Paul Morigi/Getty Images Entertainment

Investment Thesis

Due to macro headwinds common to the entire industry, as well as due to the specific problem of the absence of a permanent CEO, The Carlyle Group (NASDAQ:CG) faced challenges in fundraising in the fall. While the stock has rebounded significantly since then, the company is still trading well below its highs and at a discount to the industry average.

Given that macroeconomic turbulence is temporary and the absence of a Chief Executive has little effect on Carlyle’s operations thanks to co-founder and seasoned manager William Conway, we expect the company to navigate these headwinds successfully.

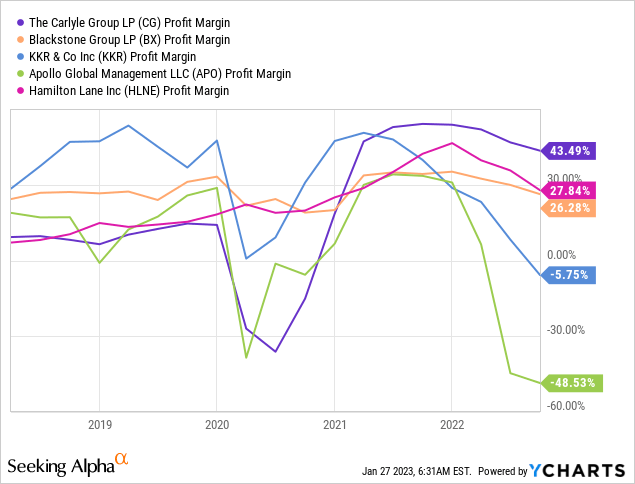

And while Carlyle’s financials have declined, they are showing more resilience than CG’s competitors. In addition, the company has best-in-class margins and a strong balance sheet that allow it to reward shareholders with dividends. We believe that the discount to the industry average is not justified. We rate shares as a Buy.

Company Profile

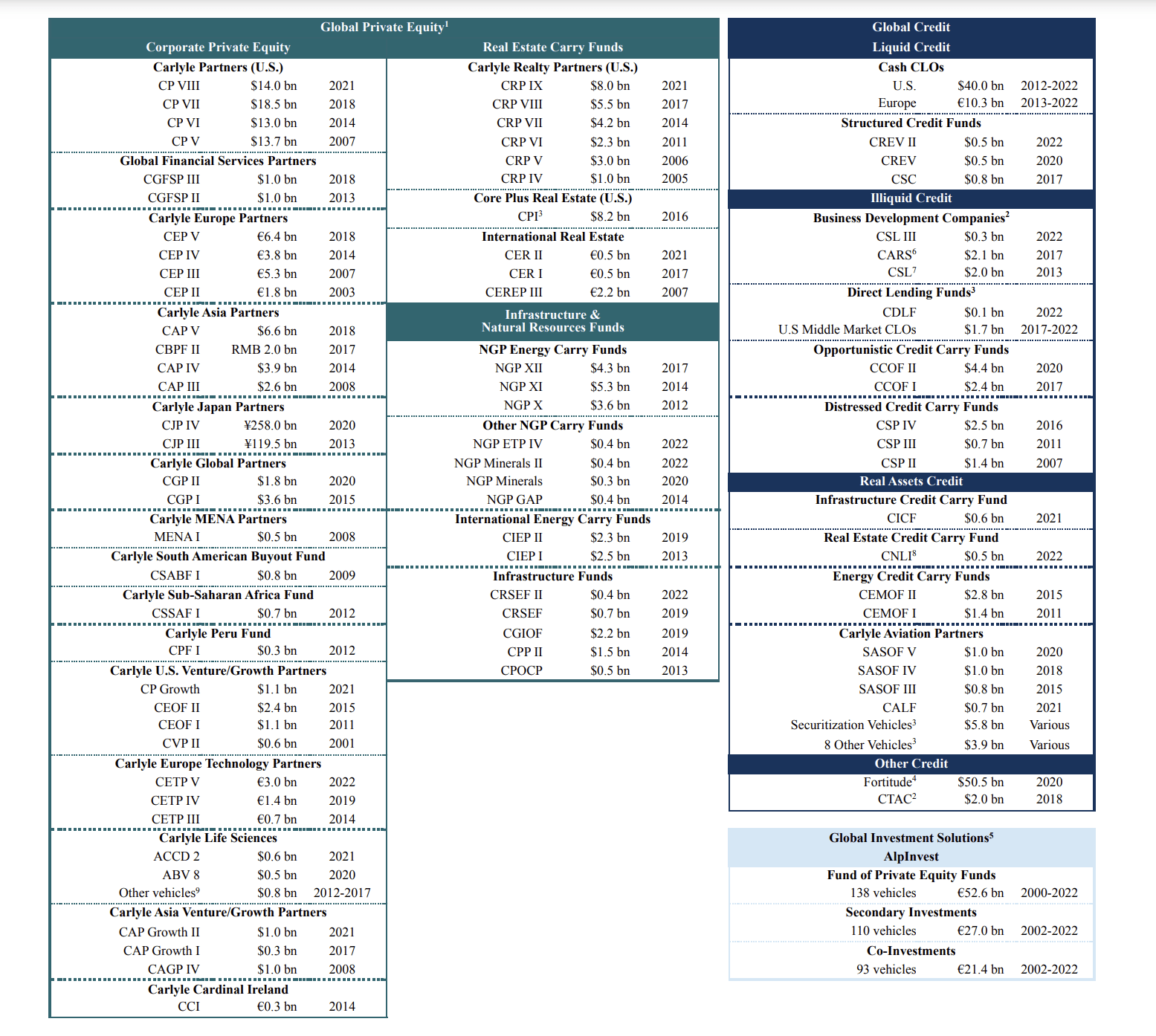

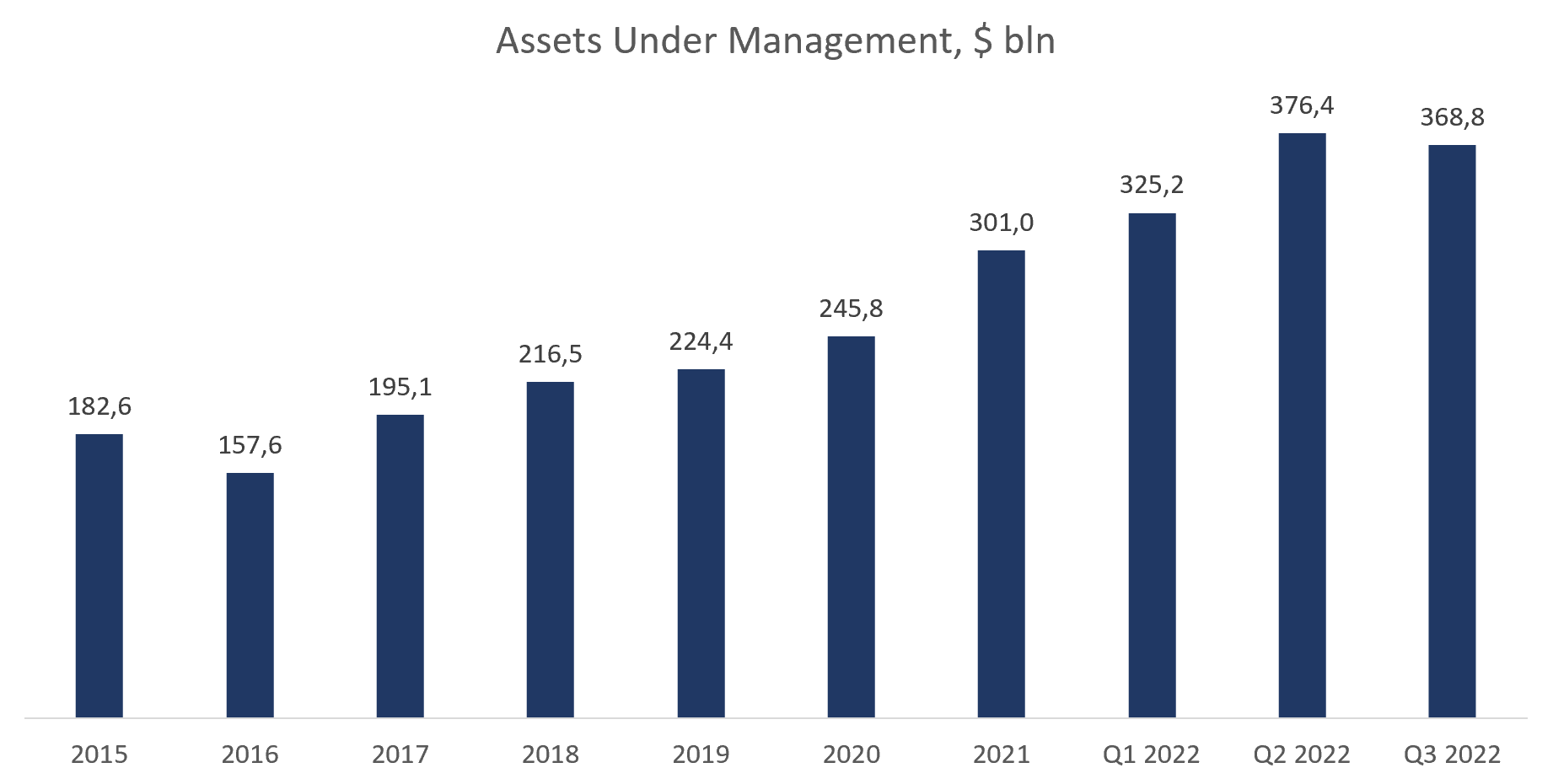

The Carlyle Group was founded by William E. Conway Jr., Stephen L. Norris, David Rubenstein, Daniel A. D’Aniello, and Greg Rosenbaum at the Carlyle Hotel back in 1987. Since then, the company has gone from being an investment boutique with $5 million of financial backing to one of the largest private equity firms in the industry with total assets under management of $368.76 million. Carlyle operates in three segments:

- Global Private Equity. In this segment, the company manages LBO funds, the middle market, growth capital, and real estate funds. The volume of assets under management is $164 billion, of which $106 billion is fee-earning AUM.

- Global Credit. This segment advises funds and vehicles specializing in debt financing, including loans and structured credit, distressed credit, infrastructure debt, direct lending, and insurance solutions. The segment has $141 billion in total AUM, including fee-earning AUM of $117 billion.

- Global Investment Solutions. In this segment, Carlyle manages a fund of private equity funds, as well as advises secondary and co-investment activities. GIS accounts for $63 billion in AUM and $36 billion in fee-earning AUM.

10-K filing

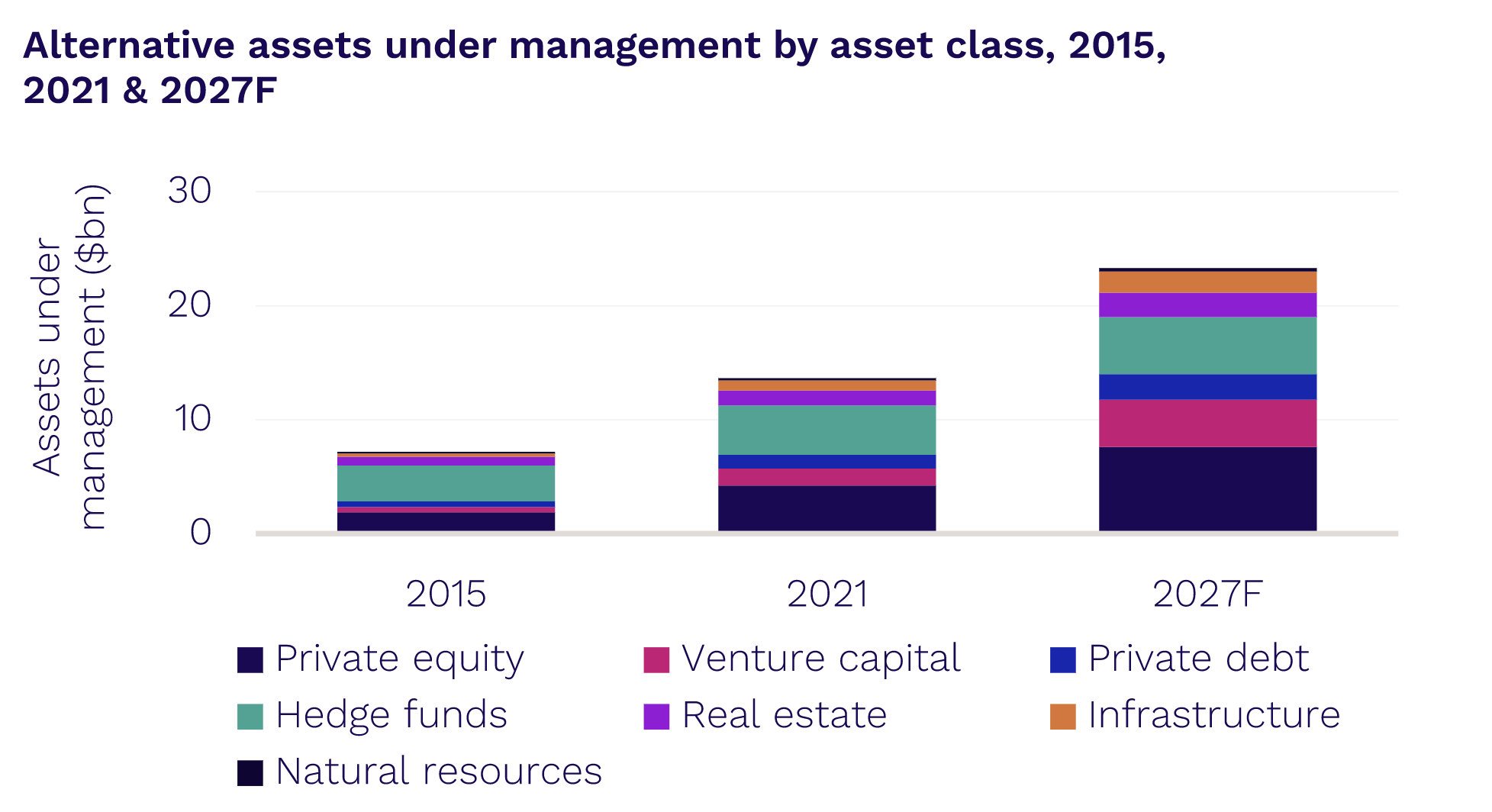

Industry Potential

According to Preqin Global Reports, the value of AUM under alternative assets managers was estimated at $13.7 trillion in 2021 and is expected to reach $23.3 trillion in 2027, implying a compound annual growth rate of 9.3% over the forecast period. About half of the alternatives’ AUM will come from private equity and venture capital, making PEVC the largest asset class in this category.

Preqin

The private equity industry is showing resilience to macroeconomic headwinds. According to Preqin’s survey, most investors value the diversification and high returns per unit of risk accepted that private equity provides them. 46% of investors plan to keep their allocations at the current level in the next 12 months, and 30% plan to increase their investments. The Ernst & Young survey also shows favorable results. According to EY, 64% of investors plan to keep their private equity allocations at the same level, and 28% plan to increase investments.

It should be noted that the respondents in these surveys were institutional investors. Large financial institutions are characterized by high inertia – investment decisions go through careful planning and many bureaucratic steps. It is unlikely that investors’ coming year plans will be significantly adjusted.

The Challenges are Temporary

Despite gains in recent months, Carlyle is still trading well below its highs and at a discount to the industry average. This dynamic is due to:

- Deteriorating market conditions and, as a result, a decrease in appetite for risky assets;

- Decreased financial results of the company;

- The absence of a permanent CEO;

- Fundraising slowdown.

As noted earlier, despite the monetary policy tightening, we believe that the demand for alternative investments will continue. But even assuming that macroeconomic turbulence takes away all risk appetite, PE firms can navigate headwinds with confidence, as their funds are formed for 5-10 years, and the average duration of recessions is only ten months. That is, Carlyle will not face a sharp outflow of AUM and a reduction in management fees.

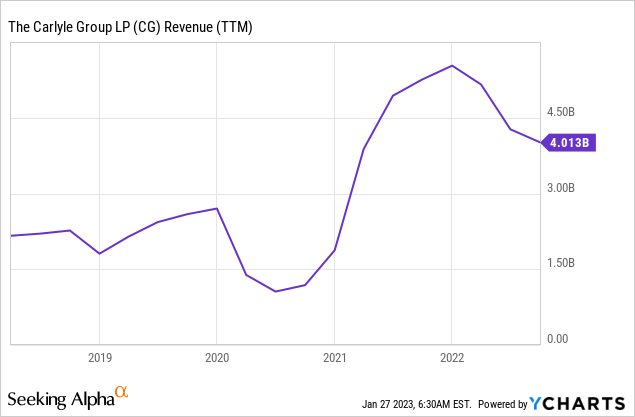

However, the company’s financial performance declined significantly. Thus, according to the results of the last reporting period, Carlyle’s revenue over the past nine months decreased by 45.2%, due to a significant drop in performance allocations, which depend on the results of managed funds. The results of private equity funds have always been highly volatile: performance declines when the market is bearish, but also quickly recovers during periods of optimism. Given the permanent nature of management fees, the question is not whether Carlyle will recover, but when it will do. And when the first signs of a recovery in activity appear, you should already be holding stocks.

