No near-term substitute for coking coal in steelmaking

shank_ali

Peter Epstein of Epstein Research [ER] has no prior or existing relationship with any person or company mentioned in this interview. Mr. Epstein owns shares in Colonial Coal

In my view, rarely has there been such a disconnect between what some shareholders believe a Company’s assets are worth and its market value!

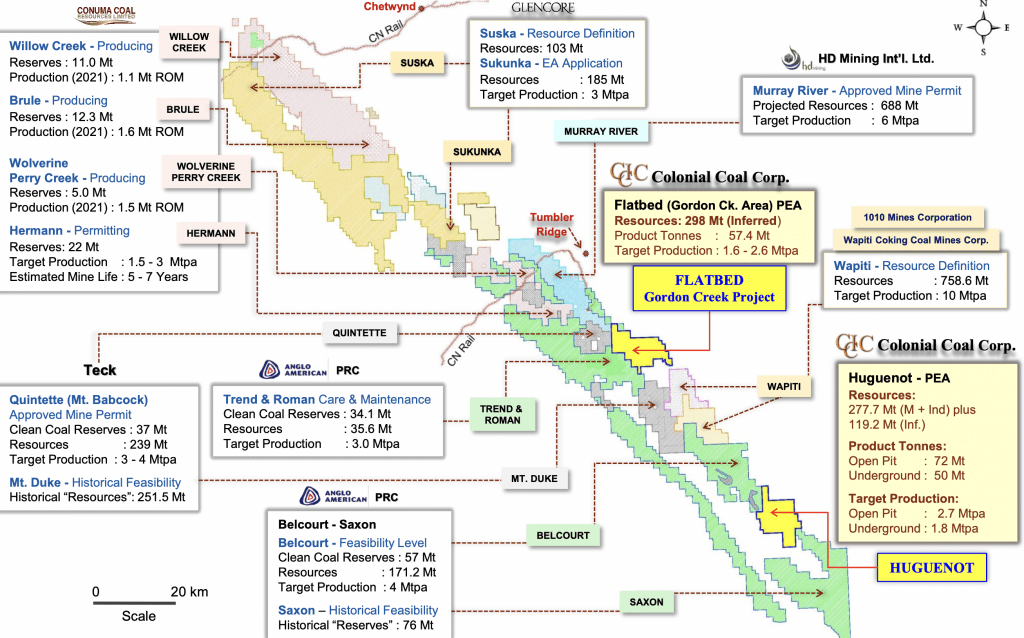

Shareholders of Colonial Coal (OTCPK:CCARF) (TSXV:CAD:CA) think its two PEA-stage coking coal projects in B.C., Canada, surrounded by hugely profitable operations owned by Anglo American (OTCQX:AAUKF) & Teck Resources (NYSE:TECK), are worth up to US$2 or more/resource tonne in the ground, but the market is says otherwise valuing the resources at US$0.245/t.

factual calculations on range of sale scenarios

Please review my last article for more detail on the Company and the ongoing sale process. The investment-bank led process began around the same time as COVID-19. Detractors consider it a red flag that it’s been nearly four years and still no bids.

It’s possible that groupthink has set in and stakeholder expectations are too high… And, it’s possible that management is largely on track, (albeit the process is moving quite slowly) and investor fatigue has taken over. I lean firmly towards the later scenario.

Management says that COVID was a major constraint on dealmaking. Each time the Company’s or a bidder’s advisor, banker, lawyer, consultant, executive or board member was sidelined, the process slowed to a crawl.

Entire countries were off limits for extended periods, most notably Canada, China & India, not necessarily at the same times. Without key suitors from those countries, calling for bids to kickstart a transaction might have resulted in a muted response.

Over the past week I asked Chairman & CEO David Austin why his team remains excited about the prospects to sell Colonial’s projects at a favorable valuation.

He pointed out that his board’s fiduciary responsibility is to maximize the value received, not merely to liquidate the assets. If that means waiting longer than some investors might like to get an extra US$0.25/t, (~C$1.20/shr.) the board remains willing to do that.

Coking coal futures price of 2,517.5 Chinese yuan per tonne = US$372/t…

investing.com

Q&A with CEO David Austin of Colonial Coal…

[ER] David, thank you for your time. Why is it taking so long to monetize Colonial’s two assets. How big a factor has COVID-19 been?

[DA] COVID-19 has been a huge factor. Dozens of international companies, lawyers, executives, consultants, financial advisers, bankers, consultants – and state-owned / affiliated parties – are involved in this unwieldy process.

Each time the process was bogged down, it took time to reschedule travel & meetings and to regain focus. The good news is that COVID seems mostly behind us. Canada lifted all remaining restrictions back in October and China is reopening, notice the copper price – it’s up +28% in the past three months.

Aside from COVID, please remember, we’re working on a complex deal in which suitors do a lot of due diligence. Giant steel & coal companies, especially state-owned/controlled entities, don’t move fast in the best of times.

[ER]– I accept that COVID was a major hinderance to the sale process, but now that it’s largely behind us (from a business point of view), I hope to see the first bid in the next several months!

[ER] How many potential bidders are at the table? Can you characterize them by country of origin, and/or type of operation?

[DA] We have over a dozen active NDAs in place. Prospective buyers are mostly from Canada, China, India, the U.S. & Australia. Japanese & Korean groups are on the sidelines, but they know our coal, we think they might still jump in.

Asian steelmakers have most of their existing & planned blast furnaces near ocean ports, making them highly reliant on the seaborne market. Transporting massive quantities of coking coal thousands of km by rail is an economic, environmental & logistical nightmare.

corporate presentation

Regarding interested parties; mostly steelmakers & coal companies. One or perhaps a few commodity traders, no investment funds. We’re talking with major companies that can easily afford to acquire our projects.

[ER]– CEO Austin and his team, investment bankers & advisors don’t think that Chinese groups will be excluded from bidding. However, I consider that a risk factor. Without Chinese bidders, competitive tension would be diminished.

[ER] Should shareholders be concerned about the blocking of Glencore’s Sukunka coking coal project located nearby Colonial’s projects?

[DA] Good question. Investors are concerned, in fact probably more concerned than prospective bidders, who know a lot about Sukunka and the other projects / mines / companies in the Peace River Coalfield.

Prospective suitors do considerable due diligence, including speaking with provincial & federal gov’t agencies about permitting steps & environmental requirements.

Gov’t commentary accompanying the Sukunka decision clearly stated that it was a project-specific action, completely unrelated to other proposed mining projects in the province. It’s worth noting that the project that privately-owned Conuma Resources just acquired is closer to Sukunka than our projects are.

Make no mistake, the issues in the Sukunka decision have been openly discussed for years with potential suitors, there’s information on those topics in our digital data room. Despite the headlines, we have many interested parties!

Giant steel & coal companies do business all over the world and face challenges wherever they look. I would argue that western Canada is not as risky as pursuing coking coal resources in Mozambique, Mongolia or Russia.

[ER]– CEO Austin seems to suggest that shareholders shouldn’t be worried about the Glencore news, but they are. Perhaps only a serious bid from a prospective suitor would alleviate this uncertainty.

Both CEO Austin & COOPerryhave agreed to remain available in meaningful ways for 2-3 years after a sale closes to help the successful bidder with ongoing First Nations relations, permitting, environmental studies, etc.

corporate presentation

As I mentioned, days before the Glencore news, Teck sold a non-core asset to Conuma, showing that coking coal deals in B.C. can and do happen.

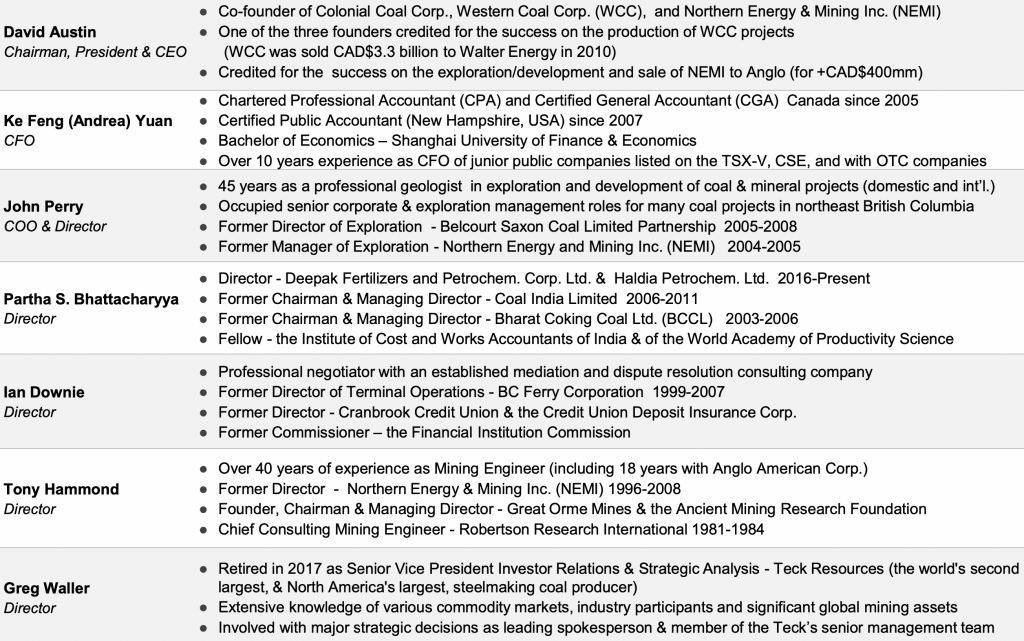

[ER] To the extent that shareholders have contact with Colonial, it’s generally through you. Please tell us about other key team members.

[DA] Colonial has a strong team and we remain confident in our investment bankers. Most investors only have access to me, but that’s by design. We simply can’t talk that much about the sale process and don’t want to risk sending mixed messages.

[ER]Mr. Austin spent considerable time talking about the strength of his team, but in the interest of brevity, please see their bios in the image below.

[ER] Teck sold its past-producing Quintette coking coal project to Conuma. Is there a read-through valuation on this transaction?

[DA] Yes, C$120M = ~US$90M was paid upfront for 274M tonnes of Measured, Indicated & Inferred resources. Conuma is assuming perhaps a couple hundred million dollars in mine reclamation (and other) obligations, as the mine operated for 18 years. Assuming that figure is US$100M, that bumps the price paid to US$0.69/t.

corporate presentation

Conuma agreed to pay Teck a 25% Net Profit Interest (“NPI“) royalty. Assuming a coking coal price of US$220/t, and 12-15 year mine life, 25% of the net present value of that mine is worth well into the hundreds of millions.

Therefore, we believe the total price paid for Quintette’s resources, obligations and ongoing NPI is at least US$3.00/t.

[ER]25% of the NPV(7%) of a 12-yr. mine, ramping up to 4M tonnes/yr., would be ~US650M (on US$220/t coking coal, US$85/t profit & US$30M in start-up costs]). Adding US$650M to the assumed obligations + upfront payment suggests Conuma is paying ~US$3.06/t.

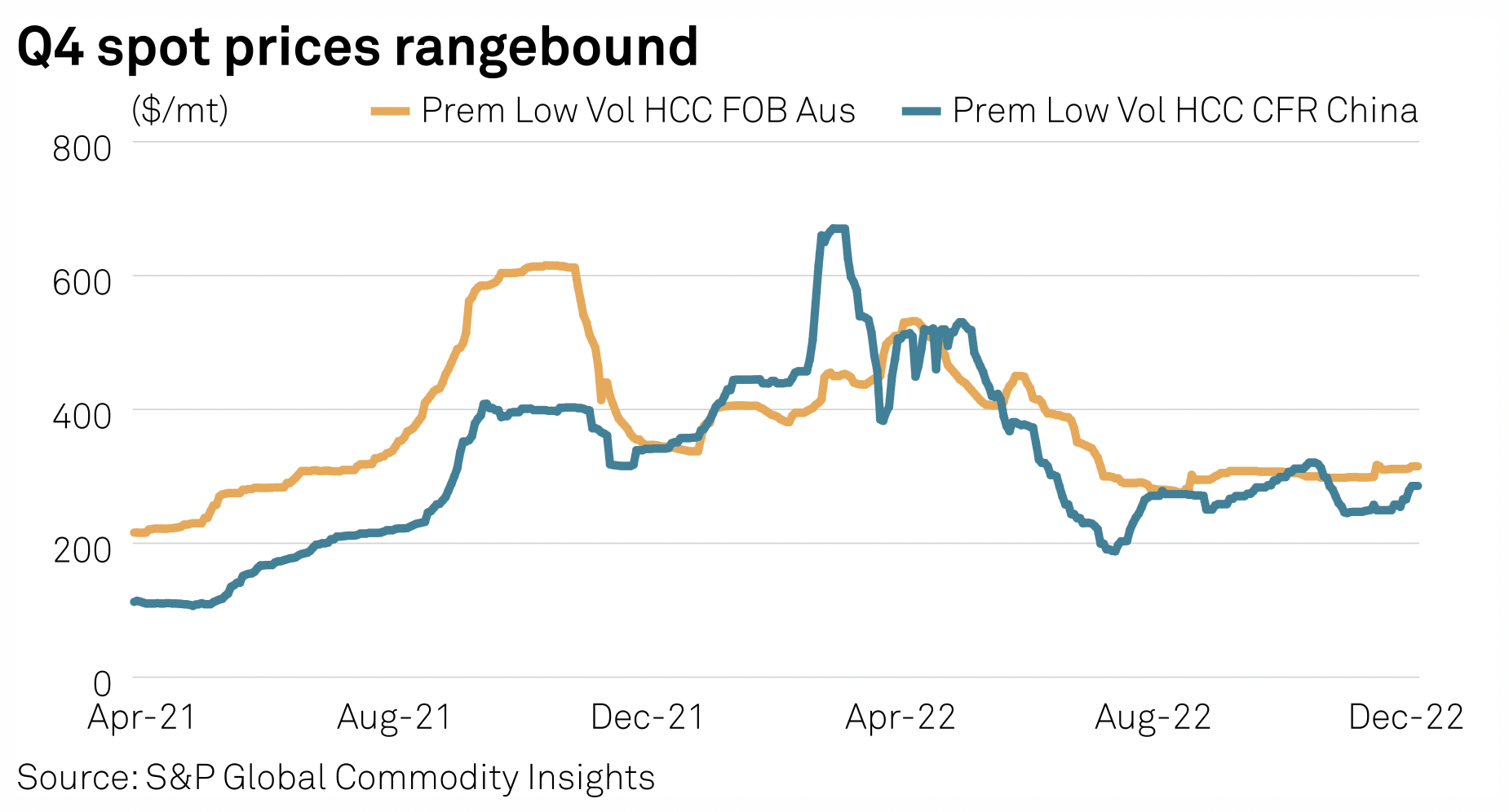

[DA] We believe our coking coal would sell at Australia premium-hard coking coal index Peak Downs(minus US$5-$10/t). In other worlds, world-class assets. According to Argus, premium-hard coking coal has rallied +68% to $315/t fob Australia on Jan. 6th from $187/t on Aug. 1st.

[ER]The true valuation is not cut & dry b/c the public does not know how large the assumed long-term liability figure is. Various commentators have offered their opinion based on a 18-yr. mining operation that the number could be in the C$100’s of millions.

S&P Global Commodity Insights 1/12/23

Also, Conuma is acquiring 274M tonnes, the vast majority are only amenable to underground mining, but the plan is for an open pit operation. The value of the 25% NPI hinges on how many years Conuma (or a successor) operates the new mine.

Will an underground mine be opened after the open pit mine shuts down? If so, the NPI is worth even more to Teck as it would presumably keep collecting on the 25% NPI.

[ER] Your team obviously has a high opinion of B.C.’s Peace River Coalfield. Can’t steelmakers go elsewhere?

[DA] No, there simply are not that many places that can deliver tens of millions of tonnes, year after year, of premium quality coking coal. The list is short, Australia, Canada & the U.S. Mongolia? Landlocked, Mozambique? Quality & logistical issues. Indonesia? Low-grade.

Australia is by far the largest exporter of top-quality coking coal, but is facing more frequent flooding, labor shortages, shrinking cap-ex (due to ESG concerns) & rail bottlenecks.

corporate presentation

[ER] Thanks again David for your valuable insights. Any final thoughts?

[DA] Thank you Peter. My team remains optimistic that we can sell one or both (preferably both at the same time) of our premium coking coal projects at an attractive level. We continue to see an uptick in activity from prospective bidders.

We recognize that the process is taking a long time, but we note that seaborne coking coal fundamentals for top-tier products are as strong as ever and securing long-term coking coal from safe, prolific jurisdictions is getting more difficult.

[ER] My key takeaways from this interview:

Unless CEO Austin is lying, the risk/reward of an investment in Colonial Coal seems compelling. Even if shareholders, management, investment bankers & other stakeholders are very wrong about the assets being worth US$2.50/t or US$2,00/t or US$1.50/t or US$1.00/t — even if the assets are worth US$0.50/t — that equates to twice the current share price. So, in my view there’s a healthy margin for error.

Assuming it’s true that Colonial Coal remains in active discussions with over a dozen potential bidders, even after the negative headline of the Glencore news on Sukunka, is comforting to me.

Moreover, the fact that the companies in the data room are mostly giant steel & coal companies with multi-billion dollar valuations is supportive of an eventual transaction taking place.

Possible under-appreciated risks:

1) It’s quite possible that bullish shareholders like myself are missing important red flags, caught in a confirmation bias loop.

2) The stock could be halted for weeks (or longer) upon bid(s) on the assets, and, the stock could be halted multiple times.

3) The winning bidder might pay in shares, not cash. Some investors might have trouble (long delays, broker problems) getting shares free-to-trade.

4) If we enter a meaningful global recession, that could delay the sale process indefinitely. Who knows what the coking coal market might look like coming out of a global slowdown?

5) There’s a chance that Chinese bidders a) might officially or unofficially not be allowed to bid, or b) might not feel welcomed to bid, so they stay away.

6) Although perceived to be less likely, it’s possible Indian groups might not be allowed to bid, or they deem the risk too high and stay away.

7) Daily trading volume is quite poor. Many investors are effectively stuck in the position as liquidity to exit is not available (especially for larger holders).

8) The longer shareholders wait for a favorable outcome, the more likely the chances of an unfavorable outcome, including from a risk not mentioned herein.

9) Some bidders might think – rightly or wrongly – that they can hold out of a long time to make Colonial Coal sell one or both projects at a lower valuation.

10) Some bidders might believe – rightly or wrongly – that lower coking coal prices are on the horizon, presumably leading to a lower sale price for Colonial’s projects.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment