Manakin

Here at the Lab, in 2022, we had mixed feelings about Capri Holdings (NYSE:CPRI). At the start, we were not very optimistic and in our initiation of coverage, we provided a neutral view with a publication called ‘On Hold For Now‘; however, after having analyzed the company’s Q1 results development, we decided to increase our internal estimates with an overweight valuation. Our buy rating was supported by a deep dive into the fashion luxury sector, a stock price derating, a “turnaround” story from Jimmy Choo and Versace brands, and also the higher guidance provided by the management teams. Today, after the third quarter release, Capri Holdings’ stock price is down by almost 25% and we are back to where we were before.

Mare Evidence Lab’s previous publication

Before analyzing Capri Holdings’ negative key takeaways, we report the CEO’s words – he specifically declared that was disappointed with the performance of the company’s “global wholesale business in the quarter which resulted in expense deleverage and a lower operating margin”. He also explained how Q3 sales were “more challenging than anticipated”. Looking at the detail, it is important to emphasize the following:

- The group’s top-line sales decreased by 6% to $1.51 billion versus last year’s results. As anticipated, luxury brands such as Jimmy Choo and Versace declined less than Michael Kors;

- Adj EBIT margin stood at 15.6%, below management expectations and Wall Street analyst consensus. As a reminder, 2021 operating margins were at 20.6%;

- Capri Holdings’ income from current operations delivered a plus $236 million versus the $331 million recorded in the prior year;

- Key to note is the net inventory evolution which reached almost $1.2 billion with an increase of 21% on a yearly basis. We suggest to our readers check our previous Puma publication called “Implications Of Nike’s Profit Warning“;

- Net income was down by 30% compared to last year’s results and as a consequence, the company’s adj. EPS notched $1.84, below the average consensus of more than $0.40.

Capri Holdings financials in a Snap

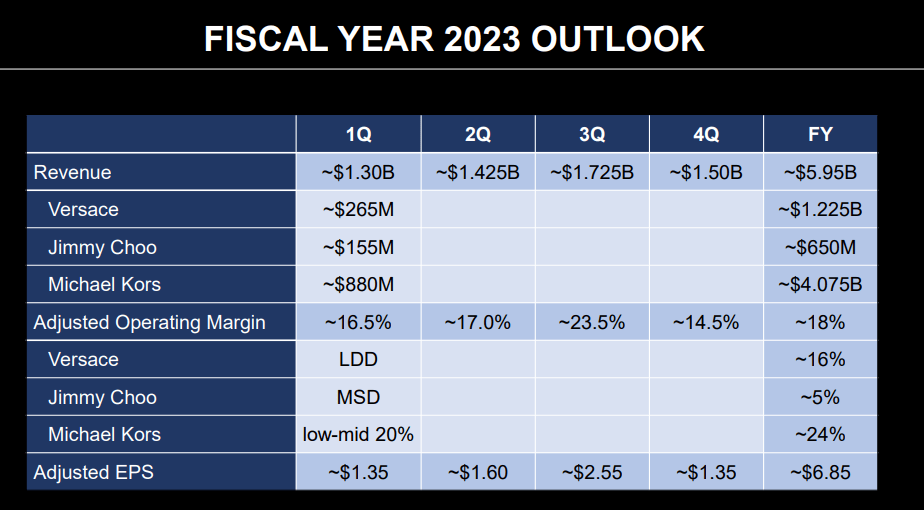

Aside from the negative financial results, looking at the 2023 guidance, reversing Capri Holdings’ outlook, Q4 sales are expected to hit $1.2 billion. This is a significant negative result compared to last year’s sales and equity research forecasts. Reversing the Q4 outlook, we also expect margin pressure that will hit Capri Holdings’ operating leverage with an estimated EPS of $0.92 compared to the previous indication of $1.35. Looking at the aggregate level, 2023 turnover is anticipated to reach only $5.56 billion. The CEO was more confident in the 2024 Fiscal Year. He explained how “Capri Holdings will generate mid-single-digit revenue and earnings growth“. He remains “confident in Capri Holdings’ ability to achieve our long-term goals over time due to the resilience of the luxury industry, the strength of luxury houses portfolio, and the talented group of employees executing our strategic initiatives“.

Capri Holdings previous 2023 outlook Capri Holdings’ current outlook

Conclusion and Valuation

Last time, in our conclusive paragraph, we were guiding for an Earning per Share estimate of $6 which was below management’s expectation. With this number, we derived a target price of $74 based on a historical P/E average. This was also supported by a new share repurchase plan of up to $1 billion. During Q3, Capri Holdings repurchased shares for a value of $300 million. We believe that Wall Street is overreacting to Capri Holdings’ release, and despite a negative 2023 outlook, here at the Lab, we were already guiding an EPS forecast below the company’s consensus. Capri Holdings is also forecasting a lower adjusted operating profit margin of 16.5% from 18%, and applying a 20% discount on its historical P/E estimates (at 14x based on the last 5 years’ average), we still value the company at $67 per share vs. the current trading at $48. Therefore, we confirm our buy rating target.

Be the first to comment