Ratnakorn Piyasirisorost/Moment via Getty Images

Summary

I see a 20% upside to Carrier Global (NYSE:CARR). The HVAC market is expanding globally and is driven by a replacement cycle, particularly in the residential sector, as summers are getting hotter and winters are getting shorter, which increases the likelihood of breakdowns and necessitates emergency replacements. CARR is well-positioned to capitalize on this growth due to its global reach, breadth of offerings, and strong relationships with distribution partners.

Company overview

CARR is a world-renowned provider of HVAC (Heating, Ventilating, and Air Conditioning) systems, commercial refrigeration equipment , and Fire & Security systems for buildings of all types and sizes.

Replacement cycle timing

To me, CARR is a bargain-priced way to gain exposure to the expanding HVAC market around the world, which also benefits from a robust self-help tailwind. The majority of the HVAC market in the United States is comprised of replacements, particularly in the residential sector, with new construction making up the remainder of volumes. Due to climate change, summers are getting hotter and winters are getting shorter, which means that HVAC systems in homes and businesses are being run for longer periods of time, increasing the likelihood of breakdown and necessitating an emergency replacement.

Residential and light commercial equipment purchases in developed markets are driven largely by a replacement cycle (products generally last on average 15 years but can be extended with proper maintenance). I believe we are entering the phase where residential replacement will begin, as the last peak of the US housing cycle occurred in 2006 and the last peak of non-residential spending occurred in 2008.

Global scale and opportunity for growth.

In my opinion, CARR has a leg up on the competition in terms of design, production, procurement, sales, and marketing thanks to the company’s global reach and breadth of offerings. CARR is in a better position to capitalize on promising markets and geographies by gaining insight into local situations, rules and regulations, and consumer demands. CARR also benefits from knowledge spill over, which occurs when the company applies the lessons it has learned or the technologies it has formed for one geographical area or client to another, thereby expanding its business in both locations. Apart from the periodic replacement process, the weather has been getting increasingly hotter. Climate change is not merely a problem in the United States and Europe. Due to the global warming, there is a captive opportunity in the final stages of AC unit penetration in developing regions (CARR has 20% exposure in developing markets as of 3Q22). Low penetration rates, soaring standard of living and utilization, and a bigger focus on safety, power efficiency, and environmental protection all point to rising demand for CARR products and services in these areas, creating a fertile ground for expansion.

Accordingly, CARR’s size, prominence, and extensive distribution network afford the company prospects for strategic growth in select international markets. It also provides CARR with exposure to both short- and long-cycle end markets and a wider range of customers to serve.

Strong relationship with distribution partners

CARR’s long-standing partnerships with its global network of channel partners put it in a position to reliably meet the needs of its customers in any market. These connections are often the result of decades of working together to sell products and develop unique solutions for a wide range of clients and uses. CARR has also formed joint ventures and alliances with its partners to improve their alignment of incentives and increase their chances of winning deals as a team.

In my opinion, CARR’s robust relationships are the result of years of hard work, numerous personal connections, and consistent excellence in the workplace. In an industry as dependent on distribution as this one, it’s important not to discount the value of these connections. When it comes to HVAC products, the vast majority of consumers rely on recommendations from others, be they professionals, store employees, or family and friends. Accordingly, recommendations from satisfied customers and reliable channel partners are crucial. Even when CARR don’t sell directly to the end user, CARR is still a provider of choice thanks to the strength of its relationships and the relationships those partners have with end users, as well as the breadth of CARR’s distribution network.

Comprehensive offerings

I believe another key strength of CARR lies in the breadth and depth of the range of products and services it offers across many different markets. CARR’s business model is not reliant on any one item, brand, sector, or consumer, even though many of CARR’s products and brands are (in my opinion) iconic in their respective industries. In my opinion, CARR is the go-to provider for a wide variety of needs because of the wide variety of products and services it offers. The implication is that CARR can target a much wider TAM and stand out in negotiations as a result (when competing for deals). The business can also benefit from diversification in the form of a diversified portfolio (and investors). The replacement cycles that drive CARR’s industry also indicate a clear cyclical trend, as was mentioned earlier. Maintaining a diversified portfolio lessens the impact of short-term challenges in any one region, field of application, or business sector.

Aftermarket sales helps to ease business cycles

As a global company with a long history in the market, CARR likely has a sizable customer base in many of the sectors they serve. As a result, CARR is in a better position to generate on-going income through the sale of service repairs, replacement parts, and products at the end of their useful lives. In addition to the sales from its equipment business, CARR also benefits from the sales of other value-added, both recurring and one-time, services.

Long-term bull case stays intact

The HVAC division was largely responsible for CARR’s 3Q22 segment EBIT exceeding expectations by 2% in the company’s most recent earnings report. This is a very positive outcome, and I am heartened to see a price tailwind of about $50 million for the quarter. Splitting the HVAC segment up, in residential HVAC, CARR grew by the high single digits, price growth was generally in line with industry peers, meanwhile volumes dropped by the middle single digits in the third quarter, suggesting distributor de-stocking.

When I think about the years after 2022, I am encouraged by the robust bookings for commercial HVAC systems and the favorable price and cost environment (which has grown double digits over the past 7 quarters). The majority of my monitored KPIs are also performing admirably. Sales of heat pumps have increased by 30% in the third quarter, and growth in aftermarket sales and other important markets has also continued unabated. All of these things lend credence to my extensive thesis and show that CARR is making good decisions and putting them into action.

Valuation

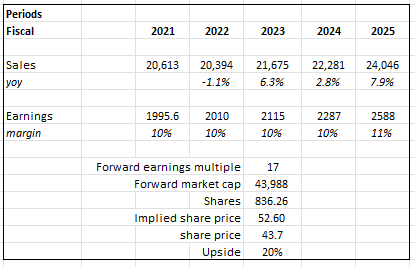

CARR has a 20% upside, in my opinion. According to consensus estimates, CARR will generate $24 billion in revenue and $2.6 billion in earnings in fiscal year 25. Based on my thesis, I believe these estimates are reasonable, and CARR should have no trouble meeting them. Continuous printing of good results could be a catalyst for CARR valuation to improve further, resulting in a “beat and rise” movement. Even if valuation does not improve, I believe the upside from here is not too bad at 17x forward earnings.

Own calculations

Risk

Cyclicality in the residential side

My model predicts a slowdown in growth in FY24 because by then, some favorable tailwinds on the mix will have normalized, but there is still an underlying problem. The residential sector is likely to go past the peak of it cycle soon. In the near term, we may see a decline in the high-single digits range for the residential HVAC market due to weak new housing fundamentals and a continuing tick down in consumer confidence.

Conclusion

Summers are getting hotter and winters are getting shorter, increasing the likelihood of breakdowns and necessitating emergency replacements, both of which contribute to the expansion of the HVAC market worldwide and drive a replacement cycle, particularly in the residential sector. CARR is positioned to take advantage of this growth thanks to the company’s global presence, extensive product line, and solid relationships with distribution partners. There is also a large market for CARR’s products and services in emerging economies, where AC unit penetration is low but where demand is expected to grow due to rising living standards and a focus on safety, power efficiency, and environmental protection. CARR will be able to consistently meet the requirements of its customers across all markets thanks to its robust global network of channel partners and the trust it has built up with them over the years.

Be the first to comment