Bill Oxford/iStock via Getty Images

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on March 29th.

REIT Rankings: Cell Towers

Hoya Capital

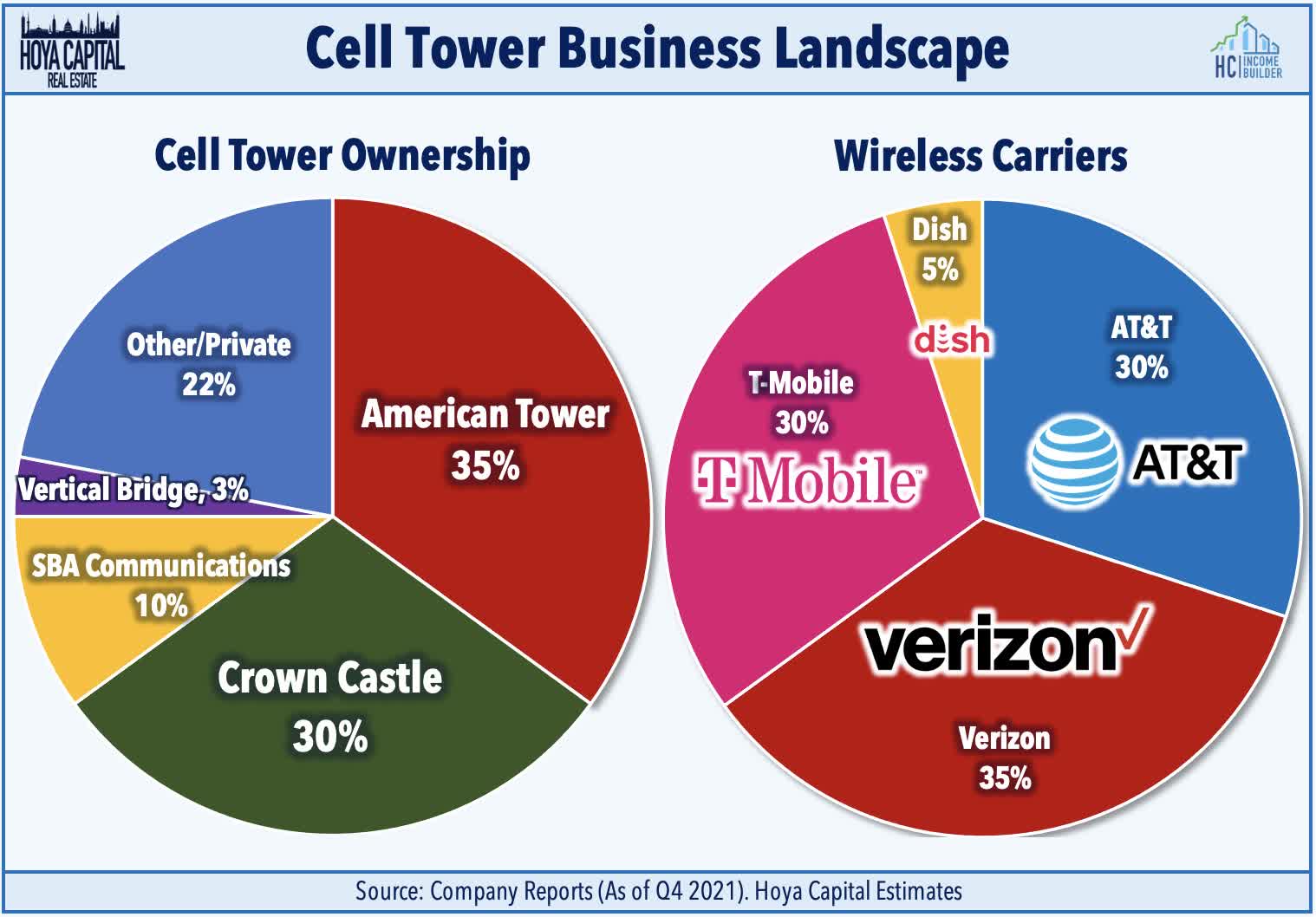

Cell Tower REITs – a perennial performance leader in the real estate sector – have uncharacteristically lagged this year, dipping into “bear market” territory for just the second time in history. Within the Hoya Capital Cell Tower REIT Index, we track the three Cell Tower REITs which account for nearly $250 billion in market value: American Tower (AMT), Crown Castle (CCI), SBA Communications (SBAC). We also track Uniti Group (UNIT), which owns a fiber-optic cable network and portfolio of small-cell sites. DigitalBridge (DBRG) – tracked in the Data Center REIT sector – owns a stake in Vertical Bridge, which manages the fourth-largest tower portfolio in the nation.

