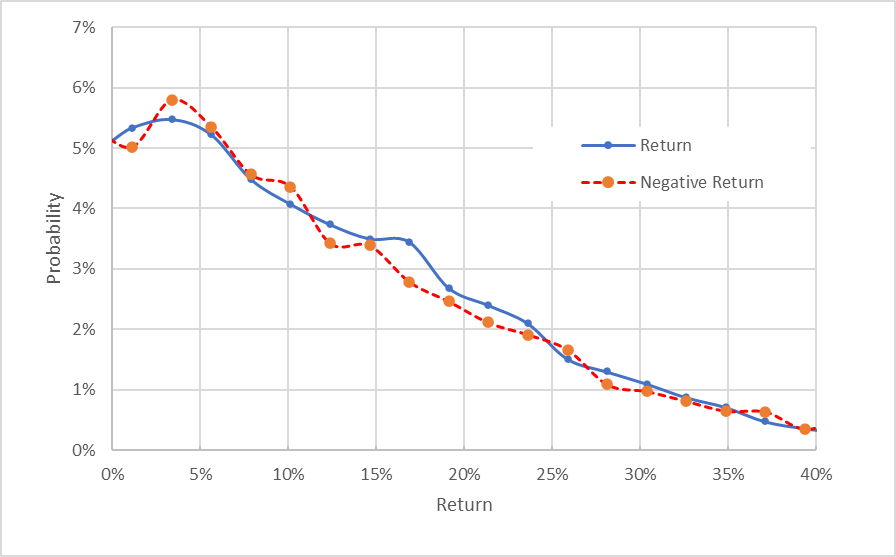

Market-implied price return probabilities for DOW for the 4.9-month period from now until June 16, 2023 (Source: Author’s calculations using options quotes from ETrade)

The market-implied outlook to June 16, 2023 is generally symmetric, with comparable probabilities of positive and negative returns, but the peak in probability is tilted to favor negative returns. The maximum probability corresponds to a price return of -3.4%. The expected volatility calculated from this distribution is 28.7% (annualized), slightly lower than at the end of August.

To make it easier to compare the relative probabilities of positive and negative returns, I rotate the negative return side of the distribution about the vertical axis (see chart below).

Geoff Considine

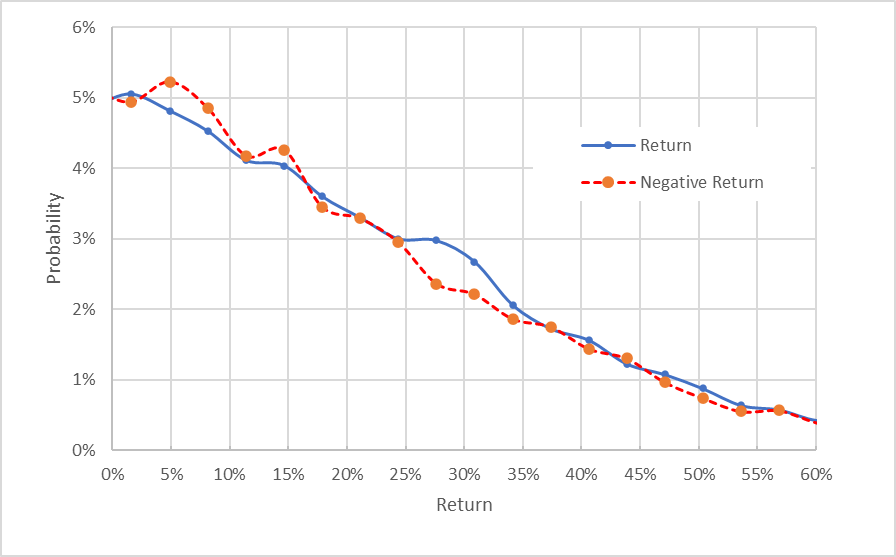

Market-implied price return probabilities for DOW for the 4.9-month period from now until June 16, 2023. The negative return side of the distribution has been rotated about the vertical axis (Source: Author’s calculations using options quotes from ETrade)

This view shows that the probabilities of positive and negative returns match quite closely, with some variability. There’s no obvious tilt in probabilities that would indicate a directional view from the options market.

Theory indicates that the market-implied outlook is expected to have a negative bias because investors, in aggregate, are risk averse and thus tend to pay more than the fair value for downside protection. There’s no way to measure the magnitude of this bias, or whether it’s even present, however. The expectation of a negative bias suggests an interpretation of this outlook as very slightly bullish.

The market-implied outlook for the 12-month period to January 19, 2024, also exhibits a close match between the probabilities of positive and negative returns. The expected volatility calculated from this distribution is 29.8% (annualized). Again, the most sensible interpretation of this market-implied outlook is slightly bullish because of the expected negative bias.

Geoff Considine

Market-implied price return probabilities for DOW for the 12-month period from now until January 19, 2024. The negative return side of the distribution has been rotated about the vertical axis (Source: Author’s calculations using options quotes from ETrade)

With a prevailing share price of $58.07 today, you can sell a call option expiring on January 19, 2024, with a strike of $60 for $5.60. Between now and January 19, 2024, we can expect $2.80 in dividends. The sum of the option premium and the dividends provides a total income yield of 14.5% over the next 12 months. Given the expected volatility of 29.8% for this period, 14.5% in total income is quite attractive.

Summary

Dow’s earnings have been falling due to several factors beyond the company’s influence. High energy prices, slowing growth, rising interest rates, and the potential for a recession in 2023 have all constrained the company’s performance. This is, of course, typical for a company in a cyclical industry such as chemicals. The consensus outlook for earnings is not encouraging. The Wall Street consensus rating for Dow continues to be a hold, but the combination of a rising share price and a falling price target has resulted in an expected total return of -2.9% over the next year. The market-implied outlook for Dow has a slight bullish tilt to the middle of 2023 and into January 2024, with expected volatility of about 30%. As we approach Q4 results, it is hard to see a lot of near-term positives. I am maintaining a neutral rating on Dow although I continue to view a covered call strategy as attractive.

Be the first to comment