shells1

Overview

Capstone Copper (OTCPK:CSCCF) is an Americas-focused copper mining company with its headquarters in Vancouver, Canada. The stock is listed in Canada (TSX:CS:CA) and the reporting currency is U.S. Dollars.

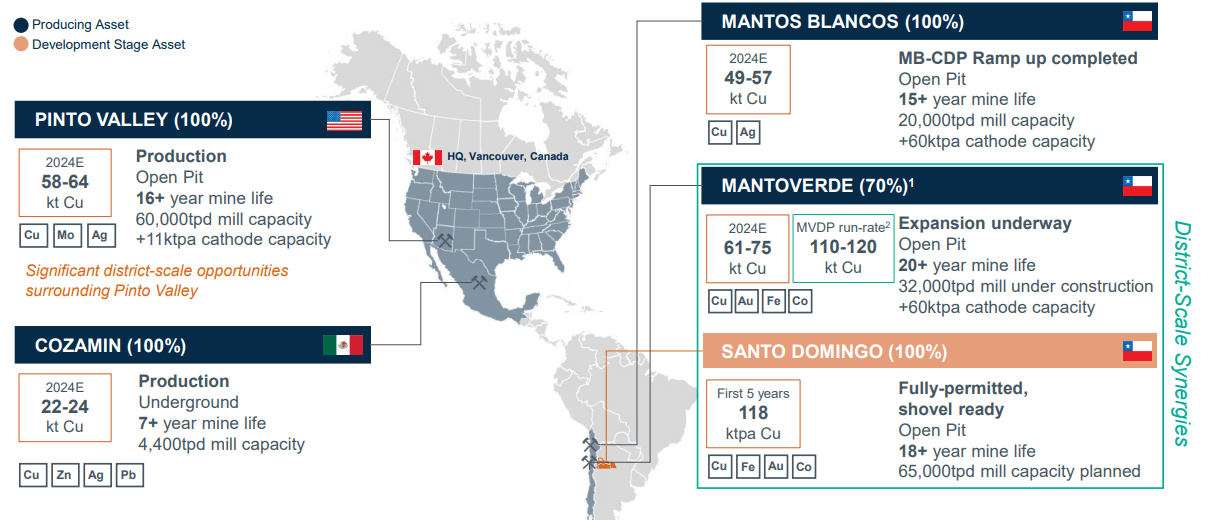

Figure 1 – Source: Corporate Presentation

The company owns the Pinto Valley copper mine in Arizona, USA, the Cozamin mine in Zacatecas, Mexico, and the Mantos Blancos mine in the Antofagasta region, Chile. Capstone also owns 70% of the Mantoverde mine in the Atacama region, Chile and 100% of the fully permitted Santo Domingo development projected nearby. The various mines have very good reserves, where most mine lives are in the 15-20-year range.

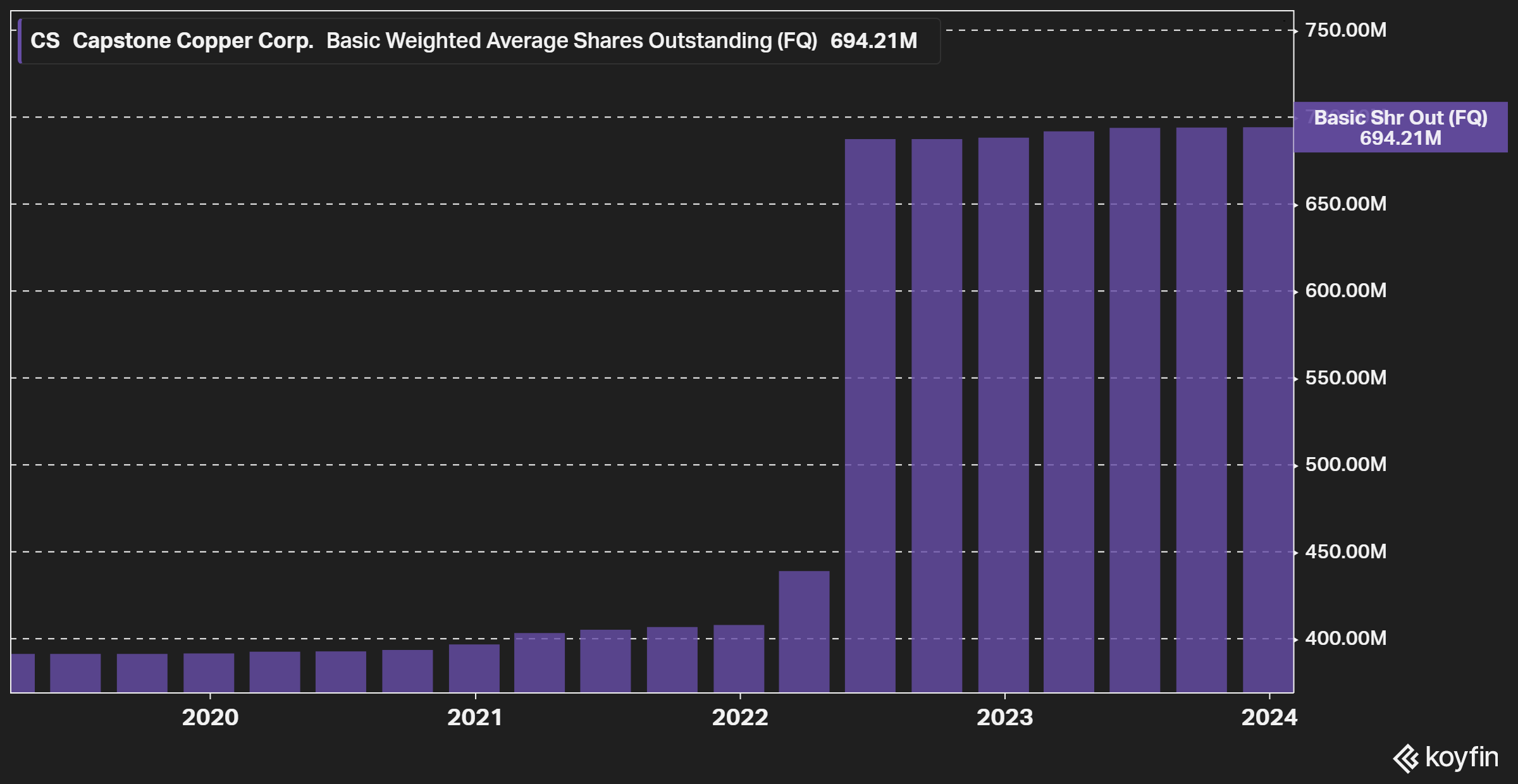

The name Capstone Copper was taken in 2022, following the completion of the merger between Capstone Mining and Mantos Copper, which is also the reason why the share count increased substantially back then.

Figure 2 – Source: Koyfin

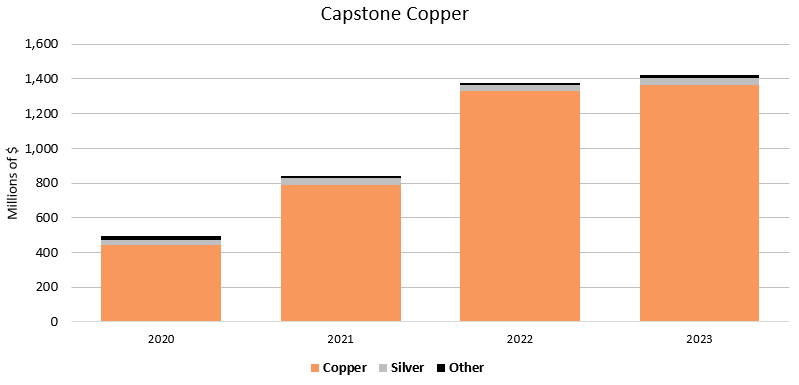

In 2023, Capstone got about 3% of revenues from silver and 1% from other metals, but as much as 96% of revenues were from copper. So, Capstone is a more copper-focused producer than many of its peers.

Figure 3 – Source: Quarterly Reports

Financials

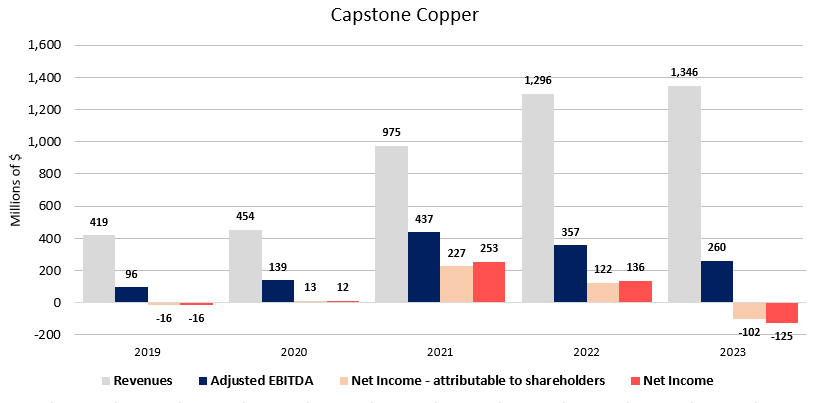

The financials for 2023 were released a month back and Capstone Copper reported $1,346M in revenues for 2023, and an adjusted EBITDA of $260M, and net income attributable to shareholders was negative $102M. Adjusted net income attributable to shareholders was better in 2023, around $0. Like most copper mining companies, we saw a more substantial profit in 2021 due to stronger copper prices, but the company has otherwise had a relatively small profit margin over the last few years.

Figure 4 – Source: Quarterly Reports

Capstone has, despite relatively minor profits over the last few years, invested heavily in growth projects and in 2024 it’s expected to see a substantial increase in production, where most of the growth will come from the Mantoverde Development Project (“MVDP”).

The MVDP is an expansion project of the Mantoverde mine, with an estimated project cost of $870M, that will allow Capstone to process sulphide ore in addition to the mine’s current oxide ore processing capabilities. It is scheduled to reach nameplated capacity in the second half of 2024.

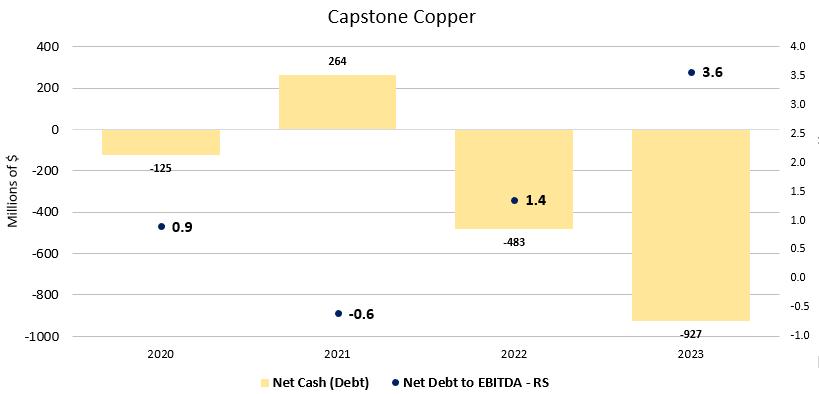

In the chart below we can see that the growth investments have stretched the balance sheet substantially lately. A couple of years ago, the company had a positive net cash position, but at the end of 2023 it had a net debt position of $927M.

Figure 5 – Source: Quarterly Reports

The 2023 net debt to adjusted EBITDA was as high as 3.6. Now, the EBITDA is expected to improve substantially in 2024 from higher production and lower costs, so the forward-looking leverage ratio is much better. The company has also raised approximately $253M in net proceeds in February, via bought deal, which will primarily be used on growth projects.

The near-term focus for Capstone is organic growth, so the company doesn’t pay a dividend or buy back shares. Investors should in my view not expect this focus to change any time soon given the financial leverage and organic growth opportunities.

2024 Guidance

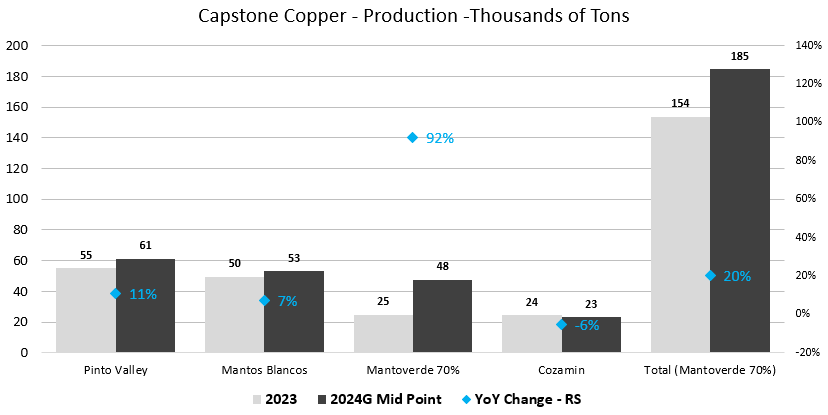

The below chart illustrates the copper production guidance for 2024 compared to 2023. I would point out that the company has not provided any sulphide guidance at Mantoverde during the first half of the year, due to the ramp up. So, the full year production guidance for Mantoverde could consequently be slightly conservative provided the ramp up goes according to plan.

Figure 6 – Source: Company Press Release

Capstone is expected to see 20% year-over-year growth in copper production during 2024 where most of that will come from Mantoverde, but Pinto Valley and Mantos Blancos are also expected to have healthy production growth of 11% and 7%.

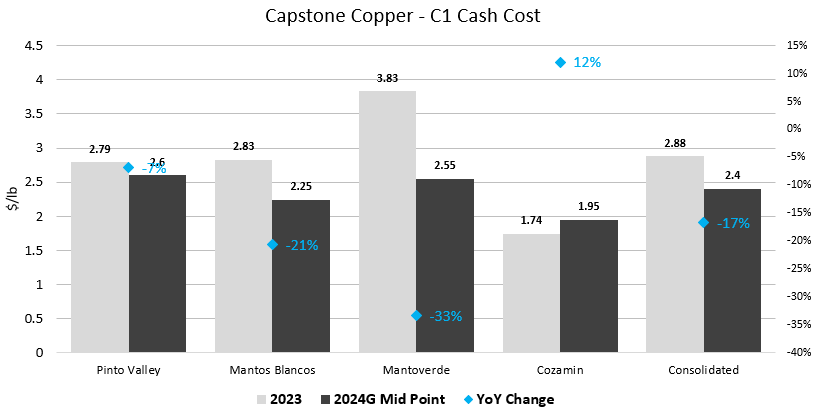

In 2024, we can also expect substantial improvements on the cost side, where consolidated C1 cash cost is expected to decrease by an impressive 17% to $2.40/lb. Like the production side, the company is guiding for improvements for Pinto Valley, Mantos Blancos, and Mantoverde, while costs are expected to increase at the Cozamin mine in Mexico.

Figure 7 – Source: Company Press Release

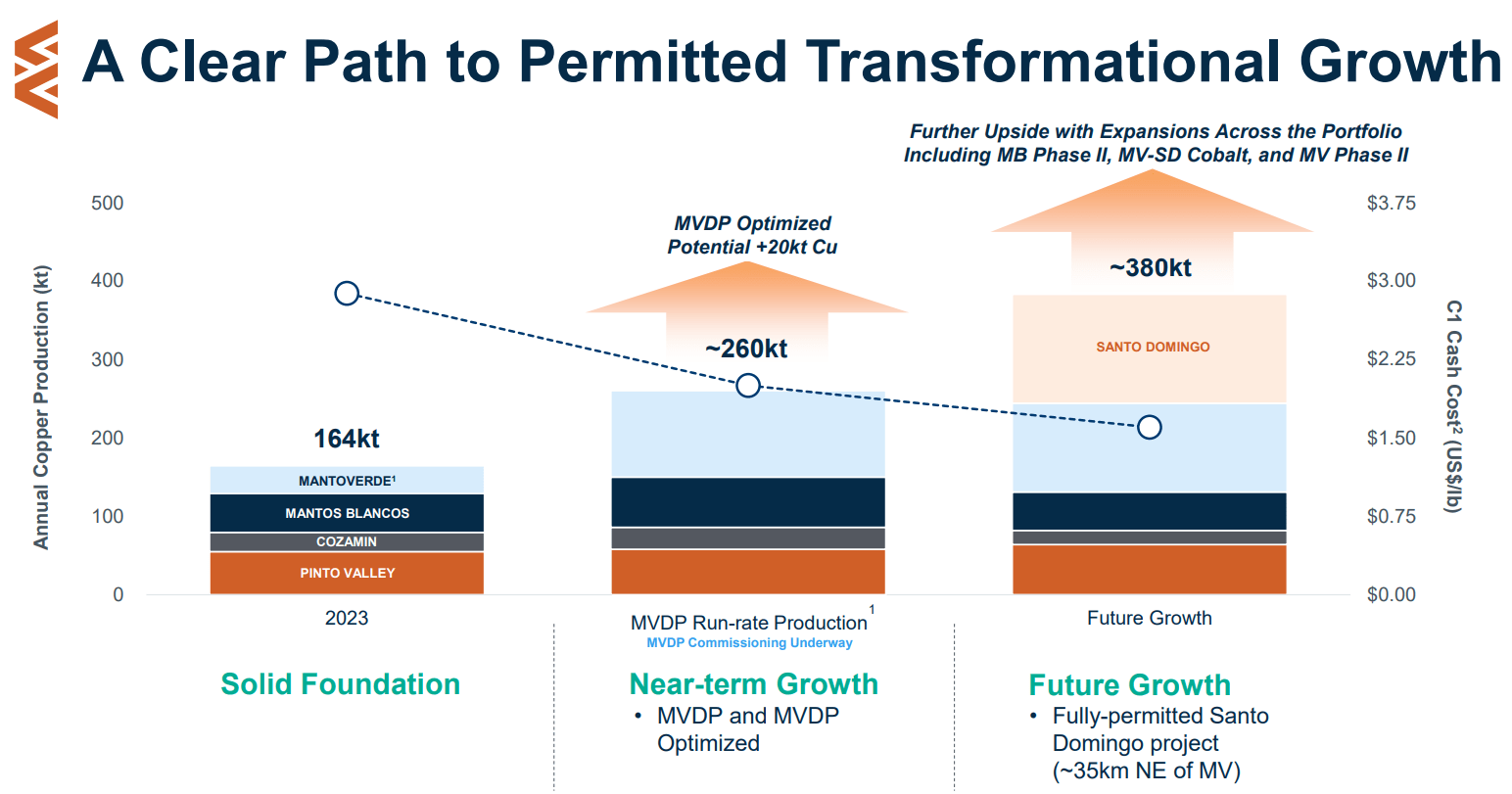

These improvements in 2024 are extremely encouraging, with substantially higher production and lower costs. However, there is more production growth ahead for Capstone, which is expected to further decrease operating costs. 2025 will be the first year with a full year of nameplate production from Mantoverde and we will likely get more clarity on the Santo Domingo timelines over the next year or two.

Figure 8 – Source: Corporate Presentation

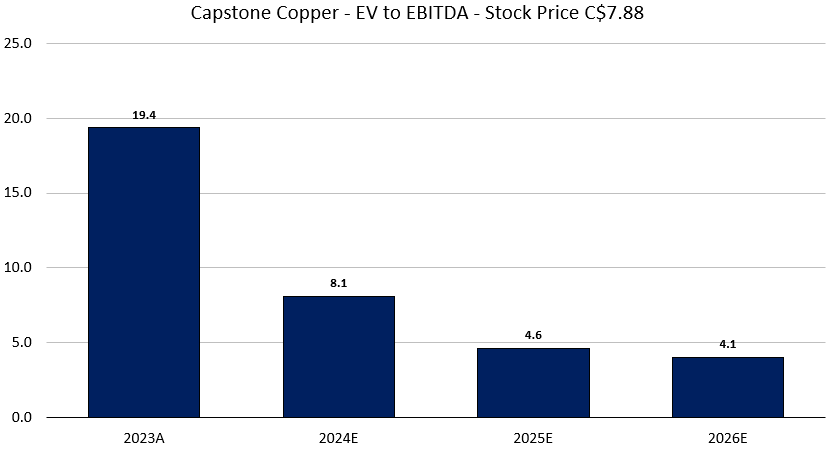

Valuation & Conclusion

For the valuation, I have used the latest share price of C$7.88 and the financials as of Q4 2023. Note that the share count and net debt have been adjusted with the figures from the February bought deal. Based on those inputs, the market cap of Capstone is at $4.4B and the enterprise value is $5.0B.

Figure 9 – Source: Koyfin

If we use the 2023 EBITDA, Capstone is anything but cheap, but the 2024 EBITDA is expected to increase substantially due to the increased production, lower costs, and possibly higher copper prices which we have seen recently. Looking further out to 2025, the valuation is starting to look even more appealing, with an EV to EBITDA of 4.6.

The company does have some debt, but I don’t think financial leverage is as much of a concern as it might look at first glance, due to the higher EBITDA going forward and recently completed bought deal. However, there is still some execution risk getting Mantoverde up to nameplate capacity, which should not be completely dismissed.

Another concern is the new Chilean tax reform, as Capstone will have just over 50% of 2024 copper production in Chile, and likely more in the future. The new tax reform looks to be manageable for most companies in the region, but it is not a positive development, and at least I am always a little bit concerned that more will follow if we see a price spike in copper prices. However, given that this reform took a while to get implemented, it is more of a minor concern in my view.

Overall, Capstone Copper is a very interesting copper mining company with a lot of organic growth ahead. The valuation is relatively attractive if we look out to 2025. With that said, given that the stock price has had a nice run lately and there is still some execution risk remaining, I am in no rush to chase the stock here and would need a more pronounced pullback to go long.

Figure 10 – Source: Koyfin

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment