RelaxFoto.de

Introduction

There are a handful of companies in the mining industry that specialize in royalties and streaming deals, and I’ve covered one here on SA, namely Nova Royalty (OTCQB:NOVRF) here. This week I found out that a company named Carbon Streaming Corporation (OTCQB:OFSTF) had decided to apply this business model to carbon credits, which is an interesting idea. Furthermore, the company looks cheap at first glance as its market valuation is slightly higher than its cash position and much lower than its estimated net asset value (NAV). However, the burn rate is high, and a large part of the cash is committed to project payments. Let’s review.

Overview of the business and financials

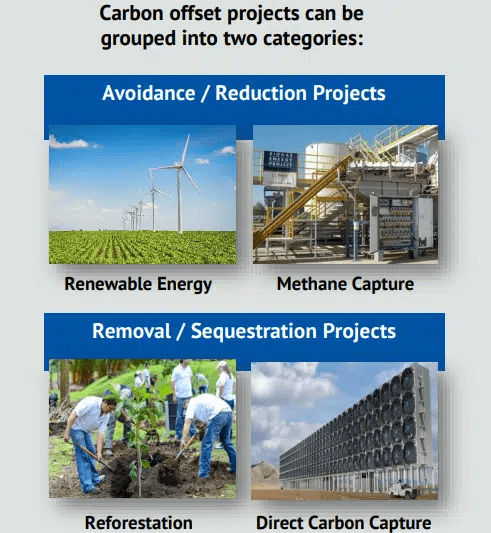

Carbon credits are also known as carbon offsets and represent work like permission slips for emissions. One carbon credit gives a company the right to generate one ton of CO2 emissions and those that have excess credits can sell them on the open market. The number of credits issued each year is usually based on emissions targets in the specific country and there are cap-and-trade programs across Canada, the EU, the UK, China, New Zealand, Japan, and South Korea.

carboncredits.com

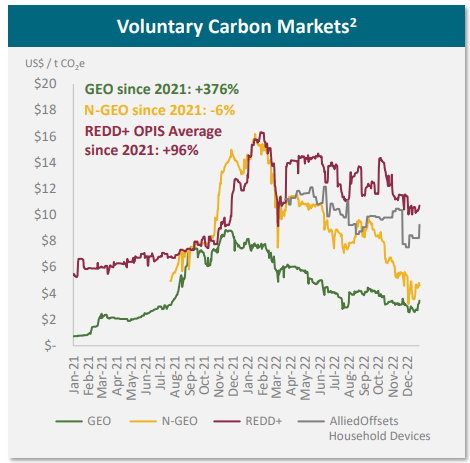

Carbon Streaming was founded in 2020 and is the only publicly traded carbon royalty company in the world. The company is listed on the NEO Exchange in Canada as well as the OTCQB in the USA. Its business includes entering into credit streaming arrangements with project developers and owners with the aim of accelerating the creation of carbon offset projects. The focus is on projects with a positive impact on the environment, local communities, and biodiversity. Carbon Streaming started raising money through capital increases in January 2021 and its maiden carbon credit streaming investment included a $6 million commitment to implement the MarVivo Blue Carbon Conservation project in northwestern Mexico which focuses on conserving and sustainably managing around 22,000 hectares of mangroves and 137,000 hectares of the marine environment. Under the deal, Carbon Streaming can buy the greater of 200,000 credits or 20% of the annual verified carbon credits from the project over a period of 30 years and it has to pay a sum equal to 40% of the net revenues from the sale of these credits. Considering REDD+ (Reducing Emissions from Deforestation and forest Degradation) carbon credits are trading at about $10 per ton, this project alone has the potential to generate annual gross profits of about $1.2 million.

Carbon Streaming

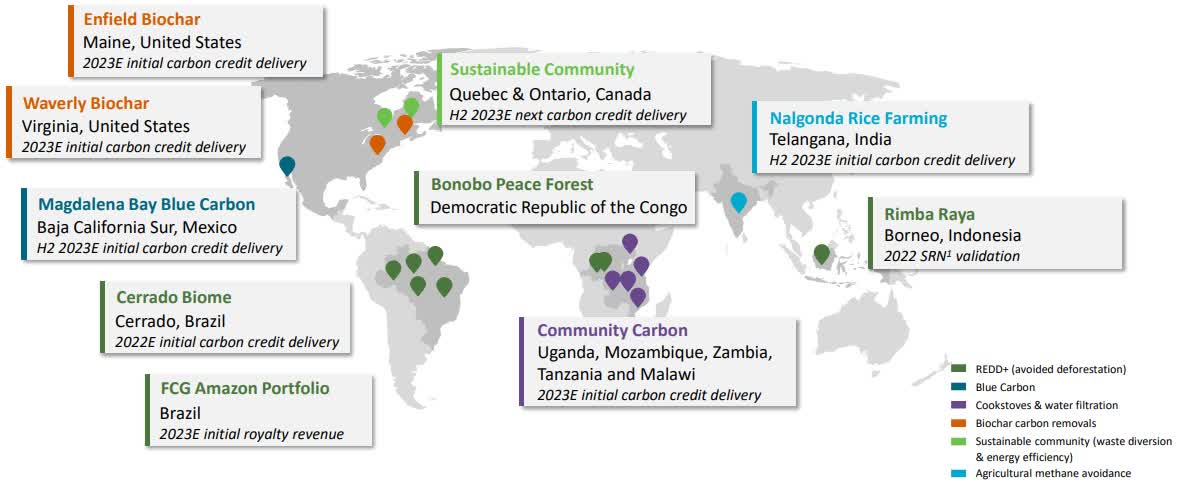

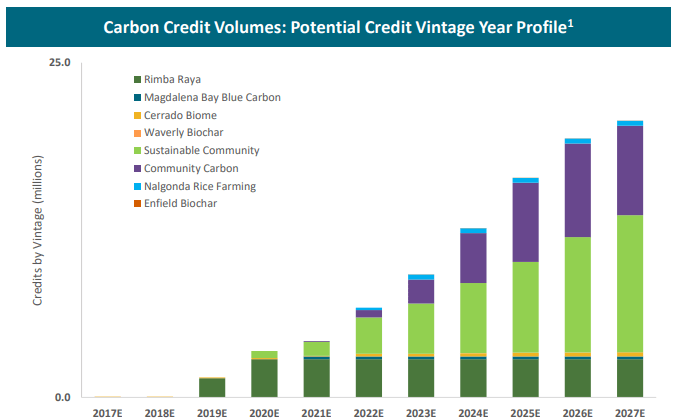

Today, Carbon Streaming has a portfolio of 21 carbon stream and royalty projects in 12 countries across the world. Many of those projects revolve around the distribution of fuel-efficient cookstoves and water filtration devices, waste avoidance, energy efficiency, methane avoidance in agriculture, and biochar carbon removal. A total of 10 of those projects are expected to issue credits in 2023.

Carbon Streaming

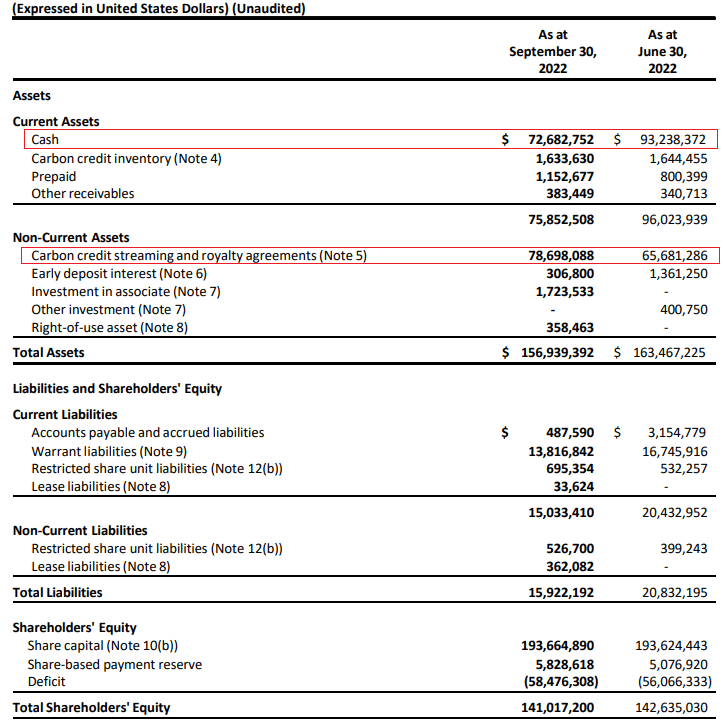

Looking at the Q3 2022 financial results, the book value of Carbon Streaming’s carbon credit streaming and royalty contracts was $78.7 million. In addition, the company had $72.7 million in cash while its market valuation stands at just $82.6 million as of the time of writing.

Carbon Streaming

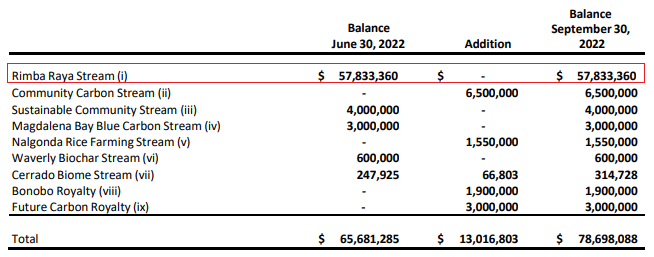

Looking through the portfolio, the largest book value by far is linked with the Rimba Raya Biodiversity Reserve REDD+ project in Indonesia which covers an area of 64,000 hectares of bio-diverse tropical peat swamp forest. It helps the world avoid around 130 million tonnes of carbon emissions.

Carbon Streaming

In April, Indonesia’s government credit issuances were put on hold due to regulatory concerns. However, the Rimba Raya project was validated by Indonesia’s carbon registry in December which puts Carbon Streaming back on track to rapidly grow revenues. According to the company’s latest corporate presentation, its NAV according to S&P Capital IQ consensus estimates is about $205 million (see slide 23).

Carbon Streaming

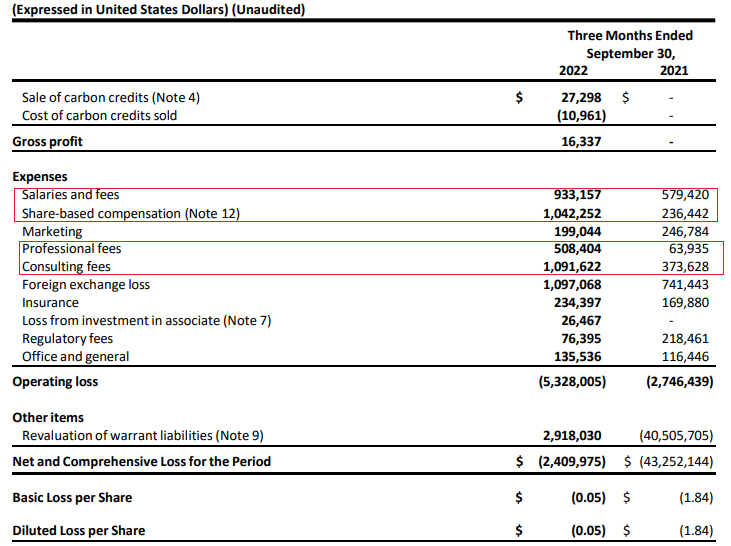

However, Carbon Streaming generated revenues of just $27,298 in Q3 2022 as it sold down a part of its inventory. I find it concerning that SG&A expenses are growing rapidly as the quarterly expenses on salaries, and professional and consulting fees came in at $3.6 million.

Carbon Streaming

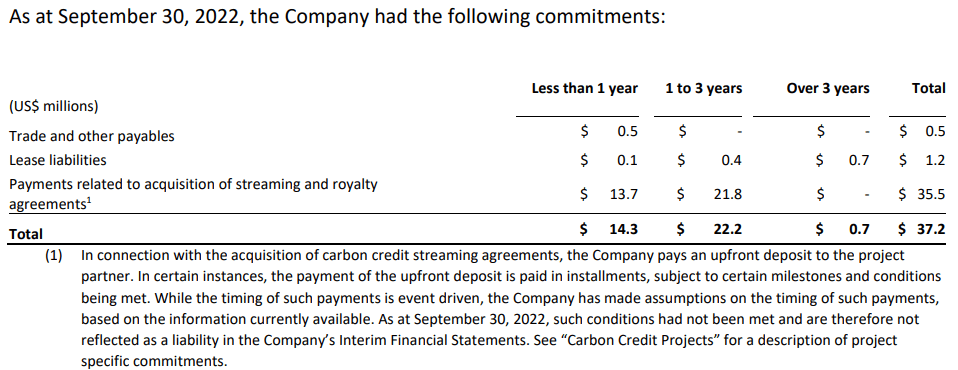

While the company had $72.7 million in cash as of September, it’s important to note that Carbon Streaming had payment commitments of $36.5 million over a period of up to 3 years. In addition, the company mentioned during its Q3 2022 earnings call that it had probably over 100 projects in its pipeline.

Carbon Streaming

I’m concerned that if there are delays in any of the major projects in the portfolio, there could be significant stock dilution. This is usually among the major risks for pre-revenue companies, and I prefer to stay on the sidelines at least until free cash flow becomes positive. Let’s see if this can happen before the end of 2023.

Investor takeaway

Carbon Streaming provides investors a way to invest in carbon credit streams and is trading at about 0.4x NAV based on consensus estimates. This seems cheap but you have to keep in mind that the company has not yet seen significant deliveries of credits from any of the 21 projects in its portfolio and that a large portion of its cash is committed to project payments. This year is set to be transformational for Carbon Streaming as several of its projects are set to issue credits and the gap to its NAV could close up if everything goes smoothly. However, keep in mind that once issued, credit sales take place over the following 12-month period and delays or regulatory issues like the ones experienced by Rimba Raya could lead to significant stock dilution.

Overall, I think Carbon Streaming looks undervalued based on fundamentals, but I’d prefer to invest in it in a more mature stage when risks are diminished. In my view, it’s best for risk-averse investors to avoid this stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment