We Are

Alternative credit may provide outperformance during periods of rising interest rates – Invesco

While interest rate increases have experienced decelerated growth, higher rates are here to stay. And in this era wherein traditional credit becomes increasingly expensive, alternative credit becomes increasingly attractive.

The Carlyle Group (NASDAQ:CG) has capitalized on this trend, expanding its debt offerings with its global credit business beating its previous record by nearly 50% to fundraise $10.1 bn in capital for 2020.

As such, the focus on credit, in addition to the strength of Carlyle’s core private equity business, I believe the company has positioned itself well for future success.

Introduction

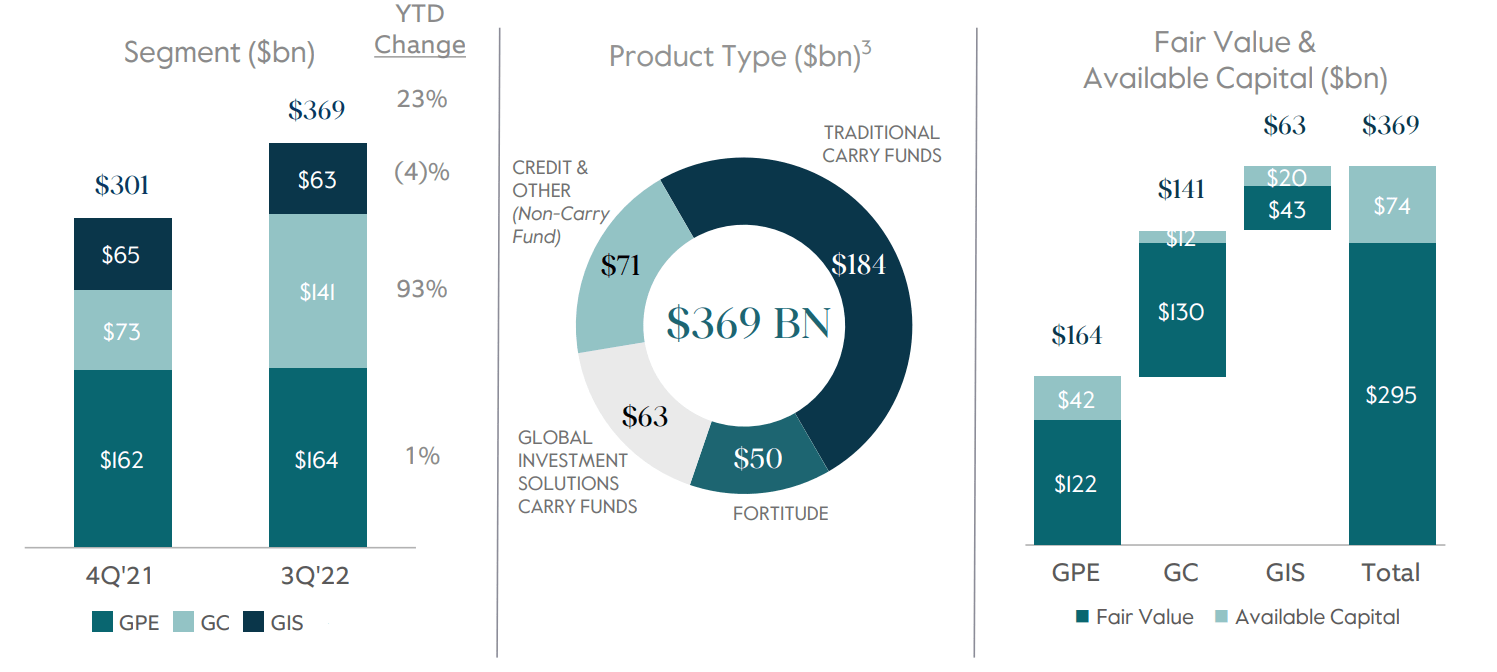

The Carlyle Group is a multinational private equity, alternative asset management and financial services corporation, with upwards of $376bn in AUM.

The firm is principally comprised of three segments; the bulk of its business- Global Private Equity, which accounts for $3.41bn of the company’s Q4 revenues; Global Credit, which accounted for $161mn in revenues, up from $107mn in Q3; and Global Investment Solutions, which earned the company $319mn.

Carlyle Segmentation (Carlyle Q3 Investor Presentation)

On a more granular level, Carlyle’s strategic plan involves a base fundraising target of $130bn, inorganic growth and cash flow via M&A, and geographically diverse growth, particularly across its India and China markets.

Valuation & Financials

General Overview

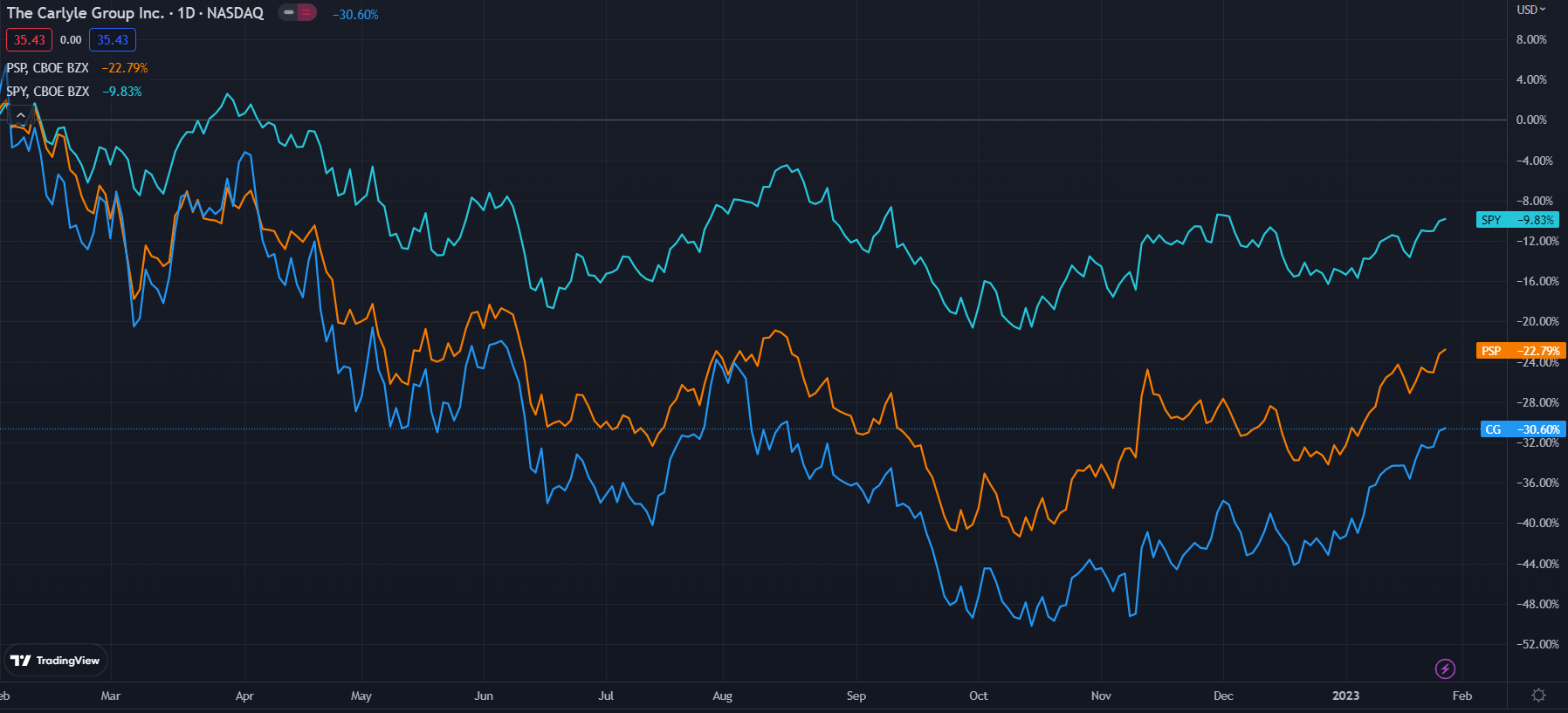

Although they have experienced a 20% price appreciation in the past month, I maintain that Carlyle remains fundamentally undervalued, underperforming against the private equity index, PSP (PSP), and the broader market.

Carlyle (Dark Blue) vs Industry (Orange) & Market (Teal) (tradingview.com)

Carlyle’s price decline was likely driven by macro events- particularly rising interest rates which materially impacted their private equity business- and subsequent margin compression and revenue loss.

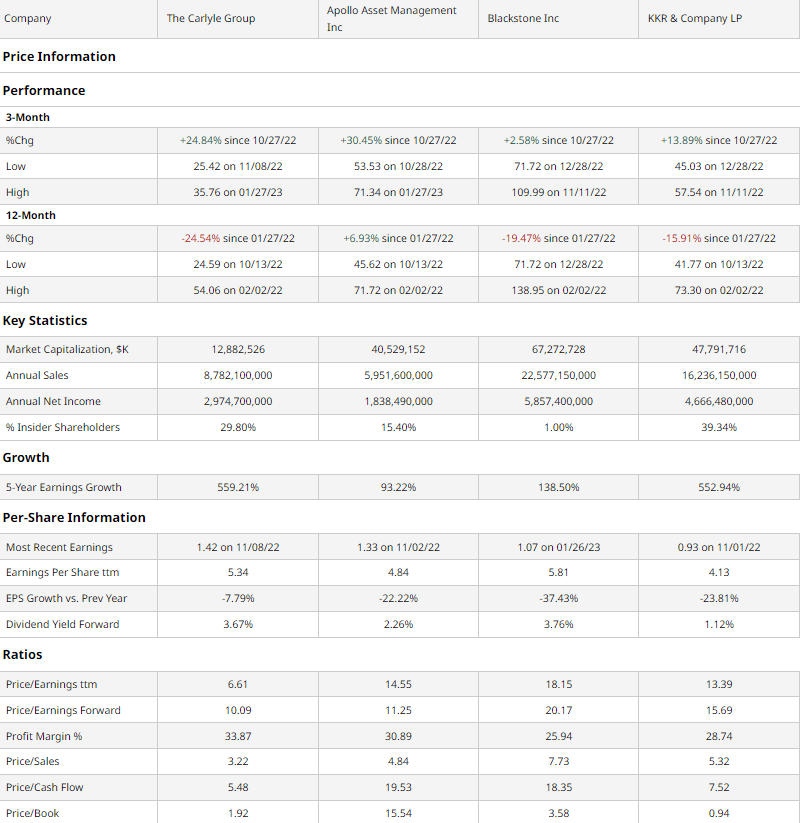

Comparable Companies

At a CAGR of ~10.2%, private equity comprises one of the fastest-growing sub-sectors within financial services; this comes on the heel of historically low-interest rates and increased demand for alternative asset class investments for pension funds, endowments, and high net-worth individuals. The companies leading this growth include; Blackstone (NYSE:BX), which particularly focuses on investment real estate; KKR & Co. (NYSE:KKR), a leader in LBO transactions; and Apollo Global Management (NYSE:APO), famous for their recent acquisitions of Athene, Yahoo!, and Tenneco.

barchart.com

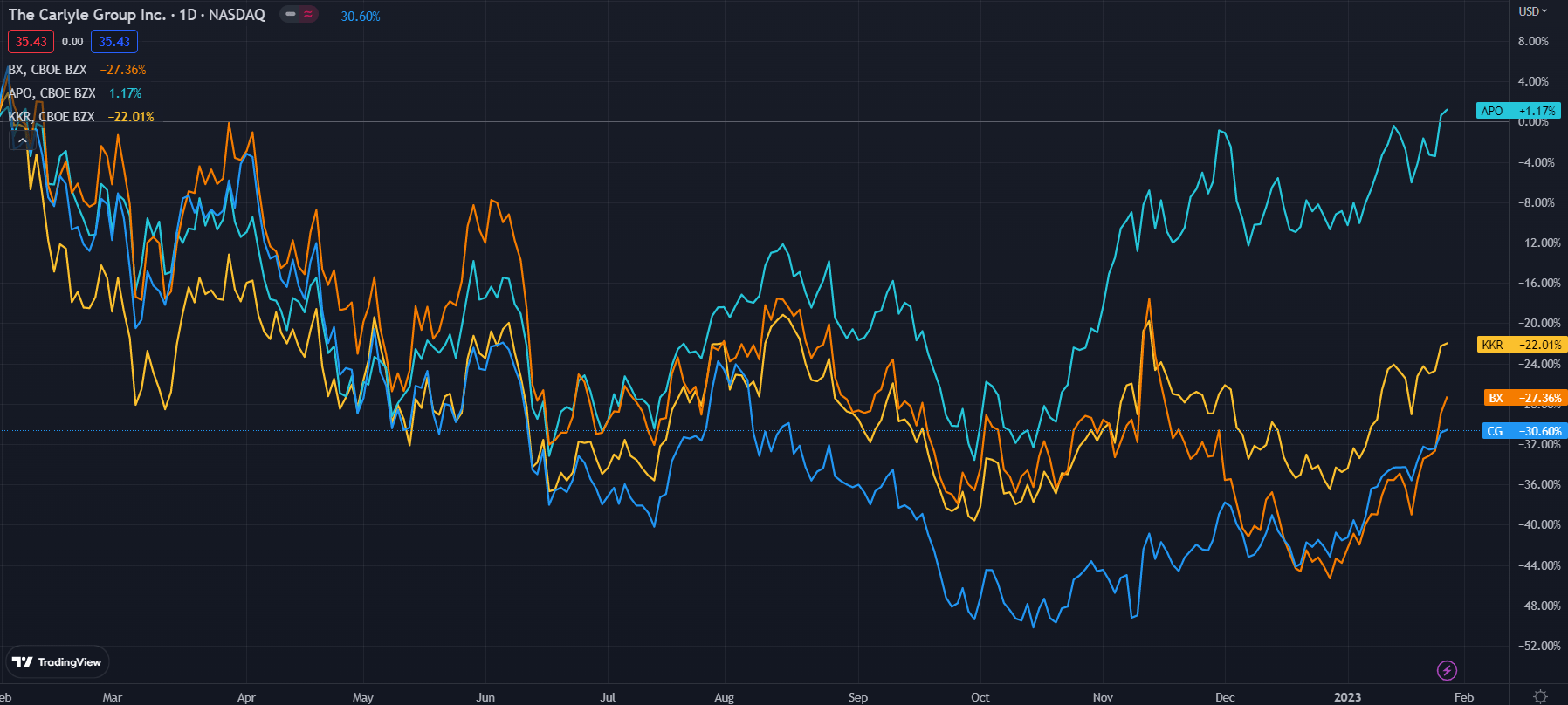

As we can see above, while Carlyle has experienced poor share price action in the trailing twelve months, they have recovered at a velocity second to only Apollo.

Yet, the company sustains their undervaluation, experiencing the greatest 5Y earnings growth while still being relatively undervalued using multiples such as P/E, P/S, P/CF, etc. Furthermore, Carlyle retains the largest margins of the competition, thus complementing the flexibility of the business in turbulent macroeconomic times.

I expect a reversion to the mean for Carlyle’s stock price in the medium term and believe that their higher margin credit business will only enhance margin expansion and the company’s overall value proposition.

Carlyle (Dark Blue) vs Competition (tradingview.com)

Valuation

Though Carlyle is aggressively moving into the alternative credit business, their primary revenue stream continues to be private equity- as such, I decided to use a discounted cash flow on the company.

According to my DCF calculations, at its base case, Carlyle is undervalued by ~22%, with its fair value being $45.55. The model operates on an FCFE and assumes a discount rate of 9%- which is the Carlyle Group’s WACC.

AlphaSpread

Carlyle’s undervaluation is further supported using a relative value analysis tool, which employs multiples such as P/S, P/E, and P/B, which, at its base case, estimates Carlyle is undervalued by nearly 19%, thereby being worth ~$43.76.

At a mean value, the firm thus should be valued at $44.66, or 26% higher than it currently is.

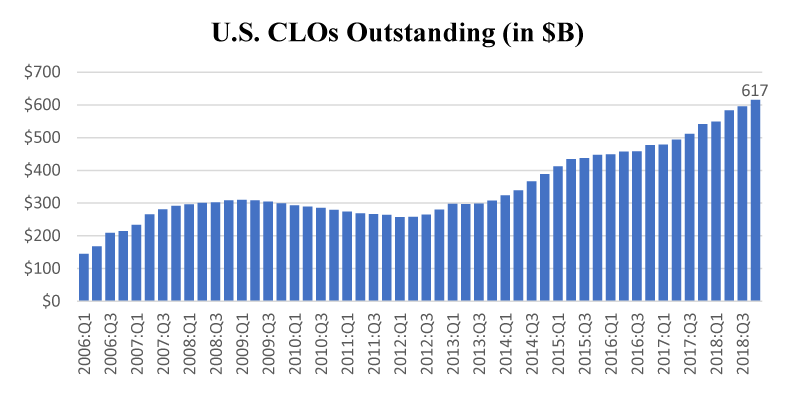

The Coming Alternative Credit Boom

This valuation, however, fails to address the Carlyle Group’s fastest-growing segment, which I believe will help separate Carlyle from the pack as real estate has done for Blackstone- with that segment being Global Credit.

As aforementioned, alternative credit is expected to become more popular with the declining continuity of traditional credit products. And Carlyle has captured this growth in their credit division- being a shining beacon during otherwise grim earnings seasons.

At the heart of Carlyle’s alternative credit strategy are collateralized loan obligations (CLOs), which are iterations of collateralized debt obligations, with a sustained focus on business debt rather than individual debt.

Alternative Credit Growth Pre-Covid (SIFMA US)

Carlyle both invests in and manages CLOs of a wide range- from higher yield, non-investment grade revolving credit facilities, to multi-tranche CLO derivatives and securities. And Carlyle’s deeply personal relationships and insights into partner firms’ operations mitigate default risk otherwise uninformed investors may experience.

To shield their portfolio from the volatility of such liquid credit, Carlyle offers both illiquid credit services- think direct lending, opportunistic, and distressed (of extra importance as of current)- as well as specialized credit the company has expertise in, such as aviation, infrastructure, and energy.

I believe Carlyle’s Q4 2022 report will continue to demonstrate the company’s tremendous growth in the arena of Global Credit.

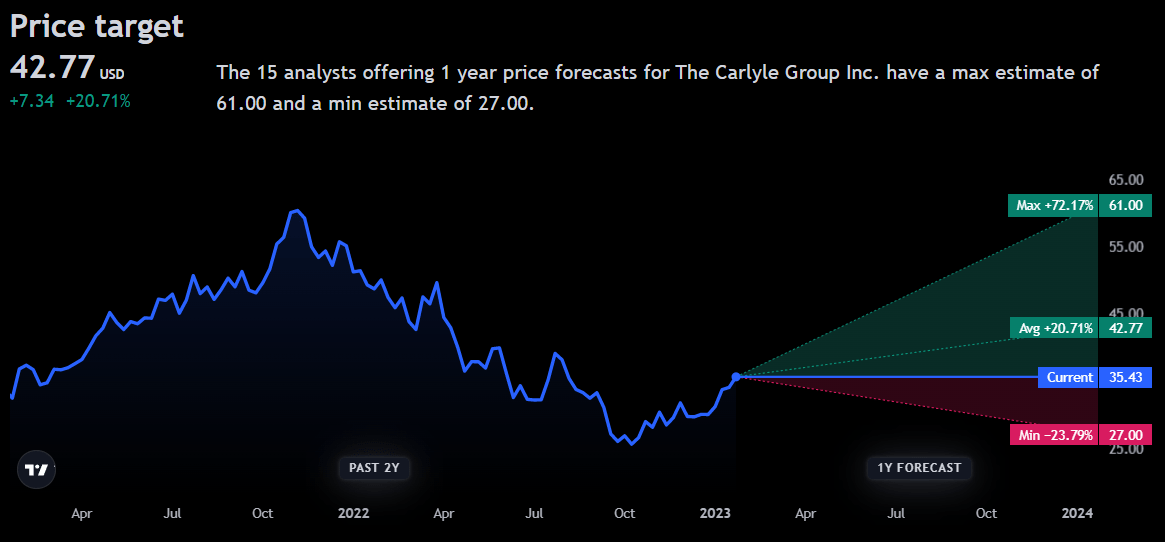

Wall Street Consensus

My positive view of the company is echoed by analysts, who forecast an average one-year price target of $42.77, up 20.71% from today.

tradingview.com

However, analysts also take note of the sensitivity of the company to macroeconomic events, pricing in a minimum projected price of $27 but also a 72% price increase to $61.

Risks

Terminally High-Interest Rates

A private equity firm first, Carlyle must contend with its ability to raise capital, which, in an increasingly fiscally and monetarily tight environment, may lead to greater expenses. Additionally, with a debt-equity of 1.24 (higher than competitors), Carlyle is highly leveraged, leaving it especially exposed to interest risk. The company has, though, put an onus on paying down debt, as debt-equity is down from 11.27 in 2019.

Geographic Expansion Risk

With Carlyle expanding to India and China, it will experience and must fortify itself against the political, regulatory, and economic risk that comes with it. This may include complying with minimum Tier 1 capital rules, trade restrictions, currency risk, intellectual property compliance, etc.

Investment Diversification Can Create Vulnerability

As I previously discussed, Carlyle is aggressively asserting itself in alternative credit, among other products. Particularly within liquid credit, this means exposure to complex derivative instruments which carry greater third-party risk than Carlyle’s traditional business. Financial failure in this arena may materially threaten the company.

Conclusion

In the short term, Carlyle’s chronic undervaluation, both compared to peers, and when considering their DCF valuation, and ability to adapt to a shifting macro environment, puts the company in a position to continue to outperform the market.

In the long term, I conclude that Carlyle’s focus on alternative credit in particular will not only enable them to experience significant margin expansion and sales growth but continue to appreciate at a price beyond that of peer companies.

Be the first to comment