Since the notorious firing of Kewsong Lee in August 2022, Carlyle’s capitalization has fallen by more than $1 billion. The position of CEO was temporarily taken by William Conway, co-founder of Carlyle. The absence of a full-time Chief Executive is a reasonable reason to stay away. In many ways, CEO determines the direction of a company’s development. However, in this case, in our opinion, the market overestimates this factor’s impact, since the co-founders who laid the foundation of the company are still actively involved in its life. William Conway has served as CEO for many years and is capable of continuing to run the company successfully until a permanent Chief Executive is found.

The quintessential of the previous challenges were the fundraising problems that Carlyle faced this fall. In the third quarter of 2022, the company raised only $6 billion compared to $10 billion a quarter ago. As a result, dry powder, capital available for investment, fell 9% to $74 billion and total assets under management declined by 2%.

Created by the author

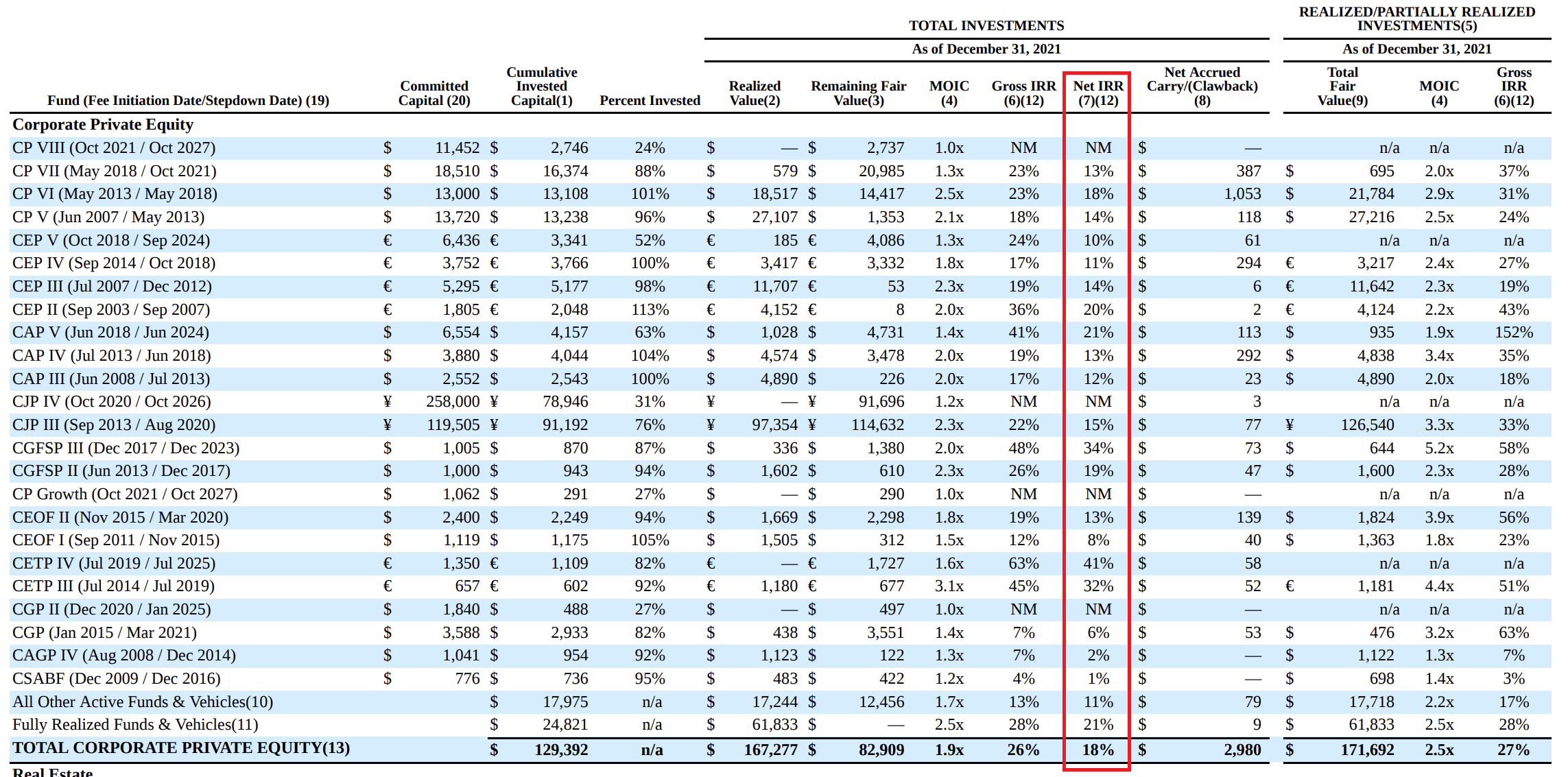

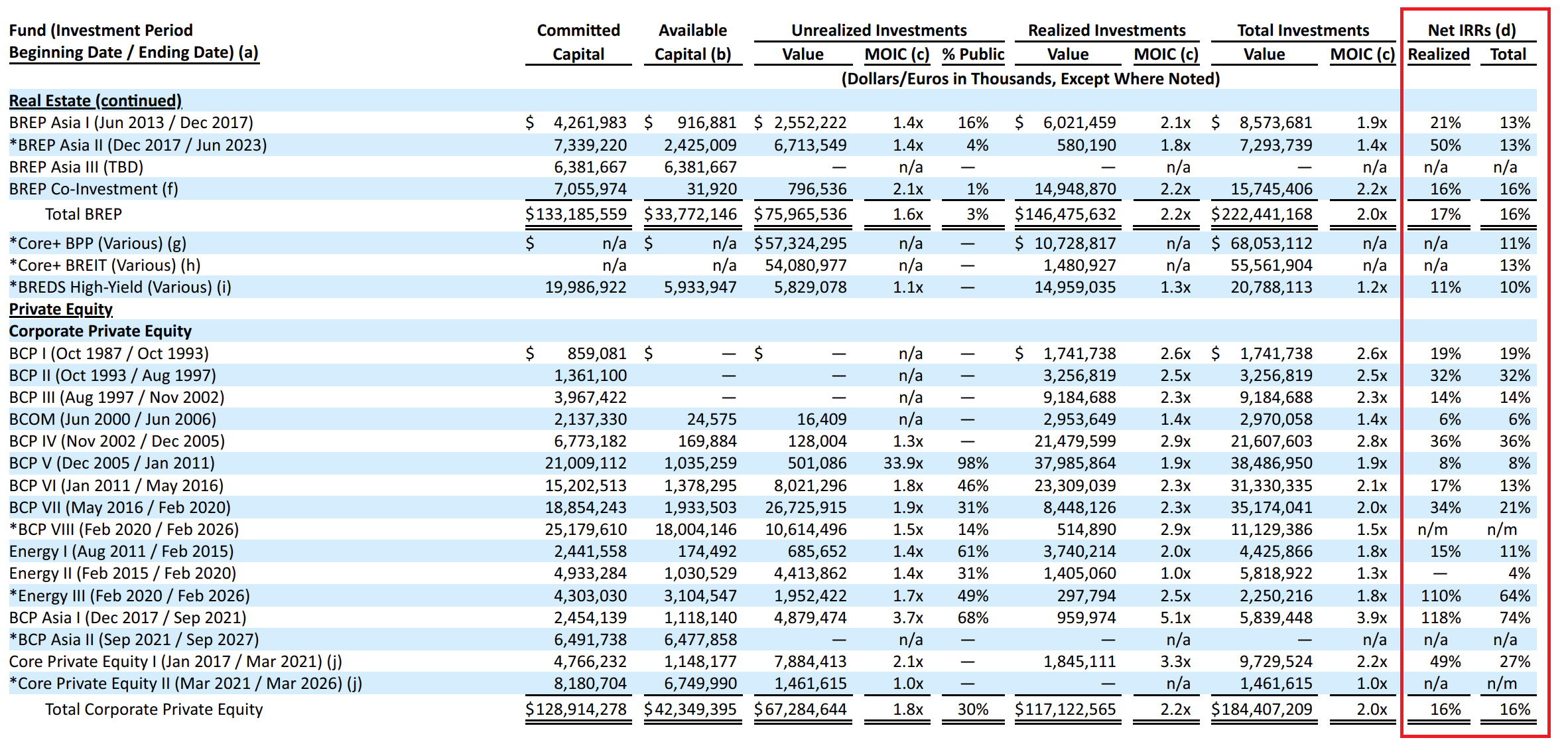

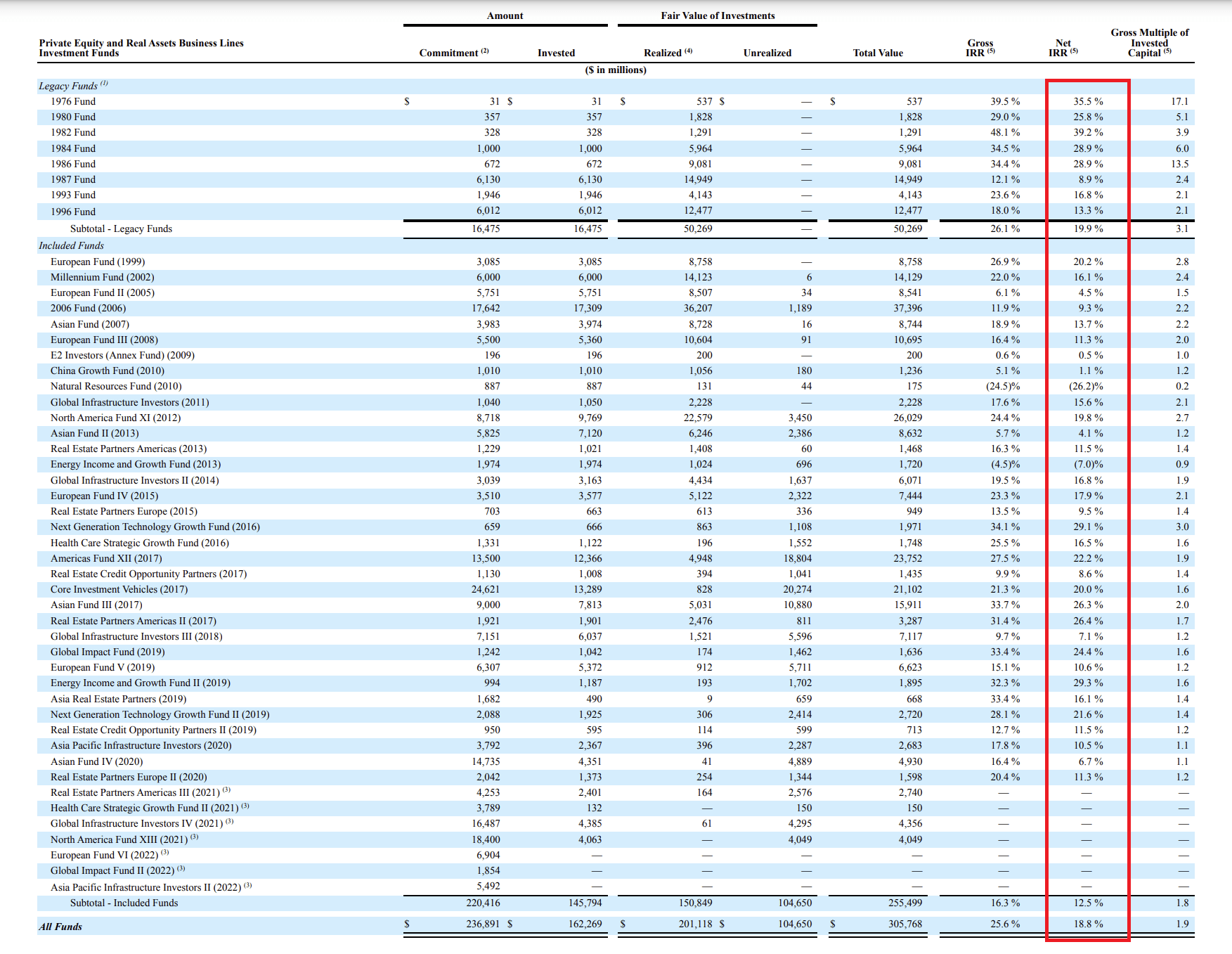

We see no other objective reasons for fundraising challenges. The company hasn’t experienced any major scandals, and Washington DC ties give Carlyle a solid reputation. In terms of returns, the funds managed by the company are also competitive.

Net IRR of CG’s funds (10-Q filing) Net IRR of Blackstone’s funds (10-Q filing) Net IRR of KKR’s funds (10-Q filing)

Probably, the deterioration of the macro environment and the absence of a permanent CEO were the decisive factors that influenced fundraising. Given the temporary nature of the first challenge and the tiny effect of the CEO’s factor on Carlyle’s operations, we expect the company will successfully navigate these headwinds.

Financial Performance and Capital Allocation

Although Carlyle’s financial results declined significantly, they proved to be more resilient than those of competitors. Thus, according to the last quarter’s results, fund management fees increased by 31.5% to $535.9 million, total investment income decreased by 62.8% to $422.3 million, and total revenue amounted to $1.09 billion, 33.6% less than a year earlier. In comparison, KKR’s (KKR)’s total revenue decreased by 58.5% in the same period, while Blackstone’s (BX) lost 83%.

The company ended the quarter with a net income of $280.8 million, down 47.3% from a year earlier. A significant portion of Carlyle’s variable costs is performance allocations and incentive fee-related compensation. The loss in revenue was largely offset by cost cuts. As a result, Carlyle demonstrates the best margin among competitors.

Carlyle has a healthy balance sheet, with debt obligations of $2.24 billion, cash and cash equivalents of $1.36 billion, and net debt of $873 million, well below trailing twelve months net income of $1.75 billion.

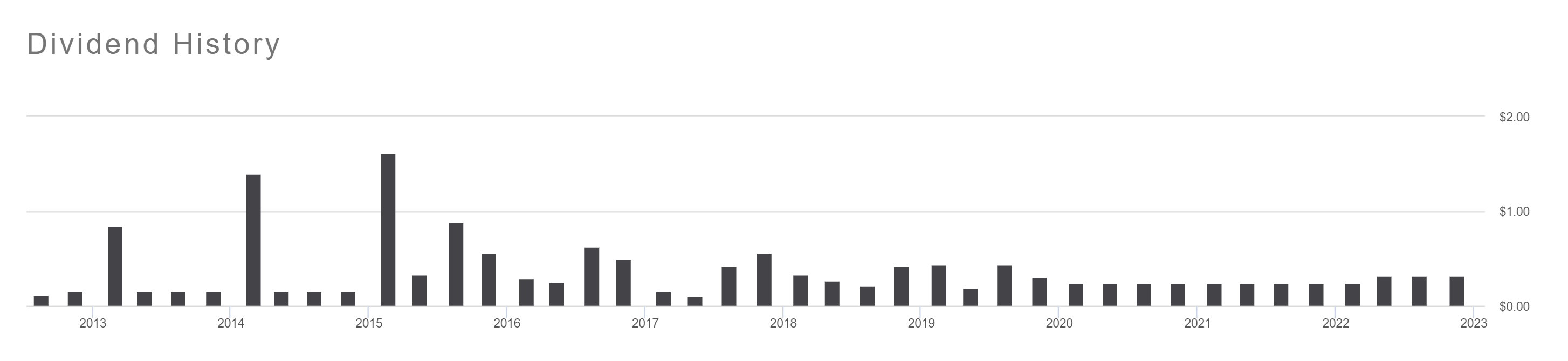

The company is able to not only maintain payouts but also increase them, as the current payout ratio is only 28.9%. It is worth noting that Carlyle has been paying dividends consistently for more than a decade. The firm has maintained a dividend even into 2020.

Seeking Alpha

Comparable Valuation

Despite relatively strong financials, industry-leading margins, strong balance, and stable dividends, Carlyle trades at a discount to major competitors Blackstone, Apollo (APO), KKR, and Hamilton Lane (HLNE).

| P/E Non-GAAP | Forward P/E | P/B | |

| The Carlyle Group (CG) | 6.61x | 8.27x | 2.10x |

| Blackstone (BX) | 16.15x | 18.57x | 8.70x |

| KKR & Co. (KKR) | 12.11x | 14.39x | 2.91x |

| Apollo Global (APO) | 14.55x | 13.30x | – |

| Hamilton Lane (HLNE) | 18.52x | 21.13x | 7.36x |

(Source: Seeking Alpha)

This is partly due to the lower growth rate of fee-earning AUM. However, the difference in dynamics is not significant enough to justify a multiple discount.

Created by the author

The average forward P/E multiple for the companies in our sample is 15.1x, which implies an upside potential of about 82%. Given the challenges Carlyle is facing, a 25% discount can be taken into account as a safety margin. Thus, a valuation at 11.3x forward earnings seems reasonable, implying an upside potential of about 37%.

Conclusion

The alternative asset management industry has shown impressive double-digit growth in recent years and is expected to continue to grow in the future. However, the market is also recognizing the outlook for the industry – PE firms trade at double-digit multiples. The Carlyle Group is an exception: the company trades at a significant discount to the industry average, which, in our opinion, is not justified. Given the temporary nature of the challenges faced by the company, the relative strength of its financial performance, a strong balance sheet, and stable dividend payments, we are bullish on Carlyle.

Be the first to comment