Hoya Capital

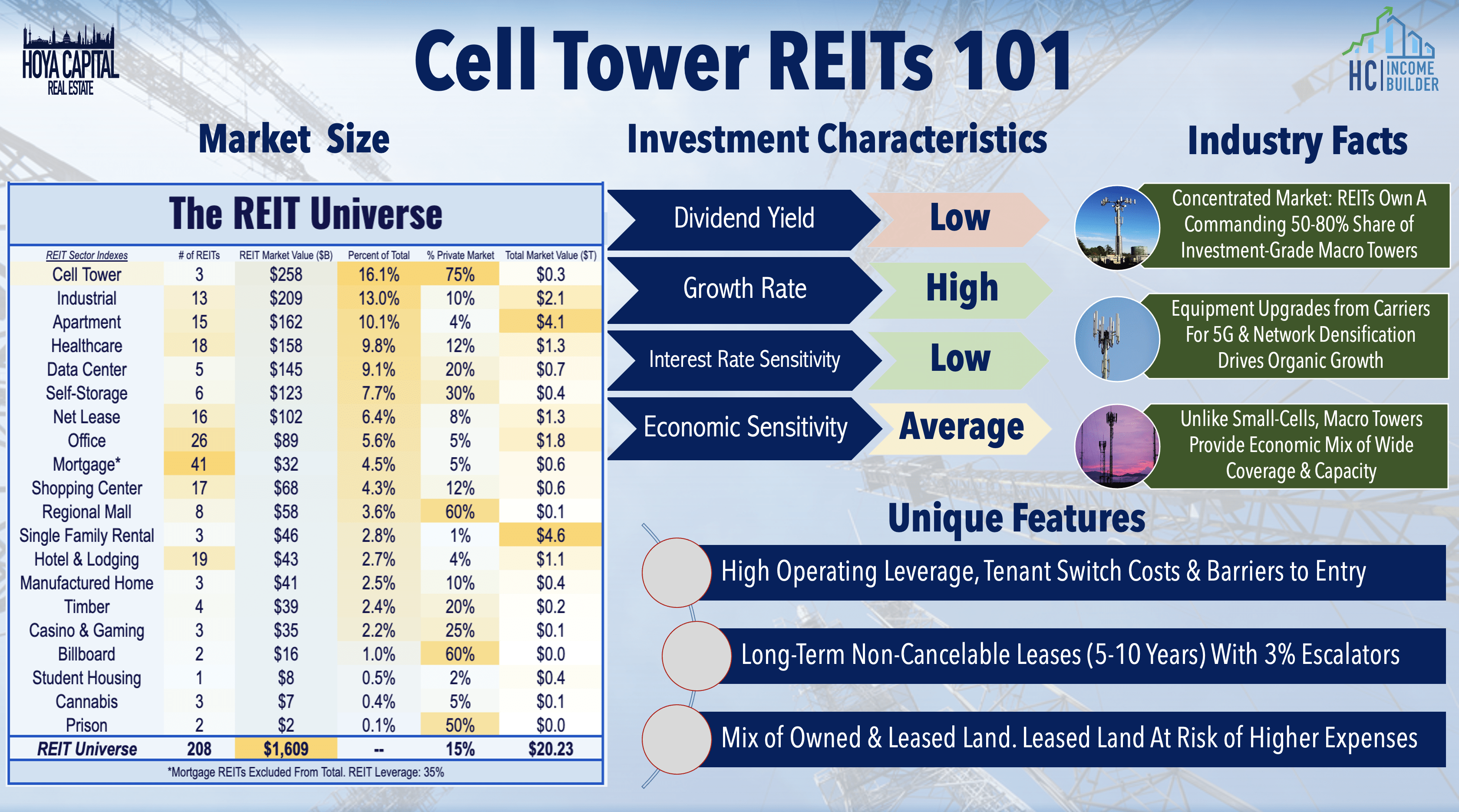

Cell Tower REITs – the single-largest real estate property sector – have been a critical growth engine of the REIT industry over the past half-decade. Cell Tower REITs’ relative dominance over the real estate sector is dwarfed by its dominance over the telecommunications sector, as these REITs control nearly 75% of wireless communication infrastructure in the U.S. and more than 50% in several major international markets. These REITs are the landlords to the four nationwide cellular network operators in the U.S.: AT&T (T), Verizon (VZ), T-Mobile (TMUS), and DISH Network (DISH), and own 50-80% of the 100-150k investment-grade macro cell towers in the United States.

Hoya Capital

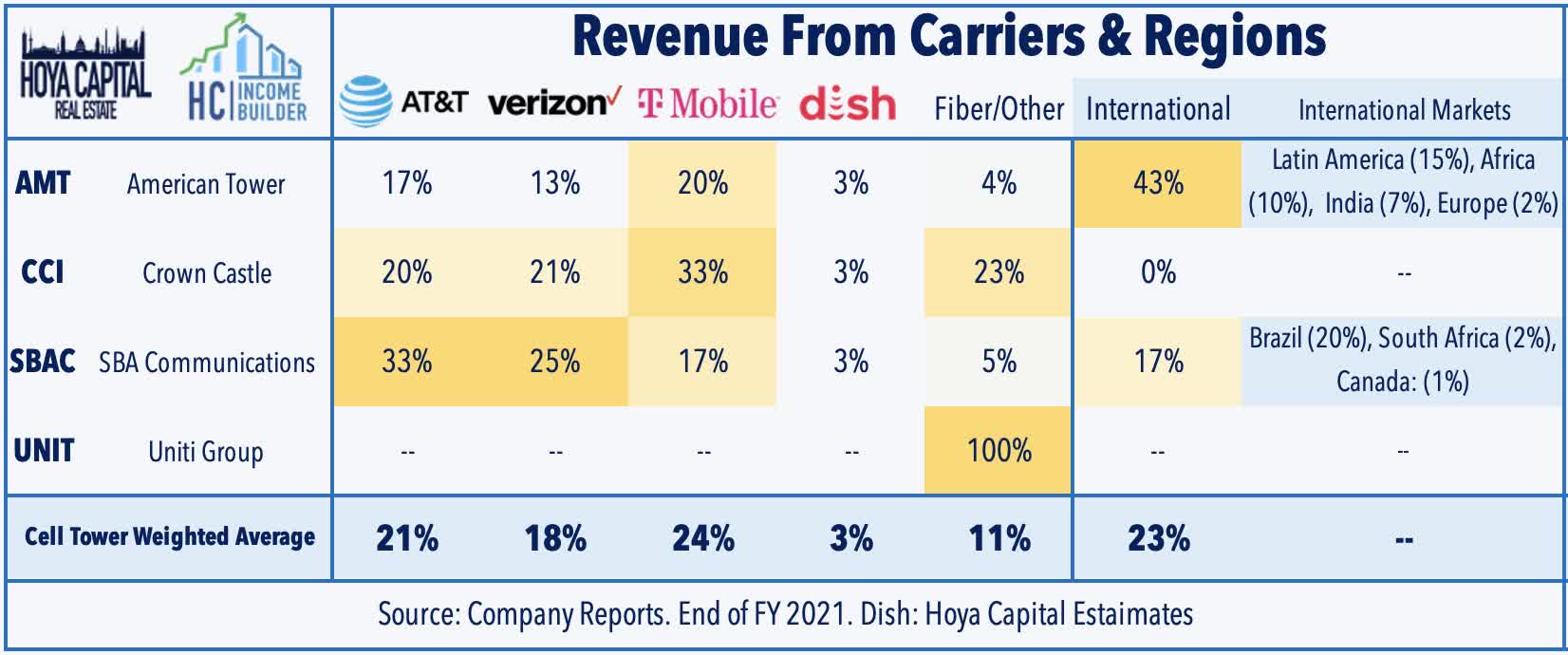

The cellular industry has seen plenty of fireworks over the last three years, underscored by T-Mobile’s now-completed acquisition of Sprint, a merger that is expected to amplify competition – and network spending – within the industry. The emergence of a fourth competitor – DISH Network – as a precondition to approval was a coup for Cell Tower REITs. DISH is expected to begin offering service in select markets later this year, but questions remain about DISH’s viability as a national competitor. Four competitors are better than three, and three definitely beats two. Even if DISH’s ambitious plans fail to materialize, the long-awaited merger has given the combined T-Mobile the ammunition and capital to compete in the 5G arms race.

Hoya Capital

This commanding competitive positioning has given these REITs substantial pricing power amid the roll-out of 3G, 4G, and 5G wireless networks, which has translated into enviable shareholder returns. While 4G networks gave us the “streaming” and “e-commerce” age, pioneered by Amazon (AMZN) and apps like Uber (UBER) and Spotify (SPOT), 5G networks are expected to spur a new wave of technological innovation fueled by “fiber-like” speeds and ultra-low latency over wireless nodes. 5G adoption in mobile devices has been propelled by the success of Apple’s (AAPL) lineup of 5G iPhones as nearly 60% of smartphones in the U.S. now have 5G capability. We continue to believe that home wireless broadband – called “Fixed Wireless Access” or “FWA” in the industry – is the true “killer app” of 5G, and many Americans will soon have 3-to-4 additional competitive home internet options.

Hoya Capital

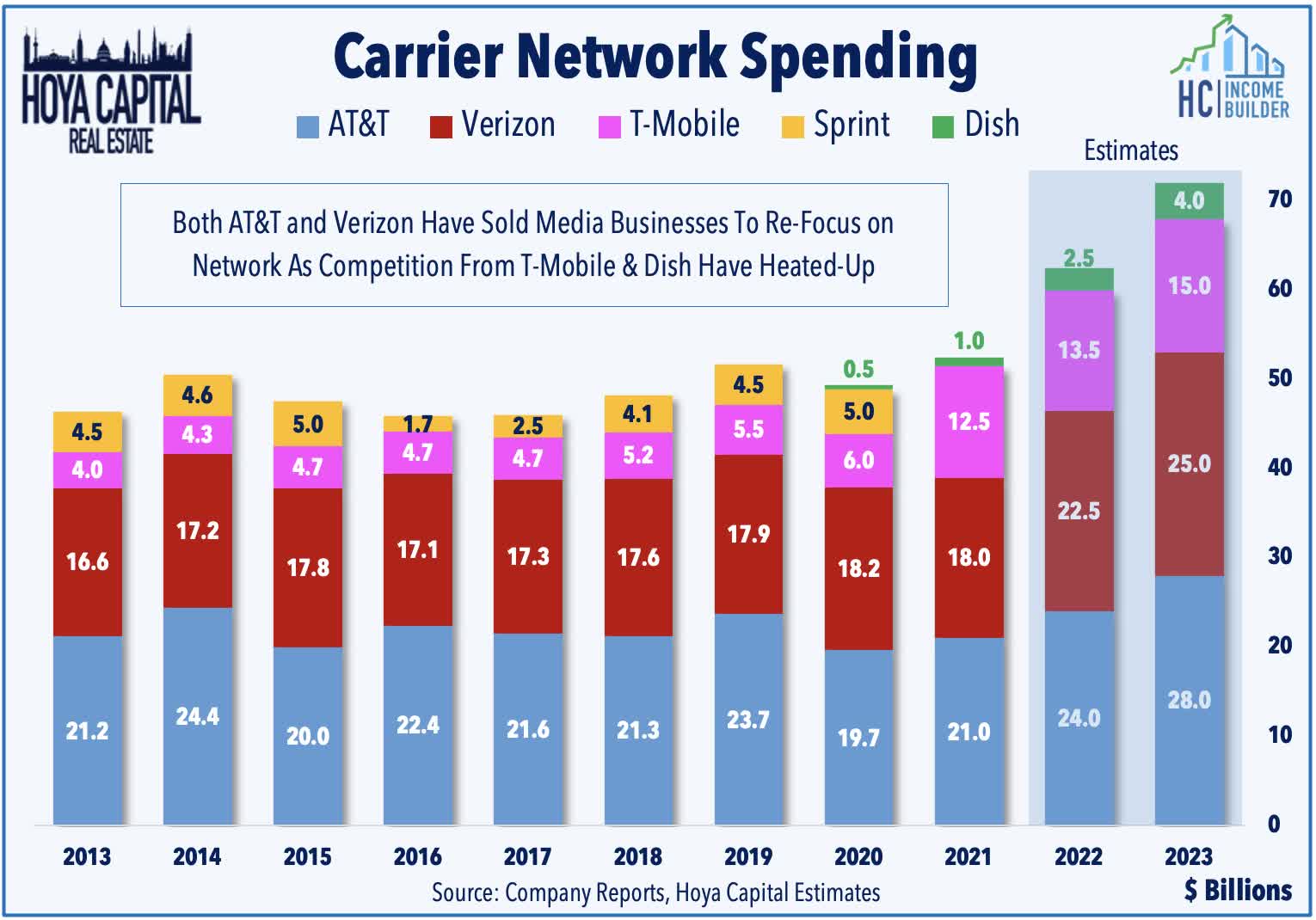

5G networks require up to 10 times more physical antennas per tower, and Cell Tower REITs typically negotiate higher revenue per tower after each incremental equipment upgrade, driving a persistent mid-single-digit “same-tower” growth rate. The three major U.S. carriers now boast “nationwide” 5G networks, built primarily by upgrading equipment on existing macro towers, an upgrade cycle that drove record levels of leasing activity in 2021 and is expected to continue – or even accelerate – into 2022. Crown Castle noted on its earnings call:

“We had the highest level of activity in the company’s history during 2021, and we’re expecting that level of activity to continue into ’22. What’s really unique about this cycle is that we’ve got 4 carriers deploying. They’ve got a significant amount of spectrum to be deployed, and they have the capital to be able to deploy that. I can’t think of another time in the history of our business where we’ve had 4 well-capitalized carriers with the spectrum and the desire to deploy their network. The focus for the legacy carriers is to touch the sites where they are already existing on the assets – on the macro assets. And we would expect the next phase of 5G build-out will be to densify their network.

Hoya Capital

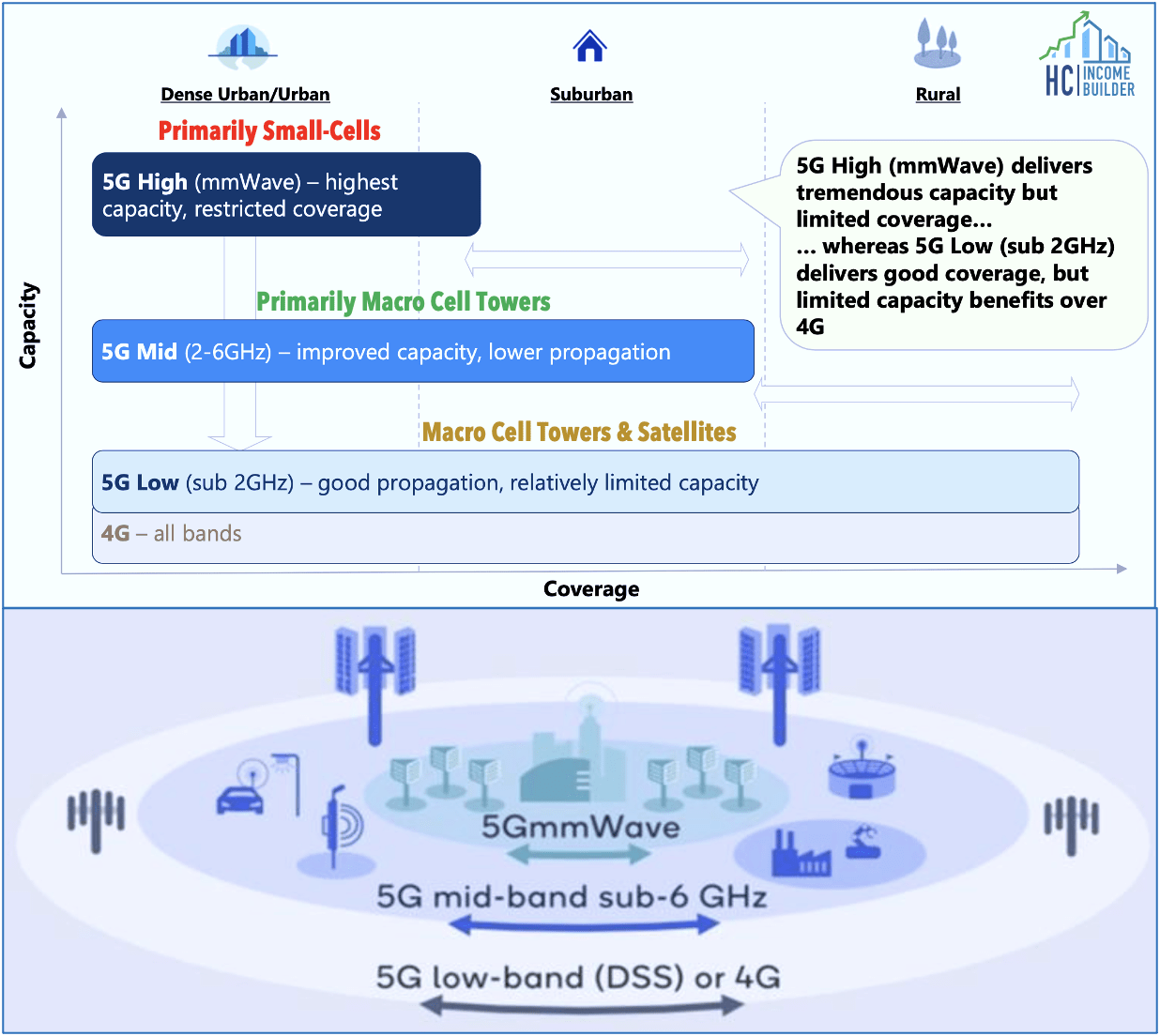

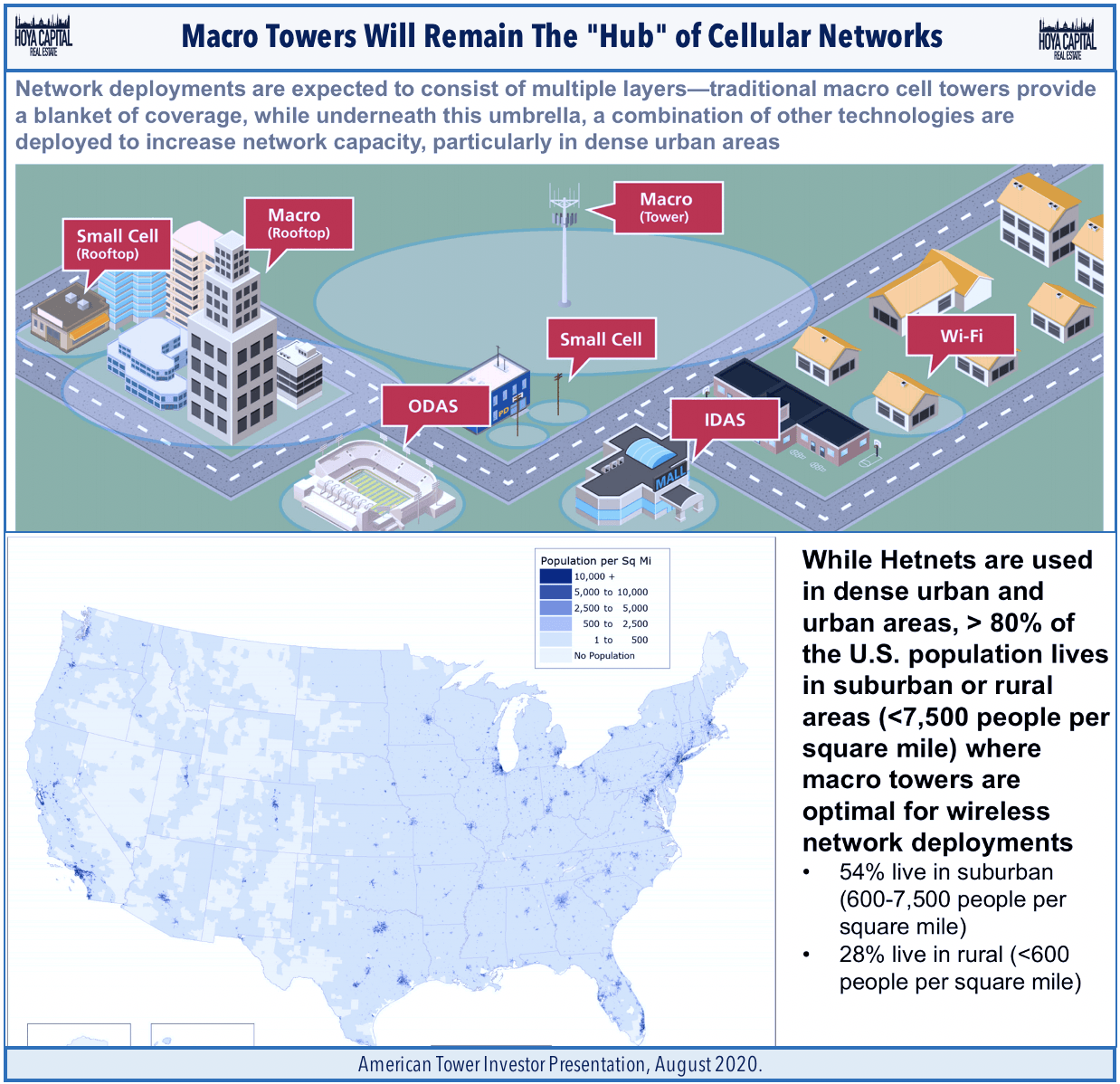

The 5G deployment has continued despite the recent dust-up with the FAA and the airline industry, issues which have been largely resolved in recent months through modifications to antenna orientations and power output in the immediate vicinity of landing aircraft. 5G build-outs have so far focused on equipment upgrades at macro towers for broad mobile coverage using mid-band spectrum which is seen as the “sweet spot” for the ideal economical mix of coverage and capacity and is generally. The next phase of deployment will likely focus on network densification through small-cell nodes, but carriers and Crown Castle – the market leader in small-cells – have delayed and/or reduced their small-cell deployment plans in recent quarters as the per-subscriber economics of has proven to be economically challenging so far.

