Dilok Klaisataporn

Investment Overview

The share price of Cassava Sciences (NASDAQ:SAVA) increased from ~$1, to $10 between 2019 and 2020, tread water between 2020 and 2021, had increased in value to >$120 by August 2021, began 2022 priced at $48, and will finish the year down ~40%, priced at ~$29 per share. Nothing short of a roller-coaster ride for its shareholders.

Cassava’s lead and only drug in development is Simufilam, indicated for Alzheimer’s disease. The drug caught the market’s attention when it met endpoints in a Phase 2b randomised, placebo controlled study back in 2021, after Cassava re-evaluated data initially found to have missed endpoints in a different lab.

Simufilam went on to produce seemingly outstanding results in a Phase 2, open label study, showing that in the first 50 patients who completed 6,9 and 12 months of treatment with Simufilam, an average -3.2 point improvement was observed on the “gold standard” ADAS-Cog scale, a measure of cognitive decline, at 12 months.

These results were potentially some of the best Alzheimer’s data ever generated, but not everybody was convinced with members of the scientific community noting the absence of a placebo arm in the study, the small patient population, and the lack of supporting evidence for Simufilam’s mechanism of action.

There was more to come for Cassava when a Citizen’s Petition was lodged with the FDA alleging that Cassava scientists may have manipulated some of the preclinical data used to secure an Investigational New Drug (“IND”) for Simulfilam from the FDA in 2017, and that the lab that re-evaluated the Phase 2b data and found it had met key endpoints was run by a long term associate of Cassava’s, Dr. Hoau-Yan Wang, at the City University of New York, who’s research had been instrumental in the development of Simufilam.

The filing of the Citizen’s Petition rocked Cassava’s share price, which declined from >$120 in August 2021, to <$20 by May 2022. Management made several efforts to defend themselves, pointing out that no agency has yet found them guilty of falsifying data, or any other form of malpractice. In November, Cassava announced it was filing a lawsuit against:

… certain individuals who executed a “short and distort” campaign against the Company. The 150+ page complaint alleges that the Defendants’ disinformation campaign caused a precipitous decline in Cassava Sciences’ stock price, a multi-billion dollar decline in its market capitalization, and delayed the Company’s work in developing a treatment for Alzheimer’s disease.

Heading into 2023, then, the investment thesis around Cassava remains extremely polarising.

According to MarketBeat short interest in Cassava stock remains high at >20%, reflecting a large section of the market’s belief that in 2023 Cassava’s Simufilam may be revealed to be ineffective against Alzheimer’s at best, and at worst, that the drug should not have been awarded an IND given preclinical data was falsified, and that the initial negative findings from the Phase 2b in 2020 were accurate, as opposed to the data collected afterwards by Dr. Wang’s lab.

On the other hand, although far from conclusive, data collected from the Open Label Phase 2 remains compelling – if looked at from certain angles and viewpoints – and there are two Phase 3 studies of Simufilam ongoing – RETHINKALZ and REFOCUSALZ – enrolling ~1,750 patients, which may read out data next year, plus final results from the open label study, from all 200 patients promised for before the end of this year.

Cassava faces challenges on three fronts headed into 2023 – these are the factors that I think will determine the company’s performance across the next 12 months, although spoiler alert, my suspicion is that shareholders may have to wait until 2024 for critical catalyst – Phase 3 study data – to arrive.

1. Cassava’s Competition In Alzheimer’s

Although Biogen (BIIB) / Eisai’s Alzheimer’s therapy Lecanemab posted some apparently strong data from a Phase 3 study showing a 27% improvement vs. placebo in its primary endpoint measure of Clinical Dementia Rating-Sum of Boxes, and may receive an FDA approval on January 6th, this therapy is still dogged by safety concerns and may be a commercial flop like its forerunner, Aduhelm. Aduhelm was approved in June 2021 but has now been shelved by Biogen owing primarily to the instances of brain swelling. Lecanemab has been associated with three patient deaths in its ongoing pivotal study caused by oedema.

Like Lecanemab, Eli Lilly’s (LLY) Donanemab targets amyloid beta deposits that build up in the brains of Alzheimer’s patients, and Phase 2 studies have shown the drug to be effective using a measure of integrated Alzheimer’s Disease Rating Scale (“iARDS”). Lilly recently shared data from a Phase 3 study comparing Donanemab favourably against Aduhelm in terms of amyloid clearance, although like Aduhelm, instances of Amyloid-related imaging abnormality (“ARIA”) suggest the safety profile may not be adequate.

Anavex Life Sciences (AVXL) data from a Phase 3 study of its Alzheimer’s and Parkinson’s Disease drug, released last month, failed to impress a sceptical market due to changed trial endpoints and some questionable interpretation of the data, despite its candidate Blarcamesine showing a 45% slower rate of decline than the placebo group in its >500 patient study.

More recently, BioVie (BIVI) stock has been trending upwards as the Nevada based company released data from a Phase 2, open-label (no placebo arm) study which showed that patients conditions “improved significantly” on the Global Rating Of Change and ADAS-COG 12, including a 2.1 points improvement on the modified ADAS-Cog12 scale (p=0.0173) among MCI and mild Alzheimer’s Disease (AD) patients.

Annovis Bio’s (ANVS) share price traded flat in 2022, although lead candidate Buntanetap – indicated for Alzheimer’s and Parkinson’s – is in a 320-patient Phase 2/3 study in Alzheimer’s, and a 450-patient Phase 3 study in patients with Parkinson’s. This micro-cap’s stock briefly traded >$100 at the peak of the Aduhelm approval / Simufilam Alzheimer’s hype cycle before poor study results saw it fail to outperform placebo based on Mini Mental State Examination (“MMSE”) scoring system, or Clinical Dementia Rating Sum of Boxes (“CDR-SB”) scale scoring.

Cortexyme (CRTX) stock is now trading <$1 after the biotech’s Alzheimer’s drug atuzaginstat failed to meet endpoints of Alzheimer’s Disease Assessment Scale–Cognitive Subscale (“ADAS-Cog11”) and Alzheimer’s Disease Cooperative Study–Activities of Daily Living (“ADCS-ADL”) in a Phase 2/3 study, and the FDA advised the company to cease development.

Prothena (PRTA) is developing a tau-targeting (tau “tangles”, like Amyloid Beta, can be found in large quantities in Alzheimer’s patients brains and are considered an alternative target to amyloid) Alzheimer’s drug in collaboration with the New York-based Pharma giant Bristol Myers Squibb (BMY), and is also developing its wholly owned candidate PRX-012, which targets amyloid, has a Fast Track designation from the FDA, and could prove a long-term challenger to Lecanemab and Donanemab.

With Swiss Pharma giant Roche (OTCQX:OTCQX:RHHBY) having abandoned development of its anti-amyloid Alzheimer’s candidate Gantenerumab in November, after Phase 3 study results failed to show statistically significant improvements versus placebo, the list of companies likely to win approval for an Alzheimer’s drug before 2025 is a short one.

Whilst it is probably more likely than not that Biogen / Eisai’s Lecanemab will be approved in 2023 – given instances of ARIA-E have been substantially lower than already approved Aduhelm – and perhaps Lilly’s Donenemab will also receive an accelerated approval next year, the gap in the market for an Alzheimer’s drug that is both effective and safe is probably the most lucrative opportunity in all of healthcare, given the nearly 5m Alzheimer’s patients in the US alone whose only current treatment options are restricted to NMDA antagonists such as donepezil (Aricept), galantamine (Razadyne), and rivastigmine (Exelon).

As a potentially disease modifying therapy, Simufilam’s addressable market doubtless runs into the double-digit billions, and Cassava is only two completed Phase 2 trials, or ~18 months away from knowing whether RETHINKALZ and REFOCUSALZ will meet their respective endpoints of ADAS-Cog12 cognitive scale, and ADCS-ADL, with iARDS as a secondary endpoint.

The opportunity is so exciting for a reason, however, and that is because no drug developer has been able to develop an effective and safe disease modifying therapy. Cassava may claim to have done so, but there is a large amount of scepticism.

2. Can Cassava’s Simufilam Thesis Stand Up To The Intense Scrutiny?

I have briefly described above the Phase 2b study – initially unsuccessful, then found to be successful by Dr. Wang’s lab – the open label Phase 2 study, and the two Phase 3 studies that are central to the approval or otherwise of Simufilam, and will comment on their role in Cassava’s approval push shortly.

It is still possible that the FDA could place a hold on these studies, however if it discovers that Cassava manipulated data in order to secure its IND, or if the results of the Phase 2b study were manipulated in any way by the CUNY lab.

Cassava aggressively denies all of the arguments put forward by the authors of the Citizen’s petition, many of whom are named amongst the defendants in Cassava’s lawsuit. In its press release announcing the lawsuit Cassava comments:

The complaint identifies over 1,000 false and defamatory statements made by the Defendants in submissions to the U.S. Food and Drug Administration as well as “reports” and presentations that Defendants published online or on social media.

According to the complaint, “Defendants saturated the market, investors, federal agencies, testing sites, and others with their false and defamatory message about Cassava. Defendants did not have any real or valid concerns with Cassava, its foundational science, or its tests. Defendants engaged in their saturation campaign to profit based on a decline in Cassava’s stock price.

Cassava has made a new hire within its legal department, adding the former Global Head of Litigation and Government Investigations for Alcon to its staff in October this year, and it seems clear from the lawsuit that Cassava intends to defend itself vigorously.

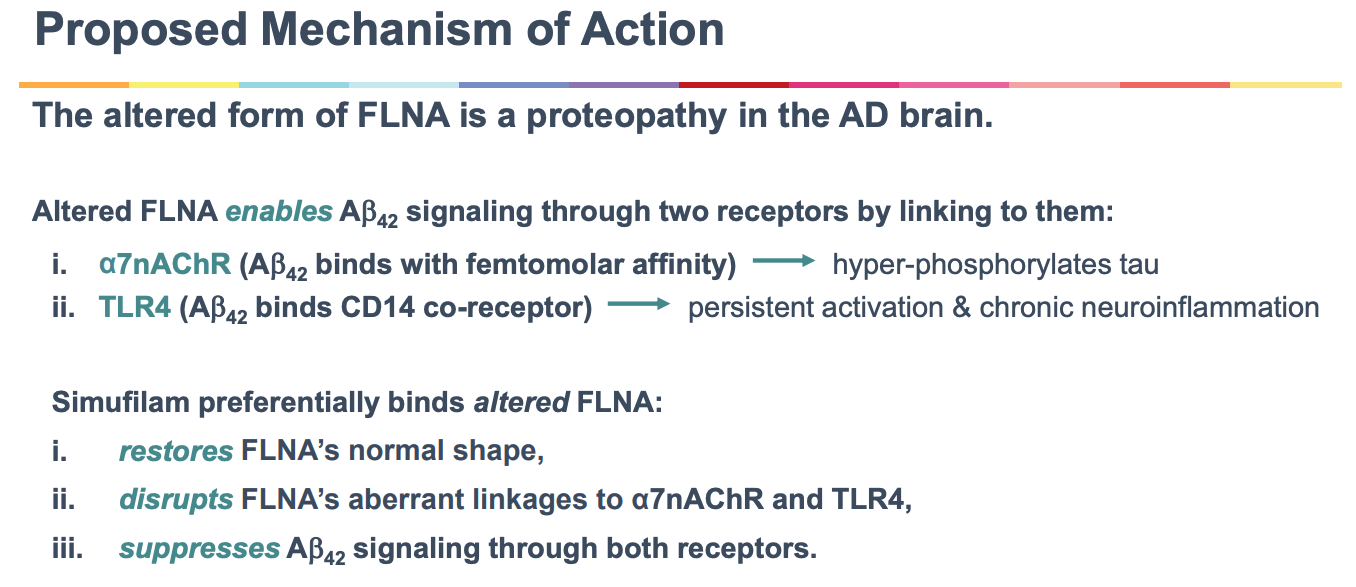

With that said, it is notable that Cassava’s latest investor presentation contains no references to data generated in any of its previous clinical studies – neither the Phase 2b nor the Open Label study. Instead, there is a slide briefly outlining Simufilam’s mechanism of action

Simufilam proposed mechanism of action (investor presentation)

Simufilam’s MoA has long been a source of controversy, given how little research there has been into Filamin-A – a “scaffolding protein” that negatively affects downstream signalling in Alzheimer’s patient’s brains, according to Cassava – by any other pharmaceuticals or biotechs.

The vast majority of evidence to show that targeting Filamin-A can help to reduce cognitive decline has been supplied by Cassava research scientists plus the clinical data from studies of Simufilam. Whilst Cassava may argue that this makes Simufilam a uniquely valuable drug, Cassava shorts have suggested the reason for this is that the thesis is bogus.

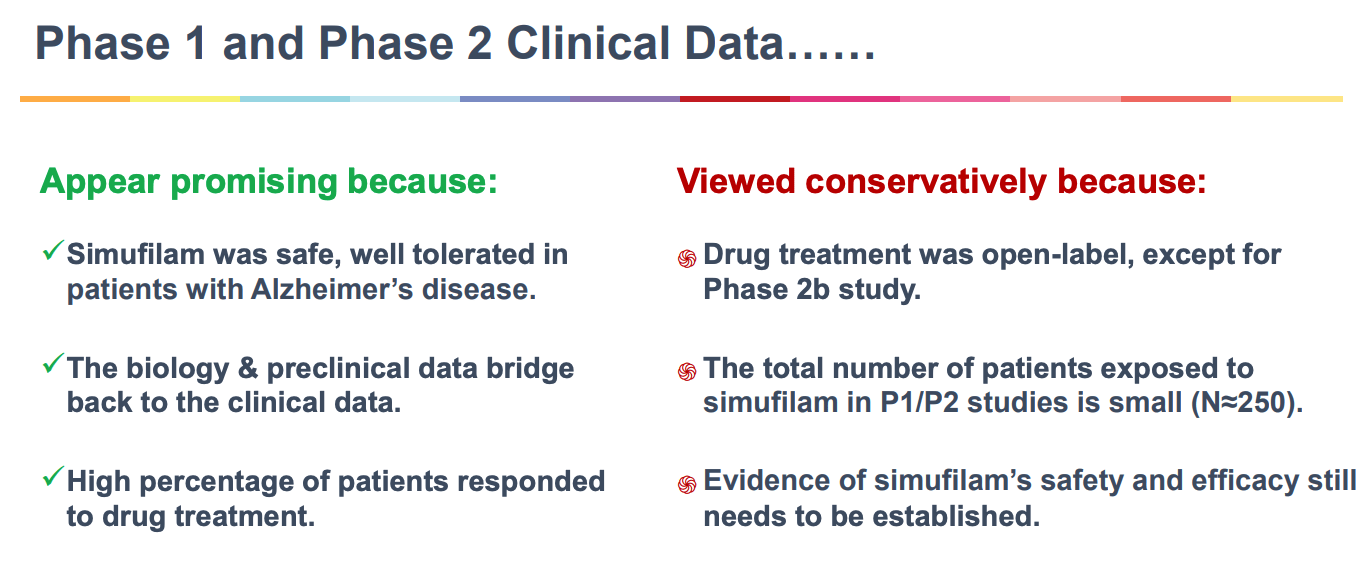

Cassava’s latest presentation attempts to present a balanced view of the current state of play after Phase 1 and 2 studies have been completed in a separate slide:

Cassava balanced Phase 1/2 study conclusions (investor presentation)

It may seem odd that Cassava is no longer quoting its own study results in its corporate presentations.

Some of the research published by Cassava in peer-reviewed journals pertaining to Filamin-A and the beneficial effects of Simufilam has been retracted since the Citizen’s Petition was filed.

Notably – according to Motion to Dismiss documents apparently put together by Cassava’s legal team and shared online – by Molecular Neurodegeneration, at the author’s request, and also by PLOS One, which retracted five articles published by Dr. Wang, and Alzheimer’s Research & Therapy. Several other publications found no evidence of data manipulation, however, and there is still no clear resolution to the debate.

There is also apparently an investigation into Dr. Wang’s lab that remains ongoing, and some Cassava shorts continue to believe that the Securities and Exchange Commission (“SEC”) and Department of Justice (“DoJ”) could decide to, or already are, investigating the company.

Looking ahead into 2023, the picture remains uncertain. Cassava continues to stand by its data in public and via its lawsuit against its accusers, but at the same time, has stopped referencing its clinical study results in its investor presentations.

Is management pinning all of its hopes on the positive outcome of its Phase 3 studies, hopeful that their success will prove the Filamin-A mis-folding thesis, and end the scrutiny of its earlier data?

3. Can Cassava Deliver The Data That Silences The Doubters in 2023?

I suspect my conclusion above may be accurate. Having made it to the Phase 3 study stage, having agreed trial protocols with the FDA, and having now enrolled >750 patients out of a total of ~1,750, with the first Phase 3 study lasting only 52 weeks, Cassava management can nearly see the finish line.

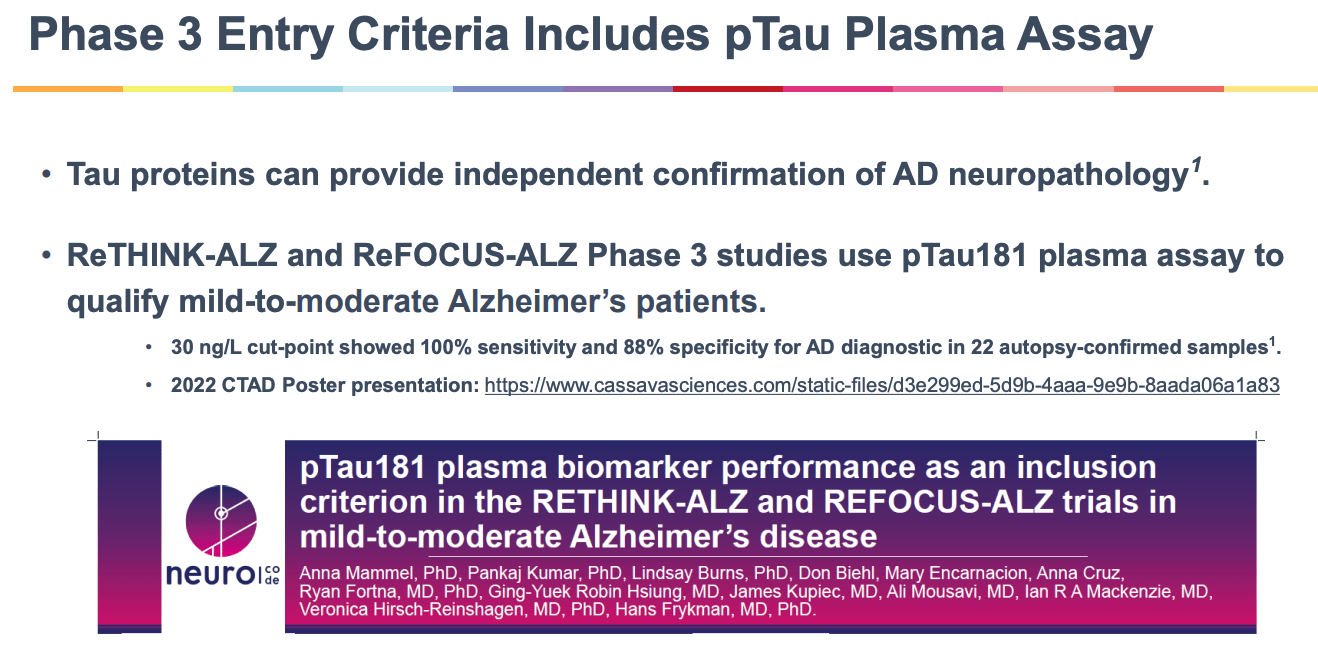

These two studies will surely provide enough data for the FDA and the scientific community to make an informed judgement about the efficacy and safety of Simufilam and whether it works. It is worth noting the unique entrance criteria for the Phase 3 studies as shown below:

Phase 3 entry criteria (investor presentation)

In a poster presentation Cassava evaluates performance of pTau181 plasma biomarkers as an inclusion criterion in RETHINK-ALZ and REFOCUS-ALZ, concluding:

This pTau181 assay appears to be performing well as a screening method for inclusion of mild-to-moderate AD subjects in two large Phase 3 clinical trials.

Besides this screening process, the endpoints of the trial ought to enable close, if not direct comparison with rival companies’ late stage studies, i.e. Biogen / Eisai, Eli Lilly, Anavex, etc. and coupled with its clean safety profile, if the data are positive it is hard to see how the FDA avoids approving the drug, creating a sensational win for Cassava.

Investors are expecting more Open Label data in the coming days, and that may provide a near term price catalyst, although everyone is aware of the limitations of this study, meaning positive data won’t necessarily be rewarded, although data inferior to what has gone before could be punished.

There will also be data made available – most likely in late 2023 – from a Cognition Maintenance Study (“CMS”) conducted by Cassava which compares cognition in ~100 AD patients who continue vs discontinue the Open Label study, the primary endpoint being change in ADAS-Cog.

Regardless, the Phase 3 studies still appear to be the most comprehensive answer to whether Simufilam is effective or not given its placebo arm, endpoints, and size. Cassava completed a ~$50m registered direct offering of shares in November, after reporting a cash position of $175m as of Q3’22, and a cash burn for the year of $57m, so the company ought to be able to complete these trials with available funds.

It may seem odd that Cassava has completed a fundraising at $30 per share, when its share price would undoubtedly soar on the next positive data readout – does this suggest that management is losing confidence in Simufilam and its data?

Cassava has certainly changed the way it is presenting Simufilam, either in response to the constant outside criticism, or because management may have less confidence in its prior studies, but there has been some recent insider buying to give the bulls some confidence also.

We don’t know if there will be any interim RETHINK-ALZ or REFOCUS-ALZ data in 2023 – Cassava may be in no rush to share data given it does not need to raise funds immediately and has a far bigger achievement in sight i.e. a full approval of the drug which would silence all of the doubters.

In answer to may own question – we may be no closer to knowing the ultimate fate of Simufilam at the end of 2023 than we are at the end of 2022.

Conclusion – Another Year of Thrills, Spills, and FUD Looms For Cassava

2023 could be the year that we see two Alzheimer’s drugs approved in the shape of Biogen / Eisai’s Lecanemab and Eli Lilly’s Donanemab, but that does not necessarily mean that everyone will embrace the amyloid beta thesis or demand the drug for their patients.

Safety concerns persist creating doubts about whether the level of efficacy justifies the risk of administration. So long as that debate exists insurers and the Centers for Medicaid and Medicare (“CMS”) may refuse to provide reimbursement for either drug, just as they did with Aduhelm.

There is still a huge gap in the market for a more effective disease modifying Alzheimer’s Therapy that Simufilam can fill with its cleaner safety profile and efficacy, if proven in a placebo controlled trial.

That makes for a massive opportunity for investors buying Cassava stock at a price <$30 to make gains of >500%. If Simufilam meets endpoints in its Phase 3 studies, Cassava’s share price ought to soar higher than >$150, which would value the company at just over $6bn market cap.

Given the company would have a double-digit billion dollar selling asset on its hands, and that a Pharma company like Vertex (VRTX) for example has a >$70bn market cap based on revenues per annum <$8bn, the upside opportunity should Phase 3 studies succeed is practically uncapped.

Witness for example the 300% gain in the share price of Madrigal Pharmaceuticals (MDGL), after its lead asset Resemtirom met Phase 3 endpoints in a study of the drug in nonalcoholic steatohepatitis – a similar market opportunity to Alzheimer’s Disease.

With that said, Cassava faces significant threats on all fronts. The company is no longer quoting its study data in its presentations, could lose its lawsuit against the authors of the Citizens Petition, be formally investigated by the SEC, DoJ, or FDA, see a clinical hold placed in its studies, or fail to reproduce positive data with its final Open Label data or CMS study data.

With a market cap valuation of >$1bn Cassava stock is not exactly cheap at $28 per share, either. Simufilam is the company’s only drug and if it is proven not to work then Cassava stock will fall by >90% because there will be no value left in the company other than a diagnostic test, SavaDx, development of which is currently on hold.

Cassava sadly lost a valued and long-time member of the company, Nadav Friedmann PH.d, who passed away this month. The company will undoubtedly continue to divide opinion and be the subject of significant speculation in 2023, and I would not be surprised to see the share price lose another 50% of its value if the latest Phase 2 data underwhelms.

I can also see there being price spikes in 2023 on speculation around legal matters, positive Phase 2 data, and any information pertaining to the RETHINK-ALZ or REFOCUS-ALZ studies.

Ultimately, by Cassava standards, 2022 did not bear witness to too much share price volatility and I think that pattern may continue in 2023, despite the hostility of bulls and bears. 2024 may be the make or break year for the Cassava shorts and longs, by which time the evidence either for or against the drug will likely be conclusive.

(Full disclosure – I hold a very small (>$150) position in Cassava but have no plans to increase my holding).

Be the first to comment