Darren415

This article was first released to Systematic Income subscribers and free trials on Jan. 8.

Welcome to another installment of our CEF Market Weekly Review where we discuss closed-end fund (“CEF”) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the first week of January. Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

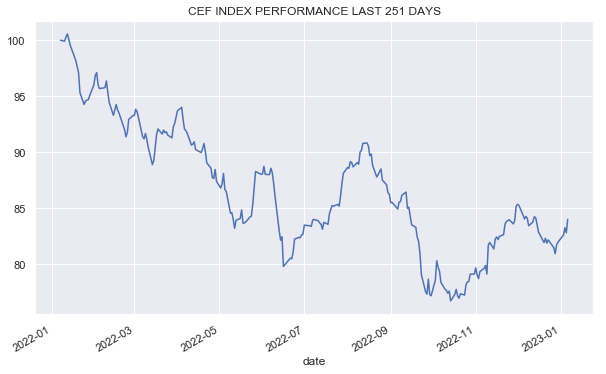

CEFs had a great week, supported by both lower Treasury yields and higher stock prices. Payroll growth continued to slow while ISM services fell sharply – indications of a slowing economy – which could allow the Fed to pivot from its hiking cycle sooner rather than later.

Systematic Income

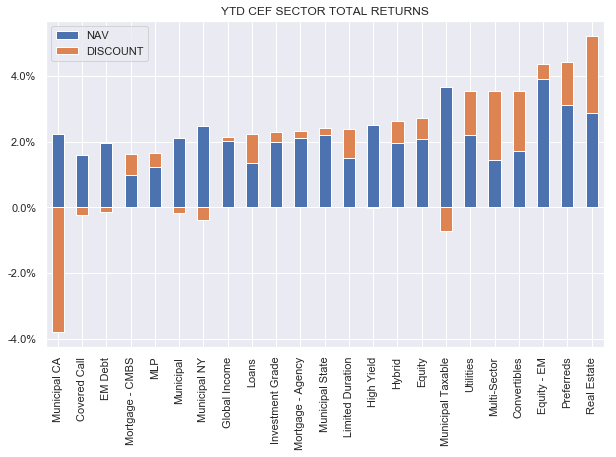

The recent CEF rally has erased most of the December weakness.

Systematic Income

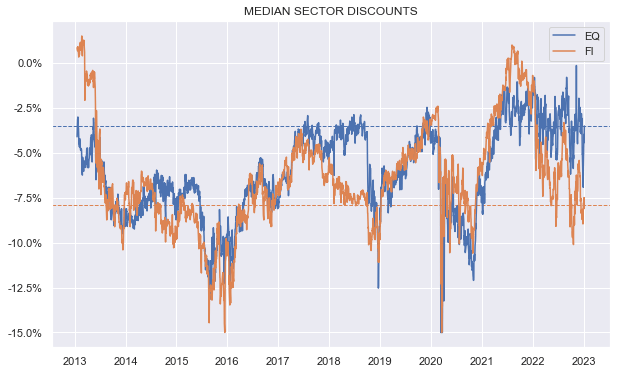

Discounts tightened around 1%. Fixed-income sector valuations remain attractive relative to its history.

Systematic Income

Market Themes

2023 began where 2022 left off – by seeing significant distribution cuts across the CEF space.

Nuveen reported distribution cuts across most of their CEFs in January. These were not the first cuts for most of them.

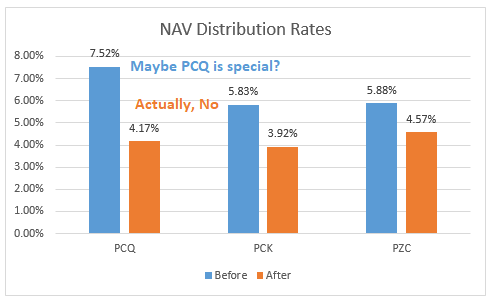

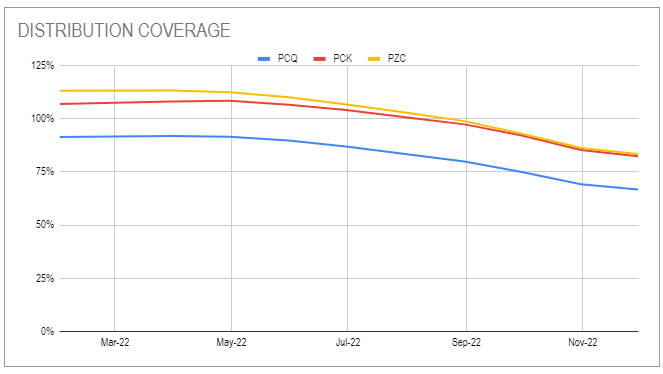

PIMCO Muni funds also finally faced reality and had big cuts of 20 to 45%. What was very interesting is the disparity in the cuts between close funds. For example, in the CA trio (PCQ, PCK, PZC) PCQ cut by 45% and the other two funds by 22% and 33%.

It’s been a weird fact of this trio that PCQ had a much higher and totally unjustified distribution rate of 7.5% on NAV versus about 5.8% for the other two funds. It’s tempting to think that there was something special about PCQ which warranted such an elevated NAV yield versus the other two funds.

The chart below shows NAV distribution rates prior to the cut (blue bars) and rates after the cut (orange bars). The fact that PCQ had a much higher rate prior to the cut fooled many investors into thinking it was special, making them bid the fund up to a very high premium level. After the cut, the NAV distribution rates for the three funds are very similar, showing that it was just a mirage.

Systematic Income

Investors could easily see that there was nothing special about PCQ since PCQ coverage was 67% versus 82% for the other two funds. This tells us that there was actually nothing behind the much higher NAV yield of PCQ. In short, covered yields – a key metric we follow on the service – was roughly the same for all three funds.

Systematic Income CEF Tool

An important consequence of this much higher NAV yield was that PCQ also traded at a much higher premium than the other 2 funds as investors mistook its high distribution rate for its higher earning potential. What’s especially odd is that its high premium pushed its current yield (i.e. distribution rate on price) below the other 2 funds which is beyond ludicrous.

What happened after the cut is that PCQ had a huge (and much bigger than the other 2 funds) price drop – a typical double-whammy for investors who like chasing unsupported high distribution rates – and one that results in permanent economic loss to investors. Just like the drop in the PTY premium when that fund cut, the 48% premium at which PCQ closed prior to the cut will likely never be regained.

Systematic Income

Invesco added a couple of cuts as well in their bond CEF VBF (which oddly was actually hiking through 2022 for no good reason) and a state Muni CEF VPV.

A sharp rise in the cost of leverage has been the primary driver of distribution cuts with deleveraging, due to a sharp drop in asset prices, being a close second driver. Leverage costs will continue to rise for some time even when the Fed finishes its hiking cycle. However, if assets continue to rally from here, deleveraging will be less of a fear and may even allow funds to add borrowings, driving higher net incomes, all else equal.

Market Commentary

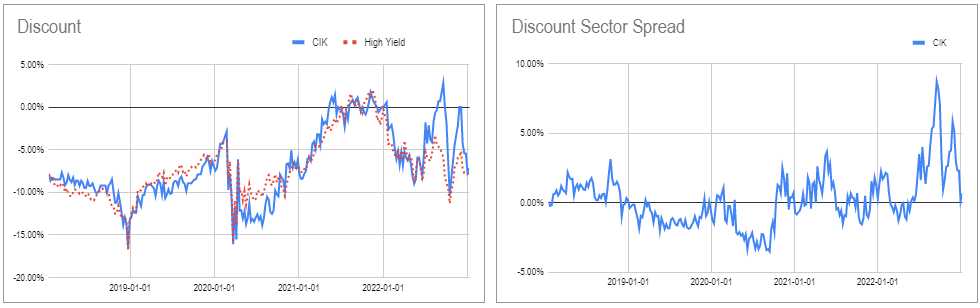

The High-Yield corporate bond CEF Credit Suisse Asset Management Income Fund (CIK) is back to an attractive valuation. CIK is one of our favorite High Yield bond CEFs. It was in the High Income Portfolio for a while until its valuation jumped relative to the sector when it was rotated to a sister fund Credit Suisse High Yield Bond Fund (DHY).

Now the fund’s valuation looks much better. It trades at a 7.2% discount as of this writing which is around the sector’s average level. Recall that it has an unusually low management fee so its middling discount is actually extremely attractive. In other words, a 7% discount for CIK is equivalent to a discount of 13-14% for a “typical” HY bond CEF.

CIK has outperformed the sector in total NAV terms over the past year and is one of the best-performing HY bond CEFs over the longer term largely due to its lower fee. We will be looking to add it or rotate to it on further weakness.

Systematic Income CEF Tool

Be the first to comment