Hoya Capital

Deeper Dive: Risks & Opportunities

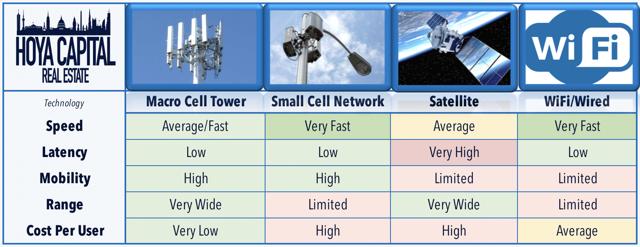

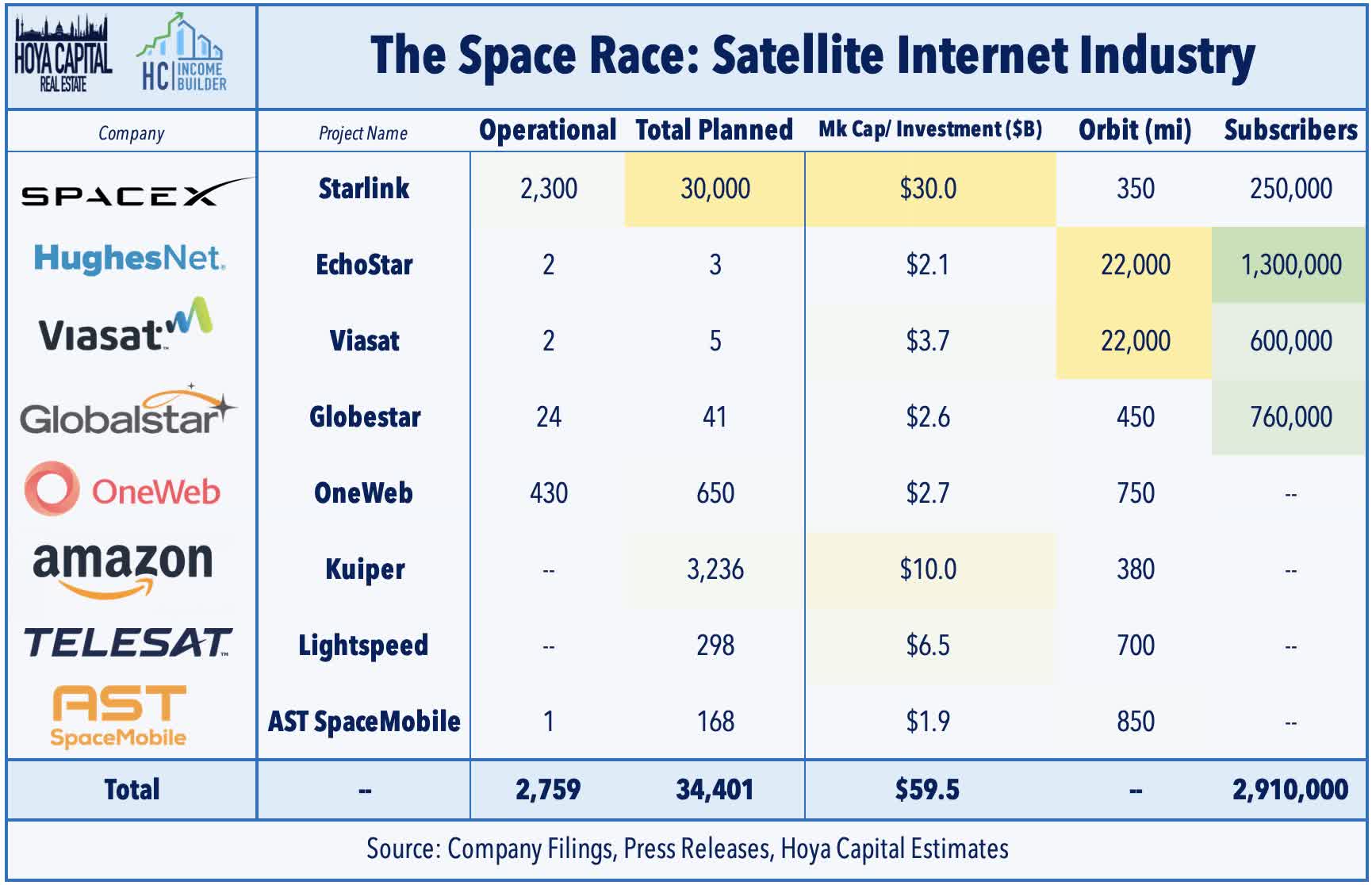

Cell tower REITs have benefited immensely from the increase in network spending from the four national carriers during the early stages of the 5G rollout, as carriers have focused early efforts on upgrading existing macro towers ahead of small-cell deployment. High-power “macro” cell towers currently provide the most economical mix of network coverage and capacity, but there are ever-present concerns that evolving technologies could eventually alter the competitive dynamics. Specifically, we believe that some caution is warranted in light of the faster-than-expected advancement of the Low-Earth-Orbit (“LEO”) satellite industry, led by Elon Musk’s SpaceX/Starlink.

Hoya Capital

Satellite internet has been around for decades through providers including EchoStar’s (SATS) HughesNet and Viasat (VSAT) that use geostationary satellites that are roughly 20k miles from earth, but LEO systems can theoretically provide 5G-like speeds through “constellations” of satellites that are far closer to Earth. Starlink – which has already deployed nearly 2,000 LEO satellites and boasts 250k subscribers – is one of a handful of companies working on LEO broadband and related technologies, a list that includes Amazon’s (AMZN) Kuiper Project, Telesat’s LightSpeed, and OneWeb. Even American Tower itself has made strategic investments in the LEO space through a partnership with AST SpaceMobile (ASTS), which seeks to provide satellite connectivity through traditional cell phone antenna systems.

Hoya Capital

While some investors have raised concern that LEO networks could outright “replace” cell towers, telecom analysts – and Elon Musk himself – see these networks as more likely to “supplement” – or at worst “co-exist” – with existing ground-based networks for the foreseeable future. We believe that macro towers will continue to be the “hub” of high-speed wireless networks for at least the next half-decade and likely beyond, but these REITs will no longer be the “only game in town” for macro coverage – particularly in situations where mobility and latency are secondary – as LEO networks get deployed. We also see the potential that LEO plays a large role in home wireless broadband service – which could compete directly with 5G cell-based home internet.

Hoya Capital

Due to the high concentration of ownership and significant barriers to entry in the United States related to restrictive zoning and the favorable economics of colocation, cell tower REITs are perhaps the only real estate sector that could be classified as true price makers rather than price takers. Cell carriers sold off their tower assets beginning in the mid-2000s to de-lever their balance sheet and free up capital to expand their networks. Supply growth is almost non-existent in the US, and the relative scarcity of cell towers, combined with the absolute necessity of these towers for cell networks, has given these REITs substantial pricing power even as the number of potential tenants has dwindled down to just four national carriers over the last two decades.

Hoya Capital

Cell Tower REIT Stock Performance

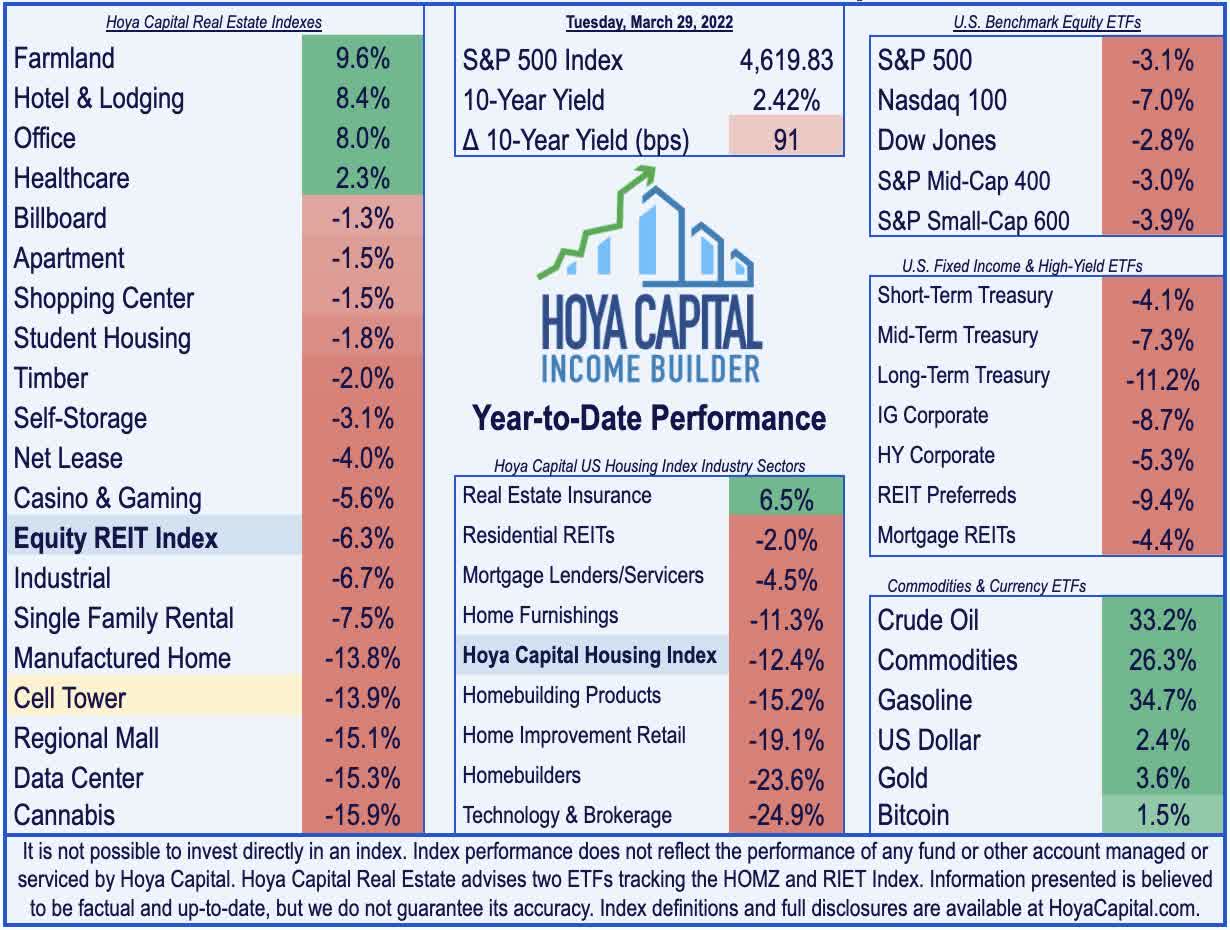

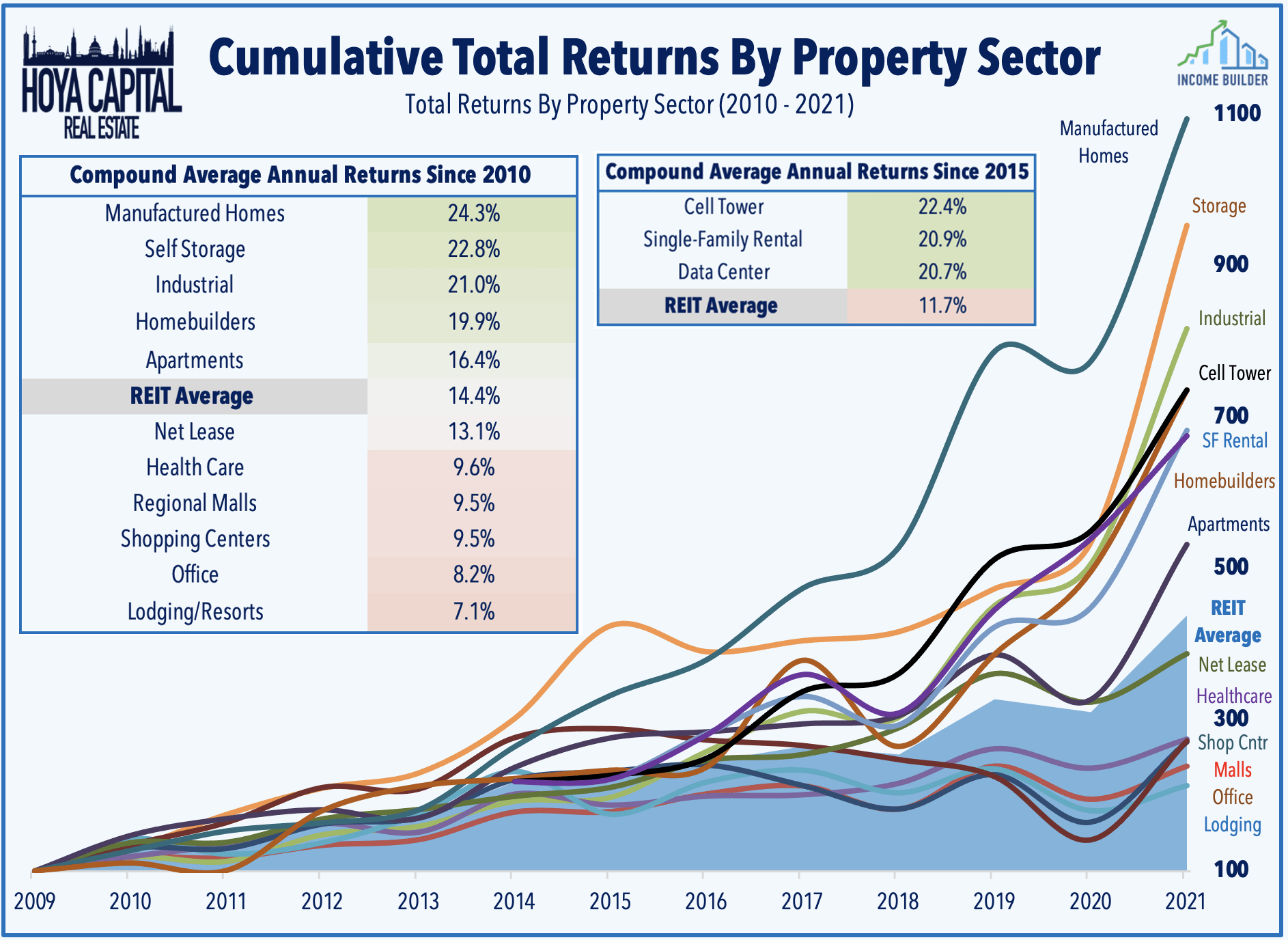

Cell Tower REITs have uncharacteristically lagged this year, dipping into “bear market” territory for just the second time since their emergence as REITs in the mid-2010s, and are trading near the “cheapest” valuation levels in recent history. Several factors are behind the recent slump including potential competition from Low-Earth-Orbit satellite networks, delays in 5G deployment related to airline interference, and broader tech-related weakness. The Hoya Capital Cell Tower REIT Index is lower by nearly 14% so far in 2022, lagging the 6.3% decline from the broad-based Vanguard Real Estate ETF (VNQ) and the 3.1% decline from the S&P 500 ETF (SPY).

Hoya Capital

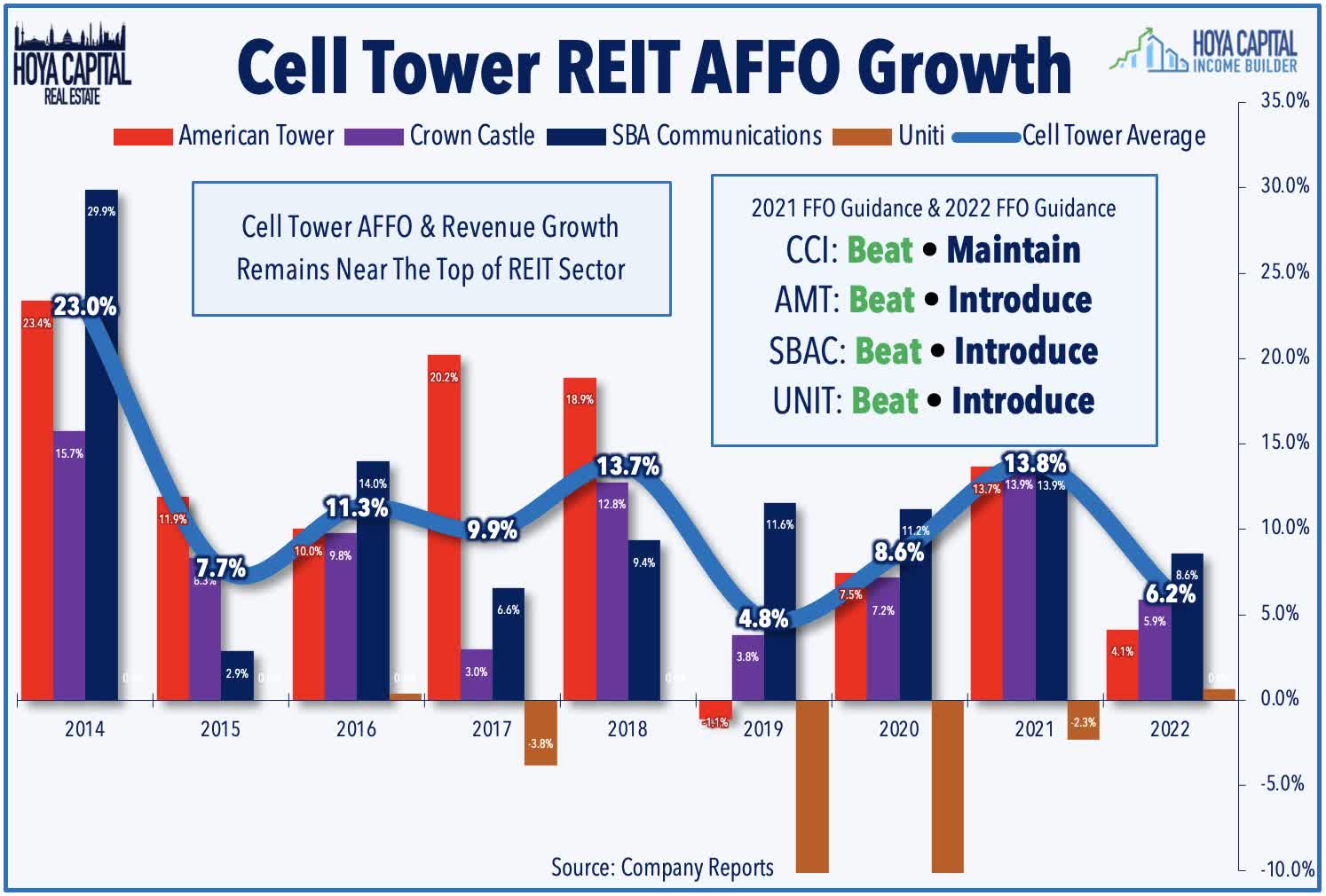

All four cell tower and fiber REITs delivered results above their prior full-year guidance, led by Crown Castle, which delivered sector-leading FFO growth of nearly 14% in 2022, followed closely behind by SBA Communications and American Tower, which reported growth of 13.9% and 13.7%, respectively. Uniti Group, meanwhile, has rebounded this year after delivering better-than-expected results and projecting a return to FFO growth in 2022 for the first time since 2016. Cell tower REITs expect to see an uptick in churn related to the T-Mobile/Sprint merger to weigh on same-tower results over the next three years, as AMT reiterated that it expects the effects of the churn to begin in Q4 of 2021 and will continue “out to 2024” with the biggest impact being in 2022, resulting in a 4% drag to full-year AFFO.

Hoya Capital

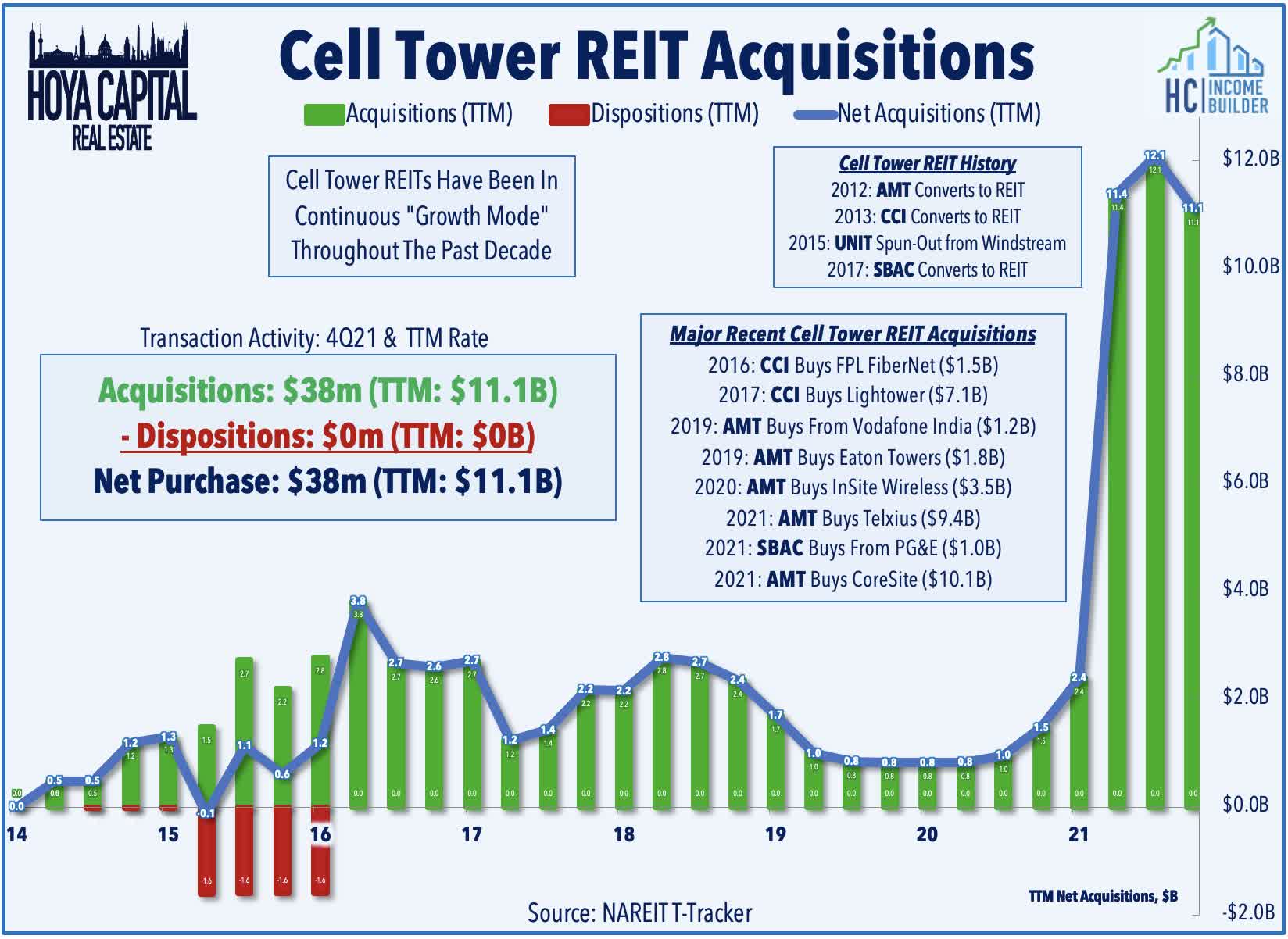

While same-tower growth is expected to moderate a bit over the next couple of years before rebounding around mid-decade, cell tower REITs have kicked their external growth initiates into a higher gear over the last year with the major deal of last year being American Tower’s $10.1B acquisition of data center REIT CoreSite, which positions AMT to be a leader in “edge” networking. Earlier in the year, AMT closed on a $3.5B deal to acquire InSite Wireless which owns 3,000 communications sites in the U.S. and Canada, and a $9.4B deal to acquire Telxius Towers, which owns 31,000 sites across Europe and South America. All three REITs also continue to expand and consolidate via smaller “one-off” acquisitions and deploying some capital into new tower builds.

Hoya Capital

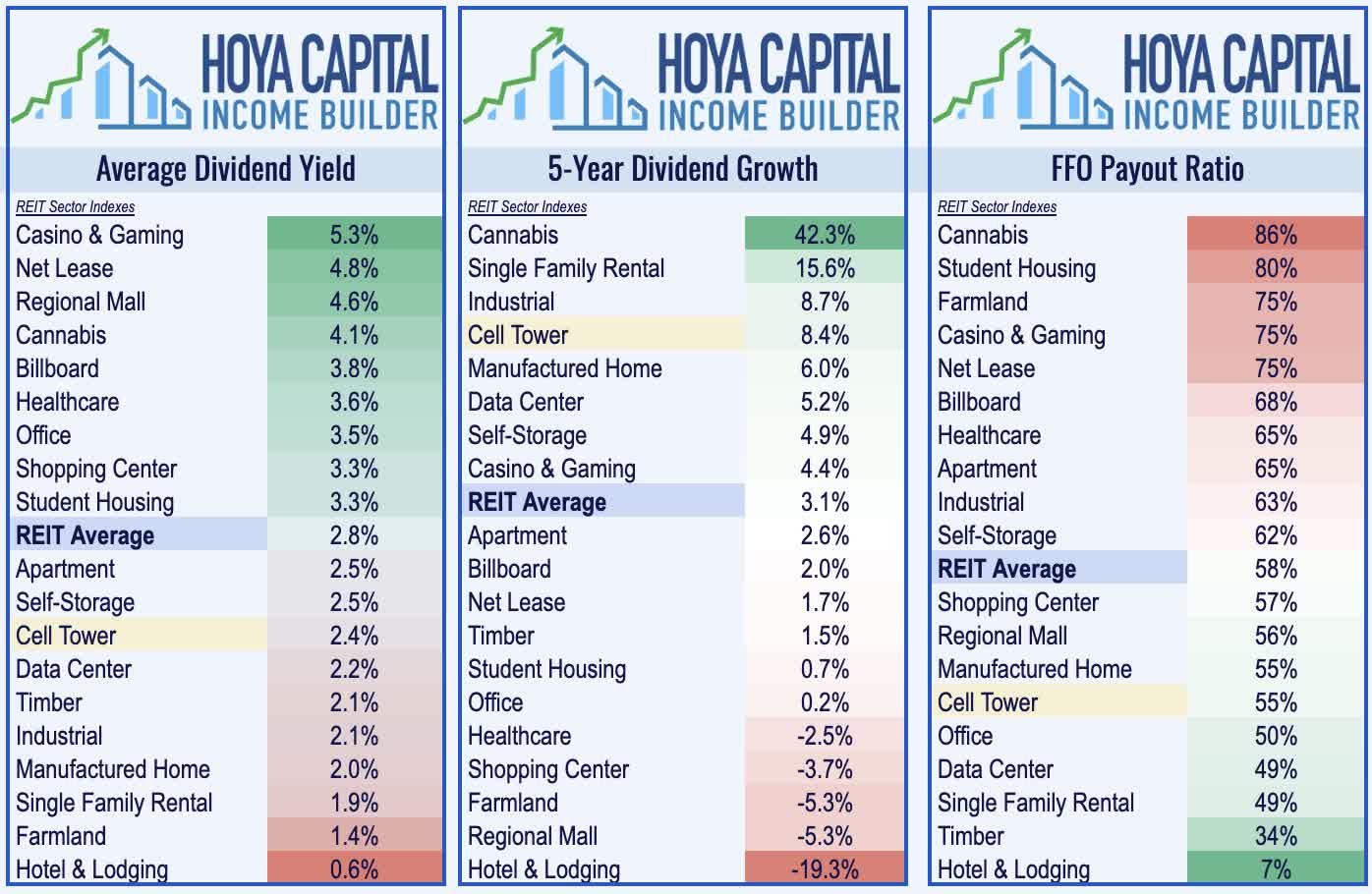

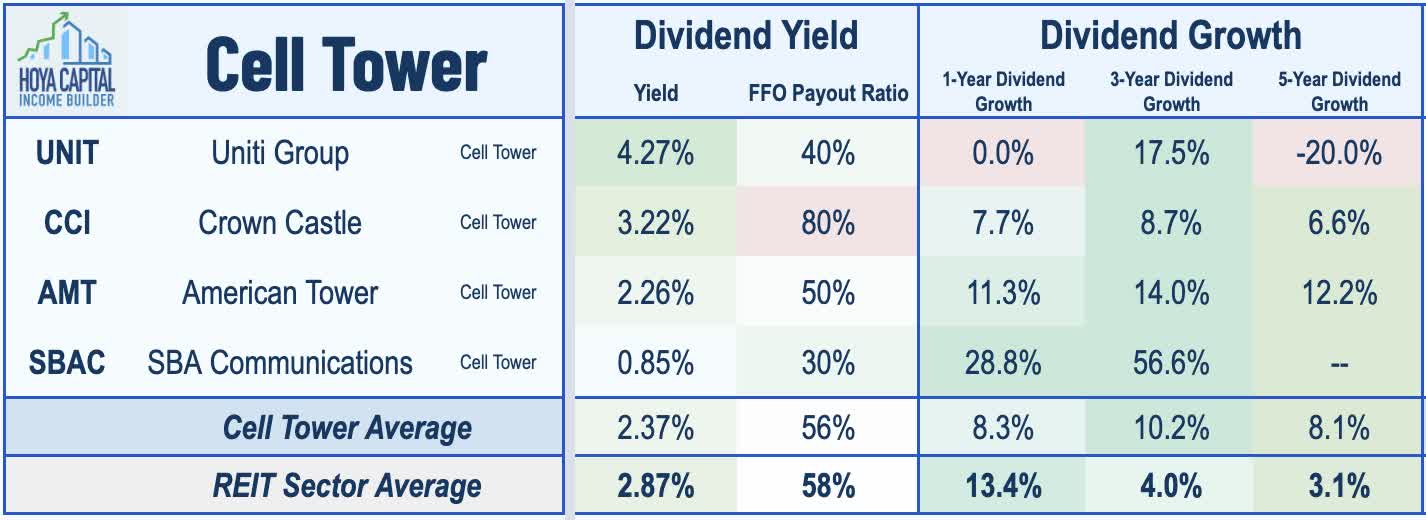

Cell Tower REIT Dividend Yields

Cell Tower REITs pay an average dividend yield of 2.4%, below the market-cap-weighted REIT sector average of roughly 2.8%, but have been among the leaders in dividend growth throughout their history. Cell towers were one of the few property sectors that were untouched by the wave of dividend cuts and suspensions that hit the REIT sector in 2020 and have delivered robust annual dividend growth averaging over 8% over the past five years. Cell Tower REITs retain roughly half of their free cash flow leaving ample free cash flow for external growth and additional dividend growth.

Hoya Capital

Among the three larger cell tower REITs, we note that only Crown Castle acts like a “typical REIT” when it comes to distributions, paying a relatively healthy 3.22% dividend yield, which is roughly 80% of its available cash flow. American Tower, meanwhile, pays a relatively low 2.26% yield, while SBA Communications pays a yield of just 0.85%. Fiber-focused Uniti Group pays a yield of 4.27%, but has lagged its peers when it comes to dividend growth.

Hoya Capital

Key Takeaways: Cautious Optimism Warranted

We recently added to our position in Crown Castle and maintained our position in American Tower in our Income Builder portfolios as the near- and medium-term outlook for cell tower REITs remains promising. That said, we believe that some caution is warranted given their potential longer-term technological risk as strong competitive positioning has historically been a fleeting privilege in the telecommunications sector. The simple physics and economics of wireless networking suggest that high-power macro communication towers will continue to be a “hub” of mobile networks for the reasonably foreseeable future, and while the technology developments with LEO networks and alternative technologies need to be monitored, we believe that current valuations adequately discount this longer-term risk.

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Prisons, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Be the first to comment