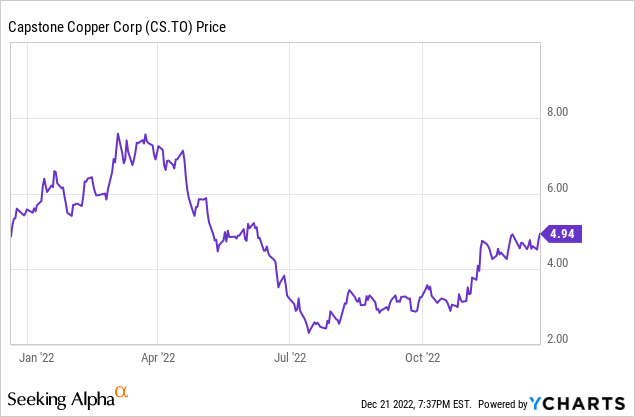

I have been following Capstone for a while now but I wasn’t very happy when Capstone Copper (TSX:CS:CA) (OTCPK:CSCCF) acquired Mantos Copper in an all-share deal, but I understand the appeal of merging both companies as Capstone will now likely produce in excess of half a billion pounds of copper from 2024 on. While the operating costs on the Chilean operations are pretty high now and the operations are free cash flow negative, the MVPD expansion (which should be completed in 2024) should more than double the production while cutting the C1 cash cost per produced pound of copper in half.

Q3 wasn’t great as the impact of provisional pricing was clearly felt

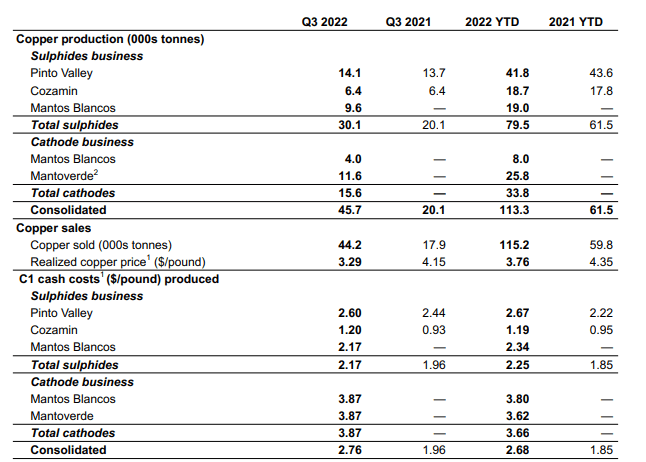

During the third quarter, Capstone produced approximately 45,700 tonnes of copper (approximately 100 million pounds) and sold roughly 44,200 tonnes of copper (just under 100 million pounds) at an average realized price of $3.29 per pound.

Capstone Copper Investor Relations

Unfortunately the operating costs were pretty high on a consolidated basis, mainly because of the Mantos Blancos and Mantoverde cathode operations which had a total average C1 cash cost of $3.87 per pound. The Pinto Valley and Cozamin operations had a C1 cash cost of $2.60 and $1.20 respectively.

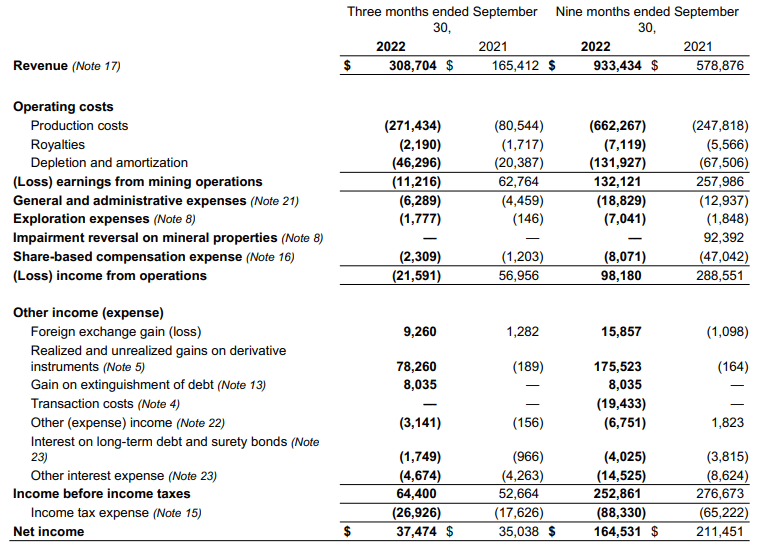

Despite this, the company reported a pre-tax income of $64.4M thanks to a $9.3M FX gain, a $8M gain on the extinguishment of debt and a $78.3M gain on derivatives (mainly related to the copper and FX hedging contracts). There’re two reasons why the normalized pre-tax income was negative. First of all, the company recorded in excess of $46M in depreciation and depletion expenses while the company also had to deal with the provisional pricing mechanism which had a very negative impact on the average realized copper price during the quarter.

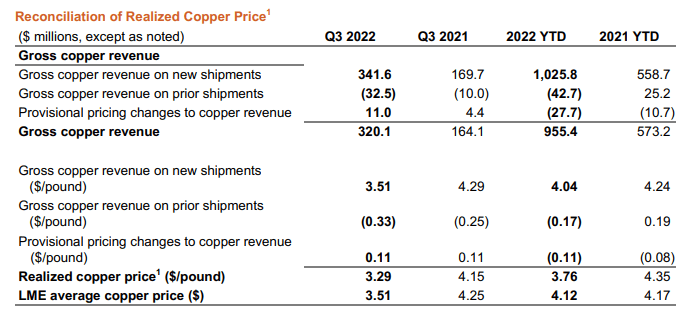

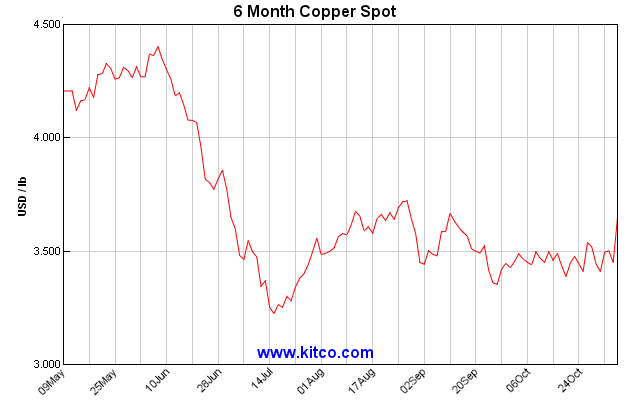

As you can see below, the average realized copper price was just over $3.50 but there was a net charge of $0.22 per pound related to the provisional pricing changes.

This phenomenon is easy to explain: a base metals company needs to record the revenue the moment the concentrate leaves its property. But most commercial offtake agreements include a settlement date on the day the buyer actually takes delivery of a concentrate shipment. And if the copper price starts to decrease between the moment the concentrate leaves the mine gate (or the port) and the moment the buyer takes possession of the concentrate, an adjustment needs to be recorded. That goes unnoticeable if these changes occur within the quarter but are a bit more complicated when a shipment leaves Lundin in Q2 but arrives in Q3. Just to give you a theoretical example: if company XYZ would ship 10 million pounds of copper on June 20 when the price isroughly $4/pound, company XYZ will record a $40M revenue.

Kitco Metals

But as you may remember, the copper price started to decrease in June and July. And as you can see in the image above, the copper price dropped below $3.50 in the first week of July. So if the shipment in our example would have arrived at the buyer when the copper price was $3.50, the revenue shouldn’t have been $40M as initially recorded by company XYZ, but just $35M as the copper price upon arrival is what matters.

As a company cannot attribute that $5M loss to the second quarter, it basically takes an ‘impairment charge’ in the third quarter: that’s what the ‘prior period adjustments’ are. And that works both ways.

Capstone generated about $14M in operating cash flow before changes in the working capital position and after making lease payments and interest payments, there wasn’t a whole lot of available operating cash flow. So it’s perfectly understandable why some investors aren’t too impressed with the current market cap of approximately C$3.5B (approximately US$2.5B), but as you may have guessed by now, there’s more than meets the eye here.

Where to go from here?

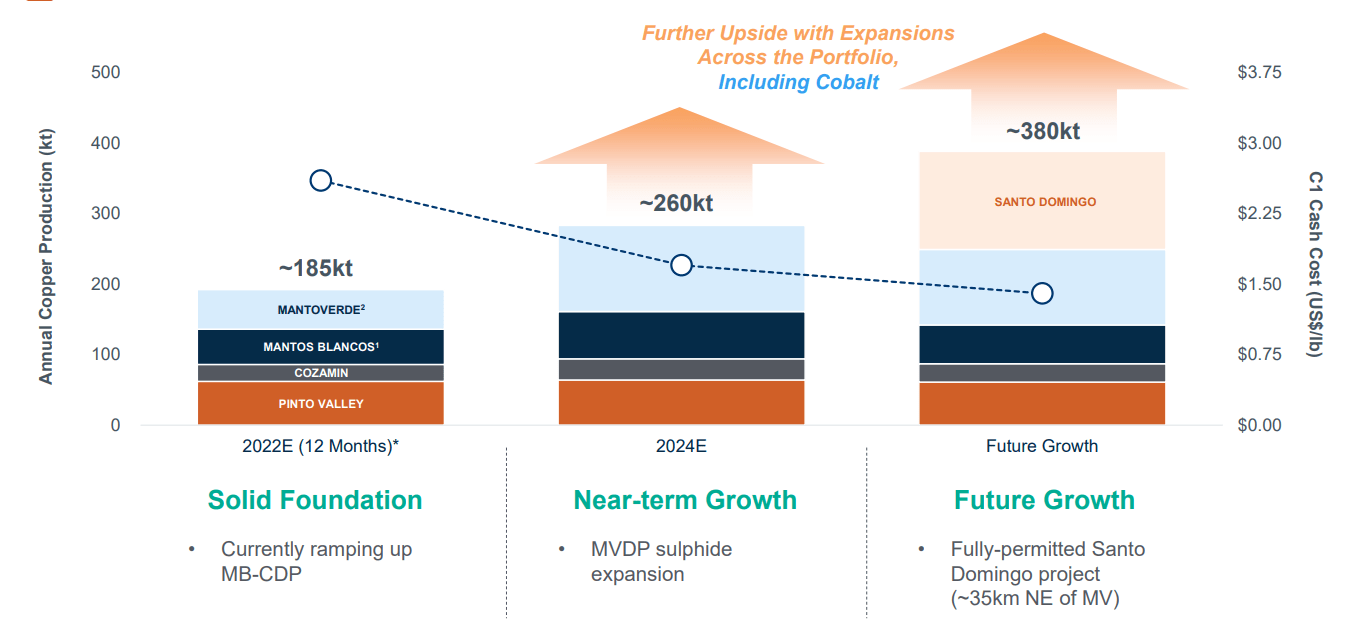

While I wasn’t the biggest fan of the decision of Capstone Mining to acquire Mantoverde Copper, I do have to acknowledge it will be the main driver to push the copper production higher. While Capstone Mining will produce about 185,000 tonnes of copper (just over 400 million pounds) in the current financial year, it is aiming to push the production rate to 260,000 tonnes (in excess of 570 million pounds) in 2024 when the MVDP sulphide expansion will be completed.

Capstone Copper Investor Relations

The MVDP expansion will allow the company to process an additional 235 million tonnes of copper sulphide reserves during a 20 year mine life (thanks to the construction of a 12.3 million tpa concentrator) which would provide a meaningful addition to the current Mantoverde production rate. The current production rate at Mantoverde is approximately 49,000 tonnes of copper per year and this will increase to 120,000 tonnes per year in a combination of concentrate and cathode. The C1 cash cost will decrease substantially from the current (very high) $3.6-3.80 per pound to less than $2.00 per pound, which emphasizes how important the MVPD completion is for Capstone Copper. The additional gold production of approximately 31,000 ounces of gold per year will also be a welcome by-product revenue.

I have no position in Capstone Copper as I was initially pretty unhappy with the Mantos Copper deal, and earlier this year I missed the buying opportunity as the share price fell by approximately 70% in just four months. I am keeping an eye on the stock as I do think the demand for copper will continue to increase while it has become increasingly difficult for producers to keep up. Not a whole lot of projects will turn into new mines within the next decade so I think it might be better to stick with producers and Capstone Copper is nicely positioned as a mid-tier producer with an anticipated 30% production growth in 2024.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

{kind=link}

Be the first to comment