I going to make a greatest artwork as I can, by my head, my hand and by my mind./iStock via Getty Images

There is a lot of money to be made in “pick and shovel” plays, as these types of companies often possess a moat through their distribution channels. Such examples can be found in nearly every industry such as healthcare.

This includes the big 3 drug distributors AmerisourceBergen (ABC), McKesson (MCK), and Cardinal Health (CAH), all three of which have seen strong returns over the past year.

This brings me to CDW Corporation (NASDAQ:CDW), which serves enterprises large and small with technology products. CDW has done rather well since my last bullish take on it near the end of 2020, producing a 50% total return, far outpacing the 12% return of the S&P 500 (SPY). In this article, I revisit the stock and highlight what makes it a solid choice at the right price.

Why CDW?

CDW is a leading multi-brand technology solutions provider to businesses, government, education, and healthcare customers. Many enterprise employees may be familiar with the CDW brand for its wide range of computer equipment and accessories that they provide, such as laptops and monitors, but beyond these services, CDW also provides security, cloud, data center, and networking solutions.

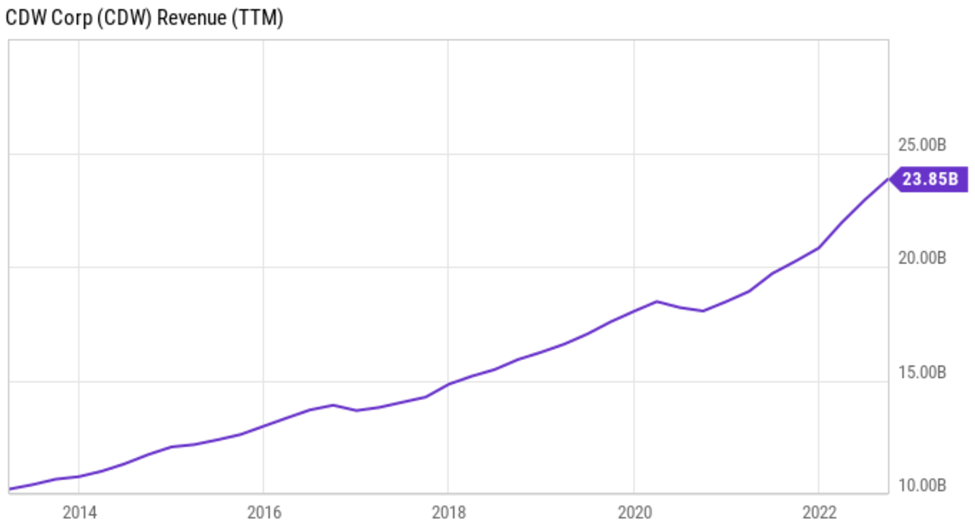

CDW has built out its reach and capabilities over the years, and has the ability to weather varying economic environments. As shown below, except for a light dip in 2020, CDW’s revenue has been on mostly a straightforward upward path and more than doubled over the past decade.

CDW Revenue (YCharts)

A part of this growth has been driven by strategic investments in recent years to further strengthen its competitive position and drive growth. This includes Aptris, a provider of IT service management and digital transformation solutions, which enables CDW to expand its offerings in the fast-growing digital transformation market. In addition, in 2021, CDW acquired Scalar, a provider of data center solutions, which expands its portfolio of data center offerings, and enhances its position in the fast-growing edge computing market.

Meanwhile, CDW continues its impressive growth track record, with net sales rising by 19% YoY on a constant currency basis to $6.2 billion in the third quarter. It’s also demonstrating healthy operating leverage through efficient scale, as operating income grew at a faster rate of 21%. This was driven by strength across the board, with the corporate segment responsible for much of the change at 25% growth, followed by public segment at 13% growth, and small business at 5% growth.

Near term risks to CDW include the potential for a recession this year. In addition, a number of tech companies such as Meta Platforms (META), Amazon (AMZN), and Netflix (NFLX) were too aggressive in hiring over the past 2 years, and recently laid off a number of employees. As such, this could slow down order activity for CDW.

Nonetheless, I see CDW’s long-term thesis as being intact, especially considered that it’s a much more diversified business than it was 5 to 10 years ago. This includes CDW’s 3-pronged strategy to capture share, enhance capabilities in high growth solutions, and expend service offerings. This is a part of the overall strategy to become an end-to-end solutions provider for both hardware and digital capabilities, as noted during the recent conference call:

In today’s environment of persistent uncertainty, our customers are increasingly leaning on CDW as a trusted partner, and they look to us to provide unbiased expert advice across the entire spectrum of IT.

This includes being a trusted partner who helps them tackle their most pressing priorities, pressing priorities like advancing their digital transformation, driving innovation and delivering exceptional stakeholder experiences, along with enhancing security and supporting collaboration in today’s distributed environment of work, learn and live everywhere.

Priorities that deliver operating efficiency and expense elasticity like burstable billing and modern hybrid and multi-cloud environments and infrastructure and new technology investments to optimize flexibility and agility. Our ability to enable solutions in support of all these diverse priorities drove broad-based and balanced performance.

Meanwhile, CDW carries a respectable investment grade BBB- rated balance sheet. Importantly, management has focused on debt reduction, paying down $656 million worth of long-term debt since the end of 2021. While its net debt to EBITDA ratio is currently elevated at 3.26x, I would expect for this leverage ratio to trend below 3x in the near term with continued debt paydown.

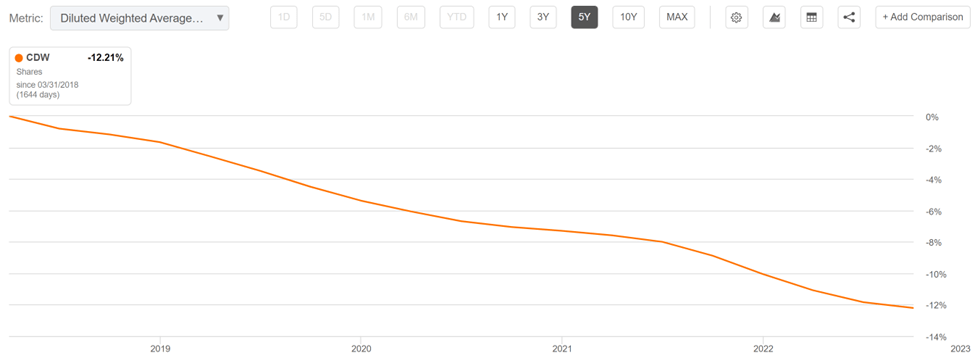

Plus, while CDW’s 1.2% dividend yield is low, it’s very well covered by a 21% payout ratio and comes with a 25% 5-year dividend CAGR and 8 years of consecutive growth. Moreover, CDW should be regarded as a total return story, as it has a strong track record of share buybacks. As shown below, it’s retired 12% of its outstanding float over the past 5 years alone.

CDW Shares Outstanding (Seeking Alpha)

Admittedly, CDW isn’t cheap at its current price of $197.62 with a forward PE of 20.2, sitting above its normal PE of 17.5 over the past decade. Given near-term uncertainties with the economy and potential for recent layoffs impacting CDW’s growth profile, I think investors would be better served waiting for a 10%+ discount from the current price.

Investor Takeaway

CDW has a wide-reaching business and has posted a strong revenue growth track record. The company is also well-positioned to benefit from its 3-pronged strategy of capturing market share, enhancing capabilities in high growth solutions, and expanding service offerings.

Meanwhile, management has been paying down debt related to recent acquisitions and is returning capital in the form of dividend growth and share buybacks. However, the valuation is a bit rich at the moment, and investors may be better served waiting for a pullback in price.

Be the first to comment