Shares of Carlisle Companies Inc. (CSL) are down about 30% so far this year, and this move put the company on my radar. There’s much to like about this dividend superstar, in particular the fact that management was sanguine enough to stick to its “Vision 25” plan that calls for a doubling of revenues by 2025. I try to keep my articles as succinct as possible, and I try to keep the “padding” to an absolute minimum. “Padding” is all of those things that either should be known or are easily searched. Netflix is a streaming service that also creates content?! Dollar General is headquartered in Tennessee?! That said, I can understand if the reader doesn’t want to wade through my streamlined ~1,800 words of dense content. For those who were too impatient to read the title of this article and remain too impatient to read to the bottom of the article, I’ll jump right to the point. Although I really don’t like the share buyback program that investors have experienced over the past several years, I think the shares represent great value at these levels. I think sooner or later, stock price will rise to match stock value. For those who remain nervous after witnessing ⅓ of the value of this stock evaporate in a matter of months, I recommend selling the puts I write about below. If you want to know the specific options series I recommend selling, you need to read on.

Financial Snapshot

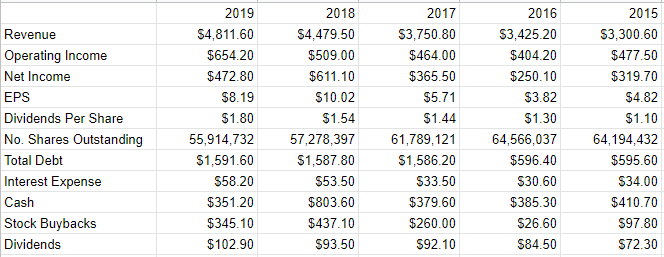

Over the past five years, the financial results here have been relatively impressive, in my view. In particular, revenue and net income have grown at a CAGR of about 7.8%, and 8.14% respectively. In addition, earnings per share have grown at a CAGR of 11% as a result of a large buyback program – more about that below. Also, dividends per share have grown at a CAGR of about 10.4% over the past five years. Frankly, I differ from some commentators who are more fawning about the excellent dividend track record here. I think management has not done a great job of treating shareholders well, given the size of buybacks relative to dividend payments over the past five years.

The Problem With Buybacks

As my regular readers know, I’ve grown skeptical of the value of stock buybacks, particularly in cases like this one, where the money spent on buying back stock dwarfs the level of dividends. Over the past five years, management here spent about $1.666 billion to buy back stock at an average price of $140.90. At the same time, the company returned just over $445 million to shareholders in the form of dividends. Had management not bought back a single share, that $1.666 billion could obviously have been spent on dividends. This would have returned an additional $18.17 per share in dividend income that investors would have enjoyed over the past five years. This compares to the $7.18 they actually did receive in that time.

Additionally, the $1.666 billion spent on buybacks could have also been used to completely eliminate long-term debt. Speaking of which, I’ve prepared a small table of scheduled debt repayments in the following table for your enjoyment and edification. This demonstrates to me that the debt is manageable, in my view, and I don’t think there’s a risk that debt payments will either crowd out growth in dividends. Specifically, the company has about $250 million of debt obligations coming due this year, but has cash on hand of about $351 million at the moment. Also, the timing for the next debt payment is two years out, and I hope the world economy would have largely recovered by then.

(Source: Latest 10-K)

(Source: Company filings)

In sum, I’d say that the financial history here is fairly good. The problem has been the money spent on buybacks. I’d rather the company actually returned that capital to owners than spend it on shares. In my estimation, the problem with buybacks is starkly revealed at times like this. If investors received that capital in the form of cash, they would have been objectively better off, in my view. That is a problem for shareholders of the past, though, and I’m interested in trying to determine whether it makes sense to buy at current prices or not. In order to do that, I’ll need to spend some time looking at the stock itself.

The Stock

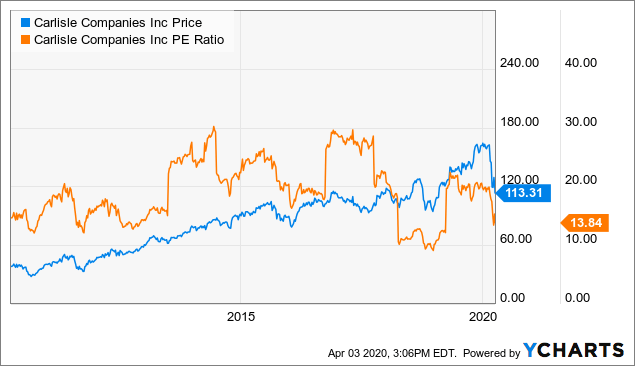

It’s all well and good for a company to generate decent cash flow for owners and to raise dividends over time, but in my view, the only way for investors to make money is by exploiting the disconnect between perceptions and reality. If the short-term perceptions about a company’s profitability are unrealistic, the shares can remain overpriced or underpriced for some period. Sooner or later, though, price and value will meet. For that reason, I want to try to identify whether the shares are too cheap or too expensive relative to value. I try to answer this question in a host of ways, ranging from the simple to the more complex. On the simple side, I look at the ratio of price to some measure of economic value. I think low P/E ratios, for instance, are both less risky and more apt to produce great returns going forward. I think a P/E ratio is “good” when the company is trading at a discount to the overall market and to its own history. At the moment, Carlisle is trading at a discount to the overall market and to its own history, which I consider to be a very positive sign.

Data by YCharts

Data by YCharts

In addition to looking at the simple relationship between price and some measure of economic value, I also want to understand what the market is currently assuming based on the current price. In order to do this, I turn to the methodology outlined by Professor Stephen Penman in his book Accounting for Value. In the book, Penman walks investors through how they can take a standard finance formula and, using the magic of high school algebra, isolate the “g” (growth) variable. This reveals to the investor what the market is currently assuming about the long-term (i.e., perpetual) growth at the company. Applying this methodology to Carlisle at the moment reveals that the market is forecasting a long-term growth rate of about 4.5%. Given the growth we’ve seen to date, I don’t consider this to be an excessively optimistic forecast. For that reason, I think the shares are reasonably priced at this point.

Options As An Alternative

While I think Carlisle is a good investment, I can understand the nervousness surrounding the name at the moment. It’s a strange twist of human nature that when anything other than stocks goes on sale, we buy more of it. When stocks go on sale, we eschew them because we assume the recent past will repeat. So, the people who see value here but are unwilling to buy at current prices have a choice. For one, they can wait for shares to drop in price. I’ve gone this route myself for years, and it is unendingly dull, mixed with a growing futility as shares remain elevated in price. The alternative is to sell put options at a strike price that makes sense to the investor. The strike price represents the price that the investor is obliged to buy the stock. If an investor likes this business and would be willing to buy at, say, $90, there’s no reason for them to not engineer that as a potential entry price. Alternatively, they may just collect premia.

At the moment, my preferred puts to sell are those that expire in September and have a strike price of $95. At the moment I type this, these are currently sporting a rather wide bid-ask spread of $5-11.20. If an investor simply takes the bid here and is subsequently exercised, they’ll be buying at a price about 21% below the current level. I consider that to be a less risky buy price than is currently on offer. Holding all else constant, that price represents a P/E multiple of ~11 and a dividend yield of 2.2%. I consider that to be a very decent entry yield for a company with this sort of dividend growth history.

In fairness, I should point out the risks associated with this strategy. Every investment comes with risks, and short put options are no different. I think the risks of put options are very similar to those associated with a long stock position. If the shares drop in price, the stockholder loses money and the short put writer will be obliged to buy the stock. Thus, both long stock and short put investors want to see higher stock prices. Also, some (though certainly not all) short put writers don’t want to actually buy the stock, they simply want to collect premia and move on. For these people, actually owning the stock is a problem. I should say that I’m not such a person. I’m happy owning stocks, but at a price that I deem acceptable.

In my view, put writers take on risk, but they take on less risk (sometimes significantly less risk) than stock buyers in the following way. Short put writers generate income simply for taking on the obligation to buy a business that they like at a price that they find attractive. This is an objectively better circumstance than the person who takes the prevailing market price for the shares. This is why I consider the risks of selling puts on a given day to be far lower than the risks associated with simply buying the stock on that day. Selling puts is analogous to receiving money for taking on the obligation to buy the stuff you were going to buy anyway, at a lower price than is currently on offer. There’s risk there, but it’s far less than simply buying, in my estimation.

Conclusion

I think Carlisle is an excellent business with an exemplary record of dividend increases. If I were a current shareholder, I’d be very unhappy that the company spent $1.66 billion to buy back shares at prices about 20% higher than the current price. I would have preferred that capital returned to me, and I could have come up with much more fun ways to spend it. Bushmills comes to mind. That said, the market is excessively pessimistic about Carlisle’s prospects, and I think that makes little sense in light of the longer-term positive drivers here. That said, just because I’m calling this a buy doesn’t make it so. For people who are still nervous about owning the shares, I advise selling the puts I recommend. I think these offer the best win-win trade available to investors at the moment.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in CSL over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: In addition to buying ~120 shares, I’ll be selling the puts mentioned in this article.

Be the first